And of course, because it’s TreasuryDirect, it’s complicated.

By David Enna, Tipswatch.com

If you hold Treasury issues of any kind (except possibly Savings Bonds) at TreasuryDirect, you should be getting a friendly email this week. It will say something like:

TreasuryDirect 1099 Statement Information

Dear Account Owner: Please check the Investor InBox section of your TreasuryDirect account and all linked accounts, if applicable, for important tax information.

OK, so there you go. No clickable link, which is probably a good idea in a time of escalating phishing attempts. But there is one link in the email, to a 2-minute video explaining how to find and print the 1099s for your main and linked TreasuryDirect accounts:

The video is fine, but it does end abruptly in the middle of a sentence, and makes no attempt to explain what you will actually see in the 1099s. If you hold Treasury Inflation-Protected Securities at TreasuryDirect, or if you have had maturing TIPS, there could be some complications. I’ve had many readers tell me they couldn’t find the 1099-INT for TIPS, and that they didn’t even know a 1099-OID exists, or what it is. These forms are there.

TreasuryDirect is NOT going to mail you these forms. You need to hunt them down.

Note: If your only holdings at TreasuryDirect are I Bonds or EE Bonds, and you didn’t have any matured or redeemed savings bonds in 2022, you won’t find 1099s for that year. Those savings bonds earn tax-deferred interest by default, and so there are no tax forms unless you redeemed an issue or had it mature.

1099 hunt: Step-by-step process

1. Log into your TreasuryDirect account. Simple enough, right? Yes, if you remember your password and can clear the two-step verification.

2. Go to ManageDirect. Once you log in, you will notice you have a message in your Inbox, which informs you the 1099s are available:

To view a summary of your taxable transactions, and to print your 1099, please access your account and go to the ManageDirect tab, then click the appropriate tax year under the heading “Manage My Taxes.”

Important: Once you are inside the account section of TreasuryDirect, never click on your browser’s back button. If you do, you will be booted out of TreasuryDirect and you will have to log in again. To navigate, either click on the top row of tabs or click “return” at the bottom of most pages.

To get to ManageDirect from the account home page, click on “ManageDirect” in the top row of tabs:

3. Click on ‘Year 2022’ in the Manage My Taxes section, bottom left.

This is what the ManageDirect page looks like. Click on “Year 2022” under “Manage My Taxes.”

4. Click on ‘View your 1099 for tax year 2022’ When the Year 2022 page opens, you will see a lot of information about every transaction in 2022, but what you want is the 1099, not this listing. So find the tiny little link to your 1099 and click.

5. Successfully respond to the security question. Yes, one more step before you get to the 1099. You have to answer the security question. This can be difficult if you created your account 20 years ago and your taste in movies has advanced since then …

Sometimes the security question is: “You were born in what city?” … A bit easier to answer.

6. Bingo! Your 1099 now opens. But this is not like any 1099 you’d see from any other bank or brokerage. It is long-winded (mine was 11 printed pages) and not really crystal clear. But thank God the form complies with “Paperwork Reduction Act Notices.”

7. Print it. There is no print button on this page. To print it from your computer, click on the page and then do a “CONTROL P.” (Or on a Mac, “Command P.”) That should open your computer’s print menu. If that doesn’t work, you could copy the entire thing into a Word document and then print that.

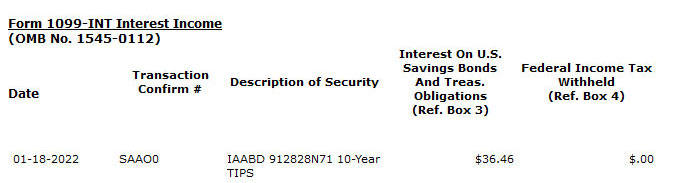

Form 1099-INT

If you hold TIPS at TreasuryDirect, you will have at least two 1099s included in these pages: 1099-INT for the coupon interest you earned, and 1099-OID for taxable inflation accruals you received in 2022. Here is what the opening lines of form 1099-INT look like.

At the very end of the 1099-INT listing, you will see the total. On your tax return, this will be entered into Box 3 on the form for 1099-INT. Correct me if I am wrong. The definition of Box 3:

The information displayed above in the 1099-INT section shows interest paid to you for tax year ending 12-31-2022. … Shows interest on U.S. Savings Bonds, Treasury Bills, Treasury Notes, Treasury Bonds and Treasury Inflation-Protected Securities (TIPS). … This interest is exempt from state and local income taxes.

