Yes, you can make sense of the complex pricing of Treasury Inflation-Protected Securities.

By David Enna, Tipswatch.com

Last week, I decided to buy $15,000 of the new 10-year Treasury Inflation-Protected Security — CUSIP 91282CEZ0 — being offered at auction by the U.S. Treasury. I was making this purchase in a Vanguard brokerage account (a traditional IRA), where I had set aside $15,095 in cash for the purchase.

The problem was: Would that $15,095 cover the cost, after any premium/discount to par value, plus any additional accrued principal and interest? The Treasury’s official announcement for the auction wasn’t much help, with all the important pricing details to be “Determined at Auction”:

So I did a quick calculation:

- I was buying $15,000 of par value.

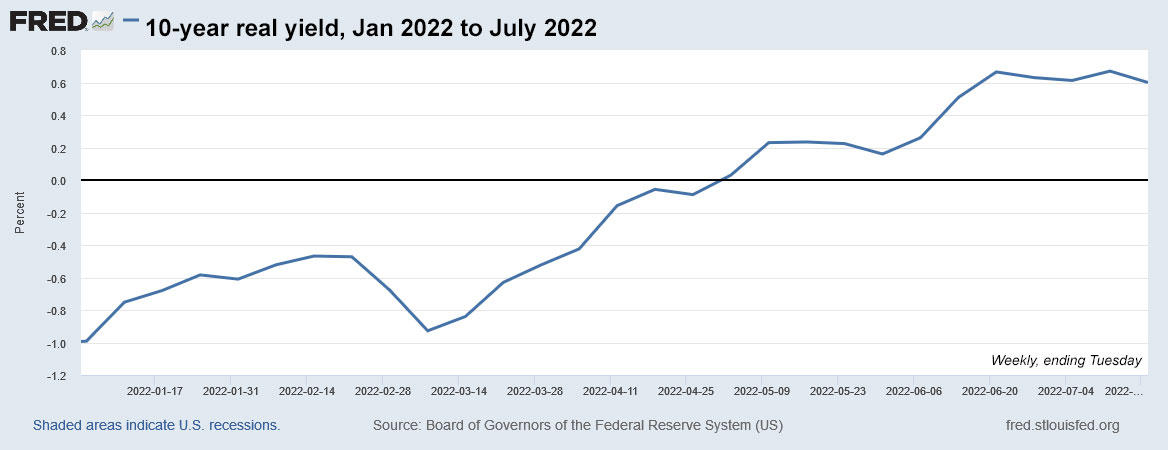

- I knew the real yield to maturity would be at least 0.50%, because that was where the 10-year TIPS market was trading. That would mean the real yield would NOT be below the coupon rate, which only happens when the real yield is less than 0.125%.

- Therefore, this TIPS would be sold with at least a slight discount to par.

- But … this TIPS would have an inflation index of 1.00495 on the settlement date of July 29, so that would add to my purchased principal, and the cost, along with a small interest adjustment for 14 days of the coupon payment (from the July 15 issue date to the July 29 settlement date).

- So, I figured, the highest cost I would end up paying wound be about $15,000 x 1.00495 = $15,074. And I concluded that my $15,095 would cover the cost.

Let’s see what happened

The auction ended up producing a real yield to maturity of 0.630%, which then caused the Treasury to set the coupon rate at 0.625%. When a TIPS has a real yield of 0.125% or higher, the Treasury always sets the coupon rate to the 1/8% below the real yield … 0.125%, 0.250%, 0.375%, o.500%, 0.625% … and so on. A real yield of 0.630% gets a coupon rate of 0.625%, and the price is set at a very small discount to par. A real yield of 0.620% gets a coupon rate of 0.500%, and the price gets a bigger discount.

Here are the auction results, as reported by the Treasury in its official announcement:

So, what does this all mean — high yield, adjusted price, unadjusted price, adjusted accrued interest, index ratio — and how does it affect the price I paid?

The high yield becomes the TIPS’ official real yield to maturity in the auction records. It is the highest yield the Treasury had to grant to complete the $17 billion offering of this TIPS, and it is the real yield granted to all non-competitive bidders (that’s pretty much anyone putting in a purchase order at TreasuryDirect or through a brokerage).

After the auction was completed, Vanguard reported my cost for $15,000 of par value to be $15,070.55. What factors went into setting that price? Once the high yield was set, all the other pricing fell into place Let’s take a look:

The key factor in this chart is the unadjusted price, which was $99.9517 for $100 of par value, and that meant my core cost for the $15,000 in par value was $14,992.75.

But, because of the inflation index of 1.00495, I will be purchasing 14 days of inflation-adjusted additional principal on the settlement date of July 29. That raises my cost to $15,066.97.

In addition, I will have to pay for the 14 days of coupon rate interest that will have accumulated by July 29. Since the coupon rate is 0.625%, 14 days of interest would be about 0.0239%. That is why the adjusted accrued interest is set at $0.239 per $1,000 of par value. Since my accumulated principal will equal about $15,066.87 on July 29, my accrued interest is about $3.60.

And that sets the total cost of the investment: Inflation adjusted value + accrued interest. $15,066.87 + $3.60 = $15,070.57. (OK, Vanguard said it was 2 cents less. I’ll take it. Savings!)

The last line on that chart shows the total value of the investment on July 29, which is simply par value ($15,000) x the inflation index (1.00495) = $15,077.85. In this calculation, I am ignoring the coupon interest which will be paid out as current income twice a year. Also, don’t confuse “total value” with “market value.” Total value reflects only par value + inflation accruals. Market value adds in the fact that the price of a TIPS changes daily on the secondary market. If you are holding to maturity, you can more or less ignore market value.

Happy side note: The inflation index for this TIPS on Aug. 31 will be 1.01939, up 1.3% for the month because of the high rate of non-seasonally adjusted inflation in June. That will put its total value at $15,290.85. Not bad.

Conclusion

I hope this primer on TIPS pricing is helpful. The July 21 auction was an easy one because the real yield ended up just a hair above the coupon rate, making the unadjusted price very close to par. In the last two years that hasn’t be true, with negative real yields far below the lowest possible coupon rate of 0.125%. I am hoping we are entering a new era of positive real yields and much more sensible TIPS pricing.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I will point out that TipswatchChat is a very careful reader and often points out my typos and wording errors,…