By David Enna, Tipswatch.com

Note: I posted an updated I Bond analysis on April 14:

Update, April 28, 2023: Treasury raises I Bond’s fixed rate to 0.9%; new composite rate is 4.30%

After a year of raging-high demand, where do we stand today on U.S. Series I Savings Bonds? Are they still an appealing asset? Are they a worthy investment for 2023? Is the variable rate likely to fall at the May reset? Should you hold out for a higher fixed rate later in 2023?

Last year, in January 2022, I titled my year-ahead guide “I Bonds: A very simple buying guide for 2022.” At the time, I Bonds had an annualized rate of 7.12%. By comparison, a 1-year Treasury bill was yielding 0.40%. See? My advice was simple: Buy I Bonds, in January or April or anytime between. But buy I Bonds.

This year, things are more complicated. Yields on nominal Treasurys are much higher. Real yields for Treasury Inflation-Protected Securities have soared to levels we haven’t seen in 15 years. Even bank CDs and online savings accounts are getting attractive. I Bonds have competition.

Before we get into those issues, here’s a quick primer for investors who are new to I Bonds:

The basics

- The fixed rate of an I Bond will never change. Purchases through April 30, 2023, will have a fixed rate of 0.4%, which means their return will exceed official U.S. inflation by 0.4% until the I Bond is redeemed or matures in 30 years.

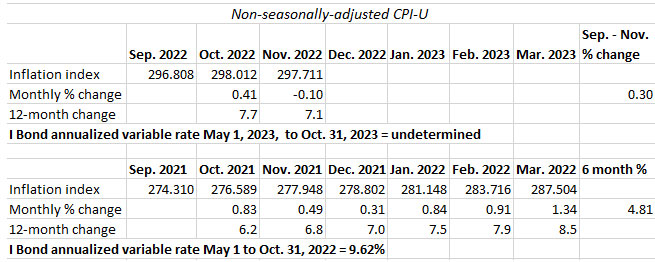

- The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 6.48%, annualized, for six months. It will adjust again on May 1, 2023, rolling into effect for all I Bonds, no matter when they were purchased.

- The current composite rate is 6.89% annualized for six months for purchases from January to April 2023.

I Bonds are an extremely safe and conservative investment. Interest accrues monthly and can never decline, even in times of deflation. Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also the option to get $5,000 a year in paper I Bonds in lieu of a federal tax refund. There is also a “gift box” strategy some investors use to stack purchases for future years.

I Bonds are a unique investment with many positives. For example, earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures. Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

The purchase limit is the reason people ponder timing their I Bond purchases; once you hit $10,000 per person per year, you can’t purchase more, at least in the traditional way.

Are I Bonds still attractive?

I Bonds purchased from January to April 2023 will pay an annualized composite rate of 6.89% for six months, which includes the fixed rate of 0.4%. Is 6.89% attractive? Definitely. But let’s look at the alternatives:

- A six-month Treasury bill has a nominal yield of about 4.76%.

- Best-in-nation 6-month bank CDs are yielding about 4.4%.

- A 1-year Treasury bill has a nominal yield of about 4.73%.

- Best-in-nation 1-year bank CDs are yielding about 4.75%.

- A 5-year Treasury note now yields about 4%.

- A 5-year TIPS has a real yield of about 1.58%.

As a six-month investment, an I Bond definitely looks attractive. But keep in mind that an I Bond has to be held for at least 12 months, and redeeming before 5 years forfeits your last three months of interest. That brings uncertainty into the equation.

Short-term investment

If you are aiming to redeem the I Bond after one year, this still looks like a contender, but with complications. You are guaranteed to earn an actual return of 3.445% in the first six months (6.89%/2), and then some undetermined return in the next six months, depending on inflation from October 2022 to March 2023, plus the fixed rate of 0.4%.

And there is the problem: We can’t accurately project U.S. inflation for the October to March period. The first two months, October and November, are already in, and inflation ran at 0.30% over that period, averaging just 0.15% a month.

So I’d guess the variable rate at the May reset will be lower than the current 6.48%, but most likely will still be at least 1.8%, based on 0.15% monthly inflation on average over the six months. That’s a conservative estimate.

Add on the fixed rate of 0.4% and you can conservatively estimate an annualized return of about 2.2% in the second six months. That creates a total return of about 4.54% for one year (6.89% + 2.2% / 2 = 4.54%) Remember, this is a conservative estimate. If inflation runs higher, your return would be higher. If inflation runs at 0.4% from December to March, the new variable rate would be 3.8%. Add on the fixed rate and you get to 4.2%. Your total return after one year would be about 5.5%.

But … redeeming an I Bond after 12 months will incur a three-month interest penalty, wiping out more than 1% of that return.

