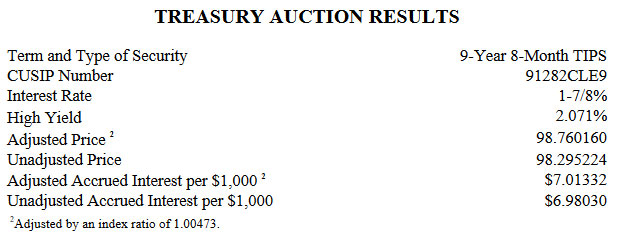

The Treasury’s reopening auction of a 10-year Treasury Inflation-Protected Security — CUSIP 91282CLE9 — generated a real yield to maturity of 2.071%, right in line with where this TIPS was trading this morning on the secondary market.

This TIPS has a 9-year, 8-month term and carries a coupon rate of 1.875%, which was set by the originating auction on July 18. Shortly before the auction’s close it was trading on the secondary market with a real yield of 2.07%, so the result looks on target. But the “when-issued” prediction was 2.05%, so demand might have been a bit weak. The bid-to-cover ratio was 2.35, also a bit weak.

In a short article on the auction, Marketwatch noted it produced “lackluster results.”

However, for investors, a real yield of 2.071% looks like a good result. An earlier reopening for this TIPS, on Sept. 19, got a much lower real yield of 1.592%.

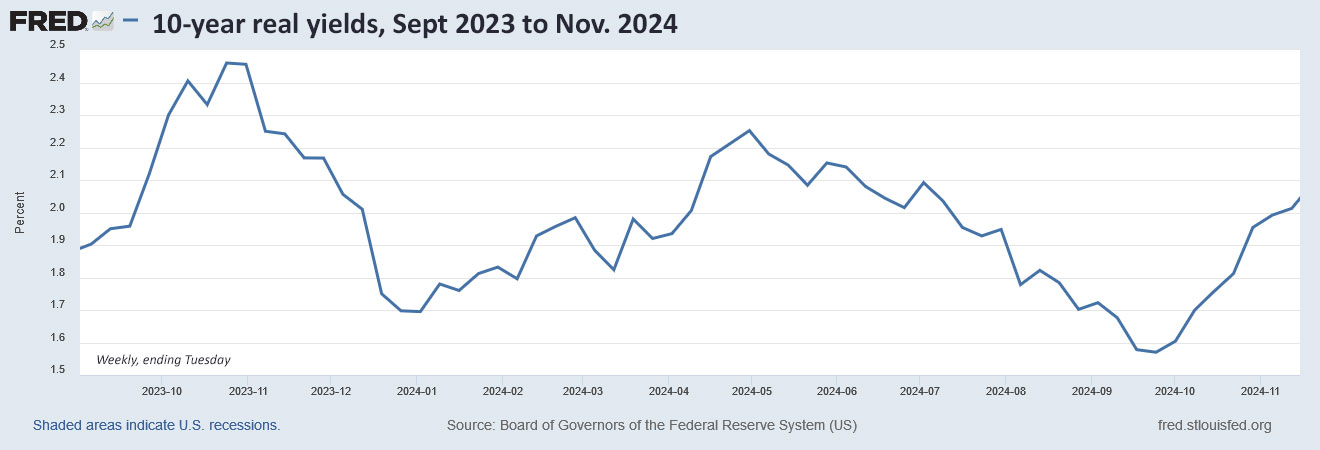

Here is the trend in the 10-year real yield over the last 14 months, showing the peak in October 2023 and the recent surge higher:

Click on image for larger version.

Pricing

Because this TIPS auctioned with a real yield higher than its coupon rate, investors got it at a discount, an unadjusted price of 98.295224. In addition, it will carry an inflation index of 1.00473 on the settlement date of Nov. 29. With that information, we can calculate the cost of a $10,000 par investment:

Par amount: $10,000.

Principal on settlement date: $10,000 x 1.00473 = $10,047.30

Cost of investment: $10,047.30 x 0.98295224 = $9,876.02

+ Accrued interest of $70.13

In summary, an investor purchasing $10,000 par of this TIPS paid $9,876.02 for $10,047.30 of principal on the settlement date on Nov. 29. From that point on, the investor will receive annual interest of 1.875% on adjusted principal, which will grow with future inflation.

