By David Enna, Tipswatch.com

April 11, 2025, update: Welcome to the I Bond ‘buying season’

April 10, 2025, update: I Bond’s variable rate will rise to 2.86% on May 1

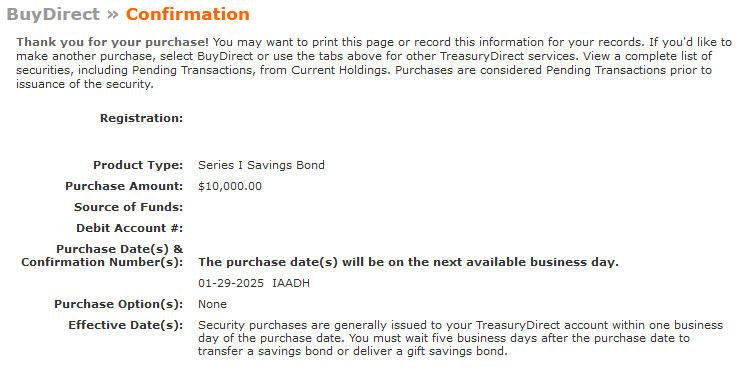

Update, Jan 31, 2025: I noted in this article that I was going to make a “test” I Bond purchase in January 2025 to see if it would trigger a purchase limit because of gift box deliveries in 2024. The transaction was scheduled for Jan. 29 and the money was withdrawn by the Treasury on that date. A day later, TreasuryDirect showed the I Bond in the account, dated Jan 1 2025. So it all worked without a hitch.

——-

I’m a big fan of all those Agatha Christie Poirot books, Sherlock Holmes, Philip Marlow, every episode of Columbo on TV. But even those great detectives would have a hard time figuring out TreasuryDirect.

So now we enter a new year, and the annual $10,000 per person purchase cap for U.S. Series I Savings Bonds has reset. But one big question remains for many investors: Can I buy I Bonds this year? And for others: When should I buy I Bonds this year? Or even … Why invest in I Bonds at all?

Just a reminder: An I Bond is a U.S. Treasury security that combines a permanent fixed interest rate with a six-month variable rate, creating an inflation-protected return. They can only be purchased in electronic form at TreasuryDirect.

Can I buy this year?

TreasuryDirect created a lot of confusion in October when it sent an email to investors holding I Bonds in a “gift box” for later delivery. The email seemed to urge delivery of those I Bonds “as soon as possible.” The email was strange, but it was authentic.

Read this for more information: “Deciphering TreasuryDirect’s mysterious gift-box email.”

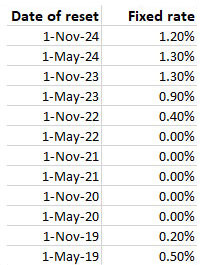

The gift box program is a widely used loophole that allows people with a trusted partner (such as a spouse) to expand their purchases of I Bonds beyond the $10,000 per person limit. The idea in early 2024 was 1) buy gift I Bonds now to lock in the attractive 1.3% fixed rate, and then 2) deliver them in future years when the fixed rate is lower.

We all assumed one thing: You could not deliver gift I Bonds to anyone who had already purchased up to the limit in that year. TreasuryDirect’s email threw that assumption out the window. I called TreasuryDirect to try to get an explanation, and so did hundreds of my readers and fellow Bogleheads. We learned (unofficially):

- TreasuryDirect would like you to deliver gift I Bonds as soon as possible.

- It would be OK to deliver I Bonds to a person who had already reached the purchase cap.

- And … maybe (or maybe not) … the person receiving I Bonds over the limit would be locked out of buying I Bonds in future years, depending on the amount delivered.

- Unspecified “changes” may (or may not) be coming to the savings bond program.

In my case, last year: 1) My wife and I each bought one set of 1.3% I Bonds early in the year, along with two sets each for the gift box. After getting the Treasury’s directive, we successfully delivered those gift box purchases in November 2024.

Now it is January 2025 and I am ready find out: Am I subject to a purchase limitation this year? The answer apparently is “no.”

