For several years, I’ve been tracking the performance of TIPS investments versus nominal Treasurys of the same term. Over the last decade, TIPS have been fairly lousy investments when compared to their nominal counterparts. That’s what happens when inflation runs at surprisingly low levels for years.

On April 15, 2021, a five-year TIPS matured. This was CUSIP 912828Q60, created at auction on April 21, 2016. In my preview article for that auction, I noted that the yield to maturity was likely to be negative to inflation, and down 68 basis points from a similar auction in December 2015. The auction a few days later ended up with a real yield to maturity of -0.195%.

So, with its negative yield to inflation, this was a lousy investment, right?

Wrong. It ended up outperforming a 5-year Treasury note, which at the time had a nominal yield of 1.35%. That created an inflation breakeven rate of 1.54%, pretty attractive. In actuality, inflation ended up averaging 2.1% over the next five years, giving this TIPS a 0.56% annual advantage over the nominal 5-year Treasury.

Understand that this is a rough estimate of performance, and it is based on inflation data starting two months before the month of TIPS issue. Inflation accruals for TIPS each month are based on inflation data from two months earlier. (That means the big jumps in inflation in March and April 2021 are not reflected in this data.)

Also, keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

Nevertheless, it is clear that CUSIP 912828Q60 ended up being a winner when compared to a 5-year nominal Treasury, because inflation ended up running higher than its rather low inflation breakeven rate.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Memo to inflation predictors: You are going to need some new formulas.

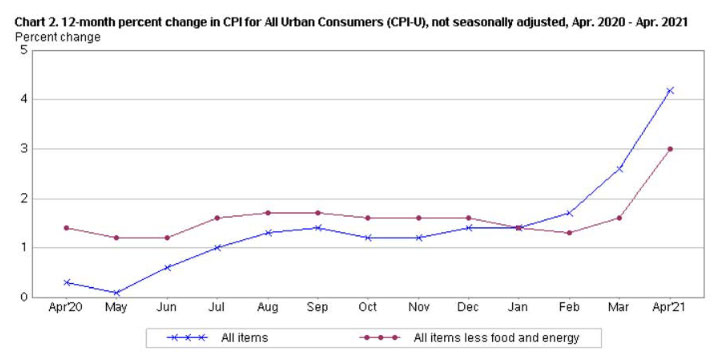

The Consumer Price Index for All Urban Consumers increased 0.8% in April on a seasonally adjusted basis after rising 0.6% in March, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 4.2%, the largest 12-month increase since a 4.9% increase in September 2008.

This result was four times the consensus estimate of 0.2% for April inflation, and the year-over-year number was also much higher than the estimate of 3.6%. Core inflation, which removes food and energy, was equally shocking: 0.9% for the month, versus an estimate of 0.3%, and 3.0% for the year, versus an estimate of 2.3%.

Clearly, economists have no way to predict U.S. inflation accurately in mid 2021, after 13 months of massive Federal Reserve and Congressional stimulus measures. And this came in a month when gasoline prices — usually a key trigger of monthly inflation — actually fell!

Here are some highlights from the BLS report:

The index for used cars and trucks rose 10.0% in April, the largest monthly increase in that category since this inflation series began in 1953. Used vehicle prices are up a massive 21% over the last 12 months.

Food prices rose 0.4% for the month and are up 2.4% year over year.

Gasoline prices fell 1.4% in April after rising 9.1% in March, but remain 47.6% higher year over year.

The shelter index rose 0.4% in April, and is up 2.1% over the year.

The index for airline fares also rose sharply in April, increasing 10.2%.

Costs of car and truck rentals rose 16.2%.

The costs of medical care services remained flat in April, and are up 2.2% year over year.

My takeaway from the April report is that inflation is surging across the entire economy, at a rate much higher than economists expected. And that happened even though gas prices were down for the month. Gasoline prices have already risen sharply in May, partially triggered by the East Coast pipeline shutdown.

