By David Enna, Tipswatch.com

This is a great time to be a holder of Treasury Inflation-Protected Securities, because probably all of your longer-term holdings are more valuable today than when you purchased them. The TIP ETF, which holds the full range of maturities, had a total return of 8.4% in 2019 and then 10.8% in 2020.

That’s the good news. The bad news is that it’s not a great time to be a buyer of TIPS. Real yields — your returns against inflation — have plummeted in 2021 and once again the full range of TIPS offerings, including the 30-year, have a real yields negative to inflation.

Of course, this is the world of safe fixed-income investing in May 2021. All safe investments, including nominal Treasurys, bank CDs and TIPS, are highly likely to under-perform official U.S. inflation into the future. The only exceptions are U.S. Savings Bonds: The I Bond will have a return matching official inflation, and the EE Bond will return 3.5% if held for 20 years, and has a good shot at beating future inflation. (Compare that with the 20-year Treasury, yielding 2.25%.)

Into this environment comes Thursday’s reopening auction of CUSIP 91282CBF7, creating a 9-year, 8-month TIPS. This is its second and final reopening auction.

- CUSIP 91282CBF7 was created at auction on Jan. 21, 2021, and generated a real yield to maturity of -0.987%, the lowest ever for any TIPS auction of this term. The coupon rate was set at 0.125%, and investors paid a premium price of about $111.64 for about $100.01 of par value plus accrued interest.

- It was then reopened on March 18, 2021, with a more-favorable real yield to maturity of -0.580%. The price dropped to about $107.62 for about $100.73 of value, after accrued inflation and interest was added in.

CUSIP 91282CBF7 is currently trading on the secondary market, and you can track its real yield and price on Bloomberg’s Current Yields page. As of Friday’s close it was trading with a real yield of -0.92% and a price of about $110.58. So at this point the real yield still remains a bit higher than January’s record low.

This TIPS will carry an inflation index of 1.01660 on the settlement date of May 28. That’s going to raise its adjusted price by 1.66%, but investors will get a matching amount of additional principal.

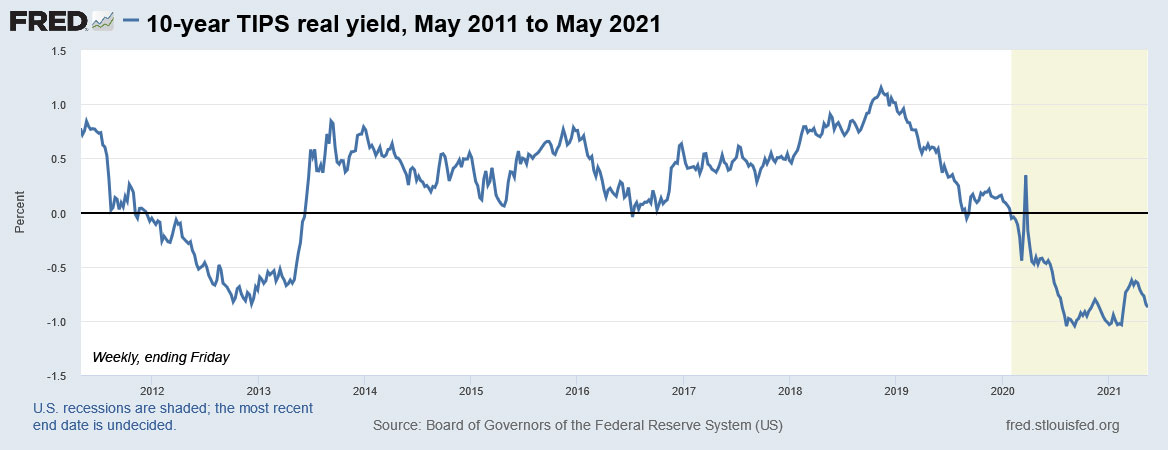

Here is a look at the trend in 10-year real yields over the last decade, a period of extremely low interest rates and relatively mild inflation:

For much of the time over the last decade, the 10-year real yield has been above zero and often in a range near 0.50%. The two exceptions are times of aggressive quantitative easing by the Federal Reserve, first from 2011 to mid 2014, and again from 2020 to today. Real yields are likely to remain well below zero at least until the Fed “hints” it will taper its bond-buying programs and eventually — after much signaling — begin raising short-term interest rates.

