If you have been reading this site for a long time, you know what this headline means: I will soon be traveling to some distant place with confusing timezone differences and potentially weak-to-zero internet.

It is so far, in fact, that I will depart on Day One and arrive on Day Three after crossing the international dateline. I will entirely miss Valentine’s Day. And I expect the jet lag to be severe. The trip will last more than three weeks and I won’t have a lot of time to follow financial news.

So expect some lag time, especially in approving comments or responding to questions. But I will try to post news when I can, including a preview of this month’s 30-year TIPS auction.

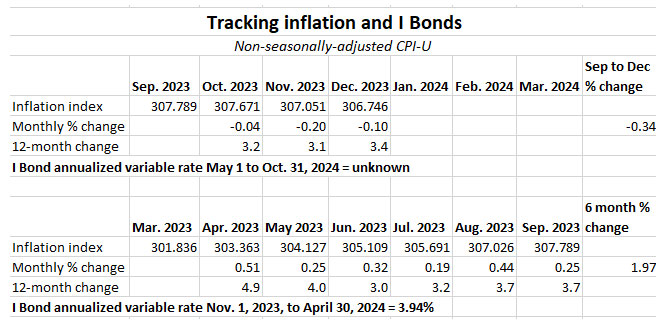

Tuesday, Feb. 13. The January inflation report will be issued at 8:30 am EST. Originally, this wasn’t going to be a schedule problem for me because my departing flight was leaving Tuesday afternoon. Things got shifted around and now I am leaving in the morning, so I won’t be able to post any news or analysis until a layover in Houston.

The forecast for January inflation is 0.2%, according to Barron’s. That is the seasonally adjusted number for all-items inflation, and — if accurate — looks tame enough to keep both the stock and bond markets happy.

I’d expect the non-seasonally adjusted number to come in higher. Last year, for example, official January 2023 inflation was 0.5%, while non-seasonally adjusted rose 0.8%. In January 2022, official inflation rose 0.6%, while non-seasonal was up 0.84%.

Why is this important? Because non-seasonally adjusted inflation will be used to set the new inflation-adjusted variable rate on U.S. Series I Savings Bonds. So far, three months into the 6-month rate-setting period, inflation has been negative, at -0.34%. So January non-seasonal inflation will need to come in at 0.34%, at least, just to get the number to zero.

All of this makes it highly likely that the I Bond in May will get a lower variable rate than the current 3.94%. Possibly much lower. But things can change.

Sunday, Feb. 18. In the morning, I will post a preview article on the 30-year TIPS auction set for Feb. 22. Although I won’t be a buyer (the term is too long for me) this could end up being attractive for the investor who can handle the long maturity date and high volatility.

As of Friday’s market close, the 30-year real yield stood at 2.13%, which I consider attractive. For perspective, here is the trend in the 30-year real yield over the last 14 years. Despite speculation that Treasury yields would plummet in 2024 as the Fed inched toward easing, long-term real yields have remained relatively high.

Click on image for larger version.

This chart is a reminder that the “window” for building a comprehensive TIPS ladder is still open. Real yields remain attractive across the maturity spectrum. Could they go higher? Sure. But I’d expect some “token” rate cuts coming from the Fed sometime this year, especially if inflation remains tame.

Thursday, Feb. 22. The 30-year TIPS auction will close at 1 p.m. EDT, which is 7 a.m. Friday in New Zealand. I’ll probably be at breakfast in Auckland and then embark on the day’s activities. I’ll get something posted, eventually. Don’t expect too much.

After that? Something crazy always happens when I travel, so sorry if I cause an international financial crisis. I might not even be aware it is happening. I’ll be back to the U.S. in time for the February inflation report, to be issued March 12.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

U.S. Series I Savings Bonds are a unique investment because all interest is rolled into principal until redemption, and in most cases, all the compounded earnings are tax deferred until the I Bond is redeemed or matures.

This is good.

And no I Bond has ever matured. I Bonds were first issued in September 1998, so history’s first I Bond maturity will come in September 2028. These early-issue I Bonds from years 1998 to 2001 had incredible fixed rates of 3.0%+, meaning they have generated fantastic returns over the years, in the range of 6.0% to 6.25% annual interest, compounded.