Here is the trend over the last 12 months for both all-items and core inflation, showing the relatively moderate trend during the heart of the COVID-19 pandemic, but surging once the nation began reopening earlier this year:

What this means for TIPS and I Bonds

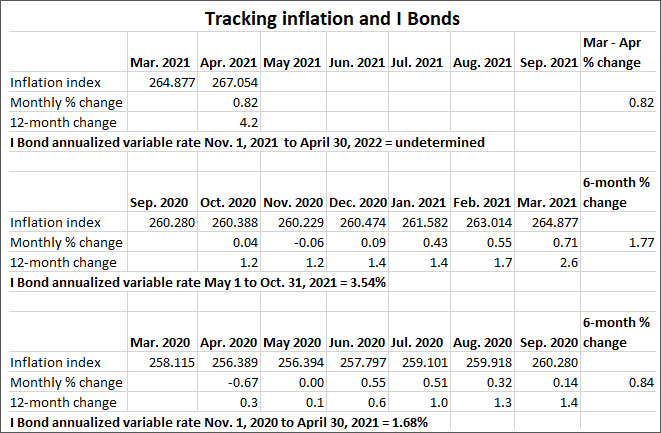

Investors in Treasury-Inflation Protected Securities and U.S. Series I Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For April, the BLS set the inflation index at 267.054, an increase of 0.82% over the March number.

For TIPS. Today’s inflation report means that principal balances for all TIPS will increase by 0.82% in June, following increases of 0.55% in April and 0.71% in May. That’s a remarkable 2.07% increase in three months, and a nice demonstration of why it’s smart to have some inflation protection in your asset allocation. Here are the new June Inflation Indexes for all TIPS.

For I Bonds. Today’s report is the first of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset in November. It’s too early to draw any conclusions, and remember that today’s report shows just how difficult inflation is to predict.

Here are the numbers:

What this means for future interest rates

The Federal Reserve has been predicting a “transitory” increase in inflation, caused partially by comparisons to the weak price trend during the early months of the COVID-19 pandemic. Note in the chart above that non-seasonally adjusted prices fell 0.67% in April 2020, followed by zero inflation in May 2020. In addition, the nation is facing some supply shortages in key items like lumber and computer chips.

The stock market isn’t reacting well to today’s news, with the S&P 500 index down nearly 1% this morning. The 10-year Treasury yield has bounced back to about 1.67%, up about 9 basis points over the last week.

But will this surge in inflation continue? From today’s Wall Street Journal report:

“I think a lot of us are expecting a pretty significant increase of spending on services in the next couple months and that’s where a lot of the pressure on CPI is going to come from,” said Richard F. Moody, chief economist at Regions Financial Corp. “It’s a question of how long that burst in spending persists. And the longer it persists, the more latitude producers have to raise prices.” …

A persistent, significant increase in inflation could prompt the central bank to tighten its easy-money policies earlier than it had planned, or to react more aggressively later, to achieve its 2% inflation goal.

Because of the weak inflation numbers in May 2020, it’s likely that core inflation will again be 3.0% or higher in the May 2021 report, well above the Fed’s stated target of “above 2.0%.” The Fed tracks a different inflation index, the Personal Consumption Expenditures index, which was 2.3% in March (the April number has not yet been released).

The Fed, however, believes this inflationary trend will be temporary, with price increases probably settling in around 2.5% by the end of the year. A few more months of the outsized inflation of March and April may force them to change their view.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I know most of my readers are experienced investors who already have a TreasuryDirect account. If you know a less-experienced investor who could use this information, please pass it along. Thanks …

By David Enna, Tipswatch.com

The news that U.S. Series I Savings Bonds are now paying 3.54%, annualized, for six months is drawing a lot of attention from new investors, people who a few months ago would have laughed off any talk of investing in savings bonds.

This is good. I love when people learn about I Bonds and EE Bonds and appreciate them as valuable and viable investments. Yes, they are “relics” from the past, but that relic status is what makes them so attractive: They have terms that create a flow of interest income much higher than you’d find with any other “modern” safe investment.

But then there is the obvious question: How do you invest in I Bonds? You could ask your broker, but don’t expect any help there. Your broker can’t sell you I Bonds, and can’t make money from advising you to buy them. You can’t buy them on the “open market.” There is only one place to purchase I Bonds, and that is the U.S. government’s site, TreasuryDirect.gov.

What do you need to open an account?