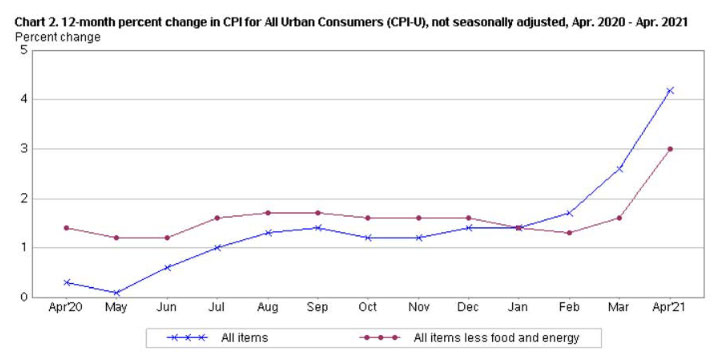

In the meantime, the Fed has stated it will accept “average” U.S. inflation of higher than 2%. So even though U.S. inflation is currently running at 4.2%, the Fed will ignore that until average inflation — maybe over 18 months? — rises “above 2%,” implying that 2.5% will be acceptable. The market’s reaction has been to force real yields lower, even as nominal yields were increasing. Because TIPS offer inflation protection, they are a more appealing investment under this Fed policy, so they are being bid up, forcing yields lower.

Here is a comparison of the nominal yield of a 10-year Treasury note versus the real yield of a 10-year TIPS over the last decade:

The key point is to note that while the two yields tend to rise and fall together, after February 2020 they have sharply diverted, with the nominal yield rising while the real yield is falling. And that brings us to …

10-year inflation breakeven rate

A nominal 10-year Treasury is currently trading at 1.63%, and if this reopened TIPS gets a real yield of -0.92%, it will have an inflation breakeven rate of 2.55%, which would be higher than any auction result since 2016 (when I started tracking this measure). In essence, it means that inflation will have to average more than 2.55% over the next 9 years, 8 months, for this TIPS to out-perform a nominal Treasury.

I think there will be plenty of investors willing to bet that inflation will run higher than 2.55% over the next decade, and so demand for this offering should be strong, at least versus a nominal 10-year Treasury.

Here’s a look at the trend for the 10-year inflation breakeven rate over the last decade, showing the rather mind-boggling surge higher once the Federal Reserve and Congress went into “stimulus” mode in March 2020:

When you compare a TIPS to a nominal Treasury, a TIPS is more attractive as the inflation breakeven rate declines, and less attractive as the inflation breakeven rate rises. Check out my “TIPS Vs. Nominals” page for more on that.

Conclusion

Once again, my personal investment decision is to sit out this auction, with the real yield likely to be close to a record low, the breakeven rate historically high, and the investment requiring a lofty premium price over par. At some point, nominal and real yields will climb higher, and more attractive options — eventually — will be available.

For the first $10,000 you invest in inflation protection, go with Series I Savings Bonds, which have a purchase cap of $10,000 per person per year. Right now an I Bond has 92-basis-point advantage over this TIPS, while providing tax-deferred interest and better inflation protection.

If you are interested in this auction, keep an eye on Bloomberg’s Current Yields page up to the morning of the auction, which closes to non-competitive bids at noon EDT. The 10-year TIPS listed there is CUSIP 91282CBF7, and it should be an accurate predictor of your likely yield and cost. But just be aware that an auction event can sometimes skew the yield higher or lower. As I noted, I think demand could be fairly strong for this TIPS from big-money investors.

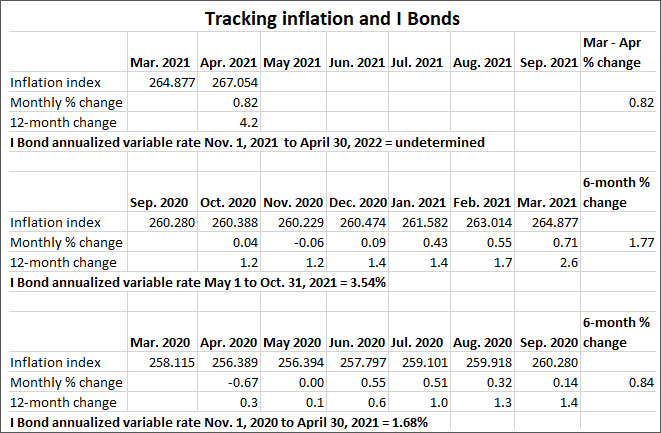

One positive factor: April’s non-seasonally adjusted inflation rate of 0.82% is going to give an immediate boost to this TIPS’ principal balance in June, up 0.82%. And adjustments in the next few months after that could also be fairly high.

I will be posting the auction results soon after the official close at 1 p.m. EDT Thursday. Here is a history of recent 9- to 10-year TIPS auctions, showing the string of negative real yields that began in May 2020:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It would be my pleasure to accommodate you However, the URL for 20 year TIPS at CNBC pulls up no…