Inflation breakeven rate

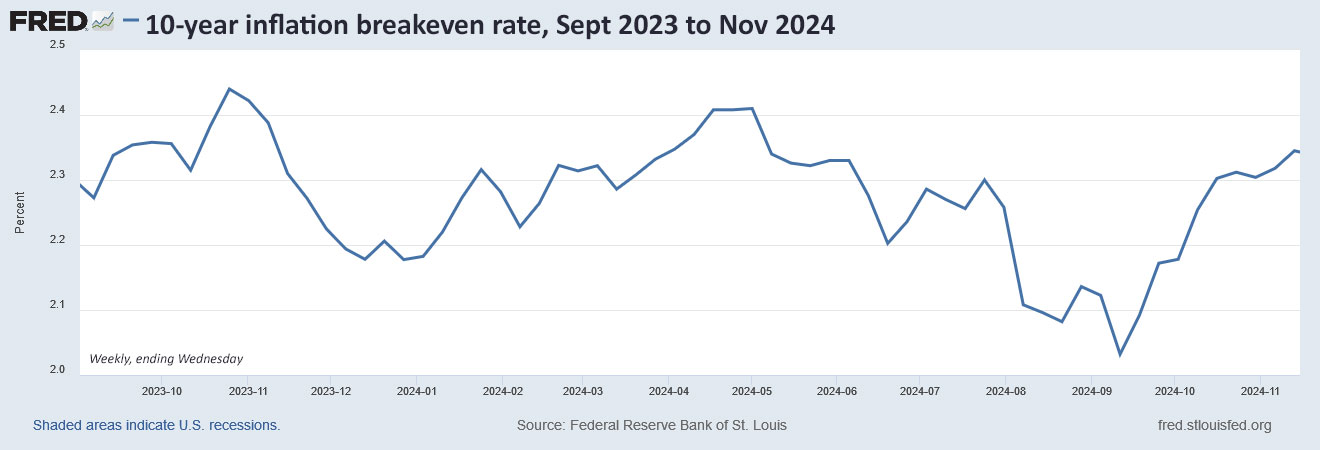

With the 10-year nominal Treasury note yielding 4.42% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.35%, a bit higher than recent results. This reflects growing uncertainty about future inflation at a time of a strong economy, strong stock market and very high U.S. budget deficits.

Here is the trend in the 10-year inflation breakeven rate over the last 14 months, showing the sharp upward trend in the two months leading to the U.S. presidential election:

Click on image for larger version.

Reaction to the auction

This was a good result for investors, easily clearing the coveted real yield threshold of 2.00%. Since January 2009, there have been 92 TIPS auctions of this term and only four have generated a real yield higher than 2%. Real yields could certainly continue going higher, but for a buy-and-hold investor a yield higher than 2.0% looks like a solid investment.

