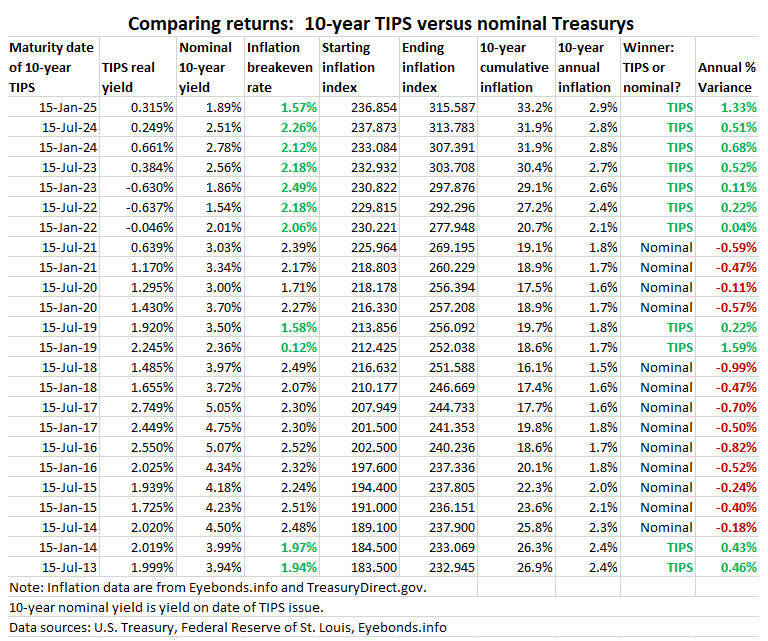

In a few days, CUSIP 912828H45 – a 10-year TIPS that originated at auction on Jan. 22, 2015 – will mature. This was a ho-hum TIPS that came to life at a strange time in the U.S. bond market.

At the originating auction, it got a real yield to maturity of 0.315% and an inflation breakeven rate of 1.57%. At the time, a 10-year Treasury note had an ultra-low nominal yield of just 1.89%, well below today’s 10-year real yield of about 2.34%.

In my preview article for that auction, I noted intense volatility in the U.S. Treasury market. I wasn’t a fan and I wasn’t a buyer.

So at this point, with the auction a week away, it appears this new TIPS issue will get a coupon rate of 0.250% and a real yield (after inflation) a bit higher than that. A year ago, a 10-year TIPS went off with a yield of 0.661% – about 37 basis points higher.

Now, 10 years later … that very low inflation breakeven rate made CUSIP 912828H45 a very attractive investment, at least compared to the nominal 10-year Treasury of the time. Annual inflation over the next 10 years averaged 2.9%, well above the breakeven rate of 1.57%. This TIPS absolutely walloped the comparable Treasury note by 133 basis points a year.

The final investment results for this TIPS were set by the November inflation report issued Dec. 11. Data from Eyebonds.info show this TIPS generated a 10-year nominal annual return of 3.241%, crushing the comparable Treasury note at 1.89%.

OK, 3.24% may not seem like much, but keep in mind that the 10-year nominal Treasury yield didn’t didn’t reach 3.0% from January 2015 until fall 2018, and that was a brief period before slipping below that level again until spring 2022.

As a reader pointed out in the comments, over the last 10 years Vanguard’s Total Bond ETF (BND) has had an annual total return of 1.14%. Total return of the TIP ETF was 1.93%, and VTIP (shorter-term TIPS) was 2.51%, all below the 10-year average inflation rate.

For its time, CUSIP 912828H45 was a very good investment, with the widest gap over a 10-year nominal Treasury since I started tracking this auction data in 2013.

TIPS versus an I Bond

If you purchased an I Bond in January 2015, it had a fixed rate of 0.0%, below the real yield of this TIPS at 0.315%. According to Eyebonds.info, that I Bond will have generated an average annual return of 2.85% as of July 2025. So again, the TIPS was the superior investment at 3.241%.

However, the I Bond has outperformed the 10-year nominal Treasury.

Thoughts

TIPS have been on a winning streak for several years, caused by the surge to 40-year high inflation that peaked in June 2022 at 9.1%. Even today, annual inflation is running higher than the auctioned breakeven rates of 2015. And so TIPS have been the winners versus nominal Treasurys in recent years.

My chart is an estimate of performance comparing inflation breakeven rates versus actual inflation.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

As I have noted many times in recent months, I believe there are changes coming in TreasuryDirect’s “gift box” program, which creates a loophole for buying I Bonds beyond the $10,000 per person annual limit for people with a trusted partner.

