By David Enna, Tipswatch.com

This year 2024 brought many surprises. For example:

- Did you think the stock market would soar higher after the Federal Reserve started lowering short-term interest rates? OK, that seemed predictable.

- But then did you foresee that longer-term interest rates would move higher as the Fed cut short-term rates? I had a feeling that could happen.

- And then that the stock market would continue soaring higher even as longer-term rates were rising?

- And that a high-risk, speculative investment like Bitcoin would rise 53% in the 45 days after the November presidential election?

- Or that the incoming Trump administration would at first cause stock-market froth and then trigger investor regret about potential policies, all in a two-month span?

- Or that the Federal Reserve would end the year apparently ready to pause its rate-cutting path into 2025?

The year 2025 is bringing uncertainty. I would not be surprised to see a fairly large sell-off in stock prices early in the year, with investors eager to harvest gains in the new tax year. But I am not a stock market expert and I have no crystal ball. So instead, here is a look back at 2024:

U.S. inflation

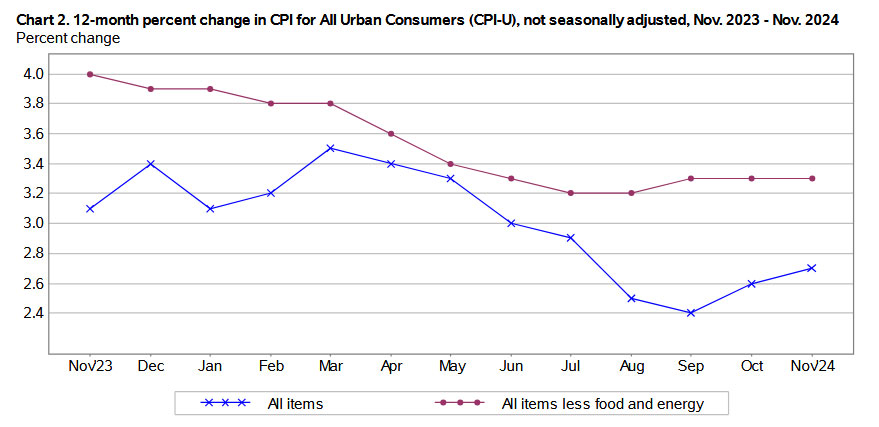

In November 2023, annual U.S. inflation stood at 3.1% for all-items and 4.0% for core. Today, as of November 2024, those numbers are 2.7% for all-items and 3.3% for core. That indicates progress. But the troubling thing — and what is clearly worrying the Fed — is that both inflation measures have been rising in recent months.

At its most recent meeting, Fed officials raised their 2025 inflation predictions for the Personal Consumption Expenditures Price Index (PCE) to 2.5% for both all-items (up from the previous estimate of 2.1%) and core (up from 2.2%). And at the same time, it cut interest rates.

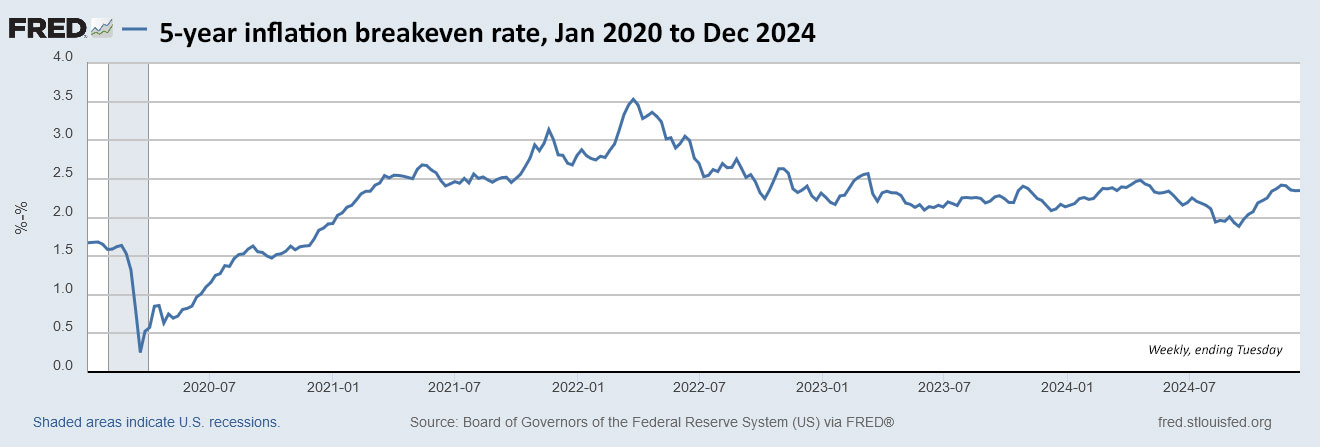

PCE tends to track lower than headline CPI, as shown in this chart from the Cleveland Fed. So that means, probably, that official U.S. inflation will rise by a rate higher than 2.5% in 2025 based on the Fed predictions. In other words, we could be seeing 2.7% to 3.0% inflation for many months to come.

In addition, you can add in the potential for higher inflation from Trump administration policy decisions on tariffs and deportations.

