When inflation rises to the highest level in 31 years, that is significant.

By David Enna, Tipswatch.com

Attention, Federal Reserve: This 2021 surge in U.S. inflation is no longer looking “transitory.” It’s looking dangerous.

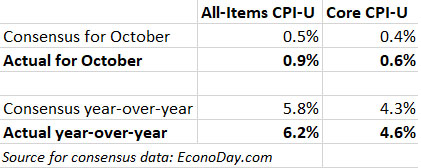

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.9% in October on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 6.2%, a three-decade high. Those results were well above economist expectations for an increase of 0.5% for the month and 5.8% year-over-year.

The annual increase of 6.2% was the largest, the BLS said, since the period ending November 1990, nearly 31 years ago. It noted that the surge in prices was “broad based,” hitting diverse areas like food, medical care, new and used cars, household furnishings and shelter.

Core inflation, which removes food and energy, rose 0.6% in October and 4.6% year of year. Those results also greatly exceeded consensus estimates of 0.4% for the month and 4.3% for the year.

As is usually the case when inflation surges, gasoline prices were a key cause. Gas prices were up 6.1% in October and are now up 49.6% in the last year. Even more troubling is the cost of food: The index for “food at home” increased 1.0% in October, and is now up 5.4% over the last year. The index for meats, poultry, fish, and eggs continued to rise sharply, increasing 1.7% following a 2.2% increase in September. The index for beef rose 3.1% over the month. Over the last decade, increases in food prices have remained relatively moderate. That is no longer the case.

The surge in prices was widespread across the economy:

- Natural gas prices increased 6.6% for the month, the largest monthly increase since March 2014.

- The index for new vehicles rose 1.4% in October and 9.8% year over year.

- Costs for used cars and trucks rose 2.5% in the month, restarting an upward trend after two months of declines.

- Shelter costs rose 0.5% for the month are are now up 3.5% year over year.

- The medical care index rose 0.5% for the month, the largest monthly increase since May 2020.

- One positive note: The index for alcoholic beverages decreased 0.2% for the month.

Here is the trend over the last year for both all-items and core inflation, showing a new surge higher in October after a few months of stability at an already high rate of inflation. The chart demonstrates that monthly inflation numbers are likely to continue very high through March 2022 because of low baseline numbers from early in 2021.

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates on I Bonds. For October, the BLS set the inflation index at 276.589, an increase of 0.83% over the September number.

For TIPS. The October inflation report means that principal balances for all TIPS will rise 0.83% in December, following increases of 0.21% in October and 0.27% in November. For the year ending in December, TIPS balances will have increased 6.2% to match inflation. Here are the December inflation indexes for all TIPS.

For I Bonds. The October report is the first in a six-month period (October to March) that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset May 1, 2022. After just a month, inflation has increased 0.83%, which translates to a variable rate of 1.66%. The current variable rate is 7.12%, based on inflation from April to September 2021.

Here are the relevant numbers:

What this means for future interest rates

In the very short term, I don’t expect the Federal Reserve to take any step to increase its federal funds rate. That is still probably 12 to 18 months away. But in the face of this current inflationary surge, the Fed needs to keep tapping the brakes on its bond-buying quantitative easing. So far this morning, stock market futures are mildly lower, indicating that this inflationary news isn’t scaring off investors.

The Fed says it has the “tools” to calm runaway inflation, but does it have the courage and political will to use those tools, which would involve sending short-term interest rates much higher? This action would also greatly increase the U.S. government’s borrowing costs at a time of massive deficits.

From this morning’s Wall Street Journal report:

“Federal Reserve officials are closely watching inflation measures to gauge whether the recent jump in prices will be temporary or lasting. One such factor is consumer expectations of future inflation, which can prove self-fulfilling as households are more likely to demand higher wages and accept higher prices in anticipation of higher future price growth. … Consumers’ median inflation expectation for three years from now stayed at 4.2% in October, the same as in September, according to a survey by the New York Fed. That level is the highest since the survey began in 2013.”

I do think that people shopping for groceries and seeing prices rising more than 5% over the last year are well aware of this inflationary threat. At least for now, inflation is becoming part of the U.S. economic equation. The Fed knows this.

I’ll end with this commentary from inflation guru Michael Ashton, author of the E-piphany blog:

“Seriously, this month’s report – while expected, at some level – turns my stomach. We have learned these lessons, painfully, long ago: you can’t spend in an out-of-control fashion and you can’t print the money that you’re spending. That’s fiscal policy 101 and monetary policy 101. Flunk them all, I say. … “

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…