Does all this mean that I think U.S. inflation has been tamed? Definitely not. But we are heading into a several-month period where the year-ago numbers will be very hard to match and exceed. So inflation should appear to “moderate” during that period. Take a look at the numbers: December 2021 at 0.31% is reasonable, but then you get January 2022 at 0.84%, February at 0.91% and March at 1.34%.

Conclusion. If your only interest in I Bonds is a quick one-year investment, you might want to look at competitive nominal investments like one-year bank CDs, online savings accounts or one-year Treasury bills. If inflation moderates, the returns could be similar but without the three-month interest penalty. The advantage of an I Bond is long-term inflation protection. If you aren’t concerned about inflation in the long term, look elsewhere.

But if you remain interested in the I Bond for one year, then I’d suggest using TreasuryDirect to set a purchase date later this month, maybe Jan. 27, to lock in January as your starting month. You could then redeem early in January 2024.

Long-term investment

Long-time fans of I Bonds buy them every year, up to the annual $10,000 per person purchase limit, to build a large cache of inflation-protected savings. After 5 years, an I Bond effectively becomes an inflation-protected, tax-deferred cash account you can draw from without penalty. (See the I Bond Manifesto for more on this.)

I am a long-time, devoted I Bond fan, and I will be buying I Bonds up to the limit this year. I want that higher fixed rate. But when to buy? The key factors in this decision are 1) potential changes in the I Bond’s variable rate, and 2) potential changes in the I Bond’s fixed rate.

Buying anytime from January through April will result in exactly the same return on your investment. That is because when you purchase an I Bond, you lock in the current composite rate (6.89%) for a full six months before the next rate reset. So a long-term investor has no urgent need to buy in January. In 2022, I bought in January to go ahead and grab the 7.12% variable rate. This year … I will wait.

Key date: April, 12, 2023. At 8:30 a.m. ET on April 12, the Bureau of Labor Statistics will release the March inflation report, setting in stone the I Bond’s next variable rate reset, going into effect May 1. At that point, you will also have an idea of where the I Bond’s fixed rate could be heading. And you will have about 15 days to decide: Buy in April, or in May?

As I said earlier, I think the variable rate could be heading lower, somewhere in the range of 1.8% to 4.0%. That’s a guess, not a projection. If the variable rate is going to fall, buying in April makes more sense, to capture 6.89% for six months.

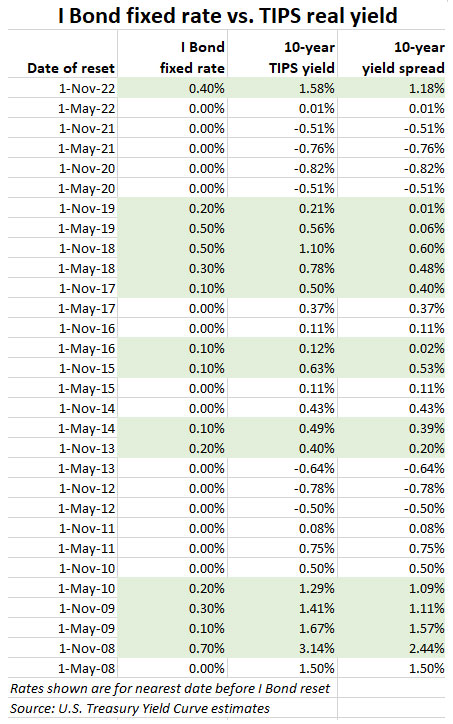

But then there is the issue of the fixed rate. Long-term investors in I Bonds know that a higher fixed rate is always more desirable, because it stays with the I Bond for the entire 30-year potential term. Could the fixed rate rise on May 1? My guess is yes, it is possible if real yields continue holding at current levels, with the 10-year TIPS trading with a real yield of 1.58%.

(Update on January 9: The 10-year real yield has fallen to about 1.3% in trading today, dropping about 28 basis points in a week. Not a good indicator for a higher fixed rate for the I Bond, but a lot of time remains.)

Oddly enough, 1.58% is exactly where the 10-year TIPS was trading on Oct. 31, 2022, the day before the Treasury raised the I Bond’s fixed rate from 0.0% to 0.4%. My opinion: The fixed rate should have been higher, but I was pleased with the decision to raise it at a time when TreasuryDirect was overwhelmed by demand for I Bonds.

The Treasury has no public formula for setting the I Bond’s fixed rate, but I have contended for years that the 10-year real yield is the best indicator of where the fixed rate is heading. At the November reset, the yield spread was 1.18%, the highest since November 2008. The fixed rate could have been higher.

What about waiting until the Nov. 1 rate reset? I’d say no because you could risk losing the above-zero fixed rate if the Fed changes course, plus the attractive composite rate (6.89%) for six months. Anything can happen though. On Jan. 1, 2022, a higher fixed rate did not look all likely at the November reset — the 10-year real yield was -0.97%. Ten months later it had increased 255 basis points.

