Have you given up on longer-term Treasurys? It’s time to get back in the game.

By David Enna, Tipswatch.com

You’ll never see me screaming “buy, buy, buy” like CNBC’s resident madman, Jim Cramer, but I do think that sensible, conservative investors should take a look at Thursday’s 10-year TIPS reopening auction.

The Treasury is offering $15 billion in a reopening of CUSIP 91282CEZ0, creating a 9-year, 10-month TIPS. An interesting side note is that $15 billion is the highest-ever amount offered at a 10-year TIPS reopening auction. These offerings have grown from $12 billion in March 2020, to $13 billion in March 2021, to $14 billion in September 2021 and now $15 billion in September 2022. That’s an increase of 25% in 2 1/2 years, and is evidence that the Treasury isn’t de-emphasizing TIPS in these inflationary times.

CUSIP 91282CEZ0 had its originating auction on July 21, 2022, when it generated a real yield to maturity of 0.630%. Its coupon rate was set at 0.625%, making it the first 10-year TIPS with a coupon rate above 0.125% since July 2019.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.07% means an investment in this TIPS will exceed U.S. inflation by 1.07% for 9 years, 10 months.

Because this TIPS trades on the secondary market, we can track its current real yield and price in real time on Bloomberg’s Current Yields page. It closed Friday with a real yield of 1.07% and a price of $95.84 for $100 of par value. The price is at a discount because the real yield is well above the coupon rate of 0.625%.

If the real yield holds above 1% at Thursday’s auction, this would be the first 9- to 10-year TIPS with a real yield that high since November 2018, very close to the end of the Fed’s last tightening cycle. In fact, since November 2018 there have been 22 TIPS auctions of this term and 12 of them generated real yields negative to inflation. These days, a real yield of 1% or higher is something to celebrate.

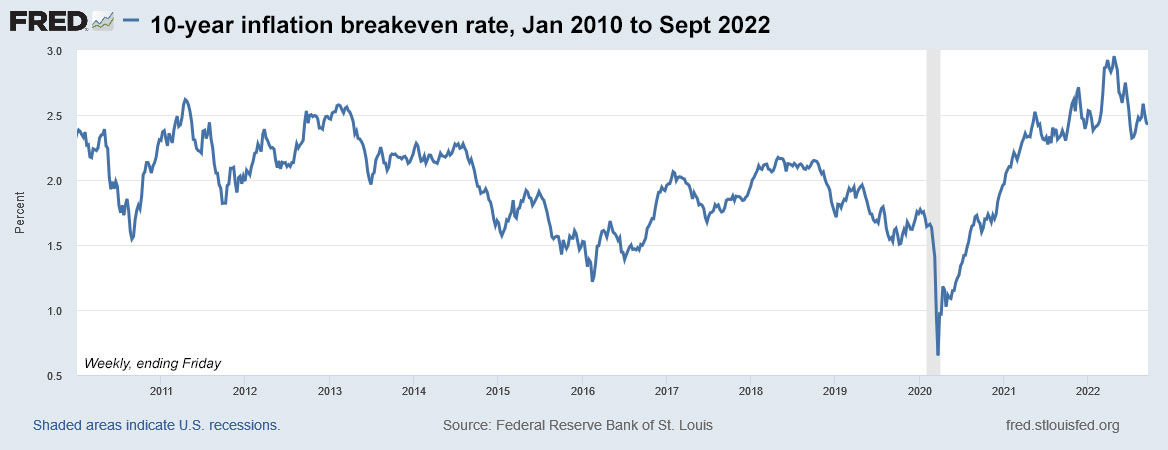

In this chart, I am taking a long view of 10-year real yields, back to January 2010, a year before the Federal Reserve began aggressive quantitative easing. The chart shows how yields peaked at the end of the Fed’s last tightening cycle in November 2018, and then went deeply negative after the Covid outbreak in March 2020.

Pricing for this TIPS

CUSIP 91282CEZ0 will carry an inflation index of 1.01972 on the settlement date of September 30, meaning that investors will be purchasing a bit less than 2% of additional principal, but at a discount of $95.84 for $100 of value (a current pricing). That will work out to about $97.73 for $101.97 of principal, plus maybe 13 cents of accrued interest, making the total cost around $97.86 for $101.97 of principal. That is a rough estimate and things can change before Thursday’s auction.

And keep in mind that the inflation index on this TIPS will drift down slightly in October, ending the month at 1.01936, based on slightly negative non-seasonally adjusted inflation in August. The markets know this is coming, and the auction price will reflect the minor change.