An image from the TreasuryDirect site. Five minutes? Possibly wishful thinking.

A taxpayer identification number … in other words, a Social Security Number.

A United States address of record. Do you need to be a U.S. citizen? No. Do you need to be living in the U.S.? No. But you need a U.S. address to register the account.

Be at least 18 years old. A child cannot open a TreasuryDirect account. But a parent or other adult guardian can open an account for a child and link it to the adult’s account.

A checking or savings account … this can be at a physical or online bank, or at brokerage, such as Fidelity or Vanguard. You will need to know your account and routing numbers.

An email address.

A web browser that supports 128-bit encryption. TreasuryDirect states that its site is “optimized for Internet Explorer,” which is classic government dumbness. IE has been replaced by Microsoft Edge and today has a market share of less than 1%. TreasuryDirect even provides “helpful” links to Windows XP service packs that have long-ago been discontinued. TreasuryDirect works fine with Firefox and Chrome browsers. I have tested it with Edge and Safari, too, and it seems to work fine.

When you get to the “Account Type” page, choose “Individual.” (You can also open an account in the name of a trust, but I have no idea how that works.)

A married couple must open two separate TreasuryDirect accounts if both spouses wish to purchase I Bonds. Each account is limited to purchasing $10,000 per person per calendar year, so if you want to purchase $20,000 in a year, you need two accounts.

(There are separate purchase caps for I Bonds and EE Bonds, so an individual can buy $10,000 of both, for a total of $20,000. EE Bonds, by the way, are also an excellent 20-year investment in today’s market. I wrote about that in September 2019.)

Once you get to TreasuryDirect’s “Individual Account Application” page, you’ll need to fill in a lot of personal information — see why you need that 128-bit encryption? — including your Social Security number, date of birth, state driver’s license number and expiration date, mailing address, email address, and bank information.

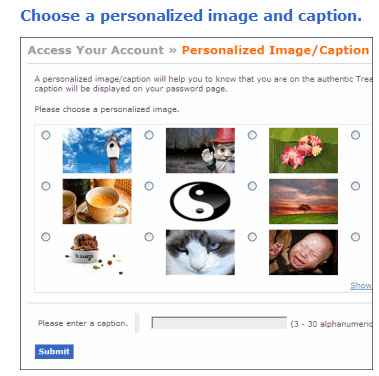

Then, TreasuryDirect will ask you to select a “personalized image and caption.” What’s this about? It is a safeguard against phishing attempts. If a scammer tries to get you to log into your TreasuryDirect account using a false address, you won’t see this image and caption. That’s a signal you are being scammed.

Next, you will choose your password. TreasuryDirect advises, “When selecting your password, avoid numbers, names and dates” that correspond to your personal information. I suggest creating a password that is UNIQUE to TreasuryDirect and not used elsewhere.

You’ll also be asked to answer three security questions, in case you forget your unique password. Favorite author? Favorite movie? And so on.

And that is it, on the last page of the account creation screens, you will be given your new account number (usually something like X-123-456-789). When you go to log later, you will be asked to provide your account number and password. As an additional security measure, you will be emailed a temporary security code to enter before you gain access to your account.

Registering your purchases

How you register a savings bond determines who owns the bond and who can cash it. The registration also determines what happens with the bond if the owner dies.

One owner. Only one person is named as owner. Only that person can make transactions. If he or she dies, the bond becomes part of the estate.

Owner and beneficiary. Only the owner can make transactions. If he or she dies, the beneficiary becomes the only owner. The beneficiary can’t be an entity. The registration says “PAYABLE ON DEATH,” or “POD.” Example of registration: JOHN DOE POD TO JANE DOE

Two owners. For electronic bonds (the only option when buying through TreasuryDirect), the first-named owner is the primary owner; the second is secondary. The registration uses “WITH.” An example of this registration is JOHN DOE SSN 987-65-4321 WITH JANE DOE SSN 123-45-6789. If one owner dies, the other becomes sole owner. If one owner is a person, the other can’t be an entity like a trust.

These ownership rules throw a lot of investors for a loop, because they expect to see “Joint Ownership With Right of Survivorship” as an option. How is “with” ownership different from “joint ownership”? I don’t know, but for a married couple, I’d recommend using this “with” ownership, which should avoid issues after the primary owner’s death.

