May inflation set another 40-year high. Food, gas and shelter prices were key factors, but prices were up in every category.

By David Enna, Tipswatch.com

This is getting a bit dangerous, don’t you think?

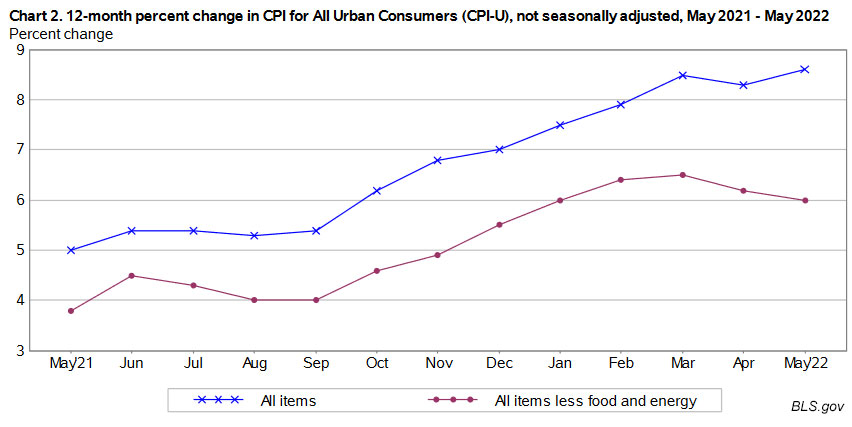

Seasonally adjusted U.S. inflation increased 1.0% in May, the U.S. Bureau of Labor Statistics reported today, much higher than the already-scary 0.7% predicted by economists. The year-over-year number rose to 8.6%, the largest 12-month increase since the period ending December 1981. Economists had been predicting the annual number would fall to 8.1%, down from April’s 8.3%.

Core inflation, which removes food and energy, also exceeded economist predictions, coming in at 0.6% for the month and 6.0% year-over-year.

The higher-inflation surprise wasn’t actually a surprise, since economists have been under-predicting U.S. inflation for more than a year. But this was a very big miss.

In its usual understated tone, the BLS said the May price increases were “broad-based.” (No kidding! There wasn’t a single major price category with declining prices.) The indexes for shelter, gasoline, and food were the largest contributors to the May all-items increase. Let’s take a look at some of the numbers:

- Gasoline prices were up 4.1% in May, after falling 6.1% in April. Gas prices are now 48.7% higher than a year ago. (And we can be sure these costs will soar again in June.)

- Food prices continued surging, with the food-at-home index rising 1.2% in the month and 10.1% over the last year, the highest annual increase since the period ending April 1979. The BLS noted that all six major grocery store food group indexes rose in May.

- The index for dairy prices rose 2.9%, its largest monthly increase since July 2007. The price of meats, poultry, fish and eggs was up a stunning 14.2% for the month.

- Shelter costs rose 0.6% in May and are up 5.5% for the year. This index seems likely to continue to rise as rent increases roll into the market.

- Airline fares were up 12.6% in May, after rising 18.6% in April.

- Apparel costs were up 0.5%, after falling 0.8% in April.

Here is the trend in year-over-year inflation over the last 12 months, showing how the all-items index continues soaring higher (thanks to gas and food prices), while core inflation has settled in around 6%, an intolerably high number:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For May, the BLS set the inflation index at 292.296, an increase of 1.1% over the April number.

For TIPS. The May numbers mean that principal balances for all TIPS will increase 1.1% in July, after increasing 0.56% in June. For the year ending in July, TIPS principal balances will have increased 8.6%. Here are the new July Inflation Indexes for all TIPS.

For I Bonds. The May number is the second in a six-month string that will determine the I Bond’s new variable rate, which will be reset on November 1 based on inflation from March to September. So far, just two months into this rate-setting period, the I Bond would get a variable rate of 3.34%. Since four months remain, a lot will change before the November reset.

Here are the data so far:

What this means for future interest rates

It’s clear that the Federal Reserve will have to continue its course of aggressive (some would say the course is actually moderately-aggressive) increases in short-term interest rates, while also slashing its huge balance sheet of U.S. Treasurys. A lot of this has been priced into the market already, but today’s inflation report clearly shows the Fed can’t veer off this course.

It’s likely that the yield curve will continuing flattening. A 5-year nominal Treasury is trading this morning with a yield of 3.13%, higher than the 10-year yield (3.06%) and equal to the current 30-year yield (also 3.13%). This is a strong signal that the financial markets fear a weakening U.S. economy, even as inflation continues at historically high levels.