Conclusion. A higher fixed rate is a possibility on May 1, even as the variable rate might be going lower. For a long-term I Bond investor, I think it makes sense to wait until April 12 to make a purchase decision. And even then the decision might be to divide your purchases, half in April and half in May, if a higher fixed rate looks at all possible.

Redeem I Bonds to purchase I Bonds?

If you are a long-time investor in I Bonds, you probably have some issues with a 0.0% fixed rate and have hit the 5-year mark so they can be redeemed without penalty. For example, I have I Bonds issued in April 2017 that qualify. If I wanted to step up to the higher fixed rate, I could sell the April 2017 I Bonds and buy the April 2023 I Bonds, getting the 0.4% fixed rate.

The negative to this strategy is that I would owe taxes on the $1,704 interest I’ve earned. That would be costly. However, the strategy still makes sense for an investor that doesn’t want to raise additional money this year to buy the 2023 allocation.

Another alternative would be to redeem I Bonds with a fixed rate of 0.0% that you’ve held just a year or two. That would cost you three months of interest, but if you delay redeeming until three months after the 6.48% variable rate cycles off, you could lower the penalty (possibly). Plus, the total taxable interest for the shorter holding shouldn’t be too painful.

I’m not a fan of rolling over I Bonds, but I can see the need for investors who need to raise the cash for a more attractive purchase.

Obvious alternative: TIPS

The one investment most similar to an I Bond is a 5-year TIPS, especially one held in a tax-deferred traditional IRA account. The I Bond can be redeemed without penalty after 5 years; the TIPS matures in 5 years. They are equally safe if you hold the TIPS to maturity. But at this point, the 5-year TIPS has a huge above-inflation yield advantage: 1.66% for a 5-year TIPS vs. 0.4% for the I Bond. This is why I recently wrote that current yields make it “advantage TIPS.”

But TIPS can be a confusing and even frustrating investment, and many investors prefer the simplicity of the I Bond, which has better deflation protection, never goes down in value, and can be redeemed in the year of your choice. I Bonds work much better as a cash alternative and can add to your tax-deferred holdings without creating worries about future required minimum distributions.

I have been buying TIPS aggressively since mid-2022 and I will keep buying the 5- to 15-year maturities as long as real yields continue at high levels. But I will also buy I Bonds in 2023. Inflation protection is a handy thing, as shown in the last two years when inflation suddenly and unexpectedly ran at 7+% annually.

Both investments can work in your portfolio.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bond Manifesto: How this investment can work as an emergency fund

• Confused by TIPS? Read my Q&A on TIPS

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Opinion: It's time to buy I-bonds again. Here are 3 ways to maximize your $10,000 inflation-fighting investment. - Rich and Wise

Based on the new CPI data this week, what are you expecting in May and what do you recommend?

I’m posting an analysis tomorrow. April 14.

Always interested in I bonds and others types similar for resource info towards advantages /disadvantages.

If I redeem I-Bonds purchased in 2001 at a bank which still handles paper I-bond redemption, then how do I get a 1099-INT for this redemption?

No. I did this with EE bonds last year, and I received a 1099-INT from the bank where I did the redemption. TreasuryDirect does not know those I Bonds exist unless you move them to that account.

I have I bonds that were purchased from 2003-2008. I am retired now and so confused about bonds. Should I cash my bonds and rebuy up to the 10000.00 ? I do not need to use the money now or in the near future and will be ok with having to pay the interest but a little confused about if it will be an advantage. Are those older bi ss now drawing the higher interest rate? Your site has been most helpful but hasn’t been able to find this answer

Most of the I Bonds issued from 2003 to 2008 have fixed rates above zero; some of them are above 1.0%. You don’t want to redeem any I Bonds with a good fixed rate. Today’s fixed rate is 0.4%, which is lower than probably all of the ones from 2003 to 2008. Also keep in mind that you can redeem any amount of I Bonds, but you can still only purchase $10,000 per person in any calendar year.

I apologize if I posted this twice, but had a glitch.

You wrote: “The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 6.48%, annualized, for six months. It will adjust again on May 1, 2023, rolling into effect for all I Bonds, no matter when they were purchased.”

I’m a little confused by this. What is the point of waiting until April to decide whether to purchase at the current combined rate if going to adjust to a potentially lower rate in May anyway?

Or, if I’m reading some of the comments correctly, do the iBonds bought in April carry that rate for six months and *then* convert to the May adjustment?

Thanks, and I really appreciate your blog!

The reason to wait is to see if 1) the fixed rate looks likely to rise above 0.4%, and 2) to see if the variable rate will be much higher or lower. Yes, I Bonds carry the current composite rate for a full six months, no matter which month you buy them.