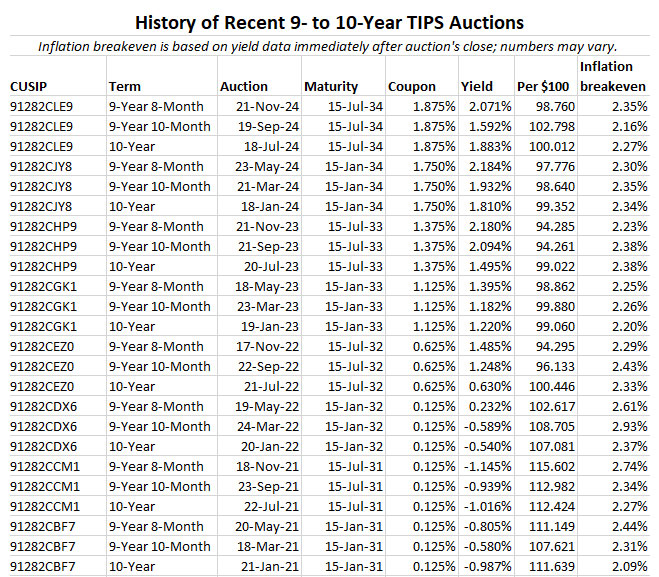

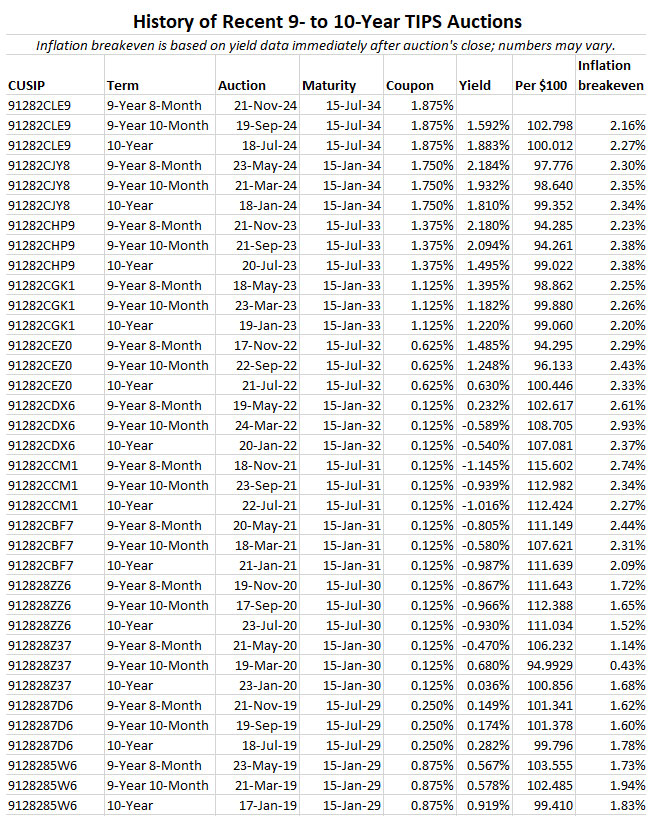

This was the last TIPS auction of this term for 2024. A new 10-year TIPS will be auctioned on January 23, 2025. Here are results for recent auctions of this term:

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Reality is beginning to settle in on the U.S. bond market. Even as the Federal Reserve continues to cut short-term interest rates, longer-term yields have been rising in recent weeks as the market:

Calculates the potential deficit risks of a Trump presidency.

Figures the possible effect of tariffs on U.S. inflation.

Observes a decently strong U.S. economy and labor market.

Ponders why risky asset classes like Bitcoin have surged 34% higher in two weeks.

And beyond all that, sees the U.S. Treasury continuing to borrow a lot of money.

As a result, mid- to longer-term Treasury yields have been rising over the last several weeks, as shown in a 56-basis-point rise in the 10-year real yield since mid-September. This surge could continue because the bond market is dealing with uncertainty. Bond investors don’t like uncertainty.

Amid this drama, the Treasury on Thursday will offer $17 billion in a reopening auction of CUSIP 91282CLE9, creating a 9-year, 8-month Treasury Inflation-Protected Security. Some history:

July 18. The originating auction for this TIPS got a real yield to maturity of 1.883%, which set its coupon rate at 1.875%, the highest coupon for this term since July 2009.

Sept. 19. The first reopening auction got a much lower real yield of 1.592%, the day after the Federal Reserve made a surprise decision to cut short-term interest rates by 50 basis points.

Now, two months later, the 10-year real yield has surged to 2.10%. CUSIP 91282CLE9 trades on the secondary market, and this weekend I am seeing price quotes right in the 2.10% range. Of course, things will change a bit before Thursday’s auction. An investor in this TIPS can also buy it at any time on the secondary market, of course.

Definition: The “real yield” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 2.10% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.10% for 9 years, 8 months.

Here is the trend in the 10-year real yield over the last 15 years, showing that while yields are off the highs of October 2023, they remain in a historically high range:

Click on image for larger version.

As for the future, who knows? It’s in the realm of possibility that 10-year real yields could climb to somewhere around 3% (as we last saw in January 2003). That seems unlikely, but if deficits soar while the U.S. economy is surging it could happen. However, if the economy dips into recession, both nominal and real yields will decline.

In the 15-year chart above, note the tiny shaded area indicating the very brief pandemic-triggered recession in 2020. One brief recession in 15 years is rather amazing. So … are we due?

Pricing

At Friday’s close, this TIPS was trading with a discounted price of 98.02. It is discounted because the real yield of 2.10% is above the coupon rate of 1.875%. In addition, it will have an inflation index of 1.00473 on the settlement date of Nov. 29. With that information, we can estimate the investment cost of a purchase of $10,000 par value:

Par value: $10,000

Actual principal purchased: $10,000 x 1.00473 = $10,047.30

Cost of investment = $10,047.30 x 0.9802 = $9,848.36

+ accrued interest = About $70.

