My opinion: Long-term investors should buy in October. Short-term term investors could wait until November. But whatever … buy I Bonds in 2021.

By David Enna, Tipswatch.com

With the release of the September inflation report on Wednesday, we got rather stunning news: All U.S. Series I Savings Bonds will have an inflation-adjusted interest rate of 7.12%, annualized, for six months. That rate will launch immediately for I Bonds purchased in November, or in six months for I Bonds purchased in October.

The key thing is: All I Bond investors will get that 7.12% eventually. But if you purchase an I Bond before the end of October, you will get an annualized return of 3.54% for six months, and then the 7.12% for six months. That adds up to a total return of about 5.33% for the year, a stellar number in our dreary world of ultra-low interest rates.

But the obvious question is: Should you buy in October to lock in that 3.54% rate, or wait until November to start off with a bang at 7.12% for six months? Let’s take a look at the pluses and minuses.

Is this a long-term investment?

Do you plan on holding this I Bond for at least five years, when it can be redeemed without the three-month interest penalty? If so, I think buying in October makes more sense than waiting for November’s higher rate. The reason: We don’t know what the next inflation-adjusted rate will be, the one that will follow 7.12%. It will be based on inflation from September 2021 to March 2022. It could be higher, yes, or it could be lower.

But I can assure you that in the next five years, it is highly likely that you will see an inflation-adjusted rate lower than 3.54%. That rate, based on official U.S. inflation from September 2020 to March 2021, was the I Bond’s highest variable rate in 10 years (dating back to the 4.6% variable rate set in May 2011). Because that 3.54% annualized rate is so attractive in today’s market, I encourage long-term I Bond investors to purchase up to the $10,000 per person cap in October, locking in the 3.54% rate for six months, and then 7.12% for six months.

Conclusion: Long-term I Bond investors should make the purchase in October.

Is this a short-term investment?

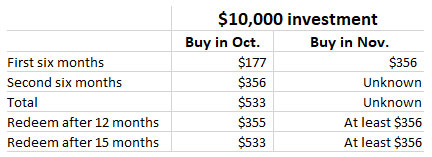

A lot of investors are looking at dabbling in I Bonds for the first time as a short-term investment, possibly for a period as short as 11 months. You can purchase an I Bond near the end of a month and get full interest credit for that month. Then, in the same month a year later, you can redeem it, near the beginning of the month. That cuts the required holding period to 11 months and a couple days.

This short-term investment makes a lot of sense in our current market, getting way-above-market returns on an extremely safe investment. And if this is the strategy you are considering, I think buying in November makes a bit more sense than buying in October. If you buy in October and redeem after a year, you will lose three months of interest at the 7.12% level, cutting your total return on a $10,000 investment down to $355. By waiting three months longer, you can boost that return to $533, because the three-month penalty will apply to a potentially lower variable rate.

If you buy in November, your worst case scenario is a return of $356 after 12 months, even if the next variable rate drops to 0.0%. (A three-month penalty on zero interest is zero.) So buying in November, and then redeeming in one year, makes more sense than buying in October.

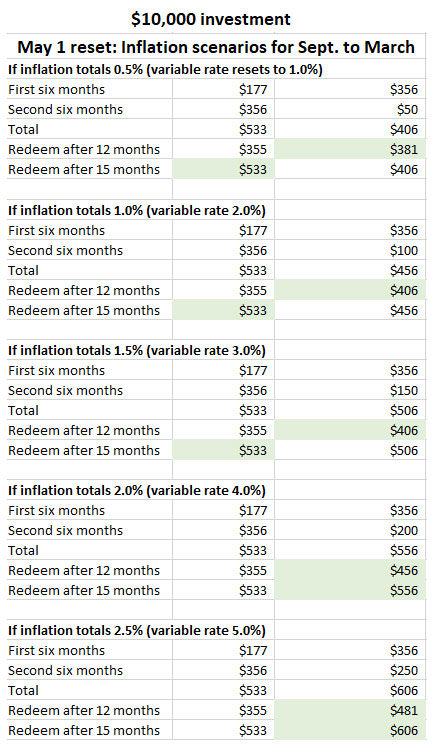

But let’s take a look at potential inflation scenarios for that next rate reset on May 1, determined by inflation from September 2021 to March 2022. That will give us a more accurate picture of the likely effects of redeeming in either 12 or 15 months. Sorry, but here comes a whole bunch of numbers, with the only changes coming in column 2 for “Buy in November.” If you buy in October, you will know your outcomes for 12 and 15 months, because those rates have been set:

In lower-inflation scenarios, buying in October and holding for 15 months will pay off versus the buy-in-November strategy. But that’s not true after 12 months, because of the high-rate three-month interest penalty imposed on the October purchase. In all scenarios, the November strategy wins for a redemption after 12 months.

