‘We are, unfortunately, about to go through a period of prolonged, persistent high inflation.’

By David Enna, Tipswatch.com

There’s a lot of speculation in financial markets right now about an upcoming dip in U.S. inflation, triggered by a strong decline in gasoline prices. We saw some of that effect in July with all-items inflation flat for the month, even though core inflation rose 0.3%. We could see a similar result in August inflation, to be released Sept. 13.

So yes, U.S. inflation is falling from its 9.1% annual peak in July, and will probably continue to gradually decline. But by how much, and how fast? How long will it take to get to the Federal Reserve’s target of 2% annual inflation?

Here’s a clearly explained outlook from Campbell Harvey, a Canadian economist who is professor of finance at Duke University and a Research Associate of the National Bureau of Economic Research in Cambridge, Massachusetts. In the video, Harvey explains why statistical and structural evidence points to U.S. inflation remaining at an annual rate of of at least 6.2% by the end of the year, even if deflationary pressures continue for several months. A more realistic number might be above 7.0%, he suggests.

“It’s kind of obvious looking at the data, but a lot of people don’t pick it up, is that we’ve already had year to date … 6.3% inflation. So if you think that inflation is going to end the year at 2 or 3 percent, it means that we are going to have strong negative inflation. … And I think that is very unlikely.”

Harvey also points out important changes in the way inflation was calculated 40 years ago versus today. The key point is that changes in the shelter index (which is weighted to be about 32% of all-items inflation) were designed to smooth out volatility, and that means inflation is printing lower than reality. The result: “There is more to come. And it is because of this smoothing.”

“The point is, this inflation has already happened, but it is not reflected in the CPI. And it will be reflected in the next year, or maybe longer. So anybody who is telling the story ‘oh well, this is just supply chain or geopolitical risk and we’ll quickly be back down to 2, 3 percent’ … No. You have to look at the actual structure of how inflation is calculated.”

It’s an excellent video. Give it a watch.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Just about every month, I get emails or comments from readers pointing out what appears to be extremely attractive real yields on very short-term TIPS — especially those maturing in less than a year. My usual response is that these real yields get highly exaggerated as maturity nears and only one coupon payment remains.

I’ll admit I don’t fully understand the mechanics of the quoted real yields when TIPS are down to the final months. But I assume — and I am pretty sure I am right — that the market is pricing these TIPS correctly. This month, we have another example, and I decided to take a walk-through look at this possible investment, CUSIP 912828UH1:

CUSIP 912828UH1 was originally issued as a 10-year TIPS on January 15, 2013. I wrote about this TIPS back then, believe it or not. It was in the early years of misery for TIPS investors, with this TIPS getting a real yield of -0.630% and a coupon rate of 0.125%. Now, as it is approaching maturity, it has built up an inflation accrual index of 1.28372 as of September 1. And on Thursday it was trading with an “apparent” real yield of 4.047%, according to the Wall Street Journal’s closing statistics.

So, an investor in this TIPS will be purchasing 28.3% of additional principal above par, and that principal is not protected against deflation in future months. In fact, the principal balance of this TIPS will decline 0.01% in September, based on non-seasonally adjusted inflation in July. We could see more declines in October and November, if falling gas prices create deflationary numbers for August and September, which seems possible.

I went onto Vanguard’s trading platform and entered a $10,000 purchase of this TIPS (for example purposes only — I didn’t complete the purchase). Here is what the order sheet showed Thursday afternoon:

Note that a purchase of $10,000 of par value will cost an investor $12,660.82. Here’s a rundown on the basics of that investment, and note that my total cost is off from Vanguard’s by 5 cents, and I have no idea why:

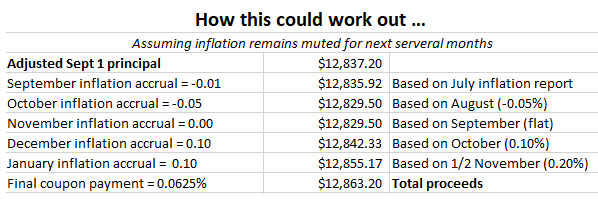

Because of the discounted price, an investor is getting $12,837 of principal from a $12,661 investment, which is attractive. But just how attractive? It’s hard to say, because the final payment at maturity on January 15, 2023, is going to depend on how hot or cold inflation runs through November. The Treasury market is speculating that inflation will decline or at least remain muted through the end of the year, which could be accurate. Or could this be recency bias based on the recent collapse in oil prices?

Here is my speculation on a “muted inflation” scenario for this TIPS, with inflation falling -0.05% in August, then remaining flat in September, rising 0.1% in October and then 0.2% November. (This TIPS will get an inflation adjustment of 15 days from November inflation in its final month.)