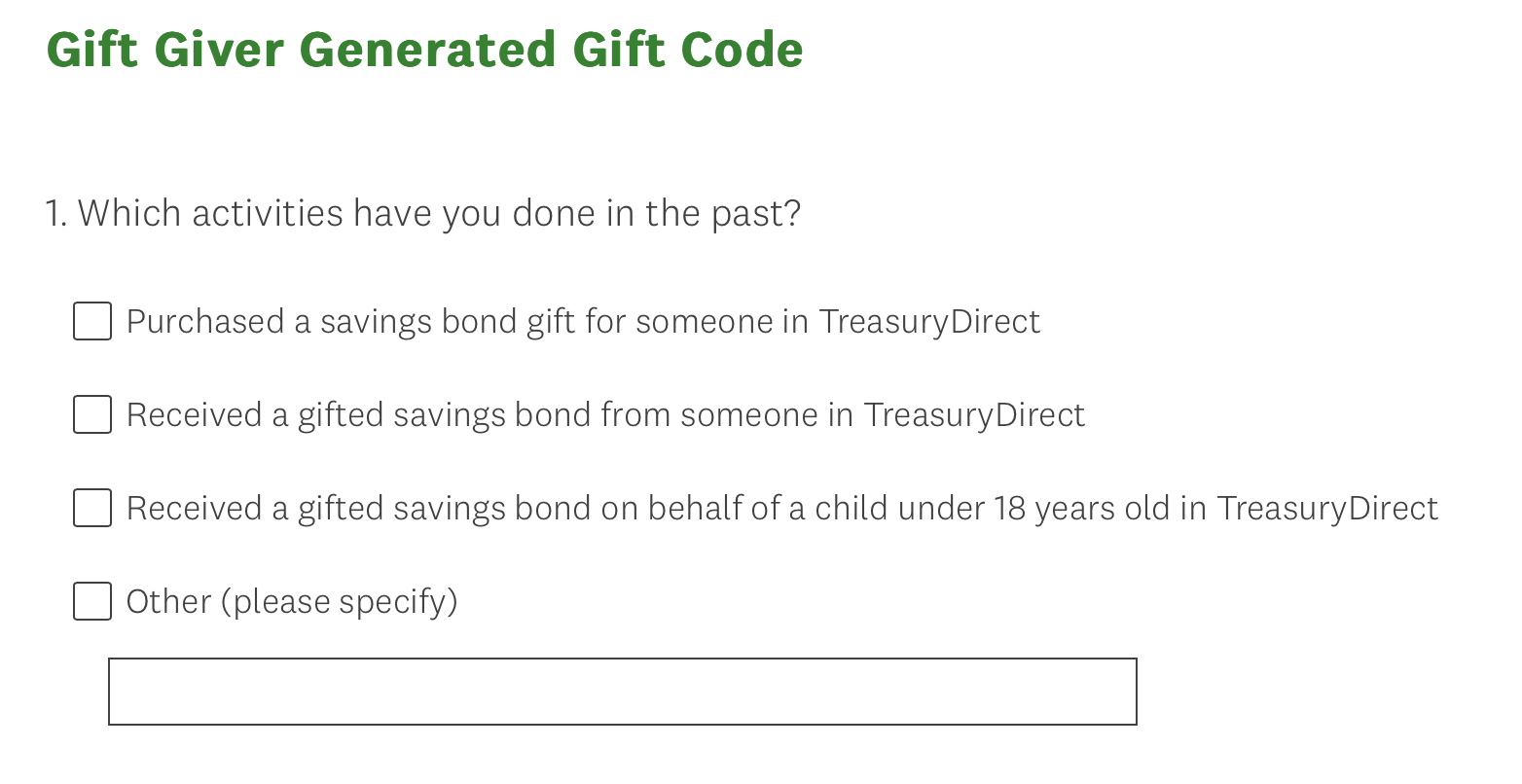

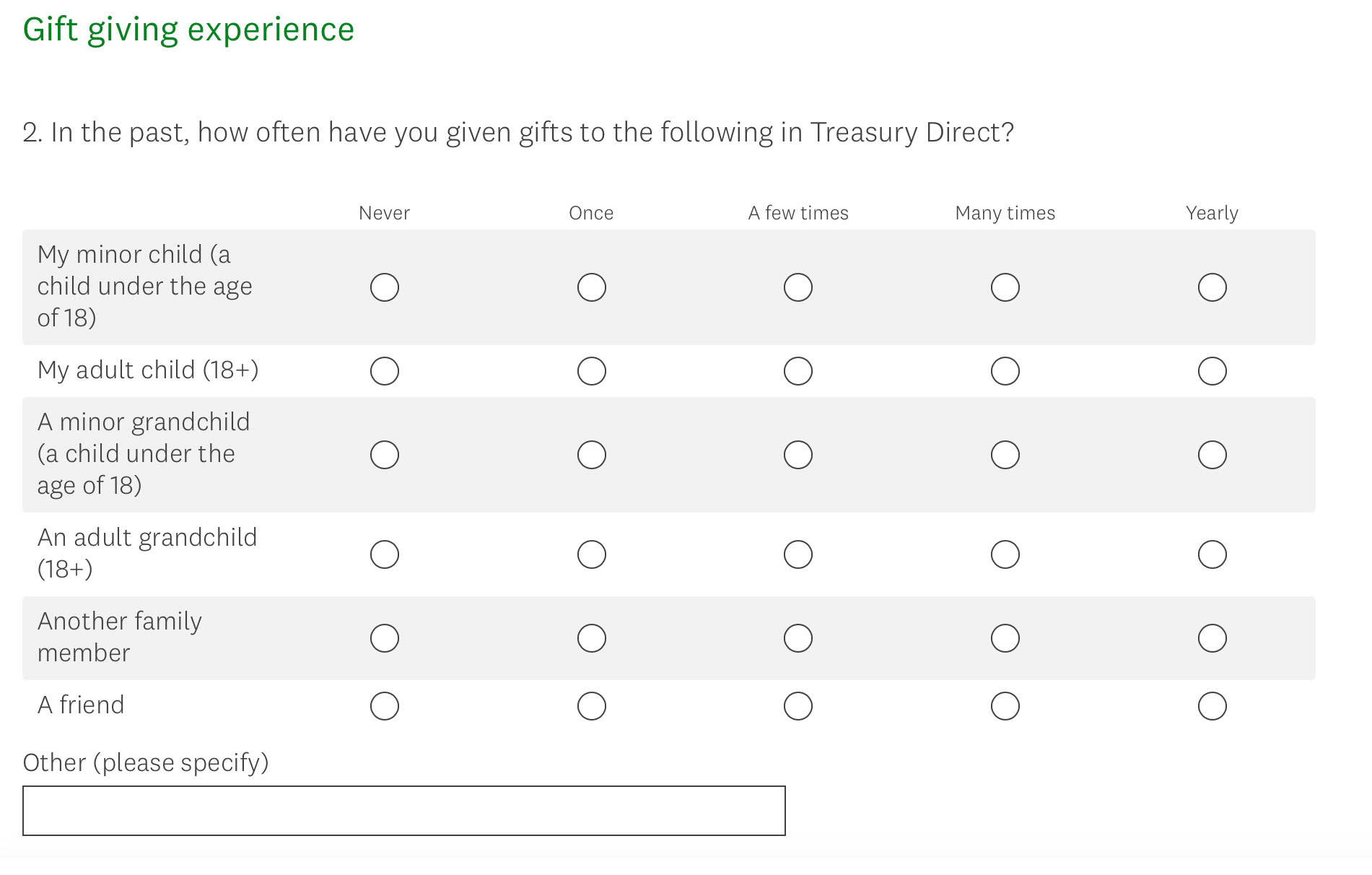

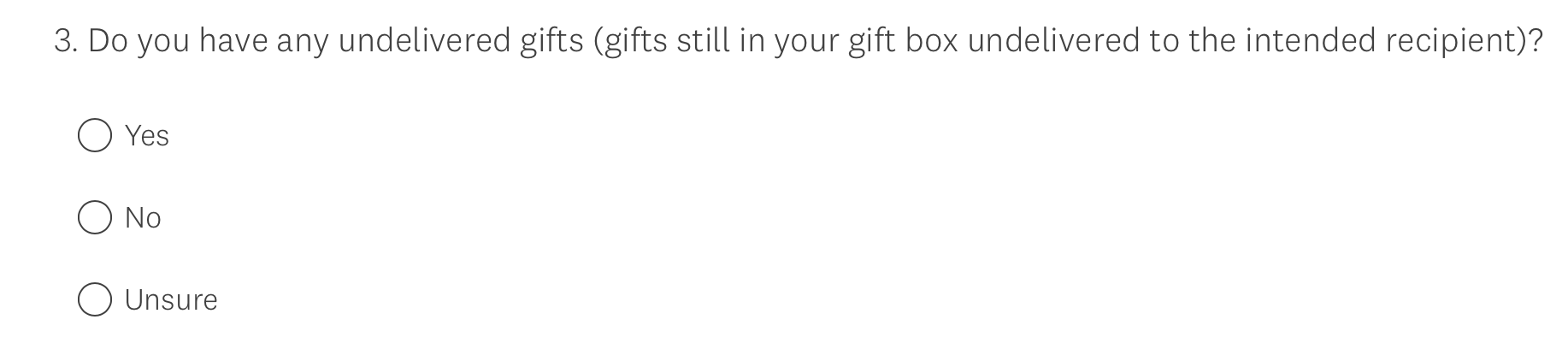

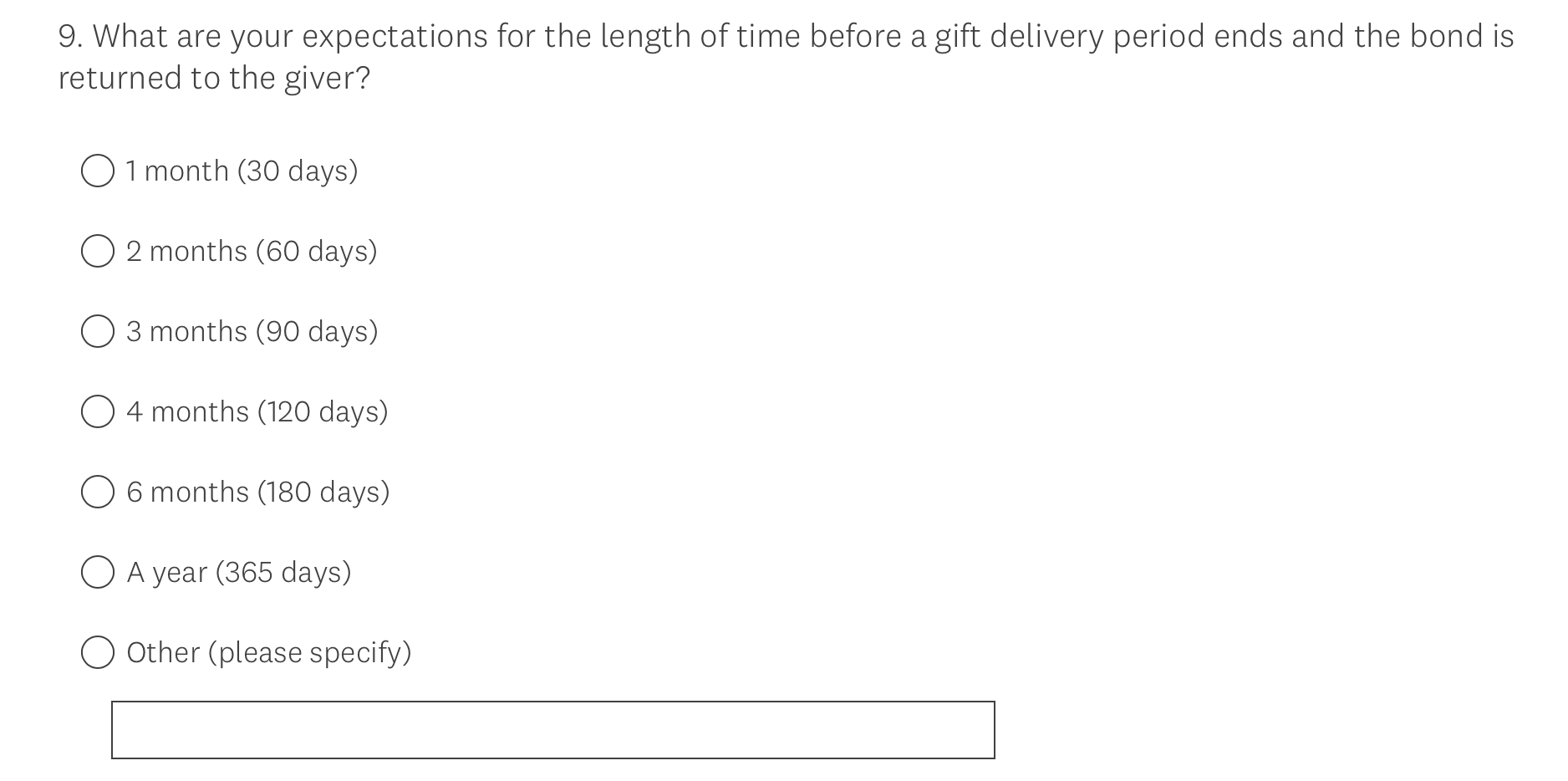

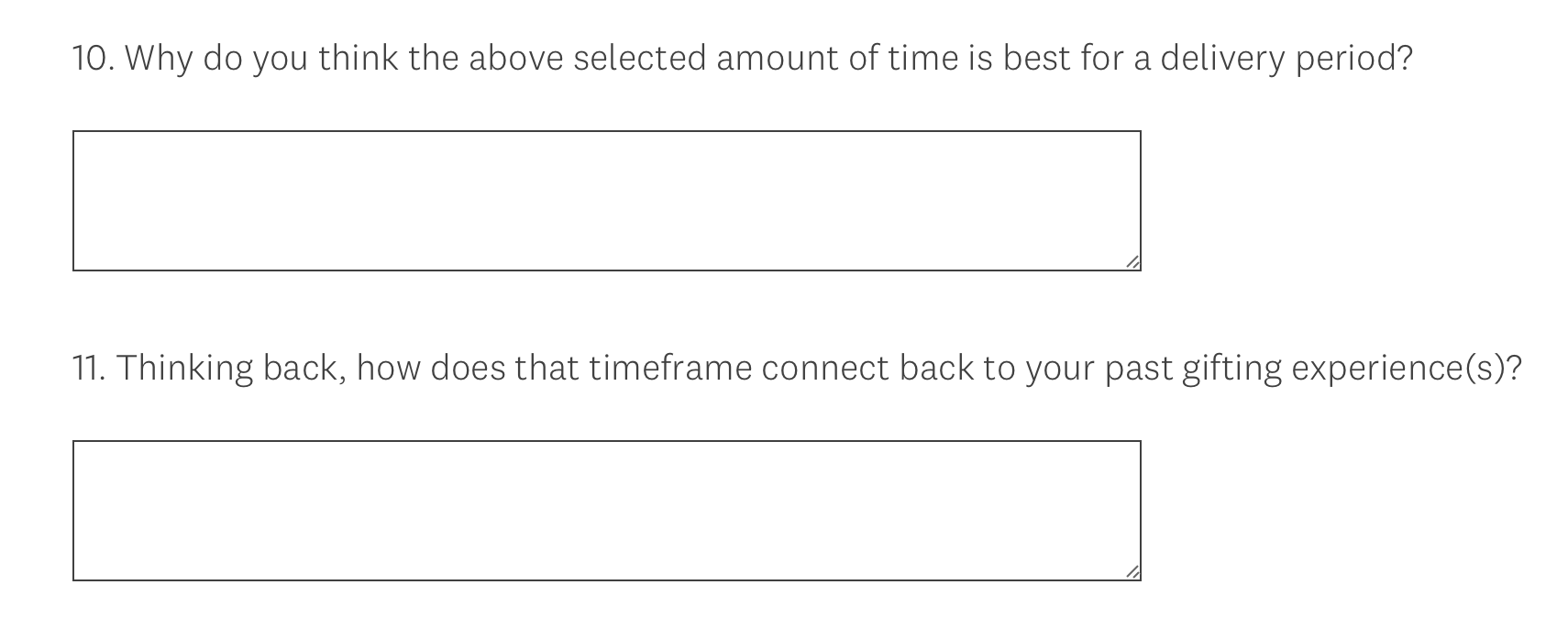

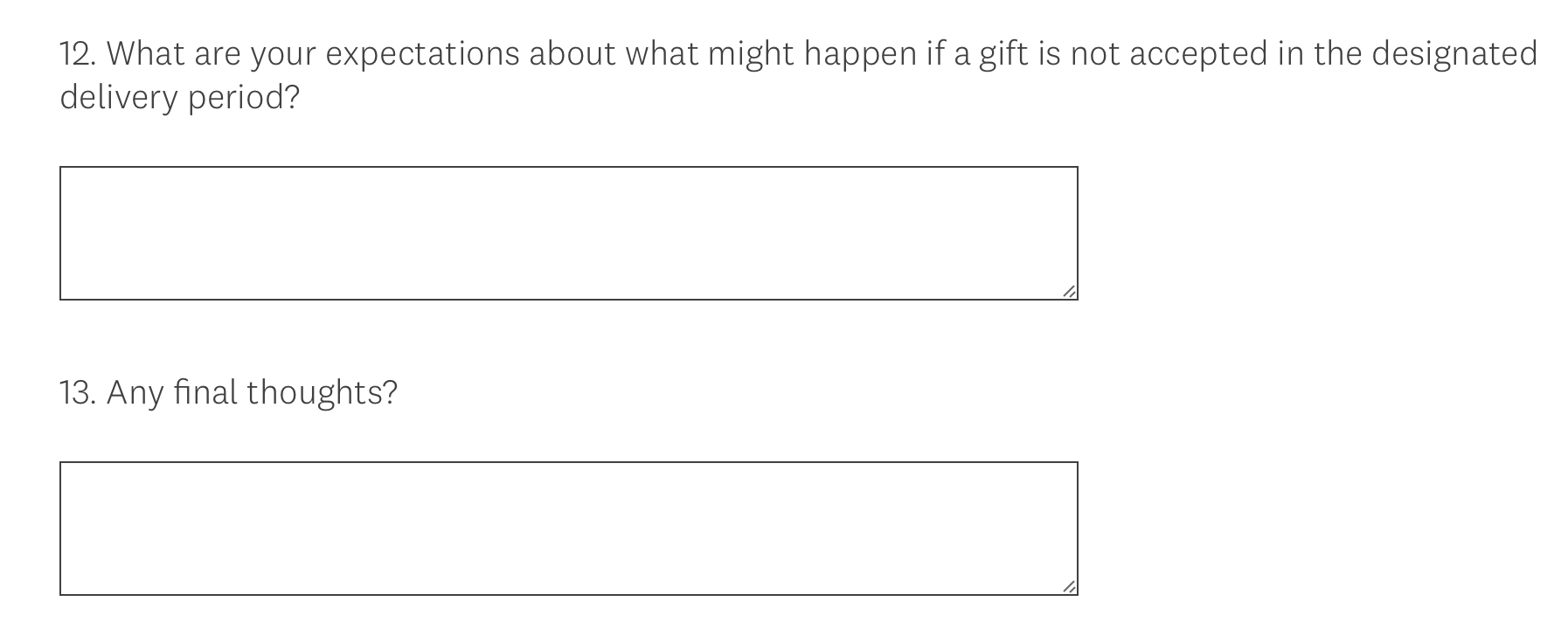

Today, TreasuryDirect began sending out an email asking investors to participate in a survey about the gift-box program. If you haven’t received the email, I am presenting the questions here for all of us to analyze:

Thoughts

I am still pondering what this means, but the core issue in the survey seems to be a new time limit on delivering bonds from the gift box. (There is no time limit now, and I Bonds in the gift box continue earning interest until delivered, possibly years in the future.) Some investors, I know, do not want a time limit, because these bonds are to be delivered to a child at some time in the future.