This is good.

What isn’t good?

A rather large tax bill is coming for investors in these early-year I Bonds. When the I Bonds are redeemed or mature, the entire amount of interest will be subject to federal income taxes in that year. (I Bond interest is not taxed at the state level.) Some people might say, “Nice problem to have,” but break-through amounts of income can trigger a series of harsh tax consequences: higher marginal brackets, Medicare surcharges, phase-out of some deductions, and the 3.8% Net Investment Income Tax.

The amounts can be seriously hefty: When I Bonds were first created in the fall of 1998, the purchase limit was $30,000 per person per year, and the Treasury even allowed credit cards to be used for purchases with no fees. (Air miles!) This means couples could buy $60,000 in I Bonds each year in those early years.

This chart shows how a $10,000 investment has grown for each of these early I Bond issues, from September 1998 to November 2002. Investors who purchased $20,000 in a year would need to double these amounts; if the purchase was $60,000 for a couple, multiply the amounts by 6.

Couples who bought $60,000 in I Bonds in November 1999 have already earned $193,896 in interest and that amount could easily grow by another 30% at maturity in November 2029, figuring annual interest of around 6%. That brings the total interest to $252,065 in 2029. Ouch.

This is an extreme example, but I have heard from many readers who did indeed buy $60,000 a year of I Bonds in the early years. That has been a great investment, but the coming tax bill causes worries.

My own example: 2031 is a problem

Many readers have been encouraging me to write on this tax issue, but I’ll admit I have been ignoring it. I figured the problem was years away, and my wife and I could handle the influx of taxable interest by adjusting other income sources in the years of maturity. I had no intention of redeeming my high-fixed-rate I Bonds … until maturity.

But then I took a closer look.

I knew we had $40,000 in early-year I Bonds with high fixed rates, but I didn’t realize that all of our purchases were in the single year of 2001, meaning they would all mature in 2031. Hmmm … problem.

Let’s look ahead to 2031. Both my wife and I will be collecting Social Security, a pension, possibly an annuity, and drawing RMDs from traditional IRA accounts. This $144,700 of extra income would very probably push us into a higher tax bracket, high Medicare surcharges and trigger the 3.5% Net Investment Income Tax. Plus, it is possible that tax rates will be higher in 2031.

What’s the plan?

Reluctantly, I am going to give up the idea of holding these high-fixed-rate I Bonds until maturity. Now my plan is to redeem one-fifth of the total each year from 2027 to 2031, bringing the interest income to maybe $28,000 a year, an amount we can deal with by adjusting other sources of income (such as IRA withdrawals).

In our case, these are still paper I Bonds, stored in a bank’s safety deposit box. I looked into the box recently and double-checked. There are 40 $1,000 I Bonds, all issued in 2001. Because the denominations are each $1,000 original value, it will be simple to redeem eight a year for five years, 2027 to 2031.

The denomination is important because paper I Bonds have to be redeemed in whole, unlike electronic I Bonds, which can be redeemed in $25 increments. TreasuryDirect says: “You cannot cash part of a paper savings bond. A paper savings bond must be cashed for its entire value.”

My bank (Wells Fargo in Charlotte) still redeems paper savings bonds, but some banks no longer offer that service. TreasuryDirect says, “Banks vary in how much they will cash at one time – or if they cash savings bonds at all.” From a recent New York Times article:

Hoping to cash in a paper savings bond that’s been lying around for a few decades? Set aside a lot of time for disappointment. …

The process is only getting harder. In May, the nation’s largest bank, JPMorgan Chase, began imposing a $500 limit on each savings bond cashed for longtime depositors — that’s total redemption value, so including any interest owed. Wells Fargo and Citi place a $1,000 limit on new customers. U.S. Bank has a five-year waiting period before it will cash a bond for a new customer.