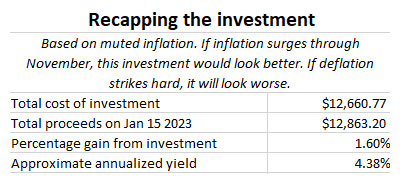

If things work out this way — pure speculation — the investor on September 1 will have invested $12,660 and will get a return of about $12,863 on January 15.That’s a gain of $203, which isn’t shabby for a 4 1/2 month investment. It’s an annualized return of about 4.38%. Not quite up to I Bond standards, but better than similar nominal Treasury yields, which are hanging just above 3%.

Based on this rough look at CUSIP 912828UH1, it seems like a reasonable investment, given the discounted price. The investor picks up the risk of the 28% inflation accrual, which could get depleted if deflation becomes a “thing” in the next several months. My example may be too optimistic. Who knows? The market is clearly signaling a belief that inflation will be very low, or negative, through November.

Would I buy it? No, I am not interested. It’s just too complex to be worth the trouble. This example was simply meant to demonstrate the “logic” of today’s market, which might be logical, or possibly crazed.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I woke up today in rainy Sitka, Alaska. Rain is not an an unusual thing in Alaska in August, I have learned. It has rained every single day on this trip, which started August 14. Rain is in the forecast for the rest of the trip.

But hey, we’ve seen some rainbows … and bears, moose, eagles, ravens, caribou, reindeer … along the way. No otters yet, I want to see an otter.

I know a lot of news has been breaking out in the last two weeks, which always seems to happen when I am traveling, especially in places with little or no internet. From the little I can grasp, it appears that Fed Chairman Jerome Powell finally set the markets straight on his intentions: To fight inflation until inflation is defeated. That was what Powell should have said, and the markets should have expected it.

But, no, the markets still had a lingering belief that the Fed would step in to save the stock market. But that can’t happen while U.S. inflation is continuing at an annual rate of 8.5% and raging even higher across the globe.

So for inflation-protected investments, what has happened in the last two weeks?

The 5-year real yield started at 0.29% on Aug. 15 and closed Friday at 0.47%.

The 10-year real yield started at 0.35% and ended at 0.47%.

The 30-year real yield started at 0.89% and ended at 0.85%.

These aren’t dramatic moves, but the current yields keep the 5- and 10-year TIPS as attractive investment possibilities. There’s a 10-year TIPS reopening auction coming up on Sept. 22, followed by a new 5-year auction on Oct. 20. Both of these could be attractive, especially since the 5-year real yield should track higher with any upcoming Fed moves in September.

I’m not connected enough right now to give an opinion on anything else going on. If you you have ideas, comments or theories, post them in the comments section below.

I will be back home in North Carolina mid-week, as long as I survive whatever Covid protocols are thrown at me in the last days of the trip. In closing, here’s a view of Denali National Park:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The U.S. Treasury’s reopening auction today of CUSIP 912810TE8 — creating a 29-year, 6-month Treasury Inflation-Protected Security — got a real yield to maturity of 0.92%. This was the highest yield for any auction of this term in more than 2 years.

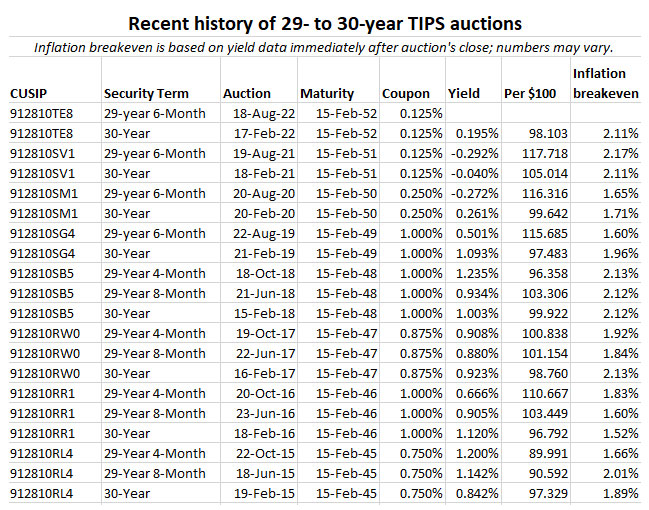

It looks like the auction was met with strong demand, with the real yield coming in a few basis points lower than where this TIPS was trading right before the auction’s close. The bid-to-cover ratio was 2.69, also an indication of good demand.