I have no idea where inflation will be heading from September to March, but I’d guess it will result in a rate reset of 2.5% to 3.5% in May. The higher the variable rate, the higher the advantage for the November purchase strategy.

Conclusion: If you are planning to buy an I Bond and redeem it in 12 months, then the buy-in-November strategy is the winner. If you might hold for 15 months, though, the advantage only comes with higher inflation in the September to March period.

Do you think the Treasury will increase the I Bond’s fixed rate in November?

I think this is highly unlikely, but anything is possible. The Treasury does weird things, sometimes. What if it suddenly decides to give I Bonds a big boost for small-scale savers? Don’t think that will happen. It’s not at all likely.

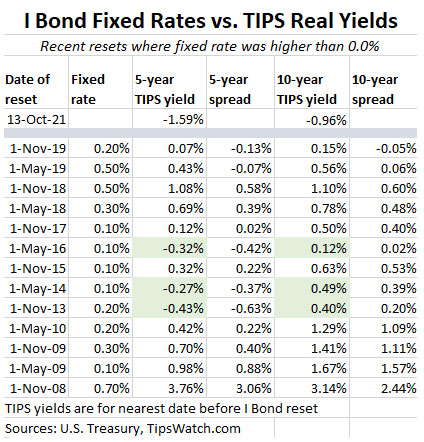

Here is a chart showing the real yields of 5- and 10-year Treasury Inflation-Protected Securities at the time of every recent I Bond rate reset where the rate was above 0.0%.

Note that in no case was the yield of a 10-year TIPS below zero when the I Bond fixed rate was set above 0.0%. The current 10-year real yield is -0.96%. The Treasury really doesn’t need to do anything to give I Bonds a boost. They already have a 96-basis-point advantage over a 10-year TIPS.

Conclusion: There’s not much hope the Treasury will raise the I Bond’s fixed rate above 0.0% for the November 1 reset. But if you believe there is a chance, go ahead and wait for the reset and buy in November.

Don’t overthink this …

I actually believe that buying I Bonds in October, and/or buying in November, are both good moves. (I bought my 2021 allocation in January, by the way.) For a long-term investor, buy in October to lock down that 3.54% rate for six months. For a short-term investor, especially one looking to redeem in the shortest time possible, buy in November.

But, whatever you decide: Buy I Bonds in 2021. Can’t go wrong with that decision.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Fast-forward this thread to July 2022 when the I-bond rate is now a whopping 9.62% – hard to be totally happy about this since it means the economy is in shambles, but let’s make the most of it! I’m a little confused about how I-bond semi-annual compounding works. What are the pros/cons of buying $10k in bonds right now (7/20/22) vs. waiting until the very last day of this current rate offering (10/31/22)? If the bonds aren’t compounded daily or even monthly, why not just wait to write that check until the very last day? Will I earn any money from having deployed that capital for an extra ~100 days? I hate spending money prematurely and will absolutely buy the full $10k by the 10/31/22 deadline to get this juicy rate (and can afford to write the check immediately). In general, should folks get into these bonds as early as possible within each six-month offering period or wait until the last possible minute? (I’ll have this same question come January 2023 when it’s time to write another I-bond check.) Thank you for simplifying things for me!

<>

The only pro is that you start the clock ticking immediately if you want to redeem this I Bond in 12 months (with penalty) or after 5 years (no penalty). A purchase in the last week of October will earn 9.62% for a full six months, and then the next variable rate (probably around 7% to 8%, annualized) for the next six months. If you buy near the end of a month you get credit for a full month of interest.

