Answer: Very well.

By David Enna, Tipswatch.com

I got a reader question this week about CUSIP 9128286N5, a 5-year Treasury Inflation-Protected Security that will mature on April 15, 2024. The question reminded me that this TIPS has completed its cycle, with its final inflation index set by the February inflation report.

As a reminder, each month’s daily inflation indexes for TIPS are set by the inflation report two months earlier. So February’s non-seasonally adjusted inflation of 0.62% set the April 15 inflation index for this TIPS: 1.22640.

That is all we need to know to judge how CUSIP 9128286N5 did as an investment, at least versus the matching nominal Treasury in April 2019. And the answer is: It did extremely well.

On April 15, an investor who purchased $10,000 par value at the originating auction will get $12,264 in principal and a final coupon payment of $30.66.

In my preview article for the April 18, 2019, auction, I surmised that this offering was “relatively” attractive but that 5-year CDs yielding above 3% were a compelling alternative. See? I can be wrong. Way off, in this case, but there was no way to know that U.S. inflation was going to surge to a 40-year high three years later.

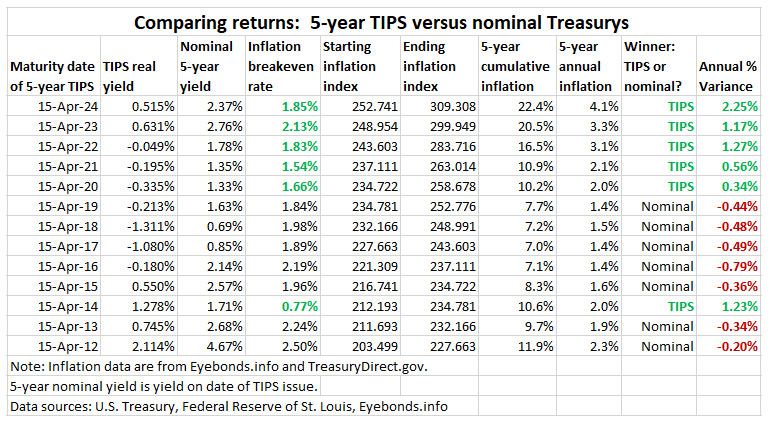

CUSIP 9128286N5 auctioned with a real yield to maturity of 0.515%, versus the 5-year nominal Treasury note yielding 2.37% on that day. That created an inflation breakeven rate of 1.85%, meaning this TIPS would out-perform the Treasury if inflation averaged 1.85% over the next 5 years.

The result: Inflation averaged 4.1%, giving this TIPS a 2.25% advantage over the comparable 5-year Treasury note. That is by far the highest positive variance for any 5- or 10-year TIPS over the last dozen years.

CUSIP 9128286N5 generated an annualized nominal return of 4.6%, which I’d call spectacular versus the meager yields available in April 2019. Here are data for all 5-year TIPS that have matured since April 2012. Note the early trend of under-performance has dramatically shifted because of the ultra-high inflation of recent years.

To view this chart at a glance, the annual variance number in the last column shows how the inflation breakeven rate compared to actual 5-year annual inflation. When the numbers are green, a TIPS was the superior investment. When they are red, the nominal Treasury was the better investment.

The next decade could be entirely different. Never predict the future decade based on the performance of the past decade.

This TIPS versus an I Bond

This comparison is especially interesting, because the U.S. Series I Savings Bond was being offered with a 0.5% fixed rate in April 2109, so the performance should be very close to the TIPS. Let’s look at a $10,000 investment:

- I Bond: As of April 1, the I Bond’s value was $12,396 and can now be redeemed without penalty.

- TIPS: As of April 15, the TIPS investor will receive $12,264 in principal and a final coupon payment of $30.66. But keep in mind that the TIPS has been paying an annual coupon payment of 0.5% along the way. Eyebonds.info says the total interest paid will be $275.88 over the five years on a $10,000 investment.

The result is that the TIPS had a slight edge in performance.

Notes and qualifications

My TIPS vs. Nominals chart is an estimate of performance.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

bdp453, it's not clear from your brief inquiry whether you are trying to learn the basic facts about TIAA Traditional,…