By David Enna, Tipswatch.com

There were no surprises in today’s Treasury reopening auction of $20 billion in CUSIP 91282CJH5, creating a 4-year, 10-month Treasury Inflation-Protected Security.

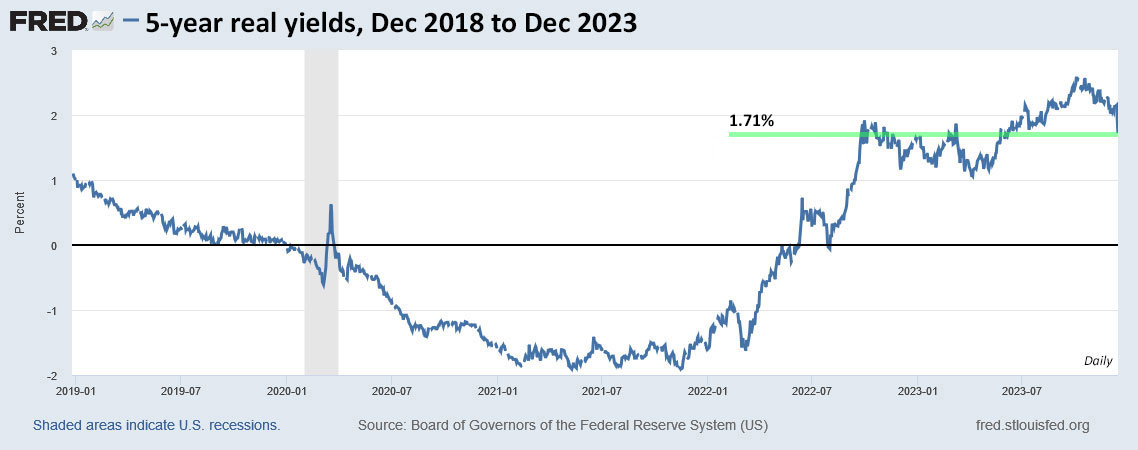

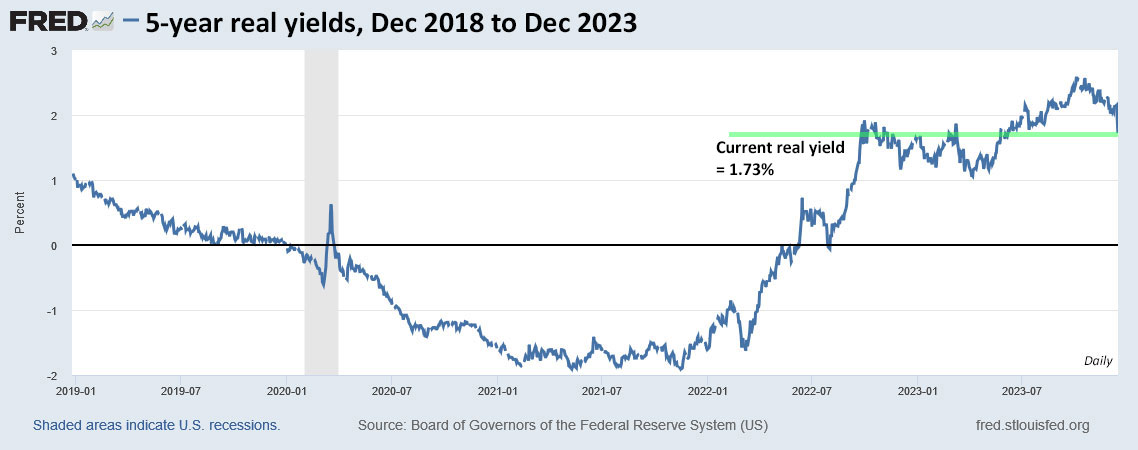

The real yield to maturity came in at 1.710%, which exactly matched the when-issued prediction used by bond traders. In the hours before this auction, this TIPS was trading on the secondary market with a real yield of 1.69%, so today’s investors got a 2-basis-point boost.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

In its originating auction on Oct. 19, 2023, CUSIP 91282CJH5 got a real yield to maturity of 2.440% and its coupon rate was set at 2.375%, the highest for any 5-year TIPS since the very first TIPS auction of this term in history, which generated a coupon rate of 3.625% on July 9, 1997. Market conditions have changed dramatically in the last two months, as shown by the 1.710% real yield generated by today’s auction.