This link is better –

http://eyebonds.info/ibonds/home10000.html

Thanks for your excellent commentary on this site. We’ve been doing I-BONDS for $10,000 each per year (wife / husband) since 2015. Then in 2020 started doing the extra $5,000 paper I-BONDS (married filing jointly thus $2500 in each SSN on IRS form 8888 with our MFJ tax refund). I was unclear from the “gift I-BOND” commentary if we are allowed to “gift” each other’s SSN an I-BOND with an “execute on x date next year” on top of our usual maximizing strategy which we plan to continue in future years. Sounds like “gifting” on top of current annual max purchases would be a “no” with maximum per SSN at $10,000 via Treasury Direct account plus a paper IRS refund of $2500 each, per calendar year? Can we form a trust (or other vehicle which we along would be connected to) and somehow also add I-BOND purchases to a trust entity beyond our individual SSN’s? Again, thanks for all your detail, hotlinks to valid sources and expertise. We appreciate it.

You can stack multiple gift box purchases in one year. But you can only deliver one $10,000 I Bond gift (plus earned interest) to each person in one year. That delivery will fill the person’s $10,000 purchase limit for the year they receive it. So you can purchase I Bonds AND and gift I Bonds in any year, but the delivery will trigger the cap for the person receiving it, in the year it is delivered. Yes, you can use trusts for additional purchases. I am not an expert in this area, however.

I have used LLCs to load up on I bonds at attractive rates. They are easy to set up and inexpensive in many states. The treasury department challenged my strategy last year and when I provided them with the documentation they said that everything is fine. I still have their emails.

Buy the a $10,000 gift bond for each other (spouses) and just hold it in your gift box. As long as you do not actually gift it to the other person then it does not count toward the $10,000 the other person can buy that year. When a year occurs that you do not plan to buy I-bonds, then gift (transfer) the bond being held in the gift box at that time. In addition, the 5 years for holding the bond (to avoid 3 month interest penalty) will start when you purchase them, not when you actually gift (transfer) them. This was advice I got on the phone from a representative at Treasury Direct.

Any updates to your POV given the most recent interest rate changes by the Fed and inflation data?

It is all going to come down to the next three months of inflation data. If inflation pops a bit higher, the Fed is going to have to hold the line and continue moderate rate increases. The market isn’t pricing that in, with the 5-year inflation breakeven at a very optimistic 2.27%. It’s surprising to see how low nominal Treasury yields have dipped for 2-year terms and greater.

Very good article. Where can I find the real yield for TIPS?

The real yield changes every day (even hour by hour) for every TIPS on the secondary market. You can use the Wall Street Journal for information on this: https://www.wsj.com/market-data/bonds/tips

Thank you for this write-up! For those of us planning to purchase the full $10k limit each year, I’m not sure I follow the benefit of waiting for April to see what the rate is going to be if I could purchase in January. Isn’t waiting 3 months to purchase similar to a self-imposed 3-month penalty? Even if the variable rate were looking to be higher or lower in April/May, I would still be purchasing (especially now to make sure we get the fixed rate locked-in). If the fixed rate were to come out higher in May, then the gift box strategy could be used to capture that as well.

I Bonds pay a full six months of the current composite rate, no matter the month of purchase. So a purchase in January gets exactly the same return as a purchase in April, for six months. So waiting causes no harm.

Yep I totally get the 6-month rate period. I just mean that if I buy in April I’m missing out on getting the interest for January February & March. The harm isn’t that you would lose the rate, it’s just that you would miss out on three months of potential interest. Buying at the end of January starts compounding 3 months earlier than buying at the end of April.

In the long run, you will earn exactly the same return if you start in January or start in April. Someone buying in April could be investing in a 3-month Treasury, now earning an annualized 4.69%. There is no penalty to waiting. The potential advantage is that you can scope out the possibility of a higher fixed rate. But, in reality, buying in January is perfectly fine, if that is your choice.

I am doing exactly this. I put the money that will likely go into I bonds into a three-month treasury that matures in late April. Then I will roll the funds into I bonds and in essence double dip for the month of interest. It also gives me the flexibility to do something other than I bonds if the new rate is unattractive. Grab a little extra interest and preserve flexibility.

isn’t the variable portion looking to be zero or negative at the next reset (april 2023) due to yoy changes ? The monthly value is already below Sept 2022s 296.808. if actual inflation still is in 5-6% range, do you expect the govt to increase the fixed rate component.

I’d say zero or negative is definitely possible for the variable rate, but the composite rate can’t go below 0.0%. If you look back to 2019 to 2020 we had similar three-month trends but ended up reserving and going positive after the full six-month cycle.

If the variable rate goes to zero on May 1, 2023 and I wanted to redeem I-Bonds I purchased in late August 2021, would the best time to redeem them be on or after November 1, 2023 (forfeiting 3 months of 0% interest)?

If you bought in August 2021, your variable rate will update each August and February.

3.54% from August to January 2022

7.12% from February to July 2022

9.62% from August to January 2023

6.48% from February to July 2023

Then, August, September, October … redeem in November. Correct.