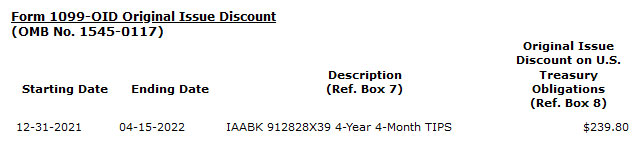

Form 1099-OID

Inflation accruals for TIPS held in a taxable account are taxable in the year they were accrued, even though they were not yet paid out. These accruals are tallied in 1099-OID, with OID standing for Original Issue Discount. These are listed in another section of the 1099, and here is what the top looks like:

At the bottom is the total, which is entered into Box 8 of the 1099-OID section of your tax return. And here is the TreasuryDirect definition:

Original issue discount (OID) is the excess of an obligation’s stated redemption price at maturity over its issue price. OID on a taxable obligation is taxable as interest over the life of the obligation. If you are the holder of a taxable OID obligation, you generally must include an amount of OID in your gross income each year you hold the obligation.

For Box 8: Shows OID on a U.S. Treasury obligation for the part of the year you owned it. Report this amount as interest income on your federal income tax return. … This OID is exempt from state and local income taxes. If the number in this box is negative, it represents a deflation adjustment.

Form 1099-B

If you had a Treasury issue that matured in 2022, you may find tax information in this section, as I did for a TIPS that matured April 15, 2022. I bought that TIPS at a Dec. 21, 2017, reopening. It had a discounted price of $98.96 for $100 of value. So apparently this triggered a very small long-term capital gain. Here is how TreasuryDirect shows this, with the amounts hidden:

TreasuryDirect says these proceeds should be reported to the IRS on form 8949, part D, which is for a long-term gain, but the gain goes in Box 1f, which is for an adjustment to a gain. All of this is a bit of a mystery to me and I don’t recall getting a 1099-B in the past. But the amount is quite small. I’ll let TurboTax handle this.

What about a conventional brokerage?

I have no idea how forms 1099-INT and 1099-OID for TIPS are handled at a typical brokerage, because all my TIPS holdings at a brokerage are in a tax-deferred account. If others have information, provide it in the comments section below.

Final thoughts

It should be obvious at this point that I am no tax expert, so nothing you just read should be considered tax advice. Still, getting these 1099s from TreasuryDirect is EXTREMELY IMPORTANT. You are going to get one email with a fairly cryptic message. That’s it. Nothing in the mail. No easy-to-read tax summary like you receive from your broker. It’s up to you to go to TreasuryDirect, find the 1099s, print them, decipher them and report them on your tax return for 2022.

Happy hunting.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi David. Thanks for this super helpful article. I was wondering if the 1099 for the savings bonds lists both names if you have an “or” or a “with” registration with another person on the bond, or just the first named person.

Would you have any information about this?

Best regards, Jill

TreasuryDirect accounts are assigned to a single Social Security number, and the 1099 comes with the name of the principal owner. If you have two accounts (one for each spouse) then you need to log into the matching account to collect the second 1099. If you own only savings bonds in TreasuryDirect, and you haven’t redeemed any, you will not get a 1099.

I have EE bonds from the ‘90’s in Treasury Direct that are maturing and I am redeeming them. The tax section shows “no taxable transactions” when I look for a 1099. I thought these were taxable upon redemption. What am I missing?

These were paper EE Bonds you converted to electronic form? And then you redeemed them inside TreasuryDirect in 2023? You should have a 1099. But I suspect that your converted EE Bonds are held in a linked “conversion” account and you need to switch to that account to see the 1099. You should see the link to that conversion account on your account homepage, listed in “Linked Accounts Information” at the bottom of the page.

That was it. You da man. They sure don’t make it straightforward. Thanks!

Hello David – I know you are not a tax professional but I hope you can clarify this for me: coupon payments and the inflation adjustments are not subject to state income taxes, however if I purchase a TIPS on the secondary market at a discount to par (example: $90 for $100 par) would the $10 gain at maturity be subject to state taxes? Thank you!

I’ve never sold a TIPS before maturity, so I don’t know the answer. I’ve had quite a few mature at TreasuryDirect and ended up (not often) having very minor capital gains to report.