Using I Bonds for higher education

If you use interest from a Series I bond to pay for higher education, you may not have to pay federal tax on the interest. However:

If you want to use the bond for your education, you must be the owner of the bond.

If you want to use the bond for your child’s education, then you or your spouse, or both, must own the bond. Your child may be a beneficiary but not a co-owner.

Your modified adjusted gross income has to be less than the cut-off amount set by the Internal Revenue Service. This amount typically changes every year. I believe the current caps are $84,950 for single taxpayers and $134,900 for married filing jointly, but a gradual phaseout of the benefit begins at lower income levels. See IRS Publication 970 “Tax Benefits for Education.”

Logging in for the first time

When you first log in, you will enter your account number (it looks something like X-123-456-789) and then you will get a notice that you must go to your connected email account for a one-time security code. Copy and paste that code into the box, submit, and you will come to the password entry page.

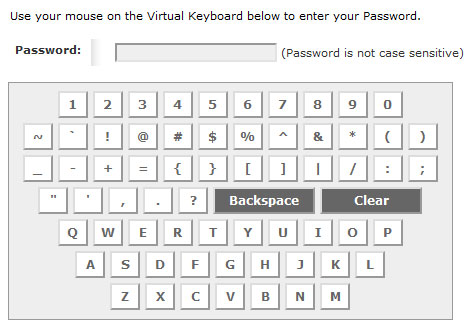

This is another security step. You enter your password using a virtual keyboard (it ignores upper and lower case). This security measure will keep keystroke-tracking viruses from learning your password. But you can see why you don’t want a 23-letter-long password. Keep it unique, and reasonable.

Here are the Treasury’s official password rules:

Length. Use at least eight characters without spaces.

Characters. Use at least one letter, one number, and one special character such as $ or %, but excluding “\”.

Content. Avoid numbers, names, or dates that are significant to you. For example, your phone number, first name or date of birth. Try to choose a password based on a memory aid.

On this page, above the keyboard, you will also see the image and caption you selected in the registration pages.

Making your first purchase

After you complete the login process, you will see your account summary page, which should be pretty empty if this is your first purchase. Up in the top row of links, click on “BuyDirect” and you will go to the purchasing menu.

Select Series I

On the next page, your preferred registration should be filled in, such “Person1” or “Spouse1 WITH Spouse 2”

Enter the purchase amount, up to $10,000 per account per calendar year.

Select the source of funds, which should already be filled in once your link to your bank or brokerage is completed.

If you select a single purchase, you can select the date for the purchase to be completed. I recommend setting a date near the end of the month, but on a weekday. For example, for this month, I’d probably select May 27, a Thursday. (An I Bond purchased late in a month earns a full’s month’s interest.)

Submit.

At this point you should see a confirmation of your purchase, but since I’ve already purchased my 2021 allocation, I can’t complete the process to test it.

How do I track/sell my holdings?

TreasuryDirect isn’t really like a brokerage account where you can check the current value of your holdings on a simple “balances” page. When you go to the account summaries page, you will see a value listed, but it is actually the original value of the I Bonds you purchased. If you click on “Savings Bonds” on that list, you go to another page, where you can select “Series I Savings Bonds” and hit submit.

On the next page — titled “Current Holdings > Summary” — you can see a list of your holdings and the “issue date,” “interest rate” and “current value,” which reflects interest paid up to that point. If you click on an individual issue and “select,” you will see at the bottom a link to redeem that savings bond.

When you redeem, you can sell the full amount (including interest accrued), or a partial amount, and you designate the bank account that will receive the funds. TreasuryDirect says you should receive the money in two business days.

(Keep in mind that you must hold an I Bond for 12 months before redeeming, and if you redeem before 5 years you will forfeit the last three months of interest.)

The Treasury also provides a web-based Savings Bond Calculator that it says are for paper bonds only, but in actuality can be used to track and list the electronic version, too. Back in January 2018 I wrote a step-by-step guide to using this calculator. Hint: It’s clunky.

How secure is TreasuryDirect?