Again, the theme is uncertainty.

Treasury Inflation-Protected Securities

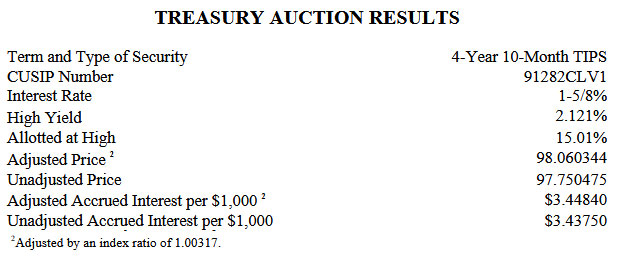

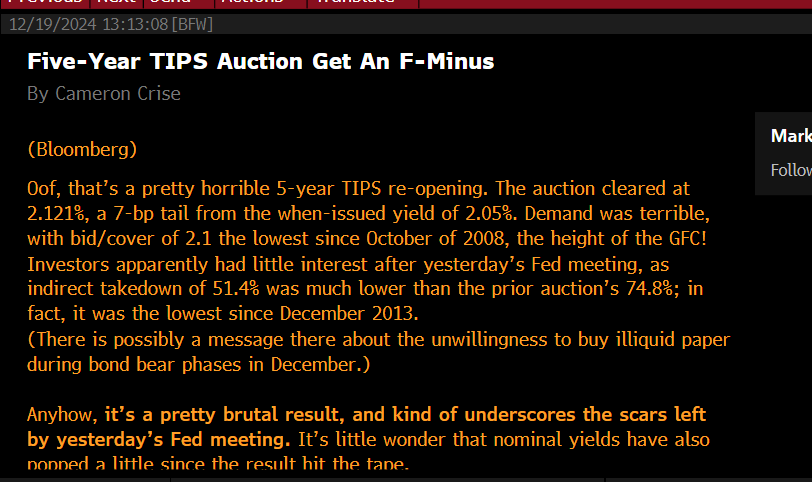

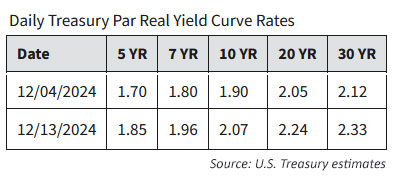

The past year was a stellar time for building a ladder of TIPS investments across the full maturity spectrum. Several times over the year, including this week, real yields were close to or above 2.0% across 5-, 10- and 30-year maturities. That offered a unique opportunity to build a ladder quickly and be done. I wrote about this last month.

Even investors in TIPS mutual funds and ETFs did relatively well in 2024, despite the upswing in real yields in recent weeks. The TIP ETF — with the full range of maturities — had a year-to-date total return of 1.48%. The short-term-focused VTIP ETF did better at 4.56%.

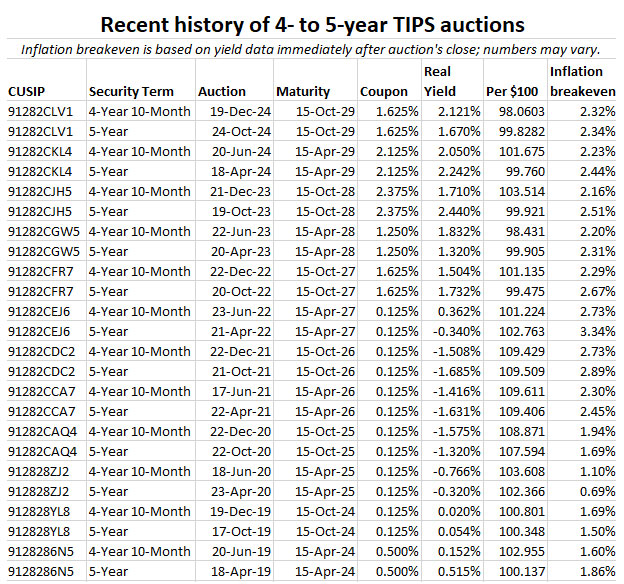

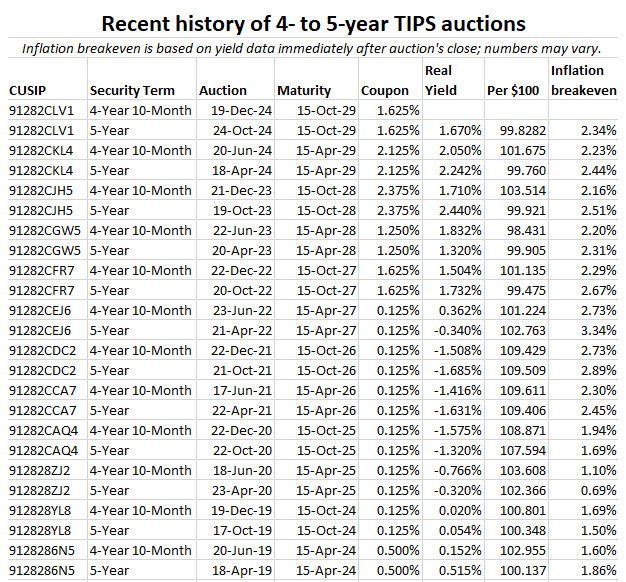

Here is a look at the 12 TIPS auctions through the year:

I have highlighted highs and lows for the year, but in my opinion every one of these auctions had a decent result for investors. Outside of the auctions, there were many mid-year and late-year opportunities to purchase TIPS on the secondary market with real yields close to or higher than 2.0%, a historically attractive target if held to maturity.