2 Qs

Redeem in early October and forfeit August, September, and October (latter is earned on Oct. 1st)… Right? Why wait until November and have 4 months of loss interest, and

If the CPI reset for May 1st goes negative, then fixed rate “must” be at least the negative amount so the composite rate is “at least” zero…Right? Ergo, we can then conclude the minimum of the fixed rate amount in mid-April when the March CPI is released

I Bonds earn interest on the first day of the month, FOR THE PREVIOUS MONTH. When you buy an I Bond, you get credit for that full month. Does not work that way when you redeem.

If the CPI reset for May 1st goes negative, then fixed rate “must” be at least the negative amount so the composite rate is “at least” zero…Right? Ergo, we can then conclude the minimum of the fixed rate amount in mid-April when the March CPI is released

Correction. Q

If the CPI reset for May 1st goes negative, then fixed rate “must” be at least the negative amount so the composite rate is “at least” zero…Right? Ergo, we can then conclude the minimum of the fixed rate amount in mid-April when the May CPI is released

Jim, on the May reset: I suspect that the variable rate will remain above zero, as I noted in this article: https://tipswatch.com/2023/01/13/is-the-i-bonds-variable-rate-heading-to-zero-maybe-not/ … But yes, if is is negative, the new composite rate is going to be zero or close to zero at the May reset, depending on how the Treasury sets the new fixed rate. But for I Bonds purchased before November 1, it would be zero.

We know there are only two components to the Ibond rate…fixed and CPI based…..And if the CPI is negative then the fixed has to be positive for a zero overall rate! And for those purchased before November 1 they will have that fixed rate (to offset the negative CPI in the example for May 1 reset) for the life of the ibond….right? Why would they have zero fixed rate and for what period of time…? How would it “go away” on the subsequent Nov 1 reset?

i understand your logic but don’t know how exactly the Treasury “sets” the floating rate. The language may see that if it is negative, you just round it to Zero. then, the fixed rate can be zero as well, not the inverse. also, once the treasury sets the fixed-rate, it stays with the bond forever. if overall rates appear to be trending to zero in the market and inflation appears to be falling as well, why provide a “high” fixed rate to offset an otherwise temporary level of higher rates today?

if the fixed component must always be at least the inverse of the negative component, we could see a high fixed component over the next few resets. The YoY changes in CPI could get to exceedingly negative. Since the fixed component stays with that bond forever, the composite rate could look pretty good if inflation turns the other way.

No, this is wrong.

May 2015 through October 2015 238.031 in September 2014 to 236.119 in March 2015 – Fixed: 0.00%; Variable: -0.80%; Composite: 0.00%

May 2009 through October 2009 – Fixed: 0.10%; Variable: -5.46%; Composite: 0.00%

I think one way to think about this is that the composite rate actually has >three< components: a variable rate and a fixed rate (which are completely independent of each other) and a zero bound.

Jim, responding to your correction Q: The Treasury could set the new fixed rate anywhere it wants, so it will be impossible to say what the composite rate will be May 1 for new I Bonds, even if you know the variable rate is below zero. In theory, the variable rate could be -0.2% and the fixed rate could be 0.4%, so the composite rate would be 0.2%.

We will know what the CPI change is and the corresponding variable rate in mid-Oct for the Nov 1 reset. And the fixed rate (to compensate for a theoretical negative variable rate in the example) would continue for the life of the ibond…therefore another option if one is so inclined is to “bank” the fixed amount in bond purchases between May 1 and Nov 1 reset…right?

TJ, there is zero relationship between the I Bond’s variable rate and where the Treasury will set the next fixed rate. If the variable rate goes negative, the fixed rate could go down on May 1 (or go up). There is no connection between the two. (I think you are assuming that because the composite rate can’t go below zero, the Treasury has to balance off a negative variable rate with an equally positive fixed rate. That’s not right. They are completely independent, but the composite rate can never go below 0.0%.)

ok thanks … i thought it was posted on here that the composite rate could not be less than zero, i.e., if the variable is negative, the fixed component has to be the inverse. so, you are saying that if the variable portion is negative, they just make it zero and then set the fixed wherever they want.

The variable rate remains negative. It offsets any positive fixed rate. The composite rate cannot go below zero.

“If I wanted to step up to the higher fixed rate, I could sell the April 2017 I Bonds and buy the April 2023 I Bonds, getting the 0.4% fixed rate.” This wouldn’t work when gifts are involved, right? Specifically: if I’ve received a $10K I Bond gift in 2023, I can’t sell it and buy a different $10K I Bond. I don’t think the Treasury is going to care that the “net effect”to me is still $10K for 2023. Correct?

Correct. If you receive an I Bond gift in 2023 (maxxing out the $10,000 limit) then your cap has been hit and you cannot buy any more, even if you immediately sell the I Bond.