This is source of rather heated debates on the Bogleheads forums, because the Treasury makes no “stated” commitment to guarantee your account against hacking or theft. For that reason, some investors will not purchase any holdings in TreasuryDirect. And this debate has been going on for more than a decade.

While the Treasury seems to dodge the “security guarantee” question, I feel strongly that it would take responsibility for any errors/hacking that it caused. But if you fall for a clever phishing attack or have an evil relative, you could face losses. The system does send you email alerts for any account changes, such as in registrations or linked bank accounts, or even if the email address was changed.

The Treasury expects you to monitor your account and provide timely notice of any irregularities. I think the risk is extremely small, and I have not heard of anyone ever losing money through hacking or theft. The complex login system that TreasuryDirect uses, including the two-factor verification and virtual keyboard, add up to strong security.

As an added security feature, TreasuryDirect allows you to place a hold on your account. If you believe someone else has learned your account access information and you want to prevent unauthorized access, you can edit your Account Info in your primary account to place a Customer Hold. This action will prohibit all transactions associated with your primary and linked accounts. After you place your Customer Hold, you will not have access to your account until the hold is removed.

What happens at tax time?

Not much. TreasuryDirect doesn’t have a “user-friendly” attitude when it comes to tax documents. It may (or may not) send you an email reminder to log in and check your current documents. It will not physically mail you anything. When you locate your tax documents, you’ll find the format to be confusing and not-printer friendly.

Of course, with I Bonds, you won’t owe any federal taxes until you redeem a bond, and I Bond interest is exempt from state income taxes. So this isn’t a big deal for an I Bond investor. But if you redeem some bonds, you will have a tax obligation that year and you’ll need to track down the forms.

Conclusion

No one is going to extol TreasuryDirect for being “user friendly,” and some of the complexities arise because of the extra security steps it places in the way of logins. Can you open an account in 5 minutes? I’d bet against that. And there could be some time needed to verify your bank account before you can make a purchase.

If you have more questions, post them below. I might not be able to answer some of the more complex or legal issues, but possibly other readers have some experience in those areas.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Treasury also maintains EE Bond’s doubling period at 20 years

By David Enna, Tipwatch.com

The U.S. Treasury just announced the May to October 2021 terms for U.S. Series I Bonds and EE Bonds, and … as we expected, there were no surprises. Both of these Savings Bonds remain exceptional investments in our current low-interest-rate market.

I Bonds

Here are details from the Treasury’s announcement:

“The composite rate for Series I Savings Bonds is a combination of a fixed rate, which applies for the 30-year life of the bond, and the semiannual inflation rate. The 3.54% composite rate for I bonds bought from May 2021 through October 2021 applies for the first six months after the issue date. The composite rate combines a 0.00% fixed rate of return with the 3.54% annualized rate of inflation as measured by the Consumer Price Index for all Urban Consumers (CPI-U). The CPI-U increased from 260.280 in September 2020 to 264.877 in March 2021, a six-month change of 1.77%.”

Here is my translation:

An I Bond earns interest based on combining a fixed rate and a semi-annual inflation rate. The fixed rate – which will continue at 0.0% – will never change. So I Bonds purchased from May 3 to October 30 will carry a fixed rate of 0.0% through the 30-year potential life of the bond.

The inflation-adjusted rate (also called the variable rate) changes every six months to reflect the running rate of non-seasonally adjusted inflation. That rate is currently set at 3.54% annualized. It will update again on November 1, 2021, based on U.S. inflation from March to September 2021.

The combination of the fixed rate and inflation-adjusted rate creates the I Bonds’ composite interest rate, which was 1.68% but now rises to 3.54%. An I Bond bought today will earn 3.54% (annualized) for six months and then get a new composite rate every six months for its 30-year term.

It’s important to note, however, that all I Bonds — no matter when they were issued — will get that 3.54% inflation-adjusted rate for six months, on top of any existing fixed rate. So an I Bond purchased in April will receive 1.68% for six months, and then 3.54% for six months.