The Treasury has stipulated in the past that a gift box item is no longer the property of the giver. It can only be delivered to the recipient, who is actually the owner. But this survey seems to imply that savings bonds that aren’t delivered within some time frame (possibly up to a year) would be returned to the giver.

Returning the savings bond to the giver opens up another set of issues, but that’s too confusing to ponder with this limited information. As one Bogleheads commentator noted minutes ago:

That sounds like it’s opening up the door to gift yourself, which would be nice for unmarried people like me.

The survey also focuses on potential problems with gift-box bonds being accepted after being delivered, possibly because the recipient is unaware of the gift or does not have the required TreasuryDirect account.

And the survey really tells us nothing about the issue of using the gift box to add to holdings in a single year, bypassing the purchase limit if you have a trusted partner, such as a spouse. That’s the loophole I think should be closed, while at the same time raising the purchase limit to $20,000 per person per year.

I’m confused, but I’ve only had a few minutes to think about this. The discussion is now open. Join in with thoughts in the comments section. I will follow up with more information if I learn anything. Many thanks to readers who sent me alerts.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Update, Jan 31, 2025: I noted in this article that I was going to make a “test” I Bond purchase in January 2025 to see if it would trigger a purchase limit because of gift box deliveries in 2024. The transaction was scheduled for Jan. 29 and the money was withdrawn by the Treasury on that date. A day later, TreasuryDirect showed the I Bond in the account, dated Jan 1 2025. So it all worked without a hitch.

——-

I’m a big fan of all those Agatha Christie Poirot books, Sherlock Holmes, Philip Marlow, every episode of Columbo on TV. But even those great detectives would have a hard time figuring out TreasuryDirect.

“Just one more thing.”

So now we enter a new year, and the annual $10,000 per person purchase cap for U.S. Series I Savings Bonds has reset. But one big question remains for many investors: Can I buy I Bonds this year? And for others: When should I buy I Bonds this year? Or even … Why invest in I Bonds at all?

Just a reminder: An I Bond is a U.S. Treasury security that combines a permanent fixed interest rate with a six-month variable rate, creating an inflation-protected return. They can only be purchased in electronic form at TreasuryDirect.

Can I buy this year?

TreasuryDirect created a lot of confusion in October when it sent an email to investors holding I Bonds in a “gift box” for later delivery. The email seemed to urge delivery of those I Bonds “as soon as possible.” The email was strange, but it was authentic.

The gift box program is a widely used loophole that allows people with a trusted partner (such as a spouse) to expand their purchases of I Bonds beyond the $10,000 per person limit. The idea in early 2024 was 1) buy gift I Bonds now to lock in the attractive 1.3% fixed rate, and then 2) deliver them in future years when the fixed rate is lower.

We all assumed one thing: You could not deliver gift I Bonds to anyone who had already purchased up to the limit in that year. TreasuryDirect’s email threw that assumption out the window. I called TreasuryDirect to try to get an explanation, and so did hundreds of my readers and fellow Bogleheads. We learned (unofficially):

TreasuryDirect would like you to deliver gift I Bonds as soon as possible.

It would be OK to deliver I Bonds to a person who had already reached the purchase cap.

And … maybe (or maybe not) … the person receiving I Bonds over the limit would be locked out of buying I Bonds in future years, depending on the amount delivered.

Unspecified “changes” may (or may not) be coming to the savings bond program.

In my case, last year: 1) My wife and I each bought one set of 1.3% I Bonds early in the year, along with two sets each for the gift box. After getting the Treasury’s directive, we successfully delivered those gift box purchases in November 2024.

Now it is January 2025 and I am ready find out: Am I subject to a purchase limitation this year? The answer apparently is “no.”

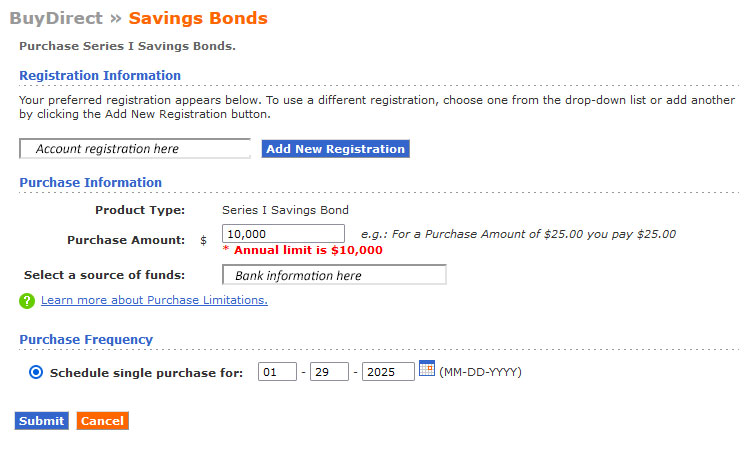

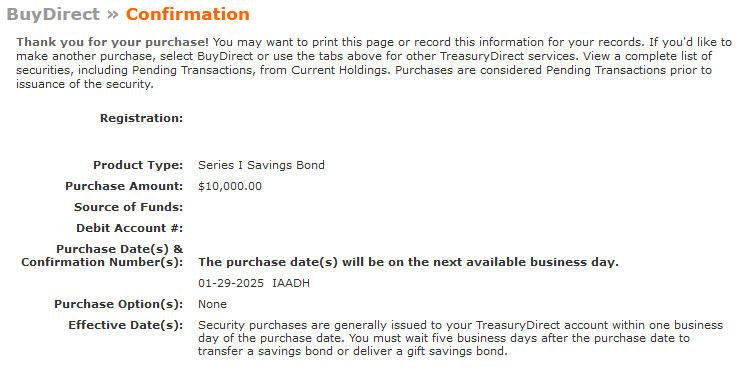

Last week, I logged into TreasuryDirect to place an I Bond order for my wife’s account:

Everything here is totally normal. Note that I set the purchase date for Jan. 29 because I Bonds earn interest for an entire month, no matter the day they are purchased. I clicked “submit,” looked at the review page and clicked submit again.

