By David Enna, Tipswatch.com

The March inflation report, released April 13, is going to create a lot of interest in U.S. Series I Savings Bonds, because the bond’s inflation-adjusted variable rate – for purchases from May to October — will increase to 3.54% from the current 1.68%.

All I Bonds will eventually get that 3.54% rate, annualized, for six months, on top of an I Bond’s fixed rate. But the new rate will raise a question for new investors in I Bonds: Should you buy before May 1, or after May 1? Or does it even matter? Before we get into that issue, let’s start with some basics, since I am assuming many new investors will now be researching I Bonds.

May 3 Update: I Bond’s fixed rate holds at 0.0%; composite rate soars to 3.54%

What is an I Bond?

An I Bond is a U.S. Treasury security that earns a composite rate of interest based on combining a fixed rate and an inflation rate.

- The fixed rate will never change. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through April 30, 2021, will have a fixed rate of 0.0%. The fixed rate will be reset on May 3, 2021, but it is highly likely to remain at 0.0%. The fixed rate is equivalent to an I Bond’s “real return,” meaning its return above inflation.

- The inflation rate changes each six months to reflect the running rate of non-seasonally adjusted U.S. inflation. Basically, the semiannual inflation rate is doubled to create what I call the I Bond’s “inflation-adjusted variable rate.” That rate is currently set at 1.68% annualized. It will adjust again on May 3, 2021, to 3.54% for I Bonds purchased from May to October. Over time, all I Bonds will get the 3.54% annualized rate for six months (on top of any existing fixed rate); but exactly when the new rate rolls out depends on the month of your initial investment.

Here is the formula the Treasury used to determine the I Bond’s current composite rate of 1.68%, drawn from the TreasuryDirect site:

| The composite rate for I bonds issued from November 2020 through April 2021, is 1.68% | |

|---|---|

| Here’s how we set that composite rate: | |

| Fixed rate | 0.00% |

| Semiannual inflation rate | 0.84% |

| Composite rate = [fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)] | [0.0000 + (2 x 0.0084) + (0.0000 x 0.0084)] |

| Composite rate | [0.0000 + 0.0168 + 0.0000000] |

| Composite rate | 0.0168000 |

| Composite rate | 0.0168 |

| Composite rate | 1.68% |

Key facts about I Bonds

An I Bond is a very safe, Treasury-backed investment that will at least track official U.S. inflation. The value of an I Bond can never decline. In a time of severe deflation, an I Bond might return 0.0% for six months, but its accumulated value will never decline. I Bond earnings compound tax-deferred for federal taxes until they are redeemed. Earnings are free of state income taxes.

The Treasury limits I Bond purchases in electronic form at TreasuryDirect to $10,000 per person per calendar year, plus allows an additional $5,000 in paper I Bonds in lieu of a federal income tax refund.

An I Bond must be held for one year, and after that, can be redeemed with a three-month interest penalty. After five years, there is no penalty for redemption. The I Bond will continue paying interest until its full maturity in 30 years. An I Bond can be purchased near the last day of a month and gain credit for a full month of ownership. That effectively shortens the initial lock-down holding period to 11 months.

I Bonds are an investment for capital preservation, not capital growth. You won’t get rich buying I Bonds, but you will be able to protect a portion of your portfolio against unexpectedly high inflation in the future.

Is there any chance the fixed rate will rise May 3?

Because of the $10,000-a-year purchase limit, there are two key strategies for investing in I Bonds: 1) Buy them every year to build up a sizable cache of inflation-protected money, and 2) Aim to get the highest fixed rate possible, because the fixed rate is permanent for the life of the bond.

I Bond investors — yes, me, too — are pretty passionate about getting the highest fixed rate possible. Right now the fixed rate is 0.0%, but a very attractive inflation-adjusted rate (3.54%) is about to kick in. Even the current rate of 1.68% is attractive versus very low interest rates across all safe investments.

The Treasury will reset the fixed rate on May 3 (because May 1 is a Saturday) and then again on Nov. 1. Is there any chance it will climb higher? I’d say with 99.8% certainty that the fixed rate will remain at 0.0% for the May reset. Why not 100%? Because at times, “the Treasury does weird things.”