Hi David – Have you written anything about when it might be advantageous to switch from paying taxes on I-bonds until cashing them in to paying them annually? I read that I would have to pay all the taxes that I have been deferring until now. I recognize that one would have a lumped tax bill that first year of doing this. I am considering this as I have a bit of control now over some of my taxable income. I thought this might not be as bad as having to pay taxes on 30K nominal of maturing I-bonds year after year when my wife and I would also be drawing Social Security and hitting RMD age.

It’s a good question. No I Bonds have ever matured, and the first ones to mature will be in 2028. But you wouldn’t want to give those early I Bonds up because they have fixed rates of 3%+ and are very valuable. The first I Bonds I own to mature will be in March 2031, with a fixed rate of 3.4%. Those have already tripled in value, but my plan is to incorporate the interest earned into my income plan for 2031. I set a target income goal for each year (since we are retired) and I pay estimated taxes.

There is no correct answer on this, but I wouldn’t want to give up I Bonds with very high fixed rates if I could avoid it.

Hi David I wasn’t clear. I am not cashing in the bonds, rather I am asking about the disadvantages or advantages of paying the taxes annually rather than at maturity. I am trying to figure out if it is better to pay a lump sum now rather than later when we would be both on Social Security and might have some problems with the tax torpedo. Thanks for letting me know that you haven’t addressed this. I could not find anything on ii on the internet, either.

Sam, sorry I misunderstood your question. Some people do pay taxes on interest annually, but this is complicated because TreasuryDirect won’t give you a 1099-INT until you redeem or the I Bond matures. So you will need to keep track of all yearly payments and report them when you redeem or let the I Bond mature. The IRS has instructions in this document: https://www.irs.gov/pub/irs-pdf/p550.pdf (starting at the bottom of page 7) The instructions say you can switch to the yearly method, but in the year you change you need to report all interest accrued to date. And then you have to stick with the yearly method, unless you get permission from the IRS to switch back.

Can you explain how to change my email address in my treasury account? Treasury sends emails to my old email address which I cannot access anymore.

If you have two-step verification that requires a code sent to your email, then your only option would be to call TreasuryDirect and have them walk you through this. But if you can successfully log into your account, then click on the Account Info tab on the top row of links. You will then have to answer one of your security questions. At that point, you can try to change your email address and click submit.

Thank you for your answer. I guess my only option is to call them & wait for hours for treasury to answer.

This article is SO helpful. Thank you David for helping “Everyman” to navigate these topics.

I’ve always bought TIPS in our IRAs (no tax hassles), but prior to reading this, i had always assumed Treasury Direct would send us 1099s in the mail when we redeem our iBonds. Now i know better, and have saved this article in my iBond file so i can refer to it when we’re “old” and cashing out of iBonds.

You really are a shining star for sharing all of this info/knowledge.

I once asked our financial advisor for info on TIPS and iBonds, and he mumbled and scoffed… as if he didn’t know the answers to my questions but definitely didn’t approve. I’ve since observed that advisors almost universally steer clients away from TIPS and iBonds (probably because they don’t make any money selling them).

With the knowledge i’ve gained over the years — in large part from your website — i’ve dumped our advisors and now manage everything on my own. The advisors always said there is no way to keep up with inflation other than risking your money in stocks. And here we are now getting very safe returns of inflation plus 1+ percent in TIPS.

Of course it’s not a growth strategy, but it’s a safe and smart wealth preservation strategy for the sizable chunk of our portfolios that we want in inflation-protected fixed income.

Could not have done it without you. Thanks again !!

Thanks for your kind words. Asking a financial adviser about I Bonds — especially when they were paying 9.62% for six months — is a pretty good test of the quality of advice you are getting. If the adviser criticizes the idea, you learn something: Time to shop for a new adviser. I have talked with many advisers who do actively recommend I Bonds and keep them out of the assets under management fee structure.

I’d like to report the interest accrued on my I-bond each year instead of the total amount many years from now when the bond matures as is permitted. But…nowhere on the treasurydirect site can I find how much interest accrued last year. When I checked last fall six months after purchase, the value was shown as 10,256; now it shows 10,400. How much accrued in 2022 and how much in 2023 I have no idea. Obviously there is be no 1099 as the bond hasn’t matured. Any clues on where accruals can be found on the Treasury site? Or do I just pick a number ($400 or less) to report and keep careful track of what I report each year?

