EE bond’s fixed rate stays at 2.7%; doubling period holds at 20 years

By David Enna, Tipswatch.com

After signaling for a few days that it would hold off to May 1 to announce new rates for U.S. Series I Savings Bonds, the ever-unpredictable Treasury did it early anyway, and it matched my expectations.

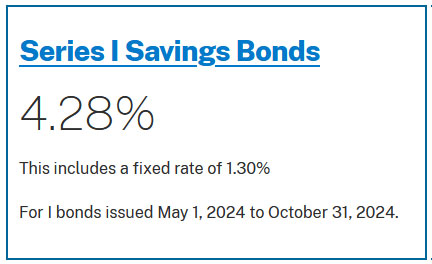

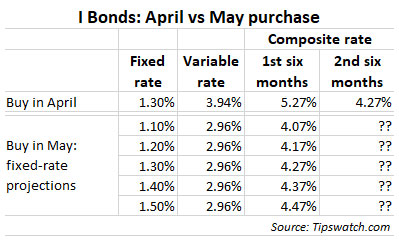

The I Bond’s new fixed rate holds at 1.3% for purchases from May to October, and the composite rate falls from April’s 5.27% to 4.28% for new purchases.

The I Bond’s fixed rate is important for investors. It is permanent and stays with an I Bond until redemption or maturity in 30 years. This new fixed rate only applies to I Bonds purchased from May to October 2024.

The inflation-adjusted variable rate applies to all I Bonds, no matter when they were issued. It changes every six months and the starting date of the change depends on the month you bought the I Bond. This new 2.96% variable rate is based on non-seasonally adjusted inflation from October 2023 to March 2024.

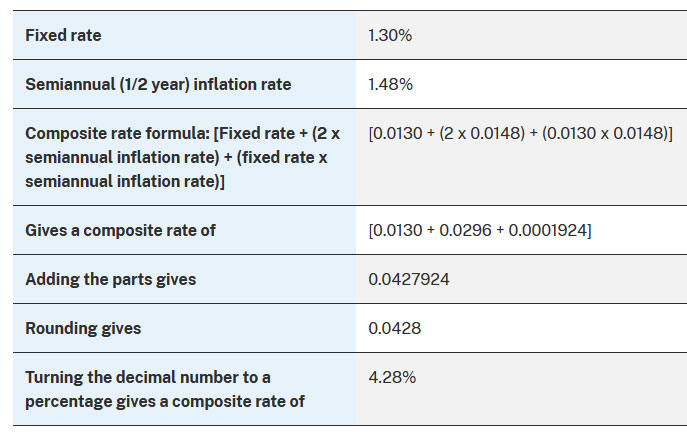

The composite rate is based on a combination of the fixed and variable rates, using this formula:

The new inflation-adjusted variable rate rolls out over time, as I noted. For example, if you bought an I Bond in April 2024, it would earn 5.27% through September, and then transition to 4.28% for six months beginning in October.

Track the history of the I Bond’s variable rate on my Inflation and I Bonds page.

No surprises

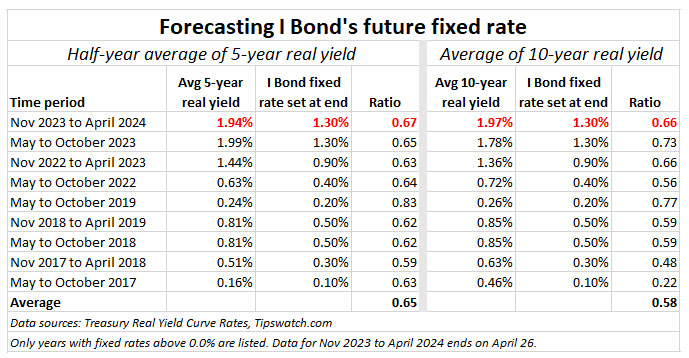

I Bond watchers (like me) had been forecasting that the fixed rate would hold at 1.3%, based on a ratio of 0.65 applied to the six-month average of 5- and 10-year real yields. and then rounded to the tenth decimal point. It was reassuring to see the forecast worked, this time. This gives us a little more supporting data on how the Treasury makes this decision.

Reaction

I have been recommending making your 2024 I Bond purchase in April to lock in both the 1.3% fixed rate and 5.27% composite rate for a full six months. Now that the fixed rate held at 1.3%, that strategy looks solid. Now we can await the November 1 rate reset.

Timing your investments can be important, because I Bond purchases are limited to $10,000 per person per year unless you use your tax return to get paper I Bonds or add to your holdings through gift-box, trusts, or business-owner strategies. Whatever rate is set in November will be available for purchase in January 2025, when the purchase limit resets.