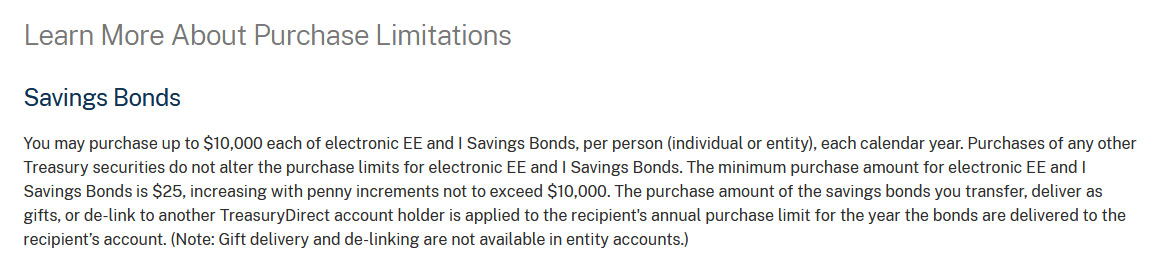

Again, totally normal. No warnings. No alerts. I think this purchase will go through on Jan. 29 as a routine transaction. Also, on the BuyDirect page, I noticed a link to “Learn more about Purchase Limitations.” I clicked and found this:

Click on image for larger version.

Notice this key wording: “The purchase amount of the savings bonds you transfer, deliver as gifts, or de-link to another TreasuryDirect account holder is applied to the recipient’s annual purchase limit for the year the bonds are delivered …”

My translation: If you receive $10,000 in gift I Bonds before you make your regular $10,000 purchase, you will not be able to buy more that year. But … if you make your regular purchase first, you can receive additional gift deliveries that year.

Important takeaway: If you are planning to deliver gift I Bonds this year, make sure to purchase your regular allocation before any delivery. Then, it appears, the gift I Bonds can still be delivered.

Also: If you made gift I Bond deliveries over the limit last year, you won’t be locked out of making a regular purchase in 2025. This is NOT official, but it is what I and others have experienced.

When should I buy I Bonds this year?

Although I set up a purchase for Jan. 29 to test my purchase theories, my usual advice would not be to buy in January, unless you feel the need to get the one-year-to-redemption clock ticking.

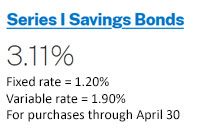

The current I Bond will pay 3.11% nominal for six months. You can do 100 basis points better in a decent money market account or high-yield savings account, for the time being. So there is no rush. Instead, be patient. I Bonds are a long-term investment.

April 10, 2025. We will get the March CPI report at 8:30 a.m. EDT, which will lock in the I Bond’s new six-month variable rate. We will also have a lot more information on whether the fixed rate will be likely to rise at the May 1 reset.

The period from April 10-28 is an ideal time to make a decision: Buy in April or buy in May, or continue waiting?

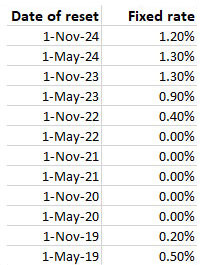

At this point, it looks possible the I Bond’s fixed rate could increase at the May 1 reset. For that to happen, using our back-of-the-envelope theory, the 5-year TIPS real yield would need to average at least 1.92% from November to April. That would get you back to 1.3%. At this writing, the 5-year TIPS is yielding 1.97%.

We won’t know until later this year. It is smart to wait. The variable rate is not a key factor in this decision, unless you want to make a short-term investment. The fixed rate is much more important for a long-term investor.

Oct. 15, 2025. The September inflation report will be issued on this day, locking in the next variable rate, and by then we will have information on the fixed rate reset coming Nov. 1. So the period from Oct. 15-29 is another potential “prime time” for an I Bond purchase.

Why invest in I Bonds at all?

Yes, at this point you can get a better nominal yield on a 13-week T-bill (4.36%) or a better real yield on a 5-year Treasury Inflation-Protected Security (1.97%). Both of those are attractive, safe investments. (And I invest in both.)

I Bonds, however, have unique qualities. They are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures.

Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

With an I Bond purchased today, you are guaranteed to earn 1.2% more than official U.S. inflation, with interest constantly compounding tax-deferred. You can redeem the I Bond after one year with a 3-month interest penalty, or after 5 years with no penalty.

My argument is that I Bonds should be viewed as a cash alternative in the form of a high-quality secondary emergency fund. You can let the principal grow without facing taxes, then after 5 years withdraw money as you need it, paying federal tax on the interest earned.

A lot of shorter-term, yield-hungry investors won’t see the appeal of I Bonds in 2025. That’s fine; there are great short-term options available right now. But many longer-term investors interested in building a sizable reserve of inflation-protected cash will want to buy I Bonds in 2025, up to the limit.

Rolling over 0.0% fixed-rate I Bonds

If you joined the mass movement into I Bonds back in October 2022, when the I Bond’s variable rate was about to reset from 9.62% to 6.48%, you are holding I Bonds with a fixed rate of 0.0% and your composite rate is going to be 1.90% for six months. That’s not a disaster, but many I Bond investors have been redeeming the 0.0% I Bonds and reinvesting the money into 1.3% or 1.2% fixed-rate versions over the last year. Or moving money into other investments.

That was the reason the gift box was so popular in recent years. Investors could redeem 0.0% sets, pay the tax on the interest, and then stash $10,000 into gift-box I Bonds to be delivered in future years. Then the Treasury set off chaos by encouraging these investors to deliver the gift-box bonds as soon as possible.