Here is the formula the Treasury used to determine the I Bond’s new composite rate:

The composite rate for I bonds issued from May 2021 through October 2021, is 3.54%

Here’s how we set that composite rate:

Fixed rate

0.00%

Semiannual inflation rate

1.77%

Composite rate = [fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

[0.0000 + (2 x 0.0177) + (0.0000 x 0.0177)]

Composite rate

[0.0000 + 0.0354 + 0.0000000]

Composite rate

0.0354000

Composite rate

0.0354

Composite rate

3.54%

None of this was a surprise, but the new terms do mean I Bonds become a very attractive investment, earning at least 1.77% over the next year, and probably much higher. That compares to 0.05% for a 1-year Treasury and maybe 0.60% for a best-in-nation 1-year bank CD. In other words, in a worst-case scenario I Bonds will return close to triple the earnings of the next-best very safe investment. The actual return will likely be much higher than 2% over the next 12 months.

(An I Bond has to be held one year before it can be redeemed, but an investor can purchase the I Bond near the end of a month and get full credit for the month. That means an I Bond can be, effectively, an 11-month investment. I Bonds redeemed from 1 to 5 years face a penalty of three months interest; after 5 years there is no penalty.)

The fixed rate of an I Bond is equivalent to the “real yield” of a Treasury Inflation-Protected Security. It tells you how much the I Bond will yield above the official U.S. inflation rate. Right now, an I Bond will exactly match U.S. inflation.

I track the correlation between the I Bonds’ fixed rate and the current real yields of 5-year and 10-year TIPS. In the past, a 10-year TIPS generally yields about 50-75 basis points higher than an I Bond. In our current market, the equation has swung wildly in favor of the I Bond, with the I Bond having a 171 basis-point advantage over a 5-year TIPS and an 76 basis-point advantage over a 10-year TIPS. Given these market conditions, there was no way the Treasury was going to raise the I Bond’s fixed rate.

Here are the fixed rate versus TIPS yields going back to 2008. As an interesting aside, notice that the 10-year TIPS yield has risen 6 basis points over the last year, while the 5-year TIPS yield has shot 50-basis-points lower.

I have noticed a lot of chatter recently about I Bonds on financial forums. I expect this to be a very popular investment in 2021. I Bonds carry a purchase limit of $10,000 per person per year, and must be purchased electronically at TreasuryDirect. Investors also have the option of receiving up to $5,000 in paper I Bonds in lieu of a federal tax refund. Learn more about I Bonds.

EE Bonds

Here are the Treasury’s terms announced Monday:

“Series EE bonds issued from May 2021 through October 2021 earn today’s announced rate of 0.10%. All Series EE bonds issued since May 2005 earn a fixed rate in the first 20 years after issue. At 20 years, the bonds will be worth at least two times their purchase price. The bonds will continue to earn interest at their original fixed rate for an additional 10 years unless new terms and conditions are announced before the final 10-year period begins.”

And here is my translation:

The EE Bonds’ fixed rate remains at 0.1%, where it has been since November 2015. Awful, right? (Check out your current money market savings rate, somewhere around 0.05%, or less.) But the EE Bonds’ fixed rate is irrelevant because…

An EE Bond held for 20 years immediately doubles in value, creating an investment with a compounded return of 3.5%, tax-deferred. So, if you invest $10,000 at age 40, you can collect $20,000 at age 60, with $10,000 of that total becoming taxable.

After the doubling in value at 20 years, the EE Bond reverts to earning 0.1% for another 10 years.

Retaining this 20-year doubling is a big deal. The Treasury has changed this holding period several times in the past, so there was a real possibility the terms could change in 2021, with the 20-year nominal Treasury currently yielding 2.19%, well below the EE Bond’s potential of 3.5%

What this means: You should only invest in EE Bonds if you are absolutely certain you can hold them for 20 years. They are an ideal “bridge” investment for someone around age 40, who can build an annual stream of income starting at age 60, potentially delaying Social Security benefits until age 70.

The EE Bond will also outperform an I Bond if inflation averages less than 3.5% a year over the next 20 years. I think that is a fairly strong possibility. For anyone with a secure 20-year timeline for investment, an EE Bond is extremely attractive.

A combination of I Bonds and EE Bonds also makes sense, providing both inflation protection and strong deflation protection. But EE Bonds only make sense for an investor committed to holding them for 20 years.

Any questions?