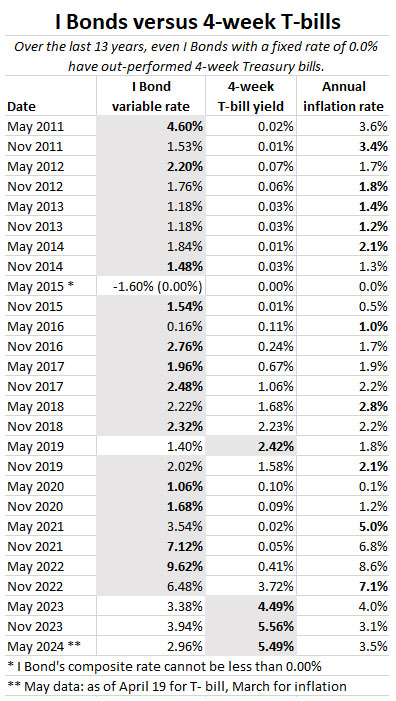

Even though T-bills have yields higher than the I Bond’s new composite rate of 4.28%, these savings bonds still make sense for investors looking to build a large cash reserve that is inflation-adjusted, tax-deferred and totally safe. Right now, it is T-bills for the short-term, I Bonds for the long-term.

EE Savings Bond

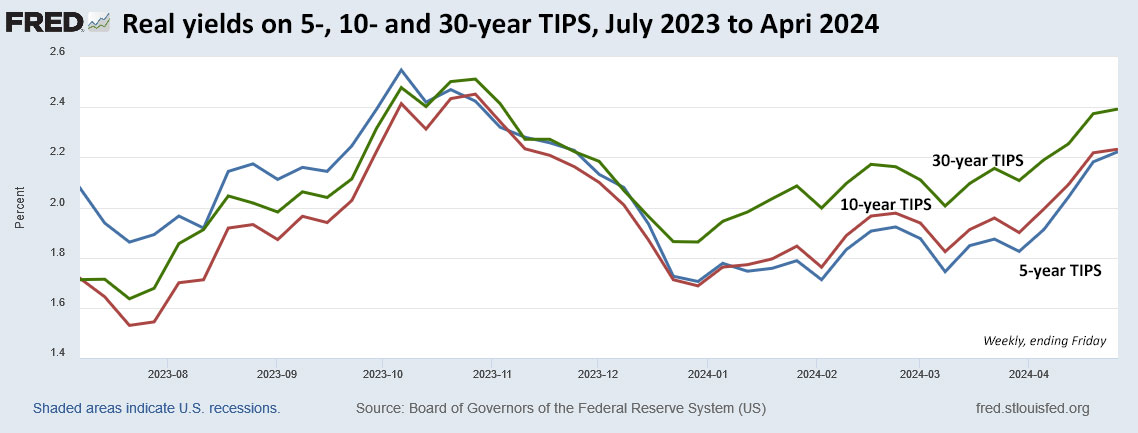

The Treasury decided to hold the fixed rate on the EE Savings Bond at 2.70%, well below the yield of comparable nominal Treasury investments. I had been predicting the rate could rise to 2.8% or 2.9%, based on the trend in yields for the 10-year Treasury note (currently yielding 4.63%).

The Treasury also held the EE bond’s doubling period at 20 years, meaning this savings bond will yield 3.53% compounded if held for 20 years. I had expected that decision, but honestly, it would be more fair to set the doubling period at 18 years, creating an effective yield of 4%.

I doubt there will be much interest in EE Savings Bonds when T-bills are earning nearly 5.5% and the 20-year Treasury bond yields 4.86%. Both of those make more investment sense. Too bad.

What’s your reaction?

Investors are sorting through a lot of issues when considering I Bonds these days. T-bills offer a better rate of short-term return, with no fear of a penalty for early redemption. Treasury Inflation-Protected Securities offer better real returns, but with more complexity and potential market fluctuations.

I suspect most I Bond investors have already purchased their allotment for 2024 and are now ready to sit back and enjoy life.

FYI, earlier today (April 30) I looked on TreasuryDirect and it “appeared” you could still set a purchase for April 30, 2024, which in theory would get the higher April composite rate. Forget it. I have already gotten feedback from a reader that a purchase entered today is getting the May rate.

The Treasury really needed to clarify its wording, which said for several days, “The current rate of 5.27 percent is available until 11:59 p.m. Eastern Time on Tuesday, April 30. The new rate becomes available at midnight.”

That was highly suspect.

Now, on the afternoon of April 30, TreasuryDirect has gone in and changed the wording on its I Bond FAQ page to this bizarre past-tense instruction:

The rate of 5.27 percent was available until 11:59 p.m. Eastern Time on Tuesday, April 30. The current rate of 4.28 percent became available at midnight.

Treasury, you screwed this one up.

Post your ideas and thoughts in the comments section below.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…