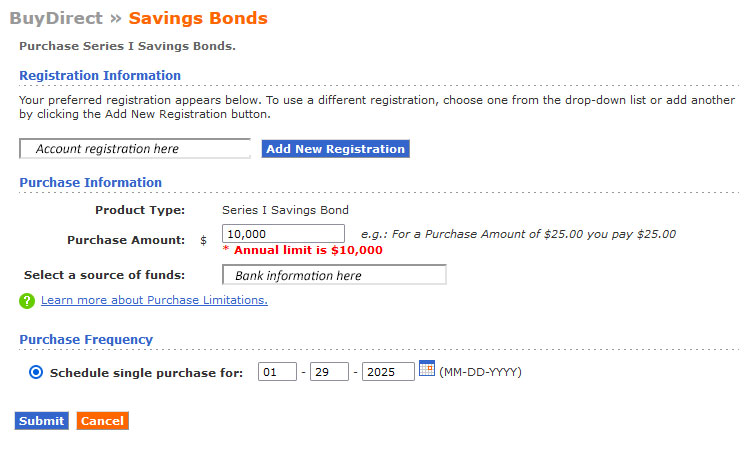

Last week, I logged into TreasuryDirect to place an I Bond order for my wife’s account:

Everything here is totally normal. Note that I set the purchase date for Jan. 29 because I Bonds earn interest for an entire month, no matter the day they are purchased. I clicked “submit,” looked at the review page and clicked submit again.

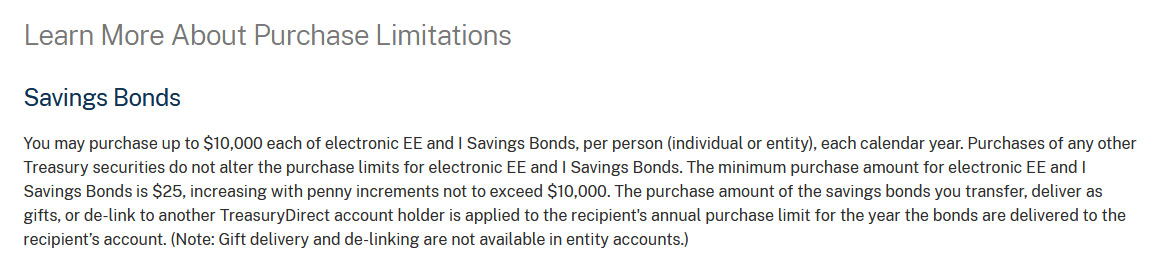

Again, totally normal. No warnings. No alerts. I think this purchase will go through on Jan. 29 as a routine transaction. Also, on the BuyDirect page, I noticed a link to “Learn more about Purchase Limitations.” I clicked and found this:

Notice this key wording: “The purchase amount of the savings bonds you transfer, deliver as gifts, or de-link to another TreasuryDirect account holder is applied to the recipient’s annual purchase limit for the year the bonds are delivered …”

My translation: If you receive $10,000 in gift I Bonds before you make your regular $10,000 purchase, you will not be able to buy more that year. But … if you make your regular purchase first, you can receive additional gift deliveries that year.

Important takeaway: If you are planning to deliver gift I Bonds this year, make sure to purchase your regular allocation before any delivery. Then, it appears, the gift I Bonds can still be delivered.

Also: If you made gift I Bond deliveries over the limit last year, you won’t be locked out of making a regular purchase in 2025. This is NOT official, but it is what I and others have experienced.

When should I buy I Bonds this year?

Although I set up a purchase for Jan. 29 to test my purchase theories, my usual advice would not be to buy in January, unless you feel the need to get the one-year-to-redemption clock ticking.

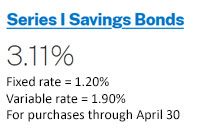

The current I Bond will pay 3.11% nominal for six months. You can do 100 basis points better in a decent money market account or high-yield savings account, for the time being. So there is no rush. Instead, be patient. I Bonds are a long-term investment.

April 10, 2025. We will get the March CPI report at 8:30 a.m. EDT, which will lock in the I Bond’s new six-month variable rate. We will also have a lot more information on whether the fixed rate will be likely to rise at the May 1 reset.

The period from April 10-28 is an ideal time to make a decision: Buy in April or buy in May, or continue waiting?