This isn’t going to be easy, but yes, you will need to keep detailed records of interest reported for each year. You are not going to get a 1099-INT from the Treasury until the I Bond is redeemed or matures. TreasuryDirect suggests using the Savings Bond Calculator (https://www.treasurydirect.gov/BC/SBCPrice) to figure the interest to report, but warning: that tool will not show you the last three months of interest until you’ve held the I Bonds 5 years. You can also check your accrued totals at the end of the year on the TreasuryDirect site, but again, that will not show the last three months of interest. At any rate, you will need to know the exact totals for each end-of-year date, so you can tell how much you earned each year, and then keep accurate records of the interest you reported, and the taxes you paid. This IRS form: https://www.irs.gov/pub/irs-pdf/p550.pdf has a section on U.S. Savings Bonds, beginning on page 7.

And by the way, you need to use the SAME reporting method for all Savings Bonds you own.

Thanks! That was very helpful and tells me what I need to know and do.

Here’s a heads up for those holding converted bonds in a separate “My Converted Bonds” account. You can transfer these converted bonds to your main Treasury Direct account via the Manage Direct tab within your My Converted Bonds account, then click on “transfer securities”. As long as you are transferring your converted bonds to your main account with the same owner name and social security number, it is not a taxable event. Once you’ve transferred out all your converted bonds to your main account, this annoyingly separate converted bonds account will disappear.

Ho boy, what have I gotten myself into? My taxes for the last several years were extremely boring, but this will make me have to pay attention.

Obviously, you’re not a tax lawyer, but if the following is blatantly wrong, please correct me:

The 1099-INT Box 3 (interest on bills + coupons for notes/bonds) and 1099-OID Box 8 (value adjustments for TIPS + under-par purchase for maturing notes/bonds) are all just interest, and all of it goes on the line for “interest” on the federal 1040, and none of it is taxed at the state level.

(thank goodness I’m not intending to futz around with any transactions that would result in me having to understand that 1099-B section)

The amount goes into box 8 and this is what TurboTax says about box 8: Original issue discount on U.S. Treasury obligations: This represents taxable interest on the federal income tax level but is typically tax-exempt interest for state and local income taxes. This flows through to the taxable interest line on your federal tax return.

When you say “The amount goes into box 8”, which amount and box 8 where? Are you just referring to the OID part?

Correct. Box 8 in the 1099-OID form. https://www.irs.gov/pub/irs-pdf/f1099oid.pdf

Thanks David. This was very helpful.

Dave

I need help. I have wanted to follow your tipswatch blog but when I put my email in the box top right and hit “Follow” nothing happens. I get no email notifications. Nothing in my spam folder. Can you or Sony help me?

Sorry this is happening. I have no idea if it happens to others, but no one else has ever complained. You can follow me on Twitter, if you use Twitter, (@tipswatch) and I always post new content there.

Thanks. This will be helpful as I bought I bonds for my kids last year and am going to report the interest on them annually.

Really? I thought interest is not taxable until it is redeemed?

For kids if you declare the interest yearly it falls under the kiddie tax so $1100/year or so tax free. (I forget the exact amount)

Thanks, that’s a good idea. Do you file a tax return for them or is there a line on your return to do that?

You technically don’t have to file a return for them, since the interest is below the $1150 threshold (in 2022), but the IRS may raise a red flag if bonds are cashed out with five figures of interest and no corresponding return.

Thanks for the reply. So this would be a separate return for the child?

Yes, you file the return on behalf of the child and sign on their behalf since they can’t legally sign. The instructions are in IRS Publication 929.

Max, the pay-as-you-go strategy is always an option. It takes tedious record-keeping, but it is a smart strategy if the taxpayer is a child and has little other income, so no tax will actually be due.

Thank you, David. I did not know that was an option but it is good to know.

Use a broker for buying and selling Treasury bills, bonds, notes. You can easily sell if you cannot hold to maturity (you can not sell Treasuries with Treasury Direct). I buy at auction and generally hold to maturity. I use Schwab. No commission to buy or sell Treasuries. Vanguard is similar. Vanguard is better than Schwab in that it uses a high yielding money market fund for its settlement fund. But Vanguard has some serious problems with its web site. So I won’t use them until those issues are resolved.

I only use Treasury Direct for savings bonds because I have no other choice. I don’t like playing hide and seek on poorly designed web sites. I also don’t like web sites that crash at the times you need them to be functioning. I don’t buy TIPS but brokers offer them.