Converting paper to electronic

Because banks are balking at redeeming savings bonds, especially in large dollar amounts, another option would be to act now to convert these paper I Bonds into electronic form. This isn’t simple, of course. My wife recently converted a batch for her mother, and the process was tedious and time-consuming. But it worked.

To do this, you must have a TreasuryDirect account (if you are reading this I am sure you do), and then you will have to create a Conversion Linked Account where the converted I Bonds will reside. This page on TreasuryDirect has answers to a lot of questions on this procedure.

Harry Sit of TheFinanceBuff.com wrote an excellent guide to conversions, which you can read here. He notes:

In the usual government fashion, they don’t make it easy. Treat it as a test for how well you’re able to follow instructions.

Once converted, you can go into TreasuryDirect and adjust the ownership registration, if needed.

It is not a fun process and that is why I am hoping my wife will do it for us: She has experience!

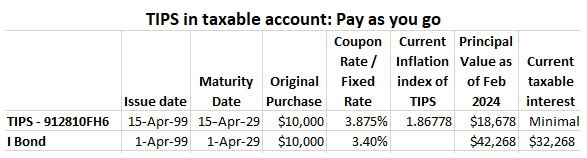

Do TIPS face this same tax problem?

Absolutely not. For example, in April 1999 I bought $10,000 par of a 30-year Treasury Inflation-Protected Security in a taxable account at TreasuryDirect. Let’s look at how it now compares with an I Bond purchased in the same month:

This one chart dramatically shows the difference between investing in a TIPS, which pays out the coupon rate biannually, versus the I Bond, which continuously rolls interest payments into principal all they way to maturity. So even though the TIPS has a higher fixed rate of 3.875%, its current value reflects only inflation of 86.7% over the last 25 years. All the earlier coupon payments — the real yield over inflation — have already been paid out.

Plus, because of the way TIPS are taxed, with inflation accruals getting taxed in the current year, when this TIPS matures on April 15, 2029, there will be only a small amount of tax due — on 3 1/2 months of inflation accruals and the final coupon payment of 1.9375%.

A TIPS held in a taxable account does not create a “tax time bomb.” You pay the taxes as you go. At maturity, taxes are pretty much a non-event.

One more point: The chart demonstrates the benefits of compounded, tax-deferred interest when an I Bond has a very high fixed rate. That April 1999 I Bond is still earning 3.4% above inflation on compounded principal of $42,268. There is no way a TIPS investor could have earned that yield by reinvesting coupon payments in an equally safe investment from 1999 to 2024. For most of that period, real yields have been below 2.25%.

Click on image for larger version.

Final thoughts

If you were one of the fortunate investors to have invested in I Bonds in the early era of 1998 to 2001, congratulations. Now you should take a careful look at your investments and the potential tax consequences of holding to maturity. You will be paying taxes, of course, but you may be able to manage the redemptions to minimize effects on your tax bracket, potential Medicare surcharges and the looming Net Investment Income Tax.

You have time to create a plan because the first-ever I Bond maturity won’t occur until September 2028.

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

One of the “interesting” challenges in dealing with the U.S. government’s TreasuryDirect website comes each January, when you might — or might not — need to go in search of federal tax forms.

If you had transactions in 2023 at TreasuryDirect, with the exception of simply buying savings bonds, you should have already received this email:

The 2-minute video (which was produced several years ago) is actually helpful, and it plays on YouTube, so you can watch it right here:

As the video notes, if you are part of a couple with separate accounts, or if you have linked accounts from converting paper I Bonds, or child accounts, or separate trust or entity accounts, you will need to go to the linked accounts and get separate 1099s. In the case of a spouse, you will need to log out and re-login to that separate account to find the second 1099. Here is what TreasuryDirect says:

It is important to check ALL of your accounts, as a separate Form 1099 will be created for each one. If you have established Custom, Minor-Linked, or Conversion-Linked accounts, you must access each account to print the Form 1099 for that account.

However, if you use your TreasuryDirect account simply to buy savings bonds (I Bonds or EE Bonds) and didn’t redeem any or have any mature in 2023, there will be no taxable transactions and you won’t have 1099s. You will see this on TreasuryDirect’s ManageDirect page:

TreasuryDirect is NOT going to mail you these forms. You need to hunt them down.