From this morning’s Wall Street Journal report:

The continued rapid pace of price increases adds pressure on the Fed to raise rates aggressively to tame inflation. “The big picture is that inflation remains very stubborn and will continue to be very slow to recede,” said Sarah House, senior economist at Wells Fargo Securities. “With what we see in energy markets in the past few weeks, we are unlikely to have seen the peak in inflation this cycle yet.”

A key concern is this: Can the Fed continue to have the fortitude to fight inflation even if the U.S. economy begins slowing, the stock market declines and unemployment increases?

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

With TIPS funds if you hold to duration will this ensure not taking a nominal loss like holding individual TIPS to maturity? My concerns is if the fund doesn’t hold them to maturity then they would be taking losses when the sell and replace right? But does it even out somehow?

Hello David, I am new to buying 5 yr TIPS at the upcoming auction at Fidelity. How do I calculate the adjust principal given the coupon, Ref CPI and inflation index ratio? I have been purchasing I bonds for several years now, but I am still learning. Thank you in advance for your help.

Hello Jimmy and welcome to the world of TIPS. When you buy at a reopening auction, you can keep an eye on secondary-market trading on Bloomberg’s Current Yields Page: https://www.bloomberg.com/markets/rates-bonds/government-bonds/us …. The 5-year TIPS listed there is the one being reopened, so you can at least get an idea of the real yield to maturity and the price for $100 of par value. If you read this post and the comments, you will see some explanation and rough estimates of the likely price and yield, but things can change before Thursday: https://tipswatch.com/2022/06/19/this-weeks-5-year-tips-reopening-auction-looks-like-a-winner/

I do write a preview of every TIPS auction, and so you can follow this site (enter your email in the box in the right hand column) and you can get some idea of what is coming up.

Pingback: Attention investors: TIPS are now a viable, attractive alternative to I Bonds | Treasury Inflation-Protected Securities

This is the third day in a row where bond prices continue to fall precipitiously.

The 5 Year TIPS costs $99.75 WITH the inflation adjustment.

With the 5 year TIPS reopening next Thursday, if this holds I’ll be a purchaser.

Originally, I was hesitant because I don’t like purchasing anything over $100.

If the current trend holds thru next week, this may not even be a worry.

A month ago, I figured that I would have to wait until October’s 5 year new issue.

Now the question is what percentage of my TIPS allocation for the year should I do now?

Here’s the TIPS auction schedule for the rest of 2022.

06/23/22 5 Year Re-Open

07/21/22 10 Year New-Issue

09/22/22 10 Year Re-Open

10/20/22 5 Year New-Issue

12/??/22 5 Year Re-Open

I’ll probably just go with 25% of available funds for TIPS at next week’s 5 year reopening.

Then see how the rest of the month and year pans out.

Not for nothing, there are many Czech, Slovak and Magyars that would take exception to be called “Eastern Europeans”.

The yields went-up significantly today.

The 10 Year TIPS would cost $99.60 WITH the inflation adjustment.

Since at maturity you’d be getting par value times the inflation factor, that’s a no lose proposition.

Unfortunately, the minimum quantity at my broker was 150.

$150K is a tad more than I want to invest at any one point in time.

So, I may be forced into just waiting for the July new issue auction in July.

I’m new to TIPS and this site yet if I understand the TD web site correctly, wouldn’t you just purchase TIPS in the June auction for the amount you desire? Go direct without a broker. https://www.treasurydirect.gov/instit/marketables/tips/tips.htm

Yes, definitely, you can buy TIPS directly at auction at TreasuryDirect, with no costs or fees. However, if you want to hold them in a tax-deferred account, you’d need to buy them through a broker in an IRA account. Most big brokerages (Vanguard, Schwab, Fidelity) let you buy TIPS at the auction with no commission. You get the same price buyers get at TreasuryDirect.

Thanks for the update, David, and I am glad you enjoyed your recent trip to Eastern Europe. A whopping 1% increase in TIPs’ inflation adjusted principal just for the month of July! That’s nice compensation for inflation. I purchased additional bonds of 5 Year and 10 Year TIPs for my IRA account today, as they all have positive real yield today. According to my calculations, by July 31, my inflation adjusted principal of all the 2022 issued 5, 10 and 30 year TIPs I have purchased so far this year combined will have exceeded my total purchase costs (including accrued inflation and interest) by 2.59%. I do not believe that the Fed will raise short-term interest rates above the rate of CPI-U; hence the 5 and 10 year TIPs, priced currently, might turn out to be a good hedge against higher and longer than expected inflation and beat the returns of conventional 5 and 10 year T Notes. I believe that current 5-10 year inflation expectations in the market may turn out to be too low.

