By David Enna, Tipswatch.com

That worked out well. A bit of jawboning earlier this week by Federal Reserve governor Christopher Waller sent both real and nominal yields climbing in the days ahead of the Treasury’s $18 billion offering of a new 10-year TIPS, CUSIP 91282CJY8.

Today’s auction result was good for investors: A real yield to maturity of 1.810% (the third highest auctioned yield since July 2009) and a coupon rate of 1.75% (the highest at auction for this term since April 2009).

At $18 billion, this was the highest amount ever offered for a new 10-year Treasury Inflation-Protected Security, and yet demand looked strong. The auction got a bid-to-cover ratio of 2.62, the highest for this term in three years. And the real yield to maturity of 1.810% was actually slightly below the “when-issued” prediction of 1.825%.

Waller, the Fed governor, said Tuesday he saw “no reason to move as quickly or cut (interest rates) as rapidly as in the past.” That shook up the bond market, pushing real yields up about 10 basis points in two days. Yield expectations for this auction rose from about 1.69% on Friday to 1.80% leading into Thursday’s result.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

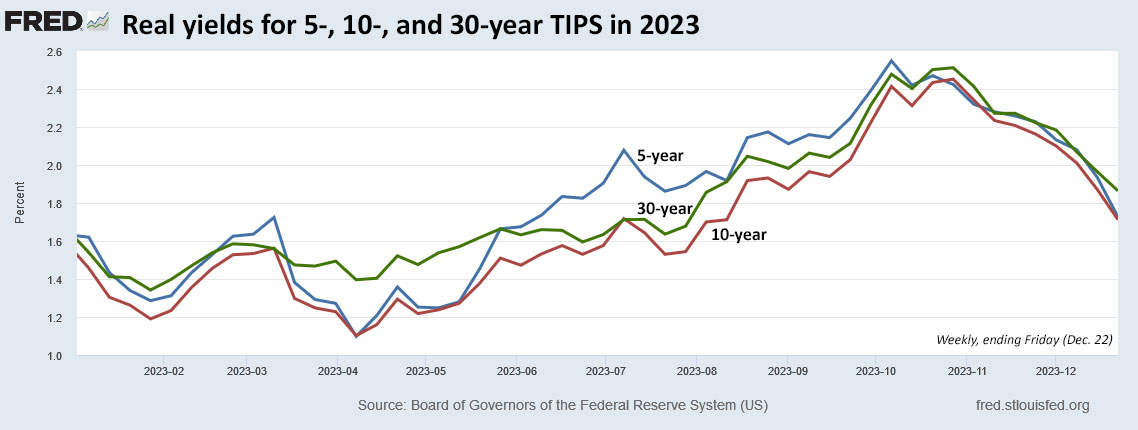

Here is the trend in the 10-year real yield over the last two years, showing that a recent downward trend has reversed this week:

Pricing

Based on the auctioned real yield of 1.810%, the Treasury set the coupon rate for this TIPS at 1.75% and investors therefore got it at a discounted price. In addition, the new TIPS will have an inflation index of 0.99896 on the settlement date of Jan. 31.

Here is how the pricing would work out for a $10,000 purchase:

- Par value: $10,000

- Inflation index at settlement date: 0.99896

- Principal purchased at settlement date: $9,989.60

- Unadjusted price: 99.454975

- Cost of investment: $9,989.60 x 0.99454975 = $9,935.15

- Plus accrued interest of about $7.68.

In summary, an investor purchasing $10,000 par of this TIPS will pay $9,935.15 for $9,989.60 of principal and will then receive inflation accruals and an annual coupon rate of 1.75% on adjusted principal for the next 10 years.

Inflation breakeven rate

At the auction’s close, a 10-year nominal Treasury note was trading with a yield of 4.15%, creating an inflation breakeven rate of 2.34% for this new TIPS. It means the TIPS will outperform the nominal Treasury if inflation averages more than 2.34% over the next 10 years. This rate, while historically a bit higher, is in line with other recent auctions of this term.

Over the last 10 years, U.S. inflation has averaged 2.8%. Here is the trend in the 10-year inflation breakeven rate over the last two years, showing how inflation expectations have drifted lower in reaction to Federal Reserve tightening:

Reaction to the auction

I set my focus set on this auction for several months because this is the first TIPS maturing in 2034 and fills a spot on my investment ladder. I am pleased with the result. Just a few days ago, I didn’t expect to get a coupon rate above 1.625%.

The TIP ETF, which holds the full range of maturities, nudged slightly higher after the auction’s close, which indicates the bond market was pleased. (Remember that the “when-issued” yield prediction was slightly higher, so demand was strong.) The bid-to-cover ratio of 2.62 reinforces that impression.

So we get a good result from the first TIPS auction of the year. Coming next month is the Feb. 22 auction of a new 30-year TIPS. Although I won’t be a buyer, the recent steepening of the yield curve could make this attractive for investors who can withstand both the term and volatility.

Then, on March 21, today’s 10-year TIPS will be reopened at auction.

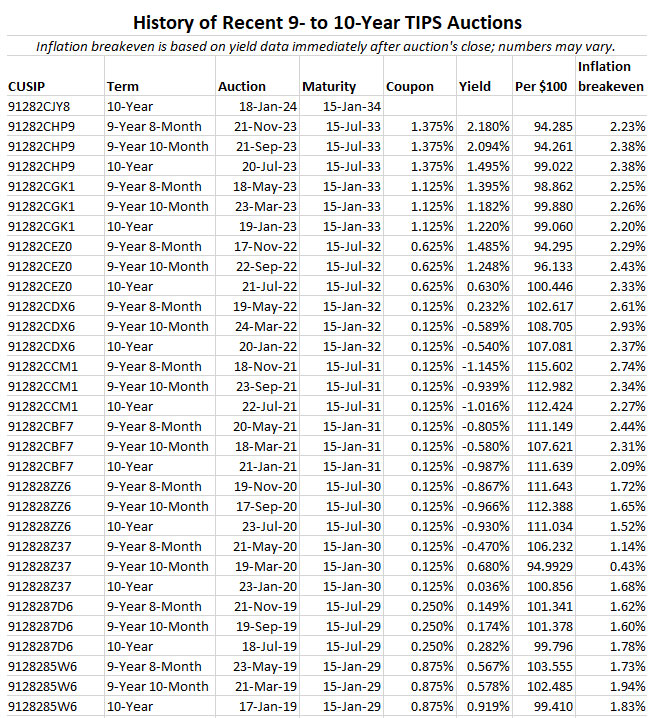

Here is a history of recent 9- to 10-year TIPS auctions. Note that just a bit more than two years ago, a November 2021 reopening auction set the record for the lowest real yield in history for this term, -1.145%. Today’s auction was 295 basis-points higher. Cheers!

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing

The wait is over...one of the missing ingredients is the benefit of starting the minimum one year old for maximum…