Are we there yet? Probably. Are our troubles over? No.

By David Enna, Tipswatch.com

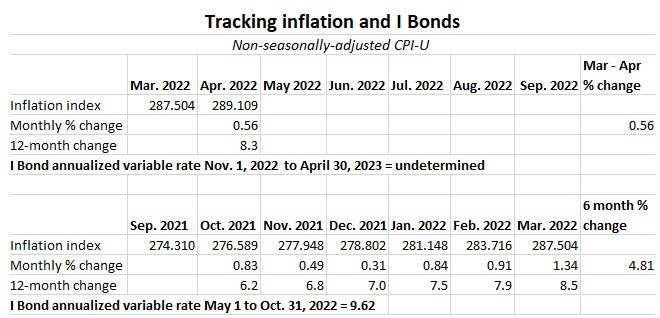

If you’ve been reading coverage of Wednesday’s April inflation report, you might have noticed two strains of news spin: 1) “Inflation is coming down,” or 2) “Inflation is stubbornly high.”

Both takes are true, and sometimes politics may flavor how the media look at current U.S. inflation, which I might mention (totally apolitically) remains at a 40-year high.

I applaud the New York Times for this straightforward take: “Consumer Prices Are Still Climbing Rapidly” and the Wall Street Journal did well with: “Inflation Slipped in April, but Upward Pressures Remain.” And I like how the Washington Post covered all the bases with: “Pace of inflation eases slightly in April but still at 40-year high.”

Less impressive, from MSNBC: “Steve Rattner: U.S. inflation may have peaked” or this, from CNN: “US inflation slowed last month for the first time since August.” Fox Business spun in the opposite direction: “Inflation soars 8.3% in April, hovering near 40-year high.”

OK. In other words, the correct answer is that annual inflation did decline slightly in April, but the U.S. remains in a deep, deep inflationary mess.

Have we hit ‘peak inflation’?

For the answer, let’s turn to Michael Ashton, an inflation guru who explains his thoughts just about weekly in his “Cents and Sensibility” podcast. In this week’s episode, he analyzes the April inflation report, and explains that while inflation may have “peaked” in March, prices are likely to continue climbing, briskly higher, well into 2023.

His take on “peak inflation”:

Peak inflation means different things to different people. … I think some of our leaders are making a big mistake trumpeting peak inflation, which to an economist means that the rate of change is going to decline. … But the consumer, who is not an economist, hears the promise that, hey, we are past the worst inflation and they hear prices are going to go down now. … When we say peak inflation, we mean the rate of change is going to slow, but prices are going to keep going up.

Here is his podcast intro: Have we peaked? Well, arguably the Inflation Guy peaked in his 20s but we are talking about inflation here. While CPI has nominally peaked in terms of its year over year rate of change, that doesn’t mean prices are going to go ‘back to normal.’ Even more important: it doesn’t mean that we have reached peak inflation pressure. Listen while the Inflation Guy explains.“

Take a listen:

Who is Michael Ashton?

His audiences know him as the “Inflation Guy.” He is a pioneer in the U.S. inflation derivatives market. Before founding his company, Enduring Investments, Ashton worked in research, sales and trading for several large investment banks including Bankers Trust, Barclays Capital, and J.P. Morgan.

Since 2003, when he traded the first interbank U.S. CPI swaps, and 2004 when he was the lead market maker for the CME’s CPI Futures contract, he has played an integral role in developing new instruments and methods for accessing and hedging various inflation exposures. In 2016, Mr. Ashton published What’s Wrong With Money? The Biggest Bubble of All. He is a graduate of Trinity University and lives in Morristown, New Jersey.

Have a question? Get the Inflation Guy app in the Apple App Store or Google Play, or email InflationGuy@enduringinvestments.com.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I buy i-bonds as long term investments, so I am always most interested in the fixed rate. Looks like I…