Important: Once you are inside the account section of TreasuryDirect, never click on your browser’s back button. If you do, you will be booted out of TreasuryDirect and you will have to log in again. To navigate, either click on the top row of tabs or click “return” at the bottom of most pages.

Here is the basic step-by-step process for finding each set of 1099s:

Log into your TreasuryDirect account on this page. Click “Next.”

Enter your account number.

After you enter the account number, you will get a message that a verification code has been sent to the associated email address. Open the email, copy the code and paste it in the box. Click “Submit.”

Enter your password and click “Submit.”

Now you are on your MyAccount page on TreasuryDirect. From here you can click on your Investor InBox in the upper navigation to see further instructions. The message will be titled “Tax Statement Notification.”

Next, click on the “ManageDirect” link in the upper navigation. Under the heading, Manage My Taxes, select the link for the 2023 tax year. Then click the link: “View your 1099 for tax year 2023.” (Make sure to select 2023, not 2024!)

At this point, you may get a huge listing of all of your interest payments, savings bond redemptions, potential capital gains and original issue discount accruals for Treasury Inflation-Protected Securities.

TreasuryDirect does not offer an easily printable .pdf version of this form. To print it, click anywhere on the browser page and hit CONTROL P on a PC or COMMAND P on a Mac. This should open up a dialog to print the pages. (Mine was 12 pages long.)

Print the 1099.

Don’t have a printer? You can copy the entire text of the 1099 and paste it into a text or Word document. Save that file for reference when you fill out your tax return.

At the bottom of the page, click on “Return.” Repeat the process for any additional spousal or linked accounts.

Examine the 1099

There is a lot to see here, and you don’t want to miss anything that needs reporting to the IRS. On a 1099 from any brokerage or bank, everything is nicely organized and summed up, with clear references to the proper boxes on your tax filing. Not so with TreasuryDirect. In fact, this 1099 is actually a collection of 1099 forms, each with special purposes.

Form 1099-INT Interest Income

If you invested in any T-bills, Treasury notes or bonds, TIPS or redeemed savings bonds in 2023, you are going to see all interest-paying transactions listed here. In 2023 I was rolling over staggered 13- and 26-week T-bills at TreasuryDirect, plus had a collection of TIPS, plus redeemed a couple 0.0% I Bonds, so my list was enormous: 44 items.

At the bottom of this long list, way at the bottom, is the total. Scroll all the way back up to the top to see that this total is Interest On U.S. Savings BondsAnd Treas.Obligations and it goes in Ref. Box 3 on the federal fax form when you are filling out the section for 1099-INT. Here is the definition of Box 3:

Shows interest on U.S. Savings Bonds, Treasury Bills, Treasury Notes, Treasury Bonds and Treasury Inflation-Protected Securities (TIPS). … This interest is exempt from state and local income taxes.

You want to make sure the interest gets recognized as coming from U.S. Treasurys, because it will be free of state income taxes.

If you had any proceeds withheld for tax purposes (highly unlikely) those totals will be listed in column 5 of this section.

Form 1099-B Proceeds from Broker and Barter Exchange Transactions

There are several sections to for 1099-B and I generally have just a few transactions listed here. To me, this seems like a relatively new part of TreasuryDirect reporting, which shows an Accrued MarketDiscount on longer-term investments that matured in 2023.

I had three TIPS mature in 2023. Two had $0.00 “gains” reported here and one had $210.47. I am assuming this resulted from an initial discount at purchase. TreasuryDirect says these proceeds should be reported to the IRS on form 8949, part D, which is for a long-term gain, but the gain goes in Box 1f, which is for an adjustment to a gain.

I am generally baffled by Form 1099-B, but the amount of taxable long-term gain is so small I just report it and forget it.