Which performed better: An I-bond purchased in October 2017 and held for five years or a 5 year TIPS purchased in October 2017?

How can a person find this out?

I Bonds weren’t offered in Oct 2017 at auction; those auctions didn’t start until Oct 2019. The 5-year real yield on Oct 15 2017 was 0.20%, the I Bond had a real yield of 0.0%, and started off with a six-month variable rate of 1.96%. Inflation increased 20.8% over the five years. The TIPS performed better; I’m estimating about 4.1% vs 3.9%.

Thank you. It appears like I Bonds get a higher inflation payout (7.12, 9.62, 6.49). During this same time, did TIPS inflation index ever reflect 9.62, for example?

According to this chart, for 2022 through November, the inflation rate is 6.6. Did TIPS ever get to 9.62 for six months?

https://data.bls.gov/timeseries/CUUR0000SA0&output_view=pct_1mth

Well, yeah, look at the period from Jan to June 2022:

Jan 0.84%

Feb 0.91%

Mar 1.34%

Apr 0.56%

May 1.10%

Jun 1.37%

Total 6.12%, annualized 12.24%

Embarrassed. Right in front of me. Thank you.

Thanks for the post and the blog.

I would love to see a detailed post detailing how deal with Treasury Direct 1099’s. From very basic, where to find it on the site, all the way to your, I would imagine, complicated 1099.

As I first time purchaser I’m trying to figure out my strategy. I’m 45, currently I have just a TD account without anything in it. I would like to hold to maturity, something to fall back on for the rest of my life.

I know from other readers’ comments that there is a lot of confusion about TreasuryDirect’s 1099 forms. They haven’t been posted yet, but when they are, I will write a guide to finding them and how to deal with them. They will not be mailed to you.

If the most likely fixed rate change is from 0.4% to 0.6%, that’s a difference of $693.50 over 30 years for the $10k investment. At such a minor difference (IMO) I think I will most likely buy in april to get the higher inflation rate for six months

Yes, in year one a boost from 0.4% to 0.6% amounts to only $20. The difference between a composite rate of 6.89% versus maybe 4.0% would be $144 in the first six months. So it would take quite a few years to break even.

I am 86 years old, and my husband is 88. If we buy I bonds would our children be penalized for cashing the bonds early if we pass away before they mature?

If you name a child as a beneficiary in the I Bond registration, TreasuryDirect says this: “If a surviving co-owner or beneficiary is named on the savings bond, the bond goes directly to that person. It does not become part of the estate of the person who died.” I think the same terms will apply, including the early withdrawal penalty for an I Bond held less than 5 years. The I Bond would not need to be redeemed. But I am not an estate expert, sorry.

I am posting this on behalf of Hoyawildcat, who had trouble getting this comment to go live: …………………………

Thanks for your excellent analysis.

Regarding I-Bond purchasing strategies, you concluded:

“A higher fixed rate is a possibility on May 1, even as the variable rate might be going lower. For a long-term I Bond investor, I think it makes sense to wait until April 12 to make a purchase decision. And even then the decision might be to divide your purchases, half in April and half in May, if a higher fixed rate looks at all possible.”

I agree entirely with this but I would suggest hedging one’s bet by buying half this month at the current rates — in order to start the interest-penalty clock — and waiting until mid-April to get a feel for what the new fixed rate will be in May and deciding then whether to buy the other half in April, at the current rates, or in May at the new rates (variable rate known in advance; fixed rate not).

How high do you think the fixed rate could go in May? More to the point, what are you hoping for? If only 0.4%, i.e. the current fixed rate, then waiting until May means that one will lose six months at the current variable rate. (The variable rate will almost certainly be lower in May.) Is it worth it to wait if the fixed rate increases to only 0.5% or 0.6%?

A lot of people are suggesting buying half in January and then deciding on the other half in mid-April. I have no problem with that. Where is the fixed rate headed? At the current real yields, I’d guess the top would be about 0.8%, but 0.5% or 0.6% seems more likely, given how cautious the Treasury seems to be. (And now that I say that, 0.5% or 0.6% really isn’t going to change the investing equation much, especially if the variable rate falls in May.)

Still new to I bonds. How can I track my I bond’s monthly interest earned on Treasury Direct site ? Unlike brokerages that one can pull up previous activity. Thank you.

After you log into TreasuryDirect, you will see a list of your current holdings. Savings Bonds will be listed, but show the original purchase price. Click on Savings Bonds and on the next page you will see “current value” of all your bonds. If you click on the radio button and submit, you can see a full list of the individual bonds and the current value. Keep in mind that TreasuryDirect will not show the last three months of interest until you have held the I Bond for 5 years. More here: https://tipswatch.com/2022/08/09/dont-go-ballistic-over-the-way-treasurydirect-reports-i-bond-interest/

I just want to confirm that you can cash out a portion of an Ibond. Can I buy a $5,000 bond and cash it out a $1,000 at a time or do I need to buy 5 $1,000 bonds? It looks like I can buy big and piece meal out to me.

