By David Enna, Tipswatch.com

Today’s 10-year reopening of CUSIP 91282CJY8 — a 9-year, 8-month Treasury Inflation-Protected Security — generated a surprisingly high real yield to maturity of 2.184%, the highest for this term at auction since January 2009.

The auction apparently drew weak demand, with a sub-par bid-to-cover ratio of 2.33. The “when-issued” auction prediction, released just before the close at 1 p.m. EDT, was 2.16%. Investors were not snapping this one up, and that meant a higher real yield than expected.

This TIPS trades on the secondary market, and around 8 a.m. today it was trading with a real yield to maturity of 2.08%. That secondary-market yield climbed to 2.15% just before the auction’s close.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

For today’s investors, the weak demand meant that this TIPS will outperform official U.S. inflation by 2.184% over the next 9 years, 8 months. We haven’t seen an auctioned yield that high for this term since January 2009, when a 10-year originating auction got a real yield of 2.245%.

Here is the trend in market 10-year real yields over the last 15 years, showing the dramatic round-trip to yields surpassing 2.0%:

Pricing

CUSIP 91282CJY8 carries a coupon rate of 1.75% that was set by the January originating auction. Investors got an unadjusted price of 96.249477, which reflects the spread between the auctioned real yield and the coupon rate. In addition, this TIPS will carry an inflation index ratio of 1.01586 on the settlement date of May 31.

With this information, we can calculate the investment cost of purchasing $10,000 par of this TIPS at today’s auction:

- Par value of investment: $10,000

- Inflation index at settlement date: 1.01586

- Accrued principal on settlement date: $10,158.60

- Cost of investment: $10,158.60 x 0.96249477 = $9,777.60

- + accrued interest of $66.91

In summary, an investor purchasing $10,000 par at this auction paid $9,777.60 for $10,158.60 of principal and will receive accruals matching inflation for the next 9 years, 8 months, plus an annual coupon rate of 1.75% on accrued principal.

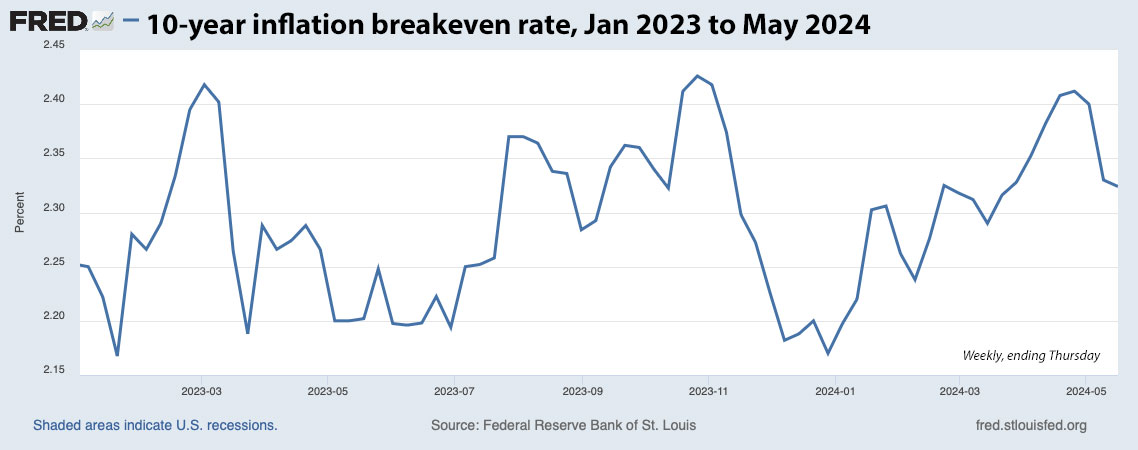

Inflation breakeven rate

With the nominal 10-year Treasury note trading at 4.48% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.30%, a bit lower than expected earlier today. It is significant to note that while the TIPS yield rose about 3 basis points at the auction’s close, the 10-year Treasury note held steady at 4.48%.

The breakeven rate is an indicator of investor expectations of inflation, but should not be considered an accurate predictor of future inflation.

Here is the trend in the 10-year inflation breakeven rate over the last 15 years, showing that today’s rate remains in the higher range, but well below the highs of early 2022.

Thoughts

I didn’t get a lot of feedback on my preview article for this auction, so I suspect there wasn’t a lot of reader interest. But the result was quite good for investors. Keep in mind that just five months ago, this TIPS originated with a real yield to maturity of 1.810%, 37 basis points below today’s result. That’s a big move.

From today’s Reuters report:

The Treasury’s $16 billion auction of 10-year Treasury Inflation-Protected Securities (TIPS) was poorly-received, suggesting investors expect price pressures will decline in the coming years. The high yield was 2.184%, higher than the expected rate at the bid deadline, which meant that investors demanded a premium to take down the note.

The bid-to-cover ratio, a gauge of demand, was 2.33, slightly lower than the previous auction’s 2.35, and the 2.40 average.

Were you an investor? What was your reaction?

Treasury will be auctioning a new 10-year TIPS on July 18. It will be interesting to watch how conditions change in the next two months.

Today’s auction closes out the history of CUSIP 91282CJY8, a TIPS that gave investors a solid first option for filling the 2034 rung of their investment ladders.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…