Overall U.S. inflation ran slightly higher than expected in September

By David Enna, Tipswatch.com

The inflation news this morning is historic. So let’s get right to it.

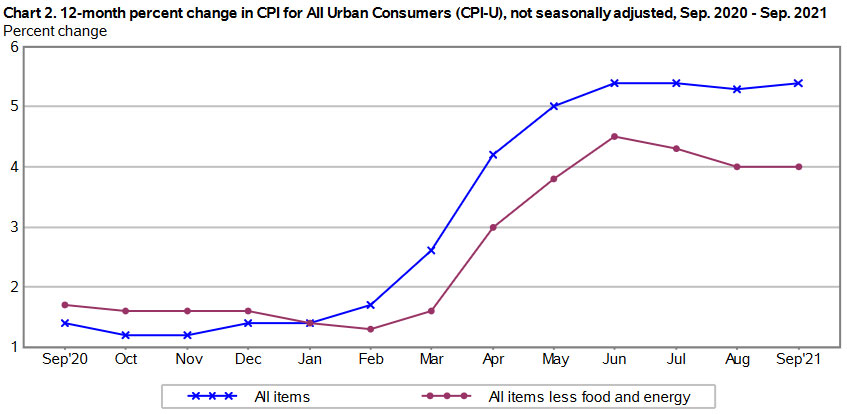

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4% in September on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 5.4% before seasonal adjustment. Both of those numbers were slightly higher than the consensus forecasts.

Core inflation, which removes food and energy, matched the forecasts of 0.2% for the month and 4.0% for the year.

The September report was particularly brutal for middle-income consumers. Food costs rose a sharp 0.9% in September and are now up 4.6% over the last 12 months. The index for meats, poultry, fish, and eggs rose 2.2% over the month as the index for beef rose 4.8%.

Shelter costs rose 0.4% and are up 3.2% year over year. The BLS said food and shelter costs contributed more than half of the overall increase in the all-items index. Gasoline prices, however, were also up 1.2% for the month, and up 42.1% year over year. Natural gas prices increased 2.7%.

Some areas saw declining prices. Airline fares were down 6.4% in the month, after falling 9.1% in August. Apparel costs dropped 1.1%. The index for used cars and trucks fell 0.7%, continuing to decline after it decreased 1.5% in August. But used vehicle costs remain 24.4% higher than a year ago.

Here is the 12-month trend in all-items and core inflation, showing that the steep increases in inflation are now leveling off at historically high levels.:

What this means for I Bonds and TIPS

Investors in U.S. Series I Savings Bonds and Treasury Inflation-Protected Securities are also interested in non-seasonally adjusted inflation, which is used to set future interest rates for I Bonds and adjust principal balances for TIPS. For September, the BLS set the CPI-U inflation index at 274.310, an increase of 0.27% over the August number.

For I Bonds. The September inflation report was the last of six that will determine the November 1 reset of the I Bond’s inflation-adjusted rate, which is combined with a fixed rate to determine an I Bond’s composite interest rate for six months. Over the March to September period, inflation rose 3.56%, the largest six-month increase in the 23-year history of I Bonds. That increase means the inflation-adjusted rate will rise to 7.12%, annualized, for six months. That is up from 3.54% currently.

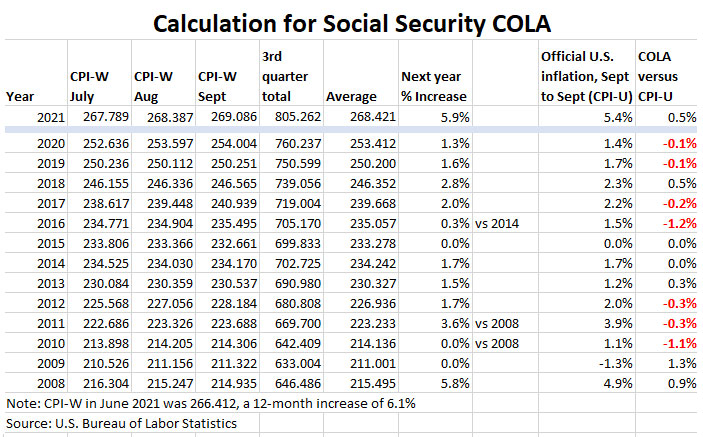

Here are the numbers used in this calculation:

The I Bond’s fixed rate — which is currently 0.0% — will also be reset on November 1, but I think it is highly likely to remain at 0.0%, which means the new composite rate will be 7.12%.

All holders of I Bonds will receive this 7.12% annualized rate for six months, but the start date of the higher rate will depend on when the I Bond was purchased. If you buy an I Bond before November 1, you will receive 3.54% for six months, and then 7.12% for six months, beginning in April. That totals out to an annual yield of about 5.33%.

Here is how the higher rate will be rolled out for I Bond investors, from TreasuryDirect:

| Issue month of your bond | New rates take effect |

|---|---|

| January | January 1 and July 1 |

| February | February 1 and August 1 |

| March | March 1 and September 1 |

| April | April 1 and October 1 |

| May | May 1 and November 1 |

| June | June 1 and December 1 |

| July | July 1 and January 1 |

| August | August 1 and February 1 |

| September | September 1 and March 1 |

| October | October 1 and April 1 |

| November | November 1 and May 1 |

| December | December 1 and June 1 |

So now the question arises: If you haven’t bought I Bonds up to the limit in 2021 (there is a purchase cap of $10,000 per person per year) should you buy before November 1, or after November 1? I will be writing more about this soon, but right now I still recommend buying in October to lock down that 5.33% annual return.