Agree with you. Only problem is Vanguard doesn’t offer the reinvestment option like Treasury Direct, even though TD limits them to 2 years.

You can automatically reinvest Treasuries with Schwab, but I choose not to. There was a good discussion about automatic reinvesting on this site a few months ago. Sometimes CDs are a better choice than Treasuries, and sometimes I prefer shorter or longer term Treasuries. It just depends on what is happening in the financial world when my Treasury or CD matures.

Might be time for me to switch to Schwab. I find the reinvestment option necessary.

Just to be clear, by automatically reinvest, I meant automatically roll over at maturity. Which means another bond will be bought right after the existing bond matures. I have seen that option for shorter term bonds at Schwab. I don’t use it. Call Schwab first and ask what Treasuries (6 month, 1 year, 2 year, etc) allow automatic roll over at maturity.

As for “reinvesting”, as in automatically reinvesting interest like CDs, well, Treasuries do not work like a CD. In other words, Treasuries do not compound their interest rate. Interest always go to the settlement account and is paid every six months on longer term Treasuries. If you buy a six month Treasury, interest goes into settlement the day of purchase. I immediately put that in a higher yielding money market fund, now about 4.27%. So that is kind of like reinvesting interest on a CD in that it increases the interest rate from say 4.87% APY to just over 5% APY. (As I mentioned, Vanguard puts the interest directly into their high yielding money market fund which saves a step, but their web site is messed up).

Brokerage money market funds do allow reinvestment of interest, like a CD. They pay interest once a month.

I have a non-zero value in “Bond Premium on Treasury Obligations” I entered it in box 12 and my tax software seemed to have no problem with it but what is it?

I read the IRS description for box 12 and I have no idea what they are talking about.

I’m guessing, but maybe something about reduction of basis? There’s a section of Pub550 titled “Bond Premium Amortization” and it sounds like perhaps there is some optional way of deferring when the interest from bond premium is taxed over the life of the bond that you can choose to invoke. But again I’m guessing, and I’m neither a lawyer nor an accountant, let alone a tax professional of any kind.

Yes, in this case, the default treatment will work.

Thank you. Very helpful. Now, For TBILLS, etc. is there an easy way to reconcile my book entries to the Treasury Direct 1099s? Do you recommend recording the securities at cost, or par and recognize the interest right away? Any suggestions?

I had several T-bills mature in 2022, which I bought at originating auctions. The 1099-INT reports these as interest and so that is how I am going to handle it for tax purposes. In my own investment records, I just keep track of the par value, since that is what will be paid at maturity.

Thank you for your help with your wonderful site. Tracking the interest with the TBills can get confusing to track, especially when you buy in one year, the security matures the next year, and is reinvested. I wonder why Treasury Direct doesn’t treat the TBills, etc., like a bank CD, where you buy at PAR, and the interest is paid upon maturity.

VERY well done David. Treasury Direct might have more clients if they had you disseminating information.

What if I have a paper Series EE bond that matured after 30 years at the end of 2022 but I waited until January 2023 to redeem it? Will there be a 1099 there now for 2022 or next year at this time for 2023 or no 1099 there because it will come from the bank where it was redeemed in one of those years?

If you have a paper EE Bond mature (as I did in July 2022) the bank where you cashed it will mail you a 1099-INT. At least mine did. Technically, you owe income tax in the year that the savings bond matures. I am not sure how your case will be handled.

Extremely helpful information. If only the Treasury Dept would copy your instructions and post them. Except they would most likely hide them under some obscure nest of links.:}

or redemption of converted bonds, that is correct. I only hold to maturity, so I don’t think of that.

If one has no sales and only Ibonds no 1099 needed?

I have one account with only I Bonds and no redemptions. ManageDirect says … “Year 2022 (No taxable transactions)” and there is no 1099.

Hi David – I downloaded my 1099’s yesterday, an one additional note is that if you have converted savings bonds (paper bonds that you converted to electronic), you must go to the “My Converted Bonds” account and look for an additional 1099.

Excellent point, thank you. Would a simple transfer cause a 1099 to be issued? Or would there need to be a redemption or maturity?

If no maturities in converted bonds, then no additional 1099 under the Converted Bonds sub account

I had not checked my linked account (converted bonds) but … Thanks for the notice (to you and David).