I bonds are definitely the way to fly. Those bought in 2000/01 are paying close to 13%, tax deferred; currently, the best deal in Dodge.

Ah yes, my wife and I began buying I Bonds throughout 2001, when the purchase limit was much higher. Those issues have fixed rates of 3.4% and 3.0%. Really nice assets, with 9 more years to go.

Serious question: are you going to cash them in all in the year they come due, or start a year or two early to avoid a higher tax bracket? Nice problem to have.

It is a good question. This year I have some EE bonds purchased in 1992 maturing (they have quadrupled in value) and I have planned for this taxable income in my overall plan for the year. I set an annual target income level, based on IRA withdrawals or conversions, so this year the EE Bonds will form a hunk of that income. As the year 2030 approaches, I’ll probably take a look at the I Bonds and the current rate situation. Otherwise, I’ll just adapt my income plan to that lump sum coming in.

Damn, sure wish more of my TiPS were in a tax-sheltered account. I’ll be playing ‘Taxman’ by the Beatles come April.

I have quite a few TIPS in a taxable account at TreasuryDirect, but I stopped purchasing them that way after I retired. The benefit of this setup is that you pay taxes owed yearly and when the TIPS matures, there is very little tax effect. That’s how I have been funding I Bond purchases for a couple years.

Seems like a good plan to me. I stopped buying TIPS thru Treasury Direct when then they ceased selling them for you. No charge at Vanguard brokerage.

If this sort of appreciation goes on I’ll be cashing in some early. Bracket creep!

As far as anything being baked in, well that’s all stock market rose colored glasses talk.

The “all knowing” market prognosticators were selling March as “peak inflation”.

Hopefully, the FED will get serious about unloading it’s Treasury bond holdings.

I’m getting FED-up with their continual postponing of selling-off their obscene amount of bonds.

Well, the 5 year TIPS currently has a yield of 0.01% (now it’s back to 0.06%).

If this news doesn’t push it positive, I don’t know what will.

I’ve been hemming and hawing about paying the inflation index premium on current bonds.

With this kind of inflation it certainly won’t take long to cover that.

The sad thing is that TIPS yields are so absolutely paltry.

Getting excited about a 0.31% yield on a 10 year TIPS is just plain bizarre.

Before 2008, they were yielding in the 2% range.

Since then ZIRP and QE pushed the rates negative (then they peaked at 1% in 2019).

I ran across an interesting quote about the type of people who purchase TIPS.

The article is titled “20 Years In, Have TIPS Delivered?” by Maciej Kowara.

I find his analysis of TIPS lacking because it ignored ZIRP and QE’s affect on TIPS.

He also kept using TIPS index funds as a proxy for the actual bonds themselves.

Here’s the quote.

“The best that can be said is that they (TIPS) provide explicit insurance against inflation, and may thus be attractive to those investors who are really buying insurance rather than investing. Given those investors’ demand for certainty, they should more properly be called savers.”

I created this site in 2011 and in the early years I was always complaining about “less-than-historical” real yields. After 11 years of Fed manipulation, I can’t say I know what the real historical rate would be. I think the 10-year TIPS real yield could get near 1% or more, but inflation expectations could hold it down,.

Well, the 5 year TIPS finally went positive (+.08).

So, it finally looks like I’ll be able to start purchasing some TIPS this year.

This bodes well for the upcoming June auction for the 5 year TIPS re-opening.

If things keep headed in the right direction, the July auction for 10 year TIPS might be a golden opportunity for purchasing TIPS below par without an inflation index premium.

If there’s any golden lining behind the latest inflation report, it’s this stuff.

“Fortitude” isn’t a word I associate with our current crop of politicians and high level public servants, so that is the question. An elephant in the room is the impact of rising rates on federal debt rollover and repayment. The absurdly low rates have meant that carrying trillions in debt has been viable. The payment required if rates rise to simply historical norms will be much larger. Where will that money come from?

It’s like the nation took out a variable rate mortgage, then a series of variable rate HELOCs. And now has to choose to drastically increase those rates. Fortitude indeed.

“Where will that money come from?”

It will come from the same place all money comes from; the government will issue it into existence, either as non interest bearing debt (US dollars) or interest bearing debt (US Treasuries)

Thank you for the update.

So much for inflation reaching its peak…

Don’t worry Joe, it’s only “transitory”.