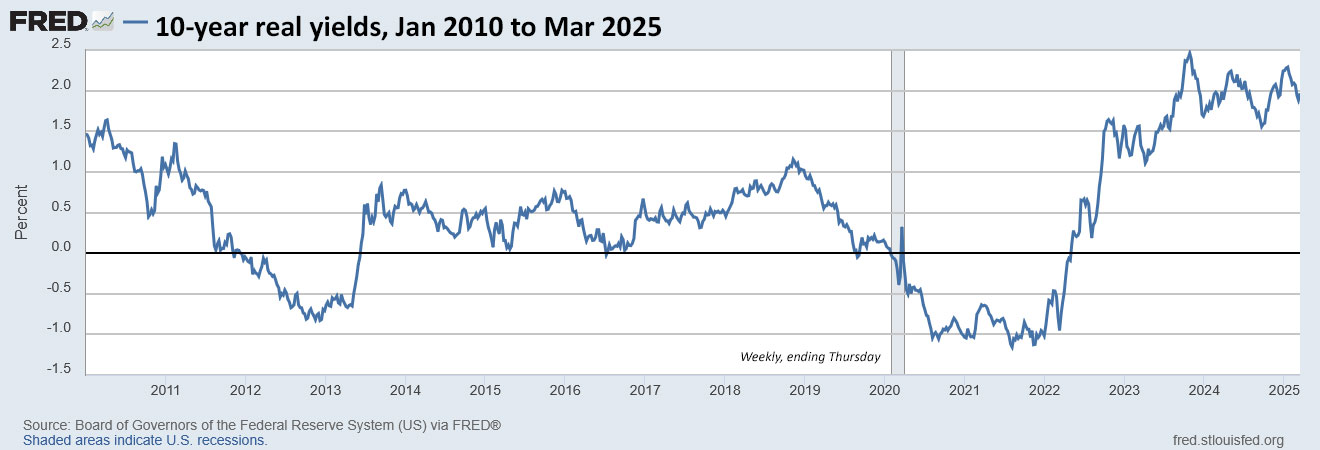

The benchmark 5-year real yield continues to fall.

By David Enna, Tipswatch.com

April 11, 2025, update: Welcome to the I Bond ‘buying season’

April 10, 2025, update: I Bond’s variable rate will rise to 2.86% on May 1

Amid all this week’s financial chaos, I am trying to focus on something I more or less understand: Projecting the May 1 fixed-rate reset for the U.S. Series I Savings Bond.

When I last looked at this topic on March 9 the real yield of a 5-year TIPS was trading at 1.57%, which was down 40 basis points from the start of this year. In the past month, the 5-year real yield has continued declining. It closed Wednesday at 1.44% according the Treasury’s daily estimate , but in the midst of tariff paranoia this morning is trading at 1.12%.

I’d expect a bounce higher, but who knows? But even ignoring this morning’s decline, it looks likely that the I Bond’s fixed rate is going to fall from the current 1.2% to 1.1% at the May 1 reset.

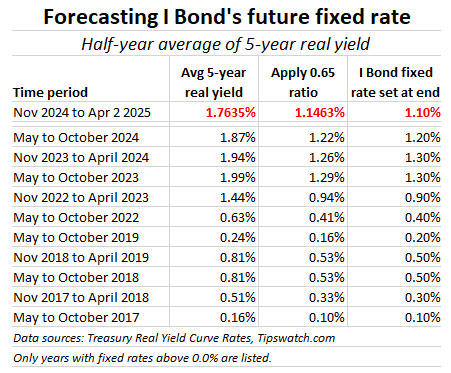

The 5-year real yield is key

The Treasury has never revealed a formula for setting the I Bond’s fixed rate, but it has stated it looks at real yield trends over time. I Bond watchers have observed that over the last decade one formula has accurately predicted the Treasury’s fixed rate decision: Apply a ratio of 0.65 to the average 5-year real yield over the preceding six months. This formula has worked without fail at least since 2017.

This morning I calculated the 5-year real yield data from the date of the last reset on November 1, 2024, to Wednesday’s close. And this week, for the first time, the data show the trend has tilted toward the 1.10% fixed rate.

Note that the I Bond’s fixed rate is always set to the one-tenth decimal point and that means the result of the 0.65 ratio calculation has to be rounded. Now that it has dropped below the 1.15% level, it rounds to 1.10%. And that level is likely to stick with the 5-year real yield plummeting this morning.

Back on March 9 I projected that the average 5-year real yield would need to remain above 1.57% through March and April for the 1.20% fixed rate to carry over to May 1. That is not happening.

Is there a strategy?

As I noted last month, the Trump administration could decide to ditch the long-standing formula for setting the I Bond’s fixed rate. Or it could be swayed by the current low yield of a 5-year TIPS and opt to go lower. Or it could decide to eliminate the savings bond program entirely. (Not likely). So we don’t know.

But from what we do know, it looks like the wisest choice for committed I Bond investors to buy their 2025 allocation late in the month of April, to capture the current 1.20% fixed rate. I ended up completing my 2025 purchases on March 28 because I had available cash and I could see the fixed rate wouldn’t be going any higher.

Are I Bonds still attractive? Absolutely. An I Bond purchased today will earn 1.2% over inflation, while a 5-year TIPS will earn 1.12%. We are back to the strange days when the I Bond has a yield advantage over a TIPS. When that happens, I Bonds are clearly the superior investment because they earn tax-deferred interest, have rock-solid deflation protection and a flexible maturity term.

Next week, on April 10, we will get the March inflation report, the final piece of data needed to set the I Bond’s new variable rate. The official seasonally-adjusted inflation number could be close to zero, but non-seasonally adjusted inflation should be higher, maybe 0.2%. That would give us a new six-month variable rate of 2.80%, up from the current 1.90%.

But that is next week’s news and I will be doing an update on the fixed-rate projection after the March inflation report is revealed.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

if you think deflation is around the corner, why would you buy TIPS?