Want to know more about I Bonds? Read this: I Bond Manifesto: Why inflation-linked savings bonds can work as part of your emergency fund

For TIPS. The September inflation report means that principal balances for all TIPS will increase 0.27% in November, after an increase of 0.21% in October. TIPS principal balances have increased 5.4% over the last 12 months. Here are the new November Inflation Indexes for all TIPS.

What this means for the Social Security COLA

The September inflation report was the third of three — for July to September — that will set the Social Security Administration’s cost of living adjustment for 2022. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For September, the BLS set CPI-W at 269.086, which produced a three-month average of 268.421, an increase of 5.9% over the same average for 2020. That means the Social Security COLA will be 5.9% for payments beginning in January. That increase (for a change) actually outstrips overall U.S. inflation, which has increased 5.4% over the last year.

This will be the highest Social Security COLA increase in 39 years, since the 7.2% adjustment for payments in 1983.

The Social Security Administration says the average monthly benefit for U.S. retirees is $1.543, so a 5.9% increase will raise that monthly benefit to $1,634. If you are in the Social Security “limbo” period — older than 62 but not yet taking benefits — your future benefits would also climb by this percentage.

However, recipients can also expect that Medicare Part B costs will rise in 2022, which will subtract — at least partly — from the higher benefits. The base premium is now $148.50 a month. I could see that rising to $158 a month, cutting the effect of the COLA increase by $9.50 a month. But this is just speculation.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: October 2021 Better of the Internet - Bonisa

Pingback: October 2021 Best of the Web

Question… Would I bonds be redeemable durning a Government Shutdown ?

Possibly not, but I would expect that all accrued interest would continue growing. I Bonds aren’t traded on any market, so redemptions could be limited (very temporarily) without much disruption. But I don’t think that will happen.

No risk I Bonds at 7.12%, annualized.

>

Thank you for the article. Those are solid numbers and welcomed. I already read an article implying this huge payout might shorten SS funding by one year. TBD.

If the government is unable to service debt at low interest levels should we be concerned how long they would be willing to pay high variable I-bond rates if inflation is not transitory?

I think the fear that Social Security benefits will be cut by 20% in the future (around 2033 or 2034) is legitimate, because that is currently the law if nothing is done about future funding. I do believe, though, that the U.S. has no choice but to pay its Treasury obligations, especially savings bonds.

It certainly seems more probable as time goes on and no action is taken. Perhaps mean testing such as is done with IIRMA is a possibility. The more you make the more SS is reduced.

Would make for interesting spreadsheet work to compare taking early versus delayed SS payments if a reduction were to occur. Does it blow a hole in the argument of waiting to take SS to come out ahead over time? A bird in the hand being more valuable than two in the bush?

“Does it blow a hole in the argument of waiting to take SS to come out ahead over time? A bird in the hand being more valuable than two in the bush?”

Read the 7-point Comment at the bottom of this article. Some interesting food for thought.

“This Decision Could Increase Your Social Security Benefit by 8% Each Year”

https://clark.com/personal-finance-credit/investing-retirement/delay-social-security-benefit/#disqus_thread

I think the political pressure against cutting benefits will be so strong that a solution will be found, probably raising the taxable limit, possibly raising future retirement ages, etc.

Hi, Kevin.

There’s no arguing with the math behind that story provided one lives longer than age 78 or so. I can recall reading articles saying that’s the approximate crossover age between early takers and maximum age.

I do believe there will be last minute decisions to maintain a semblance of solvency but I’m also realistic after watching so many years of kicking the can down the road behavior by our leadership that it may come later rather than sooner.

What I was inferring was more along the lines of this scenario;

(1) A person, aged 62, starts SS now rather than waiting until the maximum age.

(2) In 10-12 years a 20%- ?% reduction is imposed on SS benefits for all recipients…remember this is just a hypothetical scenario and not something I suspect will happen only something that is suggested by funding into the early 2030’s as we know them.

Should (2) happen, will the person who did wait until the maximum age really gain a financial edge by age 78 given (2) above?

I haven’t run the math but suspect it would take a few more years for the net benefit to be achieved. This may imply that the benefit of waiting may not be reached until one is in their early 80’s instead of 78.

Great article:

Thank you posting the info 1st thing this morning…

** No Brainer **

Over the March to September period, inflation rose 3.56%, the largest six-month increase in the 23-year history of I Bonds. That increase means the inflation-adjusted rate will rise to 7.12%, annualized, for six months. That is up from 3.54% currently.

The I Bond’s fixed rate — which is currently 0.0% — will also be reset on November 1, but I think it is highly likely to remain at 0.0%, which means the new composite rate will be 7.12%.

All holders of I Bonds will receive this 7.12% annualized rate for six months, but the start date of the higher rate will depend on when the I Bond was purchased. If you buy an I Bond before November 1, you will receive 3.54% for six months, and then 7.12% for six months, beginning in April. That totals out to an annual yield of about 5.33%.

I new new to your blog, it seems very helpful. You mentioned that if you are in the Social Security “limbo” period — older than 62 but not yet taking benefits — your future benefits would also climb by this percentage. I was wondering if you are under 62 and not yet eligible for Social Security, will your future benefits also climb by this percentage?

Short answer: No. SS benefits rise and fall with the Average Wage Index prior to age 6o. After they follow the CPI.

Thanks for the answer. I didn’t know the exact procedures for under age 62.

what social security giveth, medicare taketh away.

The new semiannual rate (3.56%) surpasses the previous annualized rate (3.54%)!

WOW!!!