Inflation breakeven rate

With a 10-year nominal Treasury note now trading with a yield of 3.45%, this TIPS currently has an inflation breakeven rate of 2.38%, which looks like a reasonable and attractive number. Inflation over the last 10 years, ending in August, has averaged 2.5%. If you believe that inflation will run lower than 2.38% over the next 9 years, 10 months, buy the nominal Treasury. If you believe inflation will run higher, buy the TIPS.

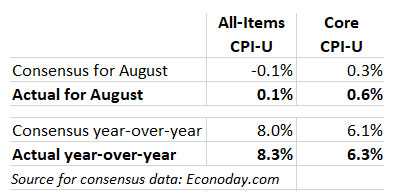

Here is the trend in the 10-year inflation breakeven rate since January 2010, showing how inflation expectations have been backing off since the Fed began tightening measures in March 2022:

Conclusion

It’s no secret that I am a fan of this auction’s potential, as long as real yields continue to hold throughout this week. That’s no sure thing, with a potential market disruption coming Wednesday when the Federal Reserve announces its decision on short-term interest rates. The market expects a 75-basis-point increase. If that what happens, yields should hold. But a month ago, on Aug. 18, the 10-year real yield was sitting at 0.36%. Anything can happen. In fact: Expect anything to happen.

Anyway, I was a buyer of this TIPS at the originating auction on July 21, and I was pleased with the real yield and coupon rate set at 0.625%, which can help cover the effects of any minor deflationary months. For the hold-to-maturity investor, there is very little risk in this TIPS. Obviously, I will be a buyer Thursday, if conditions hold. This is my opinion, and I am a journalist, not an adviser.

How high could real yields rise? This will depend on how high the Federal Reserve allows nominal rates to rise. If the 10-year note reaches 5%, it’s conceivable that the real yield of a 10-year TIPS could rise to 2.2% to 2.5%. But will the Fed sustain the courage to push rates higher, even if the U.S. economy is in turmoil? My gut says “not likely.”

I know there is also a lot of interest in the new 5-year TIPS auction coming up on Oct. 20. That one could produce a coupon rate of 1% — or maybe even 1.125% — and a real yield of about 1.13%. It will be reopened at auction on December 22, when we will know the full extent of the Federal Reserve’s interest rate decisions. In the last tightening cycle, the December 5-year TIPS reopening auctions were always among the best of the year.

Potential investors in CUSIP 91282CEZ0 can check how it is trading in real time on Bloomberg’s Current Yields page. This auction closes at noon Thursday for non-competitive bids, like those made at TreasuryDirect. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting the results soon after the auction closes at 1 p.m. EDT.

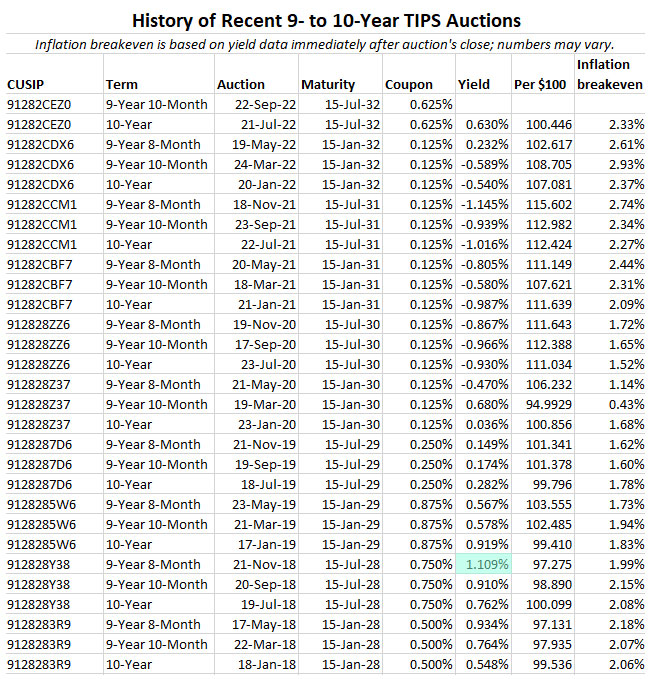

This same 10-year TIPS will be reopened at auction again on Nov. 17, giving investors one more chance at it. Here’s a history of all 9- to 10-year TIPS auctions dating back to January 2018. I have highlighted the single auction, in November 2018, with a real yield above 1%.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

bdp453, it's not clear from your brief inquiry whether you are trying to learn the basic facts about TIAA Traditional,…