On the 10/31 deadline: That’s a Monday. Do not set up a purchase for Oct. 31 because it will end up being issued in November. I’d suggest setting up that order for Oct. 27, to make sure it gets applied to October. If buying in July, I’d make sure to put the order in by Wednesday, July 27.

Thanks for the advice! Barring life disaster, plan is to sit on these bonds for minimum of five years so delaying the ticking clock a few months isn’t something I lose sleep over. Is this correct: if I buy bonds with an effective date of 7/25/22, I’ll get 9.62% annualized interest for July, August, Sept, Oct, Nov, and Dec (six months) and the new rate will kick in starting Jan 2023? But if I buy bonds with an effective date of 10/25/22. I’ll get those same payments for Oct, Nov, Dec, Jan, Feb, and March (six months) and the new rate will kick in starting April 2023?

I’ll be sure to add at least a week of buffer between when I make the purchase and the end of the month to take advantage of snagging the full month of interest with less than a full month of investment – I like that nuance!

Yes, the months you listed look correct.

Pingback: What are they and why should you buy some now? | Finance News

I purchased ibonds in 2011. Do you think I should sell those and purchase again or leave them as it is.

I don’t want to increase my bond portfolio more than where it is.

If you bought I Bonds in 2011, you have a fixed rate of 0.0%, same as the current fixed rate. You don’t need to do anything. Just hang on to those I Bonds, which will mature in 2041. All owners of all I Bonds will get that 7.12% annualized rate for six months, after six months of 3.54% ends.

Pingback: What are they and why should you buy some now? – National Financial Solution

Pingback: What are they and why should you buy some now? – Finance News Reporter

Pingback: I Bond rates can be an inflation hedge: What are they and why should you buy some now? - Daily News Updates

Pingback: I Bond rates can be an inflation hedge: What are they and why should you buy some now? - Times News Network

Pingback: I Bond rates can be an inflation hedge: What are they and why should you buy some now? - Questlation

Pingback: I Bond yields can be an inflation hedge: what are they and why should you buy one now?

Pingback: What are they and why should you buy some now? – Daily Grinder News

Pingback: I Bond rates can be an inflation hedge: What are they and why should you buy some now? | CNCB News

A somewhat minor consideration that I haven’t seen you mention in terms of which issue to buy:

It probably makes sense as you accumulate I bonds to have a pool of “early” I-bonds – (that is earning the announced rates immediately e.g. purchased in May or Nov) and a pool of “late” I-bonds (that is always earning the “old” 6-month delayed rate, e.g. purchased in Apr or Oct).

When you do want to redeem a portion of your I-bonds in the future, this gives you maximum flexibility in terms of which interest rate you want to forego. This becomes most significant if redeeming within 5 yrs and paying 3 months interest penalty. You’ll always have the choice to pay the penalty with the “new” rate or the “old” rate.

In normal times, the strategy should be to redeem the I Bonds with the lowest fixed rate. So if you need some cash, redeem I Bonds with a fixed rate of 0.0%. Of course, it is better if you have held the I Bonds for 5 years. I have always been very reluctant to redeem any I Bonds, since you can’t make up the difference because of the purchase cap. But I have in the past redeemed 0.0% fixed-rate I Bonds to buy 0.5% fixed-rate I Bonds.

Pingback: What are they and why is it a good idea to buy them now? – BMG

Pingback: What are they and why is it a good idea to buy them now? - Trending Now?

Pingback: What are they and why is it a good idea to buy them now? - Pehal News

Pingback: ¿Qué son y por qué es una buena idea comprarlos ahora? - flashinformativo

Hi David thank you for this post it was very helpful. I’m going for the long term investing approach and will buy I bonds towards the end of this month.

For next year 2022, it would likely make sense then to purchase I bonds towards the end of January so that you can lock in 6 months of 7.12% interest? Thanks again.

My usual approach would say to wait until April, when you will know the next variable rate and also get a better idea if the fixed rate will increase. (In April, you’d still get the 7.12% for six months.) However, buying in January seems like a safe decision. On a $10,000 investment, you’d earn $356 in the first six months. If the fixed rate rose to 0.2% in May, that would provide only $20 extra dollars a year, meaning it would take nearly 18 years to make up for the $356 you could have earned by buying in January.