In summary, the investor would pay $9,848 for $10,047 of principal and then receive inflation accruals plus an annual coupon payment of 1.875% for the next 9 years, 8 months. The accrued interest would be returned at the first coupon payment on Jan. 15. This is an estimate and conditions will change by Thursday.

Inflation breakeven rate

With the 10-year Treasury note closing Friday with a nominal yield of 4.43%, this TIPS currently has an inflation breakeven rate of 2.33%, higher than recent auctions of this term. Not a big surprise … this reflects the market’s uncertainty about future inflation. Over the last 10 years ending in October, inflation has averaged 2.9%, the highest 10-year rate since 1999.

A simple rule for me is that a higher inflation breakeven rate indicates that a TIPS is “more expensive” versus the nominal Treasury. In this case, I have to admit, a 10-year Treasury note paying 4.43% looks pretty attractive. But I’d still prefer to invest in the TIPS to get the future inflation protection.

Here is the trend in the 10-year inflation breakeven rate over the last 15 years, showing that the current rate of 2.33% is in the “highish” zone:

Click on image for larger version.

Some thoughts

I bought this TIPS on the secondary market on Oct. 29 with a real yield of 2.008%, so I am not in the market to buy more. I am now awaiting the auction of a new 10-year TIPS on Jan. 23, 2025. That TIPS will be my first (and possibly only) purchase for the 2035 rung of my TIPS ladder.

If you have a brokerage account, you can buy this TIPS at auction this week, or any time on the secondary market when you see a real yield you like. The advantage of the auction is that small purchases (the minimum is only $100 at TreasuryDirect) get the high real yield, but you won’t know the yield until the auction completes. The advantage of the secondary market is you can see the exact yield you are purchasing, but you may face a small penalty for buying in a small amount.

In my opinion, any 10-year TIPS with a real yield of 2%+ is attractive. It is a good target for investing. If you are buying at auction, you can follow the real yield of this TIPS on the secondary market on Bloomberg’s Current Yields page. Both the bond and stock markets are volatile right now, so things can change.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Part B costs, deductibles and IRMAA surcharges will increase about 5.9% next year.

By David Enna, Tipswatch.com

Just a month ago, Social Security beneficiaries learned their benefits would rise by 2.5% starting in 2025, the lowest increase in four years. But the good news was that the increase slightly outpaced U.S. inflation up to that point, 2.4%.

And now, the bad news: The Centers for Medicare & Medicaid Services just announced that monthly costs for Medicare Part B premiums, annual deductible and IRMAA surcharges will rise by a much higher amount, about 5.9%, for 2025.

Any day now, if you are on Medicare, you will get a letter from CMS informing you of these new premium and deductible costs for 2025. If you planned poorly, you may be meeting up with IRMAA, the Income-Related Monthly Adjustment Amount. These surcharges can be lofty, so it’s smart to plan ahead to limit these costs.

Here is a summary of the price changes:

The Part B deductible is rising 7.1% to $257.

The Part B base monthly premium is rising 5.9% to $185.

The IRMAA surcharge levels (for both Part B and Part D) are rising 5.9%.

The IRMAA income tiers that trigger the surcharges are increasing at a lower rate, generally around 3%.

Let’s dive into the key Medicare changes for 2025.

Part A premium and deductible

Most people who reach age 65 go on Medicare Part A, even if they are still working. Medicare Part A covers inpatient hospital, skilled nursing facility and some home health care services. About 99% of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

Although coverage is generally free, Part A has some sizable deductibles and coinsurance costs, and those will be rising about 2.7% in 2025.

Keep in mind that most people on Medicare have a Medigap or Medicare Advantage plan that will cover all or most of the Part A deductible and coinsurance amounts. For example, all standardized Medicare Supplement (Medigap) plans, A through N, provide coverage for Part A coinsurance, and most also cover all or most of the Part A deductible costs.

Part B: Medical insurance

Medicare Part B can be described as covering “outpatient services,” things like doctor visits, some lab tests, an annual wellness exam, diabetes screenings, etc. Medicare Part B generally pays 80% of approved costs of covered services, and you pay the other 20%. Some services, like flu shots, Covid vaccines and a wellness visit, may cost you nothing.