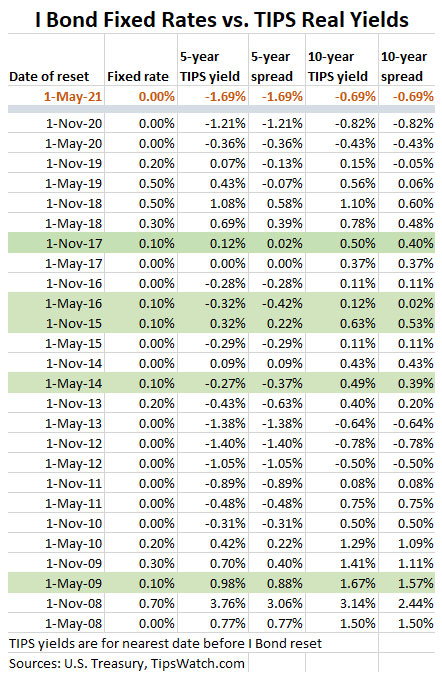

This chart shows all the fixed-rate resets back to May 2008, comparing the new rate with then-current real yields for 5-year and 10-year Treasury Inflation-Protected Securities. The top line compares TIPS yields at the market close on April 13, 2021. I’ve highlighted all instances when the fixed rate was set at 0.1%, slightly higher than it is today.

In today’s Treasury market, an I Bond has a 69-basis point advantage over a 10-year TIPS. But in every case where the Treasury set the I Bond’s fixed rate to 0.1%, the 10-year TIPS had a positive real yield, and at least a small yield spread higher than the I Bond’s fixed rate. So my conclusion is that the Treasury has no reason to raise the I Bond’s fixed rate; the bond already has a substantial yield advantage over a TIPS.

Now, the Treasury could throw us a curve ball and decide it wants to promote I Bonds for small-scale savers, and therefore set a 0.1% or 0.2% fixed rate. I’d be very surprised, and I don’t see that coming.

My conclusion. The fixed rate is going to remain at 0.0% in the May reset. The November reset is too far out for me to judge, but I’d expect it also to remain at 0.0%. And remember, any fixed rate increase in November would also be available to investors in January, when the purchase-limit clock resets.

Buy in April, or in May, or later?

Since the fixed rate is highly likely to remain at 0.0%, it should be irrelevant to this investment decision, unless you decide to wait until October to purchase I Bonds, to see if a higher fixed rate looks likely Nov. 1. By waiting until October, you’d still be able to capture the 3.54% inflation-adjusted rate for a full six months. So that is a viable option, if you believe there’s a chance that the fixed rate will increase in November.

But keep in mind, if you are investing $10,000 in an I Bond, the difference between a 0.0% fixed rate and a 0.1% fixed rate is $10 a year. In this article I am going to focus on the decision to invest in April versus May.

No matter the decision you make, an I Bond is going to be a very attractive addition to your asset allocation dedicated to “safety.” As shown in this chart, a 1-year Treasury bill is currently yielding 0.06% and best-in-nation 1-year bank CDs are yielding 0.60%. An I Bond — purchased in April or May — is going to easily outperform those metrics.

Is this a long-term investment?

I’m defining a long-term investment as a holding period of five or more years, avoiding the three-month interest penalty. We know that an I Bond with a 0.0% fixed rate will very closely match official U.S. inflation out into the future, but if you purchase an I Bond in April, you will know exactly what you will earn over the next 12 months.

Buy in April. That April-issued I Bond will earn 1.68%, annualized, for the first six months, and then 3.54%. annualized, for the next six months, for an overall first-year yield of 2.61%, more than four times the yield of best-in-nation bank CDs.

Buy in May. What if you invest in May? You would earn 3.54% annualized for the first six months, and then an undetermined rate for the next six months. Even if inflation runs at 0.0% for the next six months, you would still get a return of 1.77% for the year, nearly triple the yield of a 1-year bank CD.

I’ve modeled out other inflation-adjusted rate scenarios for the second six months, ranging from 0.5% to 3.0% for the March to September period. (Remember that the inflation-adjusted rate is double the actual-six month inflation rate; so an inflation rate of 0.84% equals an inflation-adjusted variable rate of 1.68%). So if inflation runs higher than 0.84% from March to September, purchasing in May will yield a higher return than purchasing in April.

Conclusion. There probably won’t be a lot of difference. If you believe inflation is likely to run hot from March to September, purchase your I Bonds in May. If you think inflation will cool off during that period, purchase in April. I suspect a lot of new investors will wait until May to start off with that 3.54% rate, and I can’t argue with that.

Is this a short-term investment?

As I noted above, an investor can shorten the I Bond’s 1-year holding period by purchasing late in a month and then redeeming early in that same month a year later, effectively creating an 11-month investment. But this strategy comes with a cost: The loss of the last three months of interest.