This TIPS had an originating auction in February, where it got a real yield of 0.195% and a coupon rate of 0.125%. Thursday’s auction demonstrates how much real yields have surged higher in 2022. Investors paid an adjusted price of about $84.61 for about $106.40 of principal, after accrued inflation is added in. This TIPS will have an inflation ratio of 1.06397 on the settlement date of Aug. 31.

The inflation breakeven rate, by my estimate, was 2.21%.

I am traveling this week and I am about to go on a trek into Alaska’s Denali National Park, so I will just close with the usual graphs … Real yields, inflation breakeven rate, and auction history.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

A 30-year Treasury Inflation-Protected Security is a potentially volatile investment. probably most appropriate for big-money investors like insurance companies, hedge funds and central banks. The term of 30 years makes it a tough purchase as part of a hold-to-maturity bond ladder, and the volatility creates uncertainty most small-scale investors don’t need.

The Treasury on Thursday will auction $8 billion in a reopening of CUSIP 912810TE8, creating a 29-year, 6-month TIPS. To give you an idea of this term’s volatility, consider this:

CUSIP 912810TE8 was created at an originating auction on Feb. 17, 2022, with a real yield to maturity of 0.195%, which set its coupon rate at 0.125%. The unadjusted price was about $97.96 for $100 of par value. It sold at a discount because the auctioned real yield was higher than the coupon rate.

This TIPS is now trading on the secondary market and closed Friday with a real yield of 0.90% and a price of about $80 for $100 of par value.

So do the math: In just six months, this TIPS hasdeclined in value by 18%.

However … today’s real yield of about 0.90% is a heck of a lot more appealing than February’s 0.195%. Is it enough to make this offering attractive? Not for me, but it could be for anyone who speculates that real yields will be heading deeply lower in future months.

Definition: The “real yield” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 0.90% means an investment in this TIPS will exceed U.S. inflation by 0.90% for 29 years, 6 months.

Here is the trend in the 30-year real yield over the last three years, showing the strong rise from the never-seen-before 30-year negative real yields triggered by the Fed’s aggressive market intervention after the Covid outbreak in March 2020:

So, yes, a real yield of 0.90% looks pretty attractive. But you don’t have to go back far into TIPS history to find higher 30-year real yields. As recently as February 2019, a 30-year TIPS originating auction got a real yield of 1.093% and a much more attractive coupon rate of 1.0%. But 0.9% isn’t bad by recent standards. You have to go all the way back to February 2011 to find a 30-year TIPS auction with a real yield higher than 2%.

Because CUSIP 912810TE8 has a coupon rate of 0.125%, it is an extremely inappropriate investment to hold in a taxable account (like any purchase at TreasuryDirect). If you bought $10,000 of this TIPS, you would earn $12.50 in the first year from the coupon rate, while potentially owing current-year taxes on an inflation accrual that could top $600 or more in year one. If you are in the 24% tax bracket, this TIPS would potentially be cash-flow negative by $150 or more every year for as long as you held it. Do not buy this TIPS in a taxable account.

Another thing to consider is that this TIPS will carry an inflation index of 1.06387 on the settlement date of Aug. 31. That will ramp up your cost, but also increase your accrued inflation. The adjusted price could end up around $85.12 for $106.40 of accrued value. That is a rough estimate and things could change this week. (Plus there will be a very small amount of accrued interest, about 57 cents on a $10,000 investment).

That means a $10,000 par investment at Thursday’s auction will cost about $8,512 for about $10,640 of accrued principal. For people who worry about severe deflation in coming years, that $640 is not guaranteed to be returned at maturity. However, the chance of that happening is essentially zero.