Hi David,

Would you give us your opinion on whether it’s better to pay the fed taxes annually or wait until redemption? According to TreasuryDirect it’s an either/or option: once you start paying taxes annually you can’t revert to paying taxes on redemption.

I realize that, as a rule, it’s best to defer taxes. However, if one doesn’t redeem the I-Bonds for ten or twenty years, and pays the tax upon redemption, then one will take a significant tax hit in the year of redemption, as opposed to taking minor tax hits each year between now and then. Moreover, a big tax hit twenty years hence could conceivably push one into a higher tax bracket in that tax year, not to mention the likelihood that tax rates will almost certainly be higher then than they are now. Therefore, I think it would be preferable to bite the tax bullet each year rather than waiting. What do you think?

Thanks for your excellent blog.

I have had feedback from a few readers (very few) who paid the tax annually. The primary reason has been to avoid having their children, who will inherit the I Bonds, having to pay taxes. I’m in favor of deferring the taxes and “hoping” I can manage the future bill by redeeming in a year when I can keep my adjusted gross income low. I think the tax deferral is a major plus of I Bonds, at least for ease of ownership for 29 years. The 30th year is a bit more complicated.

Apart from the trivial taxes I’ll pay on I-Bond interest, the only taxes I’ll pay here forward is on my SS and my IRA RMD, which should largely cover my living expenses. However, my effective tax rate will nearly double over the next 20 years, even if the IRS tax brackets inflate by 3% per year as they have historically, and that’s assuming that there are no future marginal tax rate increases, which is unlikely. I think I prefer the devil I know to the devil I don’t.

Thanks for your reply.

Thanks David, Love your articles. You seem to know just about all the procedural details related to I bonds, here’s one for you:

What’s the time frame / policy for buying (paper) I bonds with a tax refund? Specifically, we’re going to have a biggie coming in the 2022 tax season. Those buying I bonds with their tax refunds are going to want to lock in the juicy 7.12% rate which is available on purchases thru Apr 30, 2022. What determines the date of purchase for the I bonds from a tax refund and hence the initial rate?

For those filing near the Apr 15 deadline, that doesn’t leave much time for the return to be processed and I bonds purchased before Apr 30. Personally, I don’t receive all my tax documents until early-Apr so filing early isn’t really an option but I’d love to find a way to add an extra $5K starting at the 7.12% rate.

So… How does it work? Is there as processing delay or is the transaction back-dated to the filing date? Does it matter if you e-file or paper-file? Any other relevant details / tricks you can share?

I’ve never done the tax return purchase, so I don’t have any experience with how it works. I am guessing that filing near the April 15 deadline could push the purchase into May, or even beyond. TreasuryDirect has this: https://www.treasurydirect.gov/indiv/research/faq/faq_irstaxfeature.htm

How long will it take to receive my paper savings bonds?

They will be issued and mailed after the IRS processes your return. Once your savings bonds are issued, you should get them within three weeks. …

What will the issue date of my bonds be?

The issue date for paper bonds will be the first day of the month in which IRS submits payment for the bonds to the Treasury Retail Securities Site in Minneapolis. For example, if Minneapolis receives your order from IRS on February 18, the issue date of your savings bonds will be February 1.

my experience this year: filed taxes electronically March 14th and I Bonds purchased with refund were dated March ’21

Thanks. That’s a good data point. So they were able to issue the I-bonds within 2 weeks of electronic filing. Processing could be a little slower if submitted right near the Apr 15 deadline (big backlog of returns) but good to know.

Another data point here we filed our tax return on the E-file deadline Oct 15. Just received my paper bonds today Oct 30 in the mailbox, those bonds were issued on Oct 27.

Can we buy I or EE bonds in IRA accounts ?

No. Savings bonds cannot be purchased in a tax-deferred account.

For years I’ve been trying to get friends of mine to buy I-bonds while they lamented low interest rates. Finally, after reading some of your recent articles I’ve forwarded to them, they are buying.

Great to hear. Your friends “GOT THE MESSAGE!”

As indicated above, an I Bond may be redeemed at any time after 12 months from its issue date which is the first of the month during which you pay for it. So it’s true that the minimum holding period is 11 months and a couple of days. However, that minimum holding period results in a minimum 13 months of interest (before deduction of the penalty), not 12. For example, if you buy at the end of October 2021, your issue date is October 1, 2021 and that’s your first month of interest. You can redeem, at the earliest, on October 2, 2022. September 2022 is your twelfth month of interest and on October 1, 2022 you become entitled to your thirteenth month of interest. I think the tables above reflect a net 9 months of interest after the 3-month penalty, rather than 10 months.