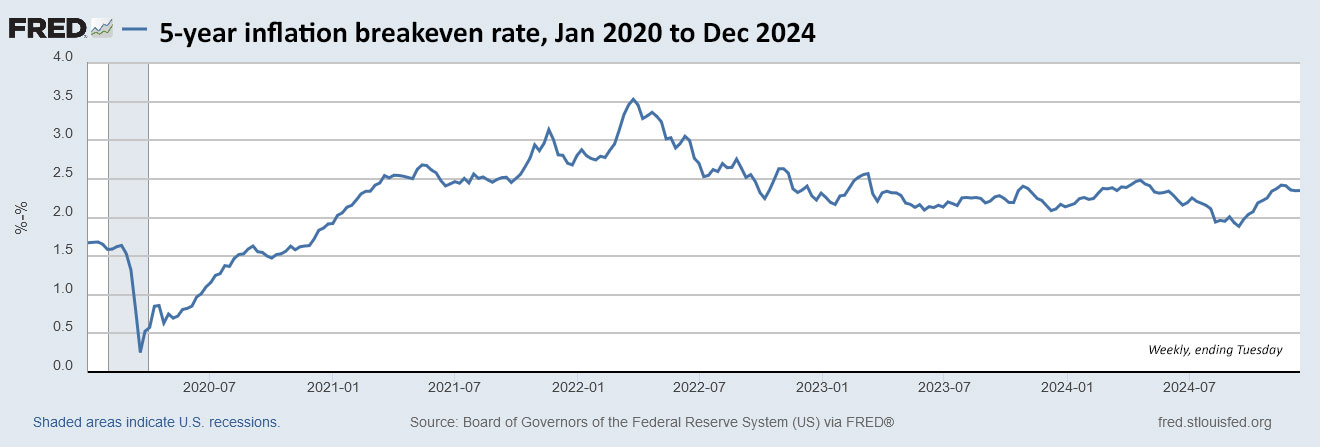

At this point, it looks possible the I Bond’s fixed rate could increase at the May 1 reset. For that to happen, using our back-of-the-envelope theory, the 5-year TIPS real yield would need to average at least 1.92% from November to April. That would get you back to 1.3%. At this writing, the 5-year TIPS is yielding 1.97%.

We won’t know until later this year. It is smart to wait. The variable rate is not a key factor in this decision, unless you want to make a short-term investment. The fixed rate is much more important for a long-term investor.

Oct. 15, 2025. The September inflation report will be issued on this day, locking in the next variable rate, and by then we will have information on the fixed rate reset coming Nov. 1. So the period from Oct. 15-29 is another potential “prime time” for an I Bond purchase.

Why invest in I Bonds at all?

Yes, at this point you can get a better nominal yield on a 13-week T-bill (4.36%) or a better real yield on a 5-year Treasury Inflation-Protected Security (1.97%). Both of those are attractive, safe investments. (And I invest in both.)

I Bonds, however, have unique qualities. They are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures.

Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

With an I Bond purchased today, you are guaranteed to earn 1.2% more than official U.S. inflation, with interest constantly compounding tax-deferred. You can redeem the I Bond after one year with a 3-month interest penalty, or after 5 years with no penalty.

My argument is that I Bonds should be viewed as a cash alternative in the form of a high-quality secondary emergency fund. You can let the principal grow without facing taxes, then after 5 years withdraw money as you need it, paying federal tax on the interest earned.

A lot of shorter-term, yield-hungry investors won’t see the appeal of I Bonds in 2025. That’s fine; there are great short-term options available right now. But many longer-term investors interested in building a sizable reserve of inflation-protected cash will want to buy I Bonds in 2025, up to the limit.

Rolling over 0.0% fixed-rate I Bonds

If you joined the mass movement into I Bonds back in October 2022, when the I Bond’s variable rate was about to reset from 9.62% to 6.48%, you are holding I Bonds with a fixed rate of 0.0% and your composite rate is going to be 1.90% for six months. That’s not a disaster, but many I Bond investors have been redeeming the 0.0% I Bonds and reinvesting the money into 1.3% or 1.2% fixed-rate versions over the last year. Or moving money into other investments.

That was the reason the gift box was so popular in recent years. Investors could redeem 0.0% sets, pay the tax on the interest, and then stash $10,000 into gift-box I Bonds to be delivered in future years. Then the Treasury set off chaos by encouraging these investors to deliver the gift-box bonds as soon as possible.

In the last two years, I have redeemed all our 0.0% fixed rate I Bonds and reinvested the money into the 1.3% or 1.2% versions (as of the scheduled Jan. 29 purchase). This makes sense for me, because I have large holdings in I Bonds and TIPS. Other people, still in the “accumulation phase” of I Bond investing, may want to hold the 0.0% versions and let them continue growing with inflation, tax-deferred.

The rollover process can be a little confusing, based on the limited information TreasuryDirect gives you for each holding. I wrote a guide back in September 2024.

“Just one more thing”

I think Treasury will make changes to the gift box program this year, but even if it doesn’t, I don’t plan to use it again in 2025. Under current rules, it appears that any amount of gift I Bonds can be delivered after an initial $10,000 purchase, Treasury has opened a gaping loophole, but only for people with a trusted partner.

What are your thoughts? Post your ideas and strategies in the comments section below. If you will bypass I Bonds this year, what alternatives are you considering?

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

UrsaTaurus, I have been contemplating similarly, buying long without the expectation of holding to maturity (I will be dead). I…