Buy in late April. In the 11-month scenario, an investor in I Bonds in April would earn 1.68% the first six months, then half of the 3.54% for the second six months (because of losing three months interest). This works out to an overall yield of 1.73% for the year, which again easily beats any very-safe one-year alternative.

Buy in late May. In this same scenario, an investor in I Bonds in May would earn 3.54% in the first six months and an undetermined yield in the second six months. Again, I’ve presented inflation-adjusted variable rate scenarios ranging from 0.0% to 3.0%, and one thing is very clear: Investing in May will out-perform investing in April in every scenario.

Even if the inflation-adjusted variable rate drops to 0.0% for the second six months, the investor would get a return of 1.77% — and the three-month penalty would be zero, because no interest was earned in the last six months. The Buy-In-May scenarios outperform Buy-in-April scenarios in every case.

Conclusion. If you are looking to invest in an I Bond as a safe place to store cash as an 11-month investment, wait until near the end of May 2021 to invest, then redeem early in May 2022.

The big picture

The financial market of April 2021 is difficult for investors seeking safety. If you are holding $10,000 in a brokerage firm’s cash or money market account, you will probably earn less than $5 of interest this year. Your monthly statement probably shows “30 cents interest.” An I Bond is a very safe investment with a flexible maturity, and that same $10,000 in invested in an I Bond could generate $250 or more in the next year, and then continue tracking official U.S. inflation.

I know, small potatoes. I’ve seen some investors chuckling in the Bogleheads forum over the obsession of I Bond investors to chase $10 to $20 in additional annual interest. But if you are holding cash for future use, you really want a return that at least matches official U.S. inflation. And I Bonds will do that, no matter if you buy them in April, in May, or later in 2021.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Why would someone at a relatively young age (say 40) invest in I bonds. Does anyone have a theory for this? I have always looked at I bonds and walked away. I may be missing something to consider, but won’t you be able to make more at broader stock market, say a safe investment, that you hold for a long time and make more than I bond. Follow that I bonds are inversely correlated to the stock market and will hold its value when the market crashes. If you are not going to sell out during a market crash, why would someone invest in I-bond as opposed to a safe stock. Someone following Asset allocation – having bond or I bond, makes sense. For someone who just have everything in market – does I bond makes sense?

This answer is pretty simple: It is a matter of placing some amount of asset allocation (5% 10%? Less?) into inflation protection. An I Bond can be considered a “bond” in your asset allocation, so if you are 80/20 stocks or 70/30, I Bonds fit into that 20% or 30% allocation. If you are 100% in the stock market — then you don’t want I Bonds. But … I Bonds can never lose value. Not one penny, no matter the inflation trend. But if inflation soars 10% in year, you gain 10%. I Bonds pay tax-deferred interest, so you can choose when to redeem and then pay taxes on the interest. The biggest reason to begin buying early is the $10,000 a year purchase cap. It takes many years to build a sizable allocation in I Bonds.

If you are 40 years old and want to be 100% into stocks, I Bond aren’t for you. They are an investment for capital preservation, not capital gain.

where can I go to buy I bonds? Is there a specific ticker?

You have to go through the TreasuryDirect.gov website and buy directly from the Treasury. There is no middleman and there is no secondary market. You buy them and then you decide to redeem them in the future. Here is a link: https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_ibuy.htm

Go to ” Teasury Direct” . : http://www.treasurydirect.gov

I thought I lost you. Then I saw your message on SA to come here. As always, thanks so much for your awesome article!! I’ll take your advise and buy in May. Thanks again, you’re the best!

If they could do it legally, Treasury would push the fixed rate to negative in May, primarily because of expected high demand as a result of the current relatively high yield. Fortunately for us, zero is as low as they can go.

You rock David. I always look forward to your thoughts.

Thanks David. Glad I found you here after your departure from Seeking Alpha. As usual, you have provided a clearsighted analysis. This article is an excellent introduction to share with family and friends unfamiliar with I Bonds. Keep up the great work!

Thank you! This answered my burning I-bond questions 🙂

Thanks so much! I LOVE to see my rather vague logic confirmed with your charts and discussion. Thanks very much!

I Love to read your articles about Ibonds. I am pretty small potatoes, but I LOVE to get a good deal and find a very safe haven for my hard earned dollars. I really enjoy reviewing the understandings I have through your charts, and appreciate your comments and logic that go along with them. Thanks so much – you are really meeting my needs.

Great write-up Dave – appreciate all of the effort you have put into your reporting