By David Enna, Tipswatch.com

A couple years ago, just as my wife and I were both retiring, we went through a rigorous financial planning exercise with an hourly-fee adviser. We were in sync on almost all his advice, except when the adviser insisted: “You need to get these TIPS investments out of a taxable account and into an IRA.”

My response: “Not gonna happen.”

For nearly a decade, I had been writing about Treasury Inflation-Protected Securities and I Bonds, both inflation-protected investments. And with TIPS, my routine was to buy them at auction directly from Treasury Direct, and hold them to maturity. I’ve never sold a TIPS before maturity, and I wasn’t interested in moving them out of Treasury Direct and selling them to fund new purchases.

The adviser (the rather famous Allan Roth of Wealth Logic) was totally correct in his advice, which follows the tenets of of proper “asset location.” Taxable investment accounts, in general, should be focused on equity-oriented, low-cost index funds that generate little annual tax exposure, while traditional tax-deferred accounts should focus on interest-bearing bond funds, REITS, insured CDs, and possibly managed stock funds that generate taxable payouts.

Roth accounts, in this asset location theory, should be focused on longer-term equity investments, since this should be the last money you will withdraw in retirement. The longer investment horizon means you can take more risk.

Realistically, TIPS do work best in a traditional (non-Roth) tax-deferred account. That could mean investing in TIPS mutual funds or ETFs, or using a brokerage account to buy Treasurys with (hopefully) near-zero commissions. But while holding TIPS in a tax-deferred account is preferable, I say holding them as a taxable investment at Treasury Direct is also acceptable as part of your overall fixed-income asset allocation. Up to a point. More on that later.

TIPS and the ultra-scary ‘phantom income’

Treasury Direct isn’t user friendly. While every brokerage and investment firm on Earth mails you tax forms (or at least notifies you they are ready to download), Treasury Direct does nothing. You’ll get nothing in the mail, you won’t receive an e-mail alert. You are expected to remember to log in to the site and retrieve your tax forms:

- Form 1099-INT shows the sum of the semiannual interest payments made in a given year. This income is generated by the TIPS’ coupon rate, and is taxable at the federal level but tax-fee at the state.

- Form 1099-OID shows the amount the principal of your TIPS increased due to inflation or decreased due to deflation. Increases in principal are taxable for the year in which they occur, even if your TIPS hasn’t matured, so you haven’t yet received that payment of principal.

Form 1099-OID is a key to the conventional wisdom to invest in TIPS in tax-deferred accounts. You are paying tax on money you have not yet received. This is often called “phantom income,” and it sounds scary, doesn’t it? However, if you have a Total Bond Fund or GNMA Fund in a taxable account and reinvest the dividends, or have a 5-year CD at a bank and are reinvesting interest, you are doing exactly the same thing. You are paying tax on money you have not yet received.

(Read this for a scholarly treatise, including incomprehensible formulas, debunking the conventional wisdom about holding TIPS in a taxable account.)

What’s the cash flow?

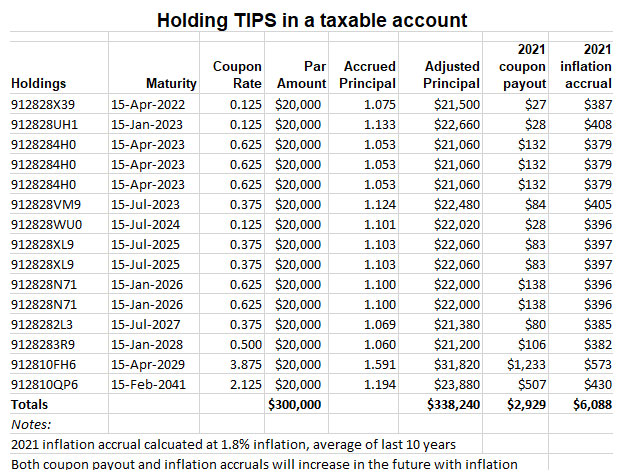

A common strategy for investments in TIPS is to build a ladder of inflation-protected investments that will stretch into your retirement, with issues maturing each year, which can then provide the money for re-investments or spendable cash. Let’s take a look at a theoretical TIPS ladder, with issues maturing every year through 2029, and then one longer-term TIPS maturing in 2041. It would look something like this (modeled as a typical ladder of purchases at least once a year, sometimes more):

This portfolio of TIPS investments in 2021 would pay $2,929 in coupon payments and also generate $6,088 in inflation accruals, based on inflation running at 1.8%. The $6,088 is the “phantom income” that is not paid out in the current year, but is taxable in the current year. As long the coupon payments can cover the tax on the phantom income, you will have a positive cash flow.