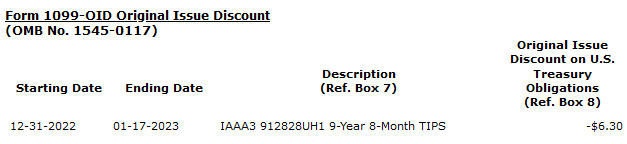

Form 1099-OID Original Issue Discount

This is a very important section for investors who hold TIPS at TreasuryDirect. The 1099-OID lists annual inflation accruals for every TIPS held in the TreasuryDirect account in 2023. These inflation accruals are federally taxable in the year they were earned, even though they were not paid out but just added to principal.

Long-time investors in TIPS are familiar with the 1099-OID, but new investors at TreasuryDirect need to pay heed to this section and report it on their federal tax return. In my example here, I am including the first amount because it is negative for the half month before CUSIP 912828UH1 matured in January 2023. So yes, these OID numbers will be negative in times of deflation.

You won’t often see a negative number for any TIPS you held for a full year. But in this case, the holding matured on January 15, 2023, so the deflationary period was for only a half month. TreasuryDirect notes:

Report this amount as interest income on your federal income tax return. … This OID is exempt from state and local income taxes. If the number in this box is negative, it represents a deflation adjustment.

Final thoughts

It should be obvious at this point that I am no tax expert, so nothing you just read should be considered tax advice. Still, getting these 1099s from TreasuryDirect is EXTREMELY IMPORTANT. You are going to get one email with a fairly cryptic message. That’s it. Nothing in the mail. No easy-to-read tax summary like you receive from your broker. It’s up to you to go to TreasuryDirect, find the 1099s, print them, decipher them and report them on your tax return for 2023.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Did it work out well? Yes. But is it worth the risks?

By David Enna, Tipswatch.com

For a few years now, I’ve been getting questions about seemingly lavish high real yields on Treasury Inflation-Protected Securities that are nearing maturity. My usual response is that these real yields — while technically accurate — get exaggerated as maturity nears and only one coupon payment remains.

For example, in late August 2023 readers spotted this TIPS, CUSIP 912828B25, maturing Jan 15 2024, just 4 1/2 months later.

Its quoted real yield was 4.080%, and at the time U.S. inflation was running at 3.7%, so some readers extrapolated a gorgeous return of 7.7% on this TIPS, in just 4 1/2 months. At the time, a 17-week T-bill was yielding about 5.5%.

But that isn’t the way it works. Only 4 1/2 months of inflation accruals remained so the end result for the TIPS was highly likely to be somewhere close to the 17-week T-bill, I figured. Time for an experiment! My thinking: I could get a better understanding of these short-term TIPS by investing in one.

To test the theory, on Aug. 30, 2023, I purchased $12,000 par of CUSIP 912828B25 on the secondary market at a real yield of 4.07% and a price of 98.73437. Because this TIPS had a high inflation index of 1.30749, the investment cost me $15,491.30 after the price discount, plus $12.52 in accrued interest.

Because this purchase was starting out with principal of $15,689.88, I was getting an immediate gain of 1.28%, plus I knew I would get 0.3125% interest at final maturity, for a total of 1.59%, which translates to an annual return of about 4.2% before any inflation accruals.

And there was the key to this whole investment: How much non-seasonally adjusted inflation (or very possibly, deflation) would we see before the January 15, 2024, maturity? Inflation accruals for TIPS are set by non-seasonally adjusted inflation two months earlier. So I already knew one month of accruals, for September:

September: accruals of 0.19%, based on July inflation.

October: ???, ended up being 0.44% based on August inflation

November: ???, ended up being 0.25% based on September inflation

December: ???, ended up being -0.04% based on October deflation

January: ???, ended up being -0.10% based on half of November deflation

In this case, the first three months added 0.88% to my principal and things were looking good. But the next 1 1/2 months subtracted 0.14% from my principal. I expected this to happen, because non-seasonally adjusted inflation often goes negative in November and December.

Verdict: This time, it worked.

My goal was to use this investment maturing Jan. 15, 2024, to help fund my next TIPS purchase … the new 10-year TIPS that was auctioned last week with a real yield of 1.81%. Would I end up doing better buying this TIPS, or just investing in the 17-week Treasury that would mature on Jan. 2, 2024?