Good logic, Alan. But I did some research (thank you Bogleheads!) and found this:

Tips for buying I Bonds …. Since I Bonds earn the full month’s interest if you own them on the last day of that month, it is generally a good idea to buy I Bonds at the end of a month after also earning interest on that same money in a bank account during most of that same month. Conversely, you would want to redeem your I Bonds at the beginning of any month, since holding them until later in the month will not earn any additional interest, unless you own them on the last day of the month.

The month’s interest for an I Bond is accrued on the last day of the month, so you have to hold them for the entire month to get credit for that month’s interest. When you buy an I Bond late in the month, you own it on the accrual date. But if you sell early in the month, that month gets no interest and so it would not apply to the 3-month penalty.

Treasury Direct is a nightmare for Estate Purposes. Your not talking about buying a fund, right? Coverted some bonds to electronic,TIPs, and amazed on how cryptic TD is! Looks like a Trust they even have a specific naming convention!

My experience with Treasury Direct has been very good. I started buying paper EE bonds in the 1970’s. I’ve carried them around with me in shoes boxes and bank safety boxes for decades. I setup a TD account and recently went through a complete conversion of the paper bonds to electronic format. Very happy with the results — website is easy to use, registration is easy, changes are easy, allows linkage to my bank, get the alerts for redemption status. Very easy to rollover the EE bonds into I bonds or into cash in one of my linked bank accounts. Much easier than manually tracking redemption and going to the bank with $2K – $3K of paper bonds every month to cash out.

Owner plus secondary, or a Trust is the best you can do for estate planning. You found a way to do beneficiaries or something else?

My plan, buy now and again in January to cover both options.

I like this strategy. As for the 2022 purchase, it will be almost impossible to pass up that 7.12% variable rate, which will be available for purchases through April 30. Even if you thought the fixed rate was rising to 0.2% in May, that 7.12% rate would cover 17 years of a fixed rate at 0.2%.

My plan is to buy $5K now and $5K again in November (ditto my wife), and then buy $5K in January and $5K in March or April, depending on the new April rate. If the April ’22 rate is higher than the November ’21 rate (7.12%), then I’ll wait ’til April; if it’s the same or less than 7.12% I’ll buy in March.

Although I have suggested buying all-out in October, I can’t argue with this strategy, except that the the 2022 strategy will involve buying in April or May, not March or April. So the key decision period in 2022 will be in mid-April, after the March inflation report is released. Still, I’m predicting that buying before May 1 will be very likely to be the better strategy. Can’t pass up that 7.12% return.

Mybad, April-May, not March-April. Thanks. But I’ll still make my decision then. If the new rate is higher than 7.12%, which I think is possible if not likely, then I’ll wait til May.

You do good work. Keep it up!!!

The key factor in mid-April will be if the fixed rate could possibly rise above 0.0%. Otherwise, if you buy in April you will get the 7.12% annualized for six months, and then the new rate for six months. So you will always get the next rate if you buy in April. But the fixed rate is permanent.

Hi Ron,

Here’s the argument for buying ibonds in October. What I thought was that if I bought in October that I would get 1 month of 3.5 then six months of 7.12 but it’s actually a full six months of 3.5. I agree with the analysis in the article below and I will be buying before the end of October.

[https://tipswatch.files.wordpress.com/2021/10/scenarios-1.jpg]

I Bond dilemma: Buy in October? Or wait until November?

My opinion: Long-term investors should buy in October. Short-term term investors could wait until November. But whatever … buy I Bonds in 2021. By David Enna, Tipswatch.com With the release o…

tipswatch.com

Tom Brady, Instructor

Business Technology Division

Trident Technical College

Charleston, SC 29406

________________________________

I don’t know why I bonds are not talked about as much as all the other investment stuff out there. Every time I read up on the financial blogs i follow nobody talks about Treasury products. If Robert Kessler likes Treasury bonds that’s good enough for me. At 7% im going to be happy buying more I bonds in November.