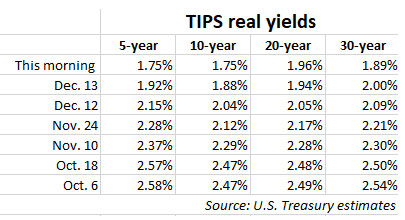

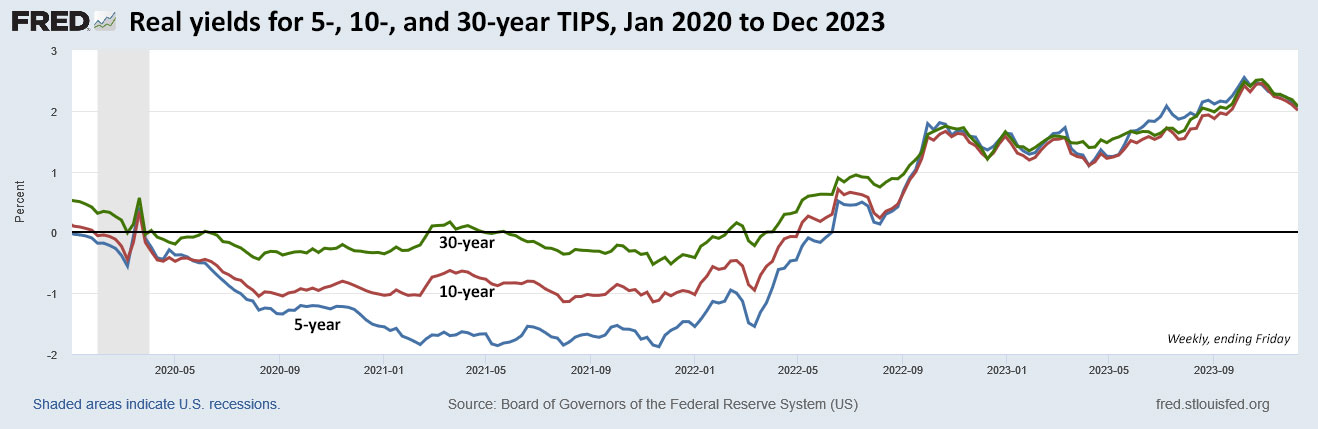

While 1.710% was well below the October auction’s real yield, it remains high by historical standards, as shown in this chart of real yields over the last 5 years:

Pricing

Because the auctioned real yield of 1.710% fell well below the coupon rate of 2.375%, investors had to pay a premium for this TIPS. This is how the Treasury reported the auction results:

The unadjusted price was 103.046880 and the inflation index will be 1.00453 on the settlement date of December 29. Let’s look at the cost of a investment of $10,000 par value for this TIPS at today’s auction:

- Par value: $10,000

- Coupon rate: 2.375%

- Auctioned real yield: 1.710%

- Adjusted principal: $10,000 par x 1.00453 = $10,045.30

- Unadjusted price: 103.046880

- Cost of investment: $10,045.30 x 1.03046880 = $10,351.37

- Plus, accrued interest of about $48.88

In summary, an investor who purchased $10,000 par value paid $10,351.37 for $10,045.30 in principal and will now collect future inflation accruals and a coupon rate of 2.375% on the principal balance until maturity on Oct. 15, 2028.