TreasuryDirect says: “How much can I cash at one time? Any amount of $25 or more to the penny. If you cash only part of what a bond is worth, you must leave at least $25 in your account. If you cash only part of what a bond is worth, you get the interest only on the part you cash.” https://www.treasurydirect.gov/savings-bonds/cashing-a-bond/

Hello. New to your very interesting blog.

Also new to I bonds. Bought $20K last year (I have an EIN).

Question. I just divide $20k by 12 and buy that much every month.

Any problems with that approach?

My intent is to diversify my holdings and accumulate for at least a decade.

Thanks!

That’s a great approach. The only negative is that you have a lot of transaction entries at TreasuryDirect; is is hard to keep track of all those $833 I Bonds? But after 5 years, you could start redeeming $1,660 a month + inflation with no penalty.

David – How do you handle your 1099-Int forms from Treasury Direct? I usually copy and paste it into an Excel spreadsheet and then cell reference the taxable amounts and tax withholding amounts in another column. Somewhat cumbersome but in the end it makes the math easier. I find it odd that TD does not sum the transaction amounts on the 1099.

I loathe the 1099-INT and 1099-OID forms I get from TreasuryDirect. They are a mess, unlike anything you’d see from a broker or bank. However, my wife was was a CPA in a former life and we get through it each tax season. If you aren’t seeing the totals, you may be looking at the wrong listing. Make sure you are seeing the actual 1099s and not the interest summary page. Eventually, there will be a link to the 1099s on top of the 2022 listings. You need to print these 1099s yourself. These have totals. (TreasuryDirect WILL NOT mail you these forms. Maybe I need to write an article about this when the forms appear for 2022. They haven’t been posted yet.)

Would really appreciate if you did do one on TD’s 1099s. Do they at least email you when they issue one?

I do think you will get an email, but it may only say, “You have a message in your inbox.” The 1099s should appear close to Jan. 31.

I want to thank you for this article. I was able to finally understand the pricing of TIPS and knew what to expect. I purchased the 10/15/2027 bond on the secondary market on the last day of trading for 2022 and received a real yield of 1.655.

I struggled with the purchase because of the experts claiming that inflation is coming back down. But really, if inflation is only 2%, this is still a nominal return of 3.655. But I am taking the bet that inflation will be higher. I plan on holding for the term.

Again, thank you for your help.

David-Would you please address strategies for redeeming EE bonds for new I-Bond purchases?

Also, a note of caution to long-term EE and I-Bond holders: While tax-deferred compounding is attractive, large amounts of interest earned at maturity may result in higher tax brackets and IRMAA (for those on Medicare). Consult with a tax advisor to determine whether declaring and paying taxes on some or all Savings Bond interest each year makes more financial sense than doing so only at maturity.

We did have 1992 EE Bonds mature last year. We knew that was coming and included it in our income plan for the year (we pay estimated taxes based on a certain income level). Those EE Bonds were still paying 4% until maturity. But if you bought in recent years, they are probably earning a 0.1% fixed rate and will double in value after 20 years, equivalent to 3.53% annually. So it depends on how close you are to 20 years.

Very cumbersome to change a beneficiary or co-owner with paper bonds

My family had to do this a while back for a relative’s holdings. The way we achieved it was to convert the paper I Bonds to electronic form, and then change the beneficiary. (This was before TreasuryDirect was overwhelmed by I Bond demand.)

I am with you David and waiting until April to decide. I have long term debt for which paying it off makes more sense than I Bonds, especially at a potentially lower rate. Changing some of the seasoned I Bonds currently at a 0% fixed rate to a non-zero fixed rate also makes sense. The taxes need to be owed regardless and I don’t see my tax rate going significantly lower in the period of time when I need the I Bonds to meet expenses. Thanks.

Excellent work, David. The 10-year real yield chart as an indicator for the direction of the I Bond Fixed Rate is very helpful since TD has, for some inexplicable reason, chosen to shroud the I Bond Fixed Rate in mystery. It’s better to have a loosely correlated comparable to go by than none at all.

I’d like to propose an alternative to your Long-Term Investment section conclusion quoted below:

“Conclusion. A higher fixed rate is a possibility on May 1, even as the variable rate might be going lower. For a long-term I Bond investor, I think it makes sense to wait until April 12 to make a purchase decision. And even then the decision might be to divide your purchases, half in April and half in May, if a higher fixed rate looks at all possible.”

Here’s my alternative. Instead of splitting I Bond purchases before and after May 1, I think it makes more sense to buy Gift I Bonds (with one’s spouse), either after the January 12th CPI report (when we’ll know half of the inflation rate and can extrapolate from there) or the April 12th CPI Report (when we’ll know the full inflation rate as you’ve recommended). This will capture the 0.4% Fixed Rate of the current I Bond to be held undelivered in the Gift Box without using up any of the annual limit.