Part B deductible. Before Medicare pays anything, you have to meet your Part B deductible each year. The annual deductible for all Medicare Part B beneficiaries will be $257 in 2025, an increase of 7.1% over the annual deductible of $240 in 2024. As of January 2020, Medigap plans sold to new enrollees were not allowed to cover the Part B deductible. But once the deductible is met, Medicare and Medigap plans will cover some or all of your Part B costs.

Part B premium. The standard monthly premium for Medicare Part B enrollees will be $185.00 for 2025, an increase of $10.10 from $174.90 in 2024. This Part B premium is paid by all people on original Medicare and is incorporated into Medicare Advantage pricing, which may or may not result in a baseline monthly cost.

So, for most people on original Medicare, Medicare Part B is going to cost $185 a month for the premium, plus the cost of the $257 deductible. That’s a total cost of $2,477 a year, up about 6% from this year’s costs.

And then … IRMAA

Since 2007, a beneficiary’s Part B monthly premium is based on reported income, known as MAGI, or modified adjusted gross income. According to the Social Security Administration handbook, for Medicare’s purposes MAGI is adjusted gross income (line 11 of your 2023 federal income tax form) plus tax-exempt interest.

Note that I mentioned your 2023 income tax return. That’s the one you filed earlier this year and now, in November, CMS announced the IRMAA surcharge brackets applied to that 2023 return. In other words, you could not know the surcharge levels until after the fact. And this is a rather brutal surcharge, because going just $1 over any limit can trigger thousands of dollars of one-year costs.

CMS says about 8% of people on Medicare pay these surcharges, up from 7% a year ago. It’s important to note that people on Medicare Advantage plans continue to pay the Part B premium, and are also subject to the IRMAA surcharges. And keep in mind that for a couple, the costs are doubled because each person pays the surcharge.

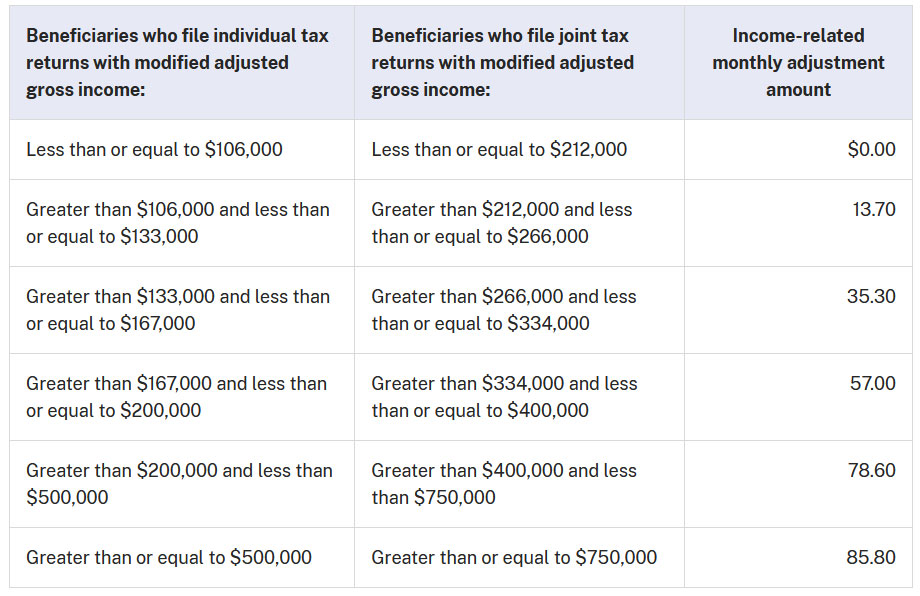

Part B. Here are the 2025 Part B total premiums and surcharges for high-income beneficiaries, which apply to income reported on your 2023 tax return:

Annual income of $212,000+ for a couple may sound like a lot, but the lower IRMAA levels can easily be reached through Roth conversions, stock sales to fund a major purchase, a new pension starting up, etc. Be aware of the potential to trigger the IRMAA surcharges and plan around that possibility.

Part D. Medicare income-related surcharges also apply to Part D, the drug program which is offered by private insurers working with Medicare. Part D premiums vary by plan, but the Part D surcharges are deducted from Social Security benefit checks or paid directly to Medicare.

