By David Enna, Tipswatch.com

This time, the economists just about got it right.

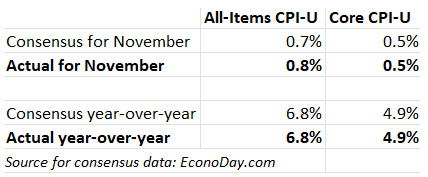

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.8% in November on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 6.8%, the largest 12-month increase in more than 39 years, since the period ending June 1982.

Those numbers came close to matching the consensus forecasts of 0.7% for the month and 6.8% for the year, so these increases shouldn’t surprise the stock and bond markets. (S&P 500 futures are up nicely in premarket trading this morning.) In recent months, economists have been woefully underestimating U.S. inflation. I think they’ve gotten the memo: Inflation is here, with a vengeance.

Core inflation, which strips out food and energy, came in at 0.5% for the month and 4.9% for the year, matching consensus estimates. That annual rate is the highest for core since 1991.

The BLS noted that the November surge in inflation was due to broad price increases across the economy, with the indexes for gasoline, shelter, food, used cars and trucks, and new vehicles among the larger contributors. For example:

- Gasoline prices were up a strong 6.1% for the month, and are now up 58.1% over the last year.

- The costs of food at home rose a painful 0.8% in November, after rising 1.0% in October and 1.2% in September. The BLS said prices increased in all six major grocery store indexes. Overall, food costs increased 6.1% over the last year.

- Prices for used cars and trucks increased 2.5% for the month, matching the October increase, and are now up 31.4% over the last year. Prices for new vehicles were up 1.1% for the month.

- Shelter costs rose 0.5% for the month, and are up 3.8% over the last year.

- Apparel costs rose 1.3% in November, and are up 5.0% over the last year.

- The costs of medical care services increased 0.3% for the month and are up a moderate 2.1% for the year.

While gasoline is often a major factor in rising U.S. inflation, the November report demonstrates that prices are surging across most key areas of the U.S. economy: Food, shelter, transportation, clothing. Here is the 12-month trend for all-items and core inflation, showing the stunning surge higher beginning in March 2021:

Because of the relatively low annual inflation indexes for December 2020 to March 2021, it’s clear that official U.S. inflation could continue running “hot” well into 2022, before possibly moderating in the spring and summer months.

What this means for TIPS and I Bonds

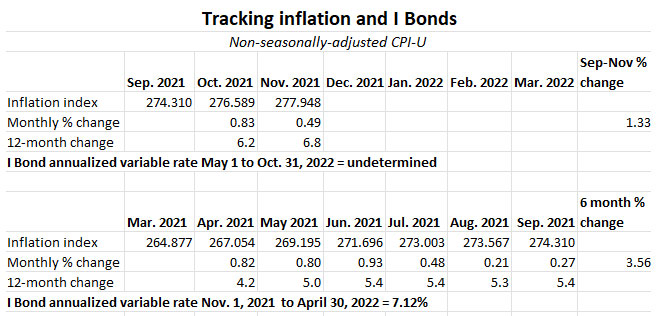

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For November, the BLS set the inflation index at 277.948, an increase of 0.49% over the previous month.

For TIPS. The November inflation report means that principal balances for all TIPS will increase 0.49% in January, following an increase of 0.83% in December. TIPS principal balances will be up 6.8% for the year ending in January. Here are the new January Inflation Indexes for all TIPS.

For I Bonds. November inflation was the second in a six-month string, from September 2021 to March 2022, that will determine the I Bond’s next inflation-adjusted variable rate, which will be reset May 1. Two months into this period, inflation has increased 1.33%, which would translate to a variable rate of 2.66%. Four months remain, and a lot can happen in four months.

Here are the numbers so far:

I Bonds currently offer a composite rate of 7.12%, annualized, for six months, and are on track to have another very attractive rate at the May 1 reset. If you haven’t bought a full allocation of I Bonds this year — $10,000 per person per calendar year — try to get that done by Dec. 31. The purchase cap will reset on January 1, allowing another $10,000 per person purchase.

What this means for future interest rates

There was a lot of talk this week on CNBC that the November inflation report could push U.S. inflation above 7.0%. That was classic “managing expectations.” Instead, inflation came in close to the consensus estimates, and even though 6.8% inflation is unsustainable, Wall Street can let out a sigh.

Because prices are increasing across a wide spectrum of the U.S. economy, and this trend looks likely to continue for several months, the Federal Reserve will continue be under pressure to “look like” it is working to control inflation. That will mean speeding up a reduction of its bond-buying quantitative easing, and eventually, increases in short-term interest rates.

Every month U.S. inflation continues to rise to 39-year highs, we get two months closer to increases in short-term interest rates. Could we see three rate increases in 2022, putting the federal funds rate to a somewhere above 0.75%? This seems highly possible, and reasonable.

Here are some thoughts from “Inflation Guy” Michael Ashton, posted this morning on Twitter:

So wrapping this up…what does this mean for the Fed? In the Old Days, the Fed by now would have already tightened a bunch. Currently, we’re talking about reducing the amount they add in liquidity, maybe a little faster. And possibly raising rates in 2022.

That is, UNLESS stocks drop like a stone. And honestly, it’s not really clear to me that the government would care to see much higher interest costs on the debt. Only way Japan has survived its mountain of debt is that is it almost interest-free, after all.

But maybe the hawks will storm the Eccles Building and the Fed will not only raise rates, but also slow money growth (these were once tightly connected; now not so much, and it’s the money growth part that matters not the interest rate part). We can hope.

More on I Bonds:

- I Bond Manifesto: Why inflation-linked savings bonds can work as part of your emergency fund

- Nov. 1 update: I Bond’s fixed rate holds at 0.0%; composite rate soars to 7.12%

- I Bond podcast: U.S. Savings Bonds for a risk-free, stellar return

- I Bonds vs. TIPS: What’s the best bet for inflation protection?

- Seeking Yield And Safety? The Best Choice Is U.S. Savings Bonds

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…