I would judge 2024 to be an excellent year for TIPS investing, based on the opportunities to snag attractive yields. But note: Real yields could rise higher, especially if inflation continues increasing and U.S. borrowing continues at very high levels. I wrote about this a week ago.

Bloomberg this morning has a detailed article focused on growing pressures in the U.S. Treasury market as the debt level swells. It explains that the primary dealer system may no longer be fully capable of dealing with bond-market disruptions.

“Issuance has gone up almost threefold in the last 10 years and the anticipation is for it to close to double to $50 trillion outstanding in the next 10 years, whereas dealer balance sheets haven’t grown at that magnitude,” said Casey Spezzano, head of US customer sales and trading at primary markets dealer NatWest Markets. … “You’re trying to put more Treasuries through the same pipes, but those pipes aren’t getting any bigger.”

U.S. Series I Savings Bonds

These inflation-protected savings bonds started the year with a fixed rate of 1.3% and a six-month composite rate of 4.28%. Today, the fixed rate for new purchases has fallen just a bit, to 1.2%, but the composite rate is sharply lower at 3.11%.

I am still a fan of and strong advocate for these Nov 2024 – Apr 2025 I Bonds, a unique, super-simple, super-safe investment that will provide tax-deferred returns exceeding inflation for as long as you hold them. My advice is to ignore the composite rate and focus on the 1.2% fixed rate, which is attractive. If inflation continues running at high levels through 2025 and beyond, these savings bonds provide protection in the form of a cash-equivalent savings account that is adjusted for inflation.

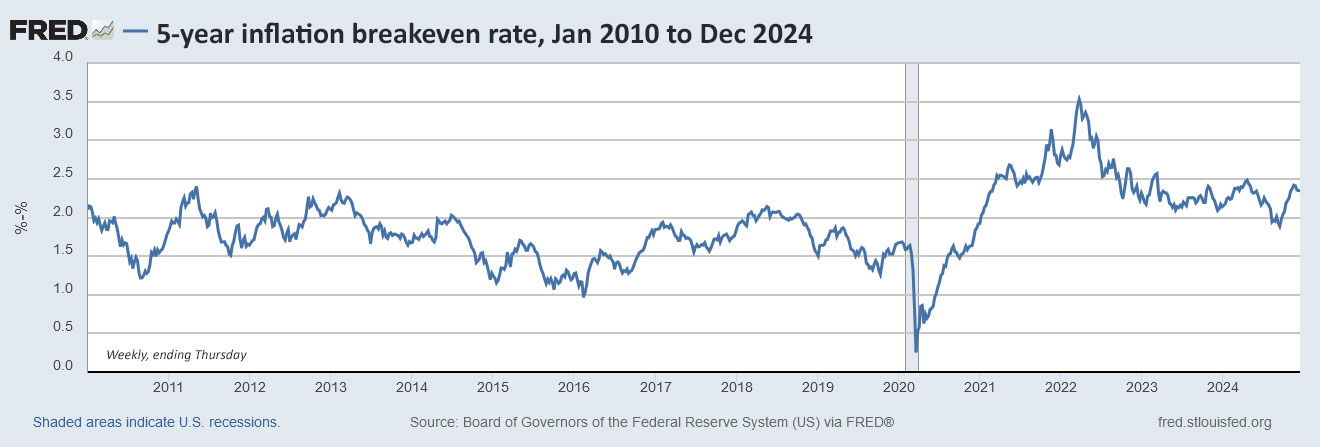

At this point, it looks possible the I Bond’s fixed rate could increase at the May 1 reset. For that to happen, using our back-of-the-envelope theory, the 5-year TIPS real yield would need to average at least 1.92% from November to April. That would get you back to 1.3%. At this writing, the 5-year TIPS is yielding 1.99%.

However, because the 5-year TIPS is sensitive to changes in short-term rates, I’d say the 5-year real yield will probably be heading lower.

Next year, changes may be coming to the savings bond program, especially to the much-used “gift-box” loophole for adding to your holdings with a trusted partner. But at this point, we know nothing. The Treasury in the last year has halted issuance of paper I Bonds in lieu of a federal tax refund, and also ended its Payroll Savings Plan for automatic contributions into TreasuryDirect.

This will be something to watch in the coming weeks.

In summary

Uncertainty seems to be my word of the day, maybe for the entire year 2025. And I believe uncertainty causes market disruptions. Things could keep humming along, but it’s probably time for a reality check for over-heated stock and alternative-investment markets.

To quote a famous American: “Be there, will be wild!”

Conservative investors will survive.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

What a bonanza they've been! I am fortunate to have had the instinct and the money to have purchased large…