If it turns out that the May 1 Composite rate includes a higher Fixed Rate than 0.4%, both spouses can then also purchase new I Bonds to max out the annual limit.

If it turns out that the May 1 Composite Rate includes a lower or 0% Fixed Rate, both spouses can deliver previously purchased I Bonds with a 0% Fixed Rate that may be currently held in their respective Gift Boxes, and hold off on new purchases.

What do you think?

Seems sensible, for people who want to use the gift box strategy. I don’t use it. Nothing wrong with it, though. It is a loophole the Treasury has created, and people are logically using it.

David, current composite rate is 6.89%, not 6.49%, right?

My not-so-simple guide this year will include partial gift presentations to position some of the gift bonds I purchased last year with 0% fixed rate, while still preserving some of the $10,000 limit for myself and spouse. Doing it in April and October seem the best options to make informed decisions.

Hi Jim! Yes, the composite rate for I Bonds purchased today is 6.89% (because of the 0.40% fixed rate), and the variable rate is 6.48%, which applies to all I Bonds, eventually, for six months.

Your first bullet has 6.49%, although rest of article had the right figure in all the calculations. Jim

>

Got it. Thanks for catching that.

I have an extensive portfolio of I bonds built in 2022 using LLCs set up for the purpose of being the registrant for I bonds. In my opinion, it is not as simple as comparing the 0.4 fixed rate to the real yield on TIPS. I bonds look backward at inflation, TIPS look forward. In a period of declining inflation, as we have now, I Bonds have an advantage. In flat or rising inflation Tips have an advantage. My I Bonds have a fixed rate of zero. When the rate gets to the point where the payback is two years or less I will roll them either to new I Bonds or TIPS depending on the inflation trajectory and available rates. With the fixed rate at 0.4 that would be when the variable rate hits 3.2.

Yes, true, getting back-loaded inflation is an advantage, in the short term. That is why the 9.62% rate was so sensational, going into effect a few months before inflation was peaking. In the long run though, a higher fixed rate on a TIPS will make it the winner.

Fixed rate is everything with I bonds,imho. I have some old ibonds with a high fixed rates. After years of compounding the fixed rate is 99% of the return. I m with you, my lo to zero fixed rate will be the first to go!

The payback on the current variable rate is about four years. I think there will be shorter payback periods in the future. I agree the fixed rate is more important. What we had in 2022 was a once-in-a-lifetime opportunity to grab some front-loaded benefits. Transitioning to bonds with a higher fixed rate makes sense. I’m just going to wait for a better opportunity which should come in the next year.

Thank you David! I like I-Bonds so much because they pay compound interest.

Treasuries pay simple interest, and I find the interest payments can be a pain to re-invest.

Short-term Treasury Bills are a good cash equivalent, but I-Bonds are best for long-term compound growth.

This is another advantage of I Bonds over TIPS, since TIPS pay out the coupon rate as current interest. But the inflation accruals do compound, giving TIPS an edge over other Treasurys.

Since “interest payments can be a pain to re-invest” with nominal Treasurys, you can instead purchase zero coupon Treasurys (i.e., STRIPS), which eliminate reinvestment risk. Currently, from about 5 through 20 year maturities, STRIPS yield more than coupon-paying Treasurys.

I don’t have a lot of knowledge of STRIPS, but I know you have to buy them at a broker. Is there such a thing as a new issue? Is it entirely secondary market? Is the market liquid?

November 2021, I was in on the 9. 62% – 0% fixed I Bonds. My question is, am I correct that after the 6 month reset (May 2022), I will only gain compound interest on the bond itself, there will be 0% variable and 0% fixed?

No, that is not correct. If you purchased in November 2021, you earned 7.12% annualized for six months. Then, beginning in May 2022, you earned 9.62% annualized for six months. In November 2022 you began earning 6.48% annualized for six months. Your fixed rate will always be 0.0%.

I am a little confused. If the May adjust to 0% variable rate and assuming the fixed rate does not changed from .4%, does that mean I am getting almost 0% for my balance in the I bond account or any new investments from May? Should I just withdraw then?

If the May 1, 2023 I-Bond inflation factor is unattractively low, and as a result you want to redeem I-Bonds purchased in November 2021, then waiting until August 1, 2023 would drop off 3 months of the unattractive interest rate rather than any of the 6.48% months.

STRIPS are created from coupon-paying Treasurys and are not available as new issues. The market is fairly liquid, but the bid-ask spread can be significant for long-maturity issues. Thus, these are best held to maturity, and they work great in bond ladders. You can buy STRIPS at most brokerages that sell Treasurys (e.g., Vanguard, Fidelity, Schwab).