Here is the result:

I adjusted the investment totals to come up with a similar ending number around $15,850. The TIPS ended up being the winner in this contest, with a nominal annualized yield of 6.21% versus 5.52% for the 17-week T-bill. That’s 69-basis-point bonus, but in actual dollars it amounts to about $75, or about one-third the cost of one trip to Costco.

This TIPS had an ending inflation index of 1.31741, 0.759% higher than the starting index of 1.30749. That is annualized inflation of about 2.02%. And remember, I figured with the final coupon payment the annualized nominal yield would be 4.2% before inflation or deflation. The actual return was 6.21%. Do the math: 4.2% + 2.02% = 6.22%, so you can see roughly how the real yield actually topped 4.0%, as advertised.

Final point: Is it worth it?

Any time you buy a TIPS with just a few months to maturity, you will be highly likely to be buying a large amount of additional principal that is not guaranteed to be returned at maturity. In this case, I was buying 30.7% extra principal at a cost of about $3,504. If deflation had struck in August and September, I would have gotten a lousy return versus the 17-week T-bill.

Deflation is more of a risk in the short-term (especially nearing the end the year) than the long term. In the future, I would be a lot more likely to buy the 17-week T-bill, which involves zero risk and a certain return at maturity.

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Back on Jan. 23, 2014, the Treasury auctioned a new 10-year TIPS, CUSIP 912828B25, generating a real yield to maturity of 0.661% and a coupon rate of 0.625%.

That doesn’t seem exciting, but at the time this was a promising result, coming in the wake of nearly three years of aggressive quantitative easing by the Federal Reserve. The auction result of 0.661% was the highest real yield at auction for any 9- or 10-year TIPS in nearly three years.

In my preview article for the auction, I noted that real yields had slipped a bit from 2013 highs, but this new TIPS still looked attractive. At the time, however, I wasn’t a buyer. (I did buy this TIPS much later; more on that coming up.) My only TIPS purchase in 2014 came in the October reopening of the July 10-year, CUSIP 912828WU0, with a real yield of 0.601%.

So how did CUSIP 912828B25 do as an investment? Pretty well, actually, when measured against the 10-year Treasury note available at the time, with a nominal yield of 2.78%.

The new TIPS had an inflation breakeven rate of 2.12%, meaning it would outperform the nominal Treasury if inflation averaged more than 2.12% over the next 10 years. The result: Annual inflation averaged 2.8% over that decade, making CUSIP 912828B25 a winner, by a large margin of 68 basis points a year.

The Eyebonds.info summary page for this TIPS shows that it generated a nominal annual return of 3.445%, well above the nominal Treasury’s 2.78%.

The lesson here is that even a mundane real yield of 0.661% can be a good investment if inflation trends work in the investment’s favor.

Catching the inflation wave

I’ve been tracking results for 5- and 10-year TIPS for a long time. For many years, the news wasn’t great. We recently completed a decade-long period of inflation running at less than 2.0%, causing TIPS to do poorly versus nominal Treasurys. Then in 2021 we entered an era of much higher inflation, and so TIPS maturing recently have done well, getting a big boost from inflation in the last three years.

To view this chart at a glance, the annual variance number in the last column shows how the inflation breakeven rate compared to actual 10-year annual inflation. When the numbers are green, a TIPS was the superior investment. When they are red, the nominal Treasury was the better investment.

The next decade could be entirely different. Never predict the future decade based on the performance of the past decade.

My later purchase of CUSIP 912828B25

Because I was getting a lot of questions about the lavishly high real yields you often see on short-term TIPS, I decided to do a 4 1/2-month experiment to see how CUSIP 912828B25 would perform versus a 17-week Treasury. You can read the details here: “Experiment: Let’s try out a very short-term TIPS“.

I will be posting an article Wednesday morning revealing the result of the experiment. Here is the link.

Notes and qualifications

My TIPS vs. Nominals chart is an estimate of performance.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

2.5% to 2.7%+ Real yield above inflation on 20 to 30-year TIP bonds.