I will be writing more about I Bonds and EE Bonds in coming weeks, since interest will be high in these investments (and TIPS aren’t particularly attractive right now). If you have questions, let me know.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

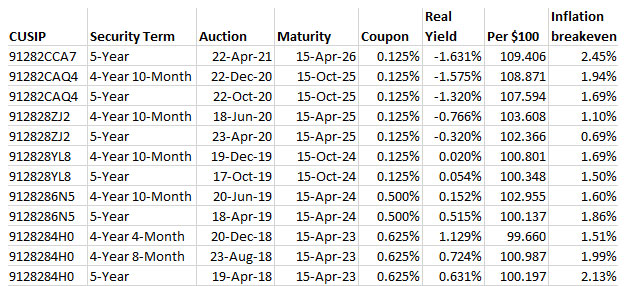

The Treasury’s offering of $18 billion in a new 5-year Treasury Inflation-Protected Security — CUSIP 91282CCA7 — auctioned today with a real yield to maturity of -1.631%, the lowest real yield at auction for any TIPS in history.

But here’s the surprise: The yield was a bit higher than expected, and it seemed to indicate lukewarm demand for this 5-year offering. The bid to cover ratio was 2.5, a decent number but well below recent auctions of this term.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

In this case, CUSIP 91282CCA7 got a coupon rate of 0.125%, the lowest the Treasury will allow for any TIPS. And that means investors had to pay a sizable premium to collect that 0.125% coupon for 5 years, plus future inflation accruals to principal. Investors paid an adjusted price of about $109.41 for about $100.32 of value, after accrued inflation and interest are added in. This TIPS will have an inflation index of 1.00273 on the settlement date of April 30.

The Treasury’s estimate of the real yield of a full-term 5-year TIPS ended Wednesday at -1.72%, about 9 basis points below today’s result. A four-year, 6-month TIPS is currently trading on the secondary market with a real yield of -1.87%, also much lower that today’s auction result.

Nevertheless, CUSIP 91282CCA7 got the lowest auctioned real yield for any TIPS in history, surpassing the -1.575% result generated by a 4-year, 10-month TIPS reopening on Dec. 22, 2020.

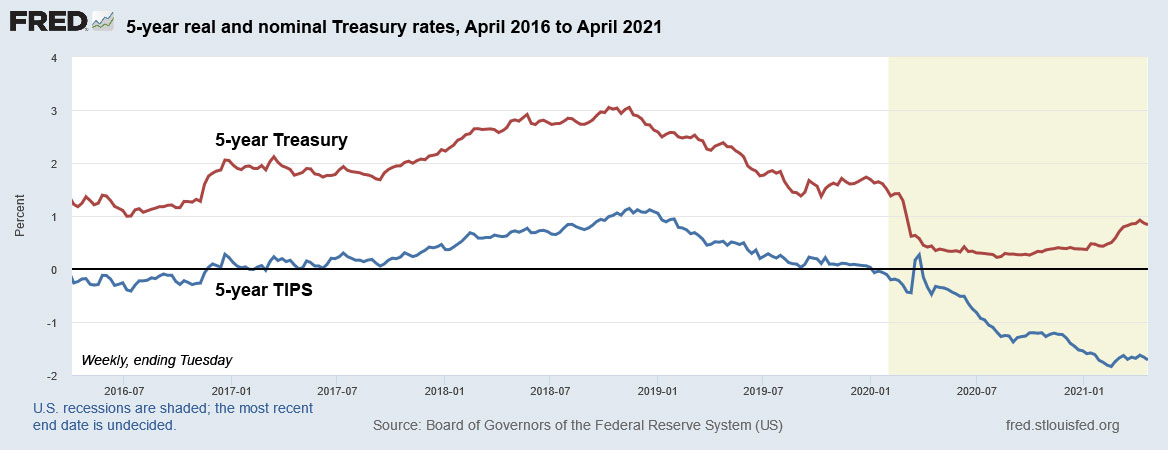

Here is the trend over the last five years for the real yield of a 5-year TIPS versus the nominal yield of the 5-year Treasury note, showing how the two yields have been moving in different directions in recent months, with the nominal Treasury yield moving higher and the real yield of a TIPS moving deeply below zero.