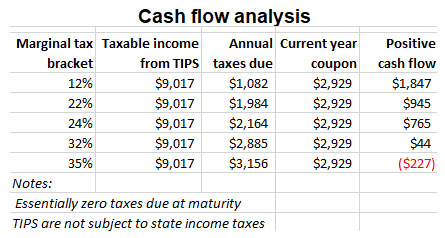

Here’s an analysis of the immediate-year cash flow, based on varying tax brackets:

When each TIPS matures, here’s the good thing: You don’t owe any tax on the accumulated inflation-adjusted principal, because you’ve prepaid it. So if you bought a $20,000 10-year TIPS in 2010 and it matured in 2020 with a 18% inflation boost to principal, you collected $23,600 at maturity and owed no tax. This could work in your favor for allocating spending money in retirement.

After retirement, the game changes?

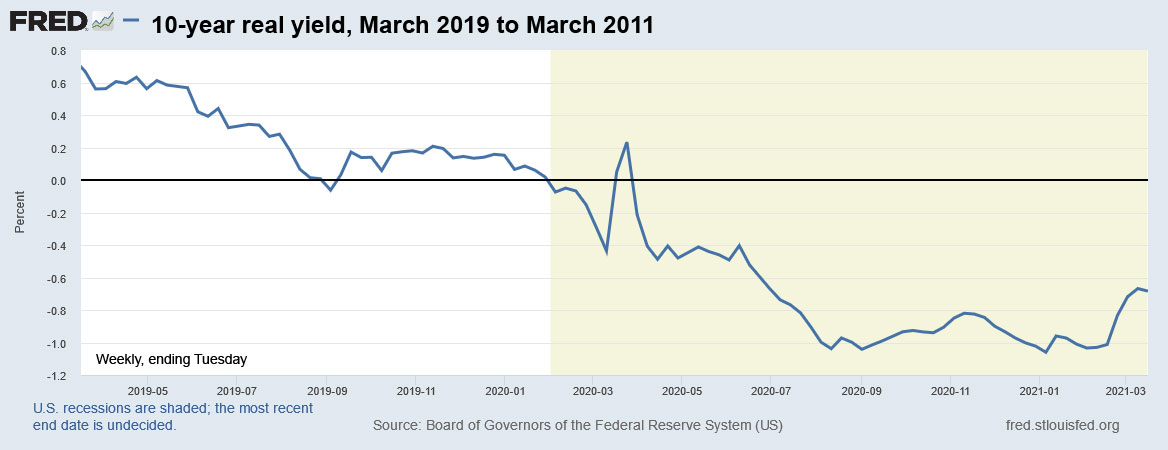

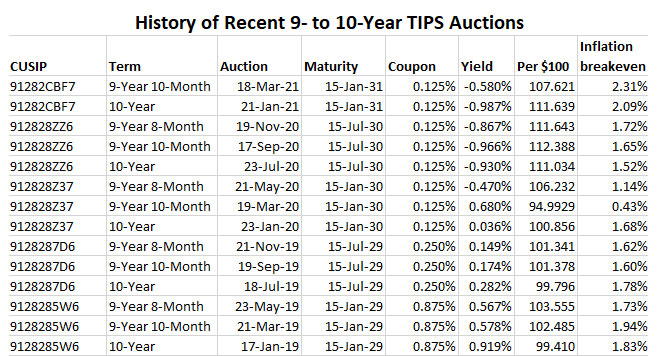

At various times over the last decade — including now — TIPS have been issued with negative real yields to maturity, meaning their returns will not match official U.S. inflation. TIPS haven’t been attractive, and I have haven’t purchased any. This was part of my deal with my financial adviser: I’d let the TIPS I hold at Treasury Direct mature out and then make all further purchases in a traditional IRA brokerage account.

Instead of buying TIPS with the maturing issues, I have re-invested the proceeds in I Bonds, which will at least perfectly match future U.S. inflation. I haven’t bought any individual TIPS issue since a March 21, 2019, 10-year TIPS reopening resulted in a real yield to maturity of 0.578%.

The key problem is: How do you fund net-higher new investments when you no longer have a source of current income? This is difficult in a taxable account when you are retired, because it means either 1) using your cash, which will have to be replenished, or 2) selling other assets in taxable accounts, possibly incurring taxes, or 3) withdrawing money from a tax-deferred account, which will incur a tax. That would make no sense. When you are retired, taxes enter into just about every financial decision .

So the obvious solution is: Use a traditional IRA brokerage account to fund future purchases of TIPS, when yields become attractive again.

But I am fine with my current TIPS investments, which will continue maturing through 2029 and providing cash for other investments, or just for fun in retirement.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It is true that I could have redeemed it when the rate was 1.9%, and maybe could have earned more…