People in Medicare Advantage plans don’t pay a separate Part D premium, since those plans include Medicare Advantage Prescription Drug (MAPD) coverage. But Part D is built into Medicare Advantage, and the IRMAA surcharge still applies.

Be aware of IRMAA

If you are just a couple years away from going on Medicare, it’s a great idea to plan your total income for this year to avoid triggering IRMAA surcharges two years later. The surcharges last only one year and then get reset the next year. The costs can be substantial for people hitting the top IRMAA tiers.

And I repeat: When you filed your federal tax return in early 2024 for the 2023 tax year you could not know what these IRMAA brackets or surcharges would be. They were just announced on Nov. 8. They are called the “2025 IRMAA levels” but apply to your 2023 tax return.

When you file your 2024 return next year, realize that you won’t know the relevant IRMAA levels until October or November 2025, many months after you have filed. Your only option is to use the 2024 numbers as a guideline. It’s a crazy system.

You can appeal an IRMAA ruling

The Social Security Administration has very specific rules that will allow you to get a waiver of the IRMAA surcharge, if you meet certain criteria for a “life-changing event,” which include:

Work stoppage

Work reduction

Employer settlement payment

Death of spouse

Divorce

Loss of pension income

You’ll need to fill out IRS Form SSA-44 to request the waiver.

Final thoughts

It isn’t unusual, unfortunately, for Medicare costs to be rising at a faster pace than the Social Security COLA. From a recent USA Today report:

2025 isn’t an outlier. Medicare Part B premiums have been rising faster than COLA for years, data show, which is part of the reason many seniors have been struggling. From 2005 to 2024, Part B premiums increased on average by 5.5% per year, while COLAs averaged less than half that rate at just 2.6%.

In 2025, the typical Social Security recipient will receive about $588 more because of the increase in the COLA. For a typical person on Medicare, avoiding IRMAA, costs of the Part B premium and deductible will increase about $140 next year. So for the average person nearly a quarter of the COLA increase will be snatched back by higher Medicare costs.

Also, other Medicare costs are likely to rise. The cost of our Part G supplemental plan increased 13% earlier this year, and some increase is likely again in 2025.

However …

Sometimes I feel the need to remind younger people: “Medicare is not free.” There are expenses and I am fortunate to say that — so far — my payments into Medicare have been higher than the services I have received. That means I am healthy. I’ll take that trade any day.

Original Medicare with a good supplement is very good insurance and worth the cost. But … don’t pay more than you need to. Keep an eye on IRMAA.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

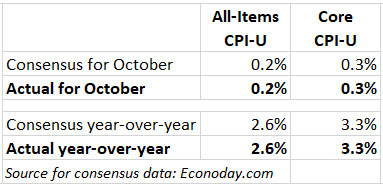

It’s good news when a monthly U.S. inflation report matches expectations. And October delivered, even though annual all-items inflation ticked higher and core remained too strong for comfort.

The U.S. Bureau of Labor Statistics reported that all-items CPI-U increased 0.2% on a seasonally adjusted basis in October, the same increase as in each of the previous three months. Over the last 12 months, the all-items index increased 2.6%, higher than September’s 2.4%. Core inflation, which removes food and energy, held steady at 0.3% for the month and 3.3% for the year.

All these numbers matched economist expectations in a clean sweep, which hardly ever happens. Inflation is hard to predict.

The BLS noted that shelter costs increased 0.4% in October, accounting for more than half of the all-items increase. Shelter costs were 4.8% higher year over year. Those increases were partially offset by a 0.9% drop in gasoline prices, which were down 12.2% year over year. More from the report:

Food at home prices rose only 0.1% for the month, after rising 0.4% in September, and are up 1.1% year over year.

Electricity costs rose 1.2% for the month and 4.5% year over year.

Apparel costs fell 1.5% for the month and are up just 0.3% for the year.

Airline fares rose 3.2% for the month and are up 4.1% year over year.

The costs of motor vehicle insurance rose 1.2% and are up 14.0% year over year.

Medical care services were up 0.4% for the month and 3.8% year over year.

Costs of new vehicles were flat for the month and down 1.3% for the year.

Used vehicle costs rose 2.7% but are still down 3.4% year over year.