Inflation breakeven rate

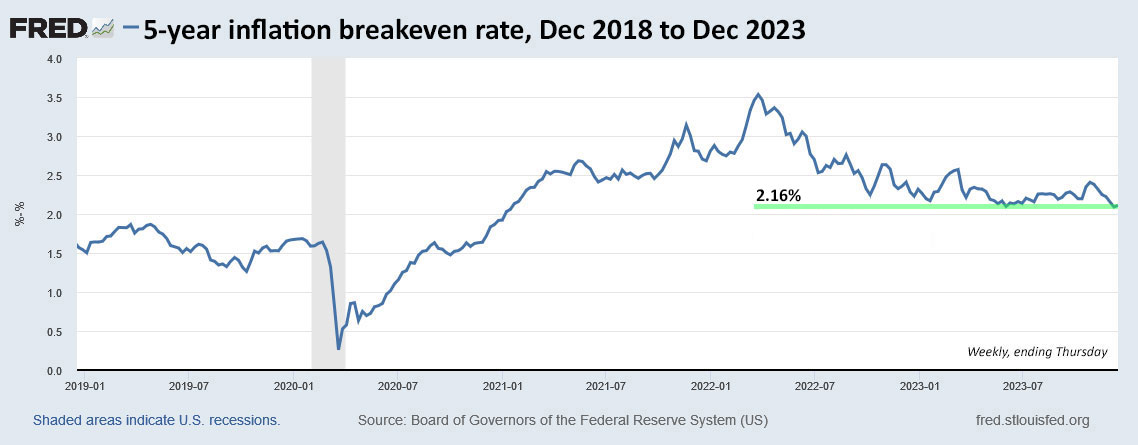

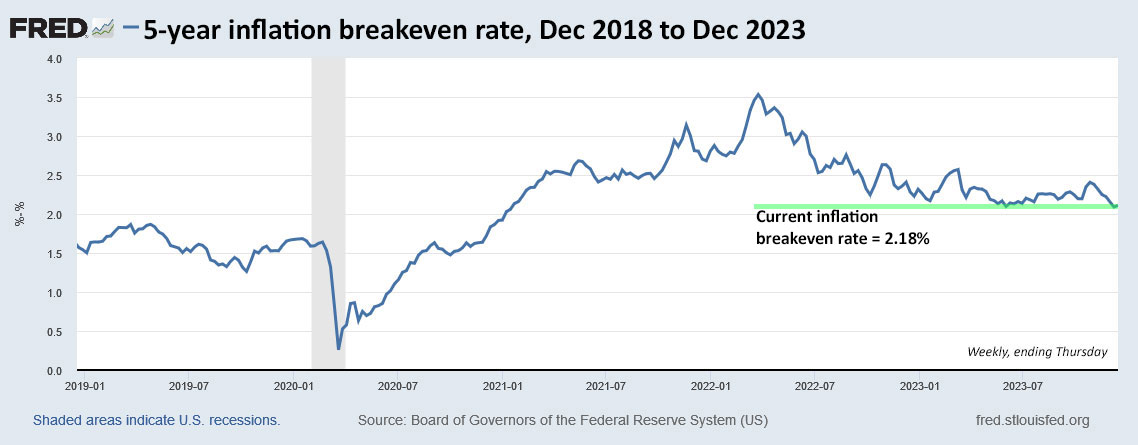

With the 5-year Treasury note trading with a nominal yield of 3.87% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.16%, much lower than results for this maturity in recent auctions. The market is now pricing inflation through the next five years very close to the Federal Reserve target of 2%. Which raises the question: Is the market crazy?

Whatever happens over the next 4 years, 10 months, investors in CUSIP 91282CJH5 at today’s auction got a low-risk, appealing result, especially versus the 5-year nominal Treasury.

Reaction to the auction

It looks like the auction went off almost exactly as expected. The bid-to-cover ratio was 2.55, indicating decent demand. The TIP ETF, which holds the full range of maturities, barely budged after the auction’s close. Everything points to a ho-hum result.

I’ve noted in recent posts that we seem to entering a new era for Treasury yields, with somewhat lower yields likely over the next several months. At the least, yields should stabilize at current levels until the Federal Reserve reveals more exact information on its future moves.

This was the last TIPS auction of 2023. Later this month I will write a recap of the year in inflation protection, including I Bonds. The next TIPS auction will be Jan. 18, 2024, with the release of a new 10-year TIPS.

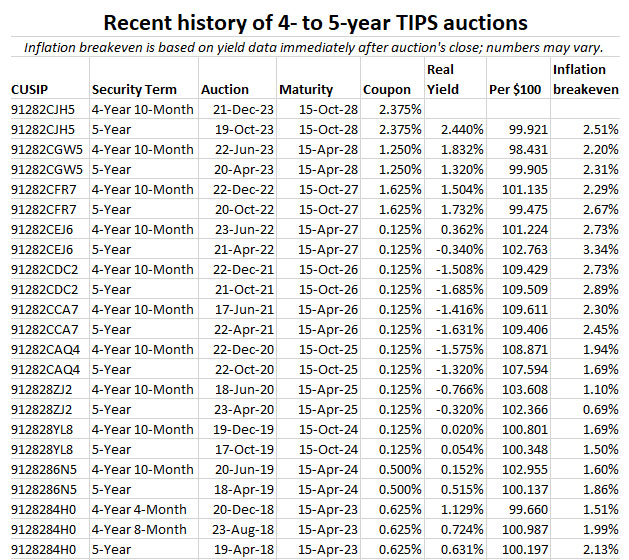

Here is the history of CUSIP 91282CJH5, which at its originating auction generated a real yield of 2.440%, the highest for this term in 15 years.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Advertisements

The wait is over...one of the missing ingredients is the benefit of starting the minimum one year old for maximum…