In the last two years, I have redeemed all our 0.0% fixed rate I Bonds and reinvested the money into the 1.3% or 1.2% versions (as of the scheduled Jan. 29 purchase). This makes sense for me, because I have large holdings in I Bonds and TIPS. Other people, still in the “accumulation phase” of I Bond investing, may want to hold the 0.0% versions and let them continue growing with inflation, tax-deferred.

The rollover process can be a little confusing, based on the limited information TreasuryDirect gives you for each holding. I wrote a guide back in September 2024.

“Just one more thing”

I think Treasury will make changes to the gift box program this year, but even if it doesn’t, I don’t plan to use it again in 2025. Under current rules, it appears that any amount of gift I Bonds can be delivered after an initial $10,000 purchase, Treasury has opened a gaping loophole, but only for people with a trusted partner.

What are your thoughts? Post your ideas and strategies in the comments section below. If you will bypass I Bonds this year, what alternatives are you considering?

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

This year 2024 brought many surprises. For example:

Did you think the stock market would soar higher after the Federal Reserve started lowering short-term interest rates? OK, that seemed predictable.

But then did you foresee that longer-term interest rates would move higher as the Fed cut short-term rates? I had a feeling that could happen.

And then that the stock market would continue soaring higher even as longer-term rates were rising?

And that a high-risk, speculative investment like Bitcoin would rise 53% in the 45 days after the November presidential election?

Or that the incoming Trump administration would at first cause stock-market froth and then trigger investor regret about potential policies, all in a two-month span?

Or that the Federal Reserve would end the year apparently ready to pause its rate-cutting path into 2025?

The year 2025 is bringing uncertainty. I would not be surprised to see a fairly large sell-off in stock prices early in the year, with investors eager to harvest gains in the new tax year. But I am not a stock market expert and I have no crystal ball. So instead, here is a look back at 2024:

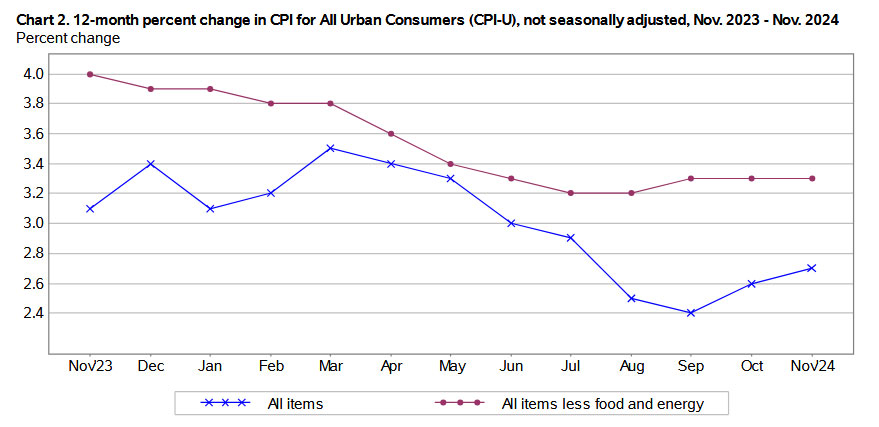

U.S. inflation

In November 2023, annual U.S. inflation stood at 3.1% for all-items and 4.0% for core. Today, as of November 2024, those numbers are 2.7% for all-items and 3.3% for core. That indicates progress. But the troubling thing — and what is clearly worrying the Fed — is that both inflation measures have been rising in recent months.

At its most recent meeting, Fed officials raised their 2025 inflation predictions for the Personal Consumption Expenditures Price Index (PCE) to 2.5% for both all-items (up from the previous estimate of 2.1%) and core (up from 2.2%). And at the same time, it cut interest rates.

Click image for larger version.

PCE tends to track lower than headline CPI, as shown in this chart from the Cleveland Fed. So that means, probably, that official U.S. inflation will rise by a rate higher than 2.5% in 2025 based on the Fed predictions. In other words, we could be seeing 2.7% to 3.0% inflation for many months to come.

In addition, you can add in the potential for higher inflation from Trump administration policy decisions on tariffs and deportations.

Again, the theme is uncertainty.

Treasury Inflation-Protected Securities

The past year was a stellar time for building a ladder of TIPS investments across the full maturity spectrum. Several times over the year, including this week, real yields were close to or above 2.0% across 5-, 10- and 30-year maturities. That offered a unique opportunity to build a ladder quickly and be done. I wrote about this last month.

Even investors in TIPS mutual funds and ETFs did relatively well in 2024, despite the upswing in real yields in recent weeks. The TIP ETF — with the full range of maturities — had a year-to-date total return of 1.48%. The short-term-focused VTIP ETF did better at 4.56%.

Here is a look at the 12 TIPS auctions through the year:

I have highlighted highs and lows for the year, but in my opinion every one of these auctions had a decent result for investors. Outside of the auctions, there were many mid-year and late-year opportunities to purchase TIPS on the secondary market with real yields close to or higher than 2.0%, a historically attractive target if held to maturity.

Click on image for larger version.

I would judge 2024 to be an excellent year for TIPS investing, based on the opportunities to snag attractive yields. But note: Real yields could rise higher, especially if inflation continues increasing and U.S. borrowing continues at very high levels. I wrote about this a week ago.

Bloomberg this morning has a detailed article focused on growing pressures in the U.S. Treasury market as the debt level swells. It explains that the primary dealer system may no longer be fully capable of dealing with bond-market disruptions.

“Issuance has gone up almost threefold in the last 10 years and the anticipation is for it to close to double to $50 trillion outstanding in the next 10 years, whereas dealer balance sheets haven’t grown at that magnitude,” said Casey Spezzano, head of US customer sales and trading at primary markets dealer NatWest Markets. … “You’re trying to put more Treasuries through the same pipes, but those pipes aren’t getting any bigger.”

U.S. Series I Savings Bonds

These inflation-protected savings bonds started the year with a fixed rate of 1.3% and a six-month composite rate of 4.28%. Today, the fixed rate for new purchases has fallen just a bit, to 1.2%, but the composite rate is sharply lower at 3.11%.