Inflation breakeven rate

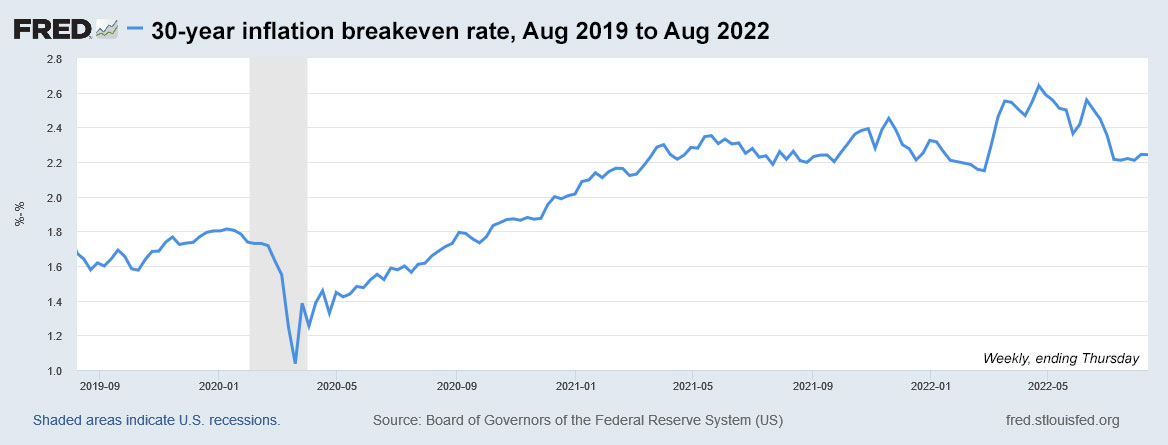

With a 30-year Treasury bond closing Friday with a nominal yield of 3.11%, this TIPS currently has an inflation breakeven rate of 2.21%, which seems in line with historical standards. The market is not forecasting steeply higher inflation over the next three decades. I think that reasonable rate makes this TIPS more appealing than a 30-year nominal Treasury.

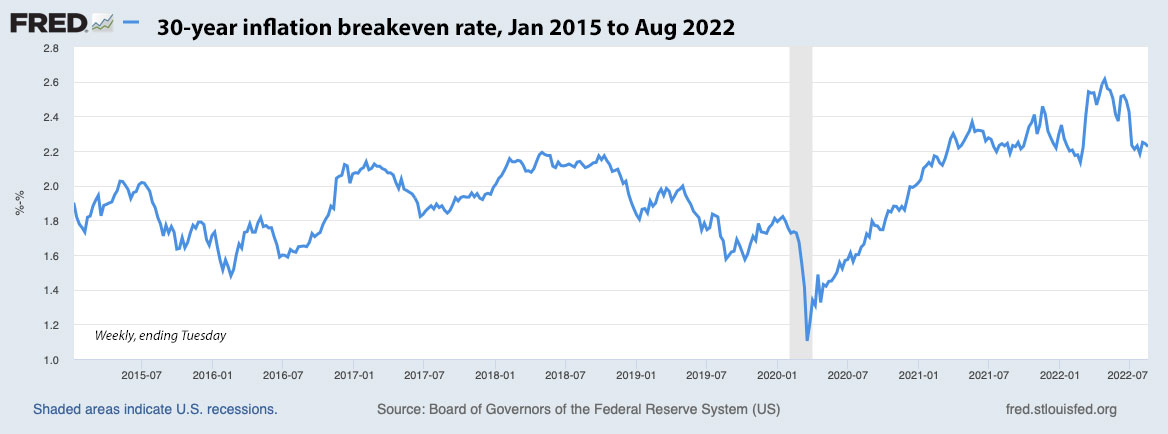

Here is the trend in the 30-year inflation breakeven rate over the last three years, showing that inflation expectations have settled down in recent months as the Federal Reserve began raising interest rates and lowering its balance sheet of Treasury holdings:

Thoughts on this auction

If you are reading this article, thank you. Not many people are interested in a 30-year TIPS. The term is too long and the investment is too volatile for small-scale investors. I’ve purchased two TIPS of this term in my investing history, both in a taxable TreasuryDirect account:

CUSIP 912810FH6 back in April 1999, with coupon rate of 3.875% and a real yield to maturity of 3.899%. Yes, I still hold it and this TIPS will have earned about 12.4% over the year ending in September. Its current inflation index will be 1.80245 on September 1.

CUSIP 912810QP6 in February 2011, just a month before I launched this Tipswatch site. It carries a coupon rate of 2.125% and so it will have earned about 10.6% for the year ending in September.

When CUSIP 912810QP6 matures, I will be 87 years old. I might make it! But any 30-year TIPS I buy today won’t mature until 2052. Prediction: I won’t make it. So the 30-year term falls out of my investing scope. If you are younger, and you want to put a small amount of CUSIP 912810TE8 on the top rung of your TIPS ladder, I can endorse the strategy. Just don’t do it in a taxable account.

You can check the Treasury’s real yield estimates for a full-term 30-year TIPS on its Real Yield Curve page and also see how CUSIP 912810TE8 is trading in real time on Bloomberg’s Current Yields page. This auction closes at noon Thursday for non-competitive bids, like those made at TreasuryDirect. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I’m traveling again

By the time this TIPS auction closes at 1 p.m. EDT Thursday, I will be traveling somewhere in south-central Alaska. I will attempt to post the auction results, but that will depend on if I have internet access and free time. I will also to try check in to answer questions, if you have any.

In the meantime, here is a history of every 9- to 10-year TIPS auction going back to 2015:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

bdp453, it's not clear from your brief inquiry whether you are trying to learn the basic facts about TIAA Traditional,…