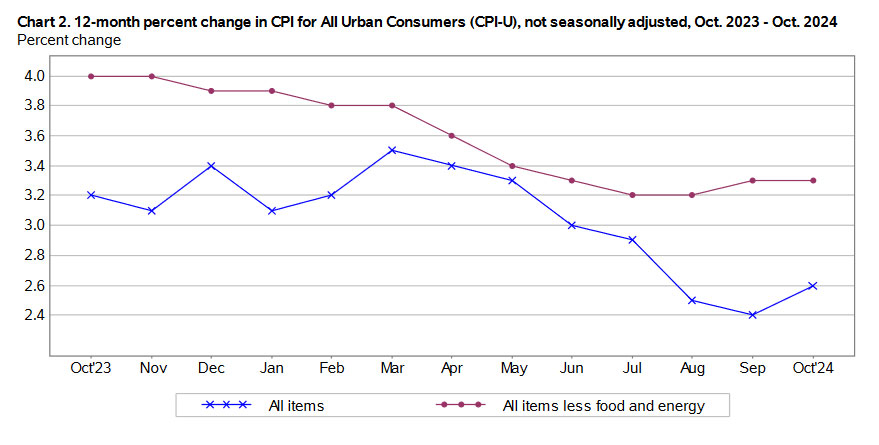

Overall, while this October inflation report met expectations, it also clearly shows U.S. inflation has not been tamed. This is not good news. Here is the trend in U.S. inflation over the last year, showing the uptick in all-items costs:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds.

The BLS set the October inflation index at 315.664, an increase of 0.12% over the September number. We are heading into the time of year when non-seasonal inflation will be running lower than adjusted inflation. Don’t be surprised if we see one or two months of deflation in this index before the end of the year.

For TIPS. The October number means that principal balances for all TIPS will increase 0.12% in December, after rising 0.16% in November. Over the 12 months ending in December those balances will have increased 2.6%. Here are the new December Inflation Indexes for all TIPS.

For I Bonds. October marks the first month of a six-month string that will determine the I Bond’s new variable rate, to be reset May 1, 2025. After one month, inflation has increased 0.12%. It’s way too early to draw any conclusions from that. (But in October 2023, non-seasonal inflation fell 0.04%, the first of three consecutive deflationary months.) Here are the data:

Overall inflation rose in October, which was expected but can’t be welcomed. Because the numbers were in line with expectations, we can probably expect the Federal Reserve to go ahead with a 25-basis-point cut in short-term rates in December.

The effect of that cut on the economy would be minor because longer-term rates have increased dramatically in the last few weeks. U.S. 30-year mortgage rates have increased from about 6.1% at the beginning of October to 6.8% today.

The figures underscore the slow and frustrating nature of the battle against inflation, which has often moved sideways — sometimes for months at a time — on its broader path down. …

“October’s CPI report remains in the same holding pattern as the past few months – inflation isn’t picking back up, but it’s also not cooling any faster,” said Anna Wong of Bloomberg Economics.

“October’s CPI report contains no information that would discourage the FOMC from cutting rates again at the December meeting,” said Michael Arnold, Bloomberg Economics Editor.

My impression is that this report changes nothing. Inflation remains well above 2.0% and will continue to be a long-term danger if the U.S. economy and stock market hold strong.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Because of a remarkable confluence of events, including last week’s presidential election result, real and nominal yields for U.S. Treasurys have been rising dramatically, up 40 to 50 basis points since October 1.

But this article is not about politics. It is about opportunity.

Just a couple months ago, I was hearing from investors ruing the fact they missed the chance to build a ladder of Treasury Inflation-Protected Securities with yields near 2024 highs. But now that real yields have again surged higher, that door is open again.

Why a TIPS ladder?

Jason Zweig, personal finance columnist for the Wall Street Journal, wrote an article last week titled, “What to Buy if the Election Has You Worrying About Inflation.” I talked with Zweig last week before he posted the article. A lot of our discussion focused on the sometimes unexpected risks of investing in ETFs holding a broad range of TIPS. From the article:

In 2021, TIPS funds returned an average of 5.5%, while a U.S. bond index fund fell 1.7%. Naturally, investors and financial advisers bought TIPS in titanic quantities that year, pouring $42.4 billion into mutual funds and exchange-traded funds that specialize in them, according to Morningstar.