Negative real yields are not rare for TIPS, especially for the 5-year maturity. We’ve seen them often ever since the Federal Reserve began aggressive quantitative easing programs in 2011. But today offered a first: the lowest real yield for any TIPS of any maturity at auction.

Inflation breakeven rate

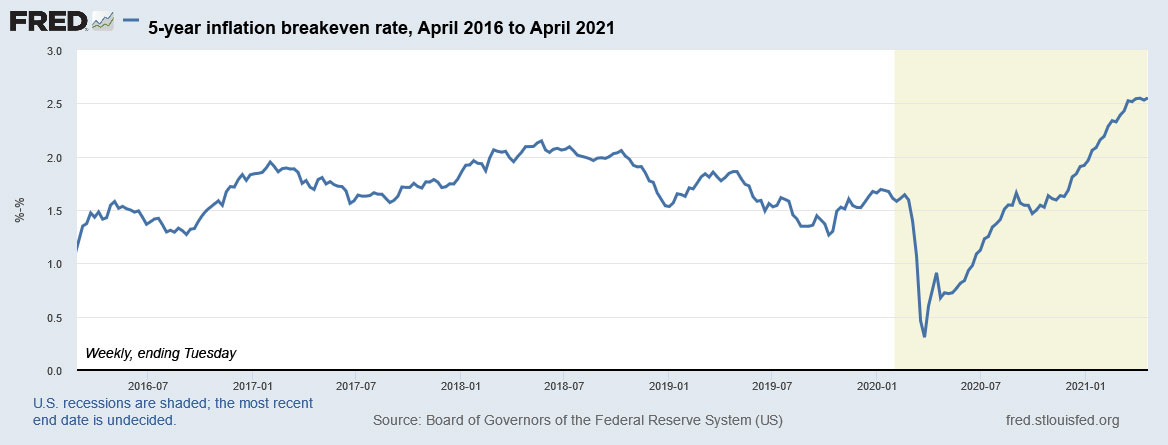

With a nominal 5-year Treasury trading at 0.82% at the auction close, this new TIPS gets an 5-year inflation breakeven rate of 2.45%, a bit below the number that looked likely as trading began today. But 2.45% is still higher than the result for any recent auction for any 4- to 5-year TIPS. In fact, since 2013, only two TIPS auctions of this term have generated a breakeven rate higher than 2.0%.

Here is the trend in the 5-year inflation breakeven rate over the last 5 years, showing the immense move higher since March 2020, when the Federal Reserve and U.S. Congress began aggressive programs to stimulate the U.S. economy, with the accepted side effect of driving inflation higher:

When the inflation breakeven rate rises, TIPS get more expensive versus a nominal Treasury. Before today’s auction closed at 1 p.m. EDT, a breakeven rate of as high as 2.7% looked possible. That might have sent some investors scurrying for cover.

Reaction to the auction

Based on the 4-year, 6-month TIPS trading on the secondary market with a real yield of -1.87%, I was expecting a real yield to maturity of -1.70% or lower for this TIPS. I can understand a shorter-term TIPS getting a lower real yield right now, because investors are pricing in higher inflation for the next year, but not necessarily for the longer term.

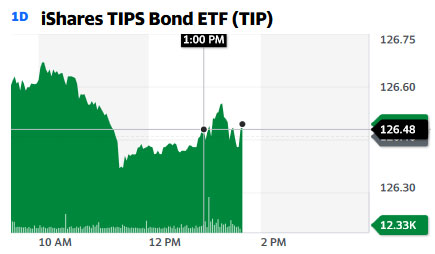

The TIP ETF — which holds the full range of maturities of TIPS — had been trading higher this morning, and seemed unbothered by the auction result, which closed at 1 p.m. EDT. This looks like the market saw the result … and yawned.

Investors at today’s auction should welcome the higher-than-expected real yield, even if it was a record low. And keep in mind that their holding will get a 0.71% boost in principal in May, reflecting non-seasonally adjusted inflation for March 2021.

This TIPS will be reopened at auction in June, and then the Treasury will offer a new 5-year TIPS in October. Here are auction results over the last three years:

It is true that I could have redeemed it when the rate was 1.9%, and maybe could have earned more…