I am still a fan of and strong advocate for these Nov 2024 – Apr 2025 I Bonds, a unique, super-simple, super-safe investment that will provide tax-deferred returns exceeding inflation for as long as you hold them. My advice is to ignore the composite rate and focus on the 1.2% fixed rate, which is attractive. If inflation continues running at high levels through 2025 and beyond, these savings bonds provide protection in the form of a cash-equivalent savings account that is adjusted for inflation.

At this point, it looks possible the I Bond’s fixed rate could increase at the May 1 reset. For that to happen, using our back-of-the-envelope theory, the 5-year TIPS real yield would need to average at least 1.92% from November to April. That would get you back to 1.3%. At this writing, the 5-year TIPS is yielding 1.99%.

However, because the 5-year TIPS is sensitive to changes in short-term rates, I’d say the 5-year real yield will probably be heading lower.

Next year, changes may be coming to the savings bond program, especially to the much-used “gift-box” loophole for adding to your holdings with a trusted partner. But at this point, we know nothing. The Treasury in the last year has halted issuance of paper I Bonds in lieu of a federal tax refund, and also ended its Payroll Savings Plan for automatic contributions into TreasuryDirect.

This will be something to watch in the coming weeks.

In summary

Uncertainty seems to be my word of the day, maybe for the entire year 2025. And I believe uncertainty causes market disruptions. Things could keep humming along, but it’s probably time for a reality check for over-heated stock and alternative-investment markets.

To quote a famous American: “Be there, will be wild!”

Conservative investors will survive.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It is a possibility, says a T.Rowe Price analyst.We haven’t seen that level in 25 years.

By David Enna, Tipswatch.com

The chief investment officer at T.Rowe Price is making a bold prediction: Yields on the 10-year Treasury note could reach 6% in 2025.

“Is a 6% 10‑year Treasury yield possible? Why not? But we can consider that when we move through 5%,” Arif Husain wrote in a T.Rowe Price report. He is predicting the benchmark yield may reach 5% in 2025 before climbing higher. He writes:

I continue to expect higher intermediate‑ and long‑term Treasury yields, steepening the curve as Federal Reserve (Fed) rate cuts anchor short‑term yields.

Husain says the U.S. economy is now in a “calm before the storm.” Here are some of his key takeaways:

Increases in U.S. government spending and potential tax cuts, combined with a healthy economy, are likely to push Treasury yields higher.

Decreasing foreign demand for U.S. Treasurys could further elevate yields.

The incoming U.S. administration creates uncertainty. Policies on tariffs and immigration are potentially inflationary.

Husain sees little chance for a U.S. recession in 2025, which could help ease interest rates. His prediction came just before a too-hot CPI inflation report issued Dec. 11 was followed a week later by hawkish Federal Reserve signals, which sent Treasury yields surging higher.

The 10-year Treasury yield has increased 33 basis points in the month of December. It is a key data point across the U.S. economy, influencing everything from corporate debt to mortgages, even car loans.

Reaction

I agree that yields on the 10-year Treasury note could climb above 5% in coming months. That’s possible, but not a sure thing. We are heading into a time of economic uncertainty as President-elect Trump unveils new policies. Last week’s debt-crisis-gambit was not a good start.

The 10-year Treasury yield closed Friday at 4.52%, but the high for 2024 was 4.70% set on April 25. I’d say 5% would be within reach in the aftermath of any market-disturbing event, even if the Federal Reserve cautiously lowers short-term interest rates in 2025.

“Longer‑term Treasury yields should be increasing, steepening the yield curve,” Husain writes.

What would a 5% 10-year mean for TIPS?If 10-year inflation expectations hold around 2.4% (not desirable) you’d probably see the real yield on a 10-year TIPS rising to 2.6%, or higher, from the current 2.23%.

6% is a lofty target

Let’s look back at the last time the U.S. had a 10-year Treasury note yielding at or above 6%. That was January 2000, another time of market turmoil: A dot-com bubble about to burst, plus mania over the year 2000 crashing computers worldwide, resulting in massive corporate spending to avoid the problem.

Click on image for larger version.

Interesting fact: On January 12, 2000, a 10-year TIPS was auctioned with a real yield to maturity of 4.338% and a coupon rate of 4.250%, which probably ranks as the “greatest” 10-year TIPS auction of all time. The inflation breakeven rate was 2.38%, very close to a typical rate today.

At that point, in 2000, TIPS were a very new investment product, with just a three-year history. But it does show that the 6.7% nominal rate of early 2000 was not a reaction to high inflation.

Some facts about that time, 25 years ago:

U.S. Gross National Product grew at a real rate of 4.79% in 1999, the highest rate for any year since then until the pandemic bounce-back in 2021 at 5.80%. In 2024, GDP is growing at a rate of about 3.1%.

U.S. inflation increased 2.7% in 1999, which matches the current U.S. rate as of November 2024. In the year 2000, it surged to 3.4%.

The U.S. unemployment rate at the end of 1999 was 4.2%, which again matches the rate of 4.2% for November 2024.

The federal funds rate was 5.5% in January 2000, with another 100 basis points in increases coming by May 2000. Today, that rate is effectively 4.3%.

The U.S. budget deficit in 1999 was … actually, it was a surplus of $126 billion. Hard to believe, isn’t it? For 2024, the U.S. budget deficit is running at about $1.8 trillion.

Looking at these factors, except for the strong GDP growth of 1999 and higher short-term interest rates, you could almost assume longer-term interest rates should be higher in 2025 than in early 2000. Inflation rates and unemployment rates are quite similar. But the size of the U.S. budget deficit heading into 2025 is massively higher.

Getting the federal deficit under control should not be a Democratic vs. Republican issue, or liberal vs. conservative. It has to be done, either through spending cuts or tax increases or a combination of the two. It will take a brave politician to advocate for either. Husain writes:

With the Trump administration promising to cut taxes, there is little chance that the deficit will meaningfully decrease. The Treasury Department will need to continue to flood the market with new debt issuance to fund the budget deficit, pressuring yields higher.

I think a yield of 6% still looks unlikely in 2025, but if nominal Treasury yields surge above 6%, the nation’s problems will only get worse.

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am definitely not a fan of purchasing TIPS with negative real yields. My goal is to get a safe…