Right on cue, in 2022 the Fed jacked up interest rates and TIPS lost about 12%. Fickle investors fled TIPS funds, yanking out a combined $37.2 billion in 2022 and 2023.

Dumping all this money into and out of TIPS makes no sense.

Zweig then explained the advantages of buying individual TIPS and holding to maturity:

If you buy TIPS directly and hold them to maturity, your future rate of return after inflation is certain, as is the return of your principal. …

“We aren’t mathematical beings, we are emotional animals,” says Allan Roth, a financial planner at Wealth Logic in Colorado Springs, Colo. If you buy TIPS directly, “you know your spending power, what your cash flow is going to buy, in each future period,” he says. “You don’t know that if you buy a TIPS fund. And that makes it easier to stay the course if you own the TIPS directly.”

I am not a fan of broad-based TIPS funds and ETFs, although I have owned them in the past. By the time of the big bond decline of 2022, I had consolidated my TIPS funds holdings into Vanguard’s Short-Term TIPS ETF (VTIP) which ended 2022 with a total return of -2.96%, not devastating. As TIPS real yields started climbing out of negative, I began converting all my VTIP and part of my Total Bond Fund (BND) investments into a ladder of individual TIPS, all in a traditional retirement account.

Roth has been an important advocate for using a ladder of TIPS (at current yields) to create a reliable and totally safe withdrawal rate of 4%+ through a 30-year retirement. And thanks to his urging, the process of filling a TIPS ladder has gotten a lot easier. Just last month, Roth published an article titled, “Four Easy Steps to Build a TIPS Ladder.” He writes:

The world is and always has been risky and it’s feeling riskier than usual. What if stocks have a real and protracted plunge rather than the teddy bears we have had this century? What if all of this government debt causes hyperinflation? Building a TIPS ladder gives us a license to spend and creates a spending floor.

Roth’s article gives step-by-step instructions for creating a model TIPS ladder using the tool at Tipsladder.com. I won’t repeat the steps here, but the result could be an investment list like this — at a cost of $452,656 — for a TIPS ladder running from 2025 to 2054 and providing a safe, inflation-adjusted base income of $20,000 a year, with a safe withdrawal rate of 4.42%.

Click on image for larger version. Source: Tipsladder.com

An opportunity to build, or improve

Here is a chart showing real yields for 5-, 10-, and 30-year TIPS over the last 15 years, showing how TIPS of all maturities are near highs for this 15-year period.

Click on image for larger version.

The unique thing about this chart is the alignment of real yields into a much tighter band than we’ve seen historically. And that means that an investor can find attractive real yields for every year of a TIPS ladder. That’s an opportunity.

My personal TIPS ladder was built chaotically, and I have added in some nominal Treasurys and CDs timed to mature in the years 2025 to 2029 to allow me to purchase 10-year TIPS to fill the gap years of 2035 to 2039. Here are my Treasury investments laddered through 2043, with a comparison to the real yields you can find today on the secondary market:

Looking at this list, I’d say I could do better today in some cases than I did building the ladder in late summer/early fall 2023. I am happy with these investments, but will still look for opportunities to add to the ladder. Just last week, for example, I purchased the July 2034 TIPS with a real yield of 2.008%. (That same TIPS will have a reopening auction on November 21.)

Can real yields continue climbing higher? Certainly. But if you can nail down a real yield of 2.0%+ over the long term, you’ll end up fine, with a safe yearly withdrawal rate of 4.4% or more.

My ladder ends in 2043, but if you are building beyond that year, you can find very attractive yields through 2054. The real yield curve has been steepening, meaning you get a better return for a longer maturity. These very-long term TIPS are highly volatile, so you need to invest, forget and hold to maturity. Zweig writes:

Of course, in the bond-market bloodbath of 2022, the prices of individual TIPS fell. So did TIPS funds. Those losses apparently felt much more intense to people who owned TIPS funds than they did to investors who owned the underlying securities directly. That’s probably because direct holders draw comfort from the expectation that they’ll hold the TIPS until maturity. …

If you want to assure yourself of having a known amount of investment income in a specific year, buy TIPS directly. …

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I believe you asked 'what is your money earning now?' and I answered... I'm earning a lot more real yield…