By David Enna, Tipswatch.com

The U.S. Treasury’s reopening auction of a 10-year Treasury Inflation-Protected Security — CUSIP 91282CBF7 — generated a real yield to maturity of -0.805%, a bit higher than was indicated by open-market trading in this TIPS.

This is a 9-year, 8-month TIPS and it carries a coupon rate of 0.125%, which was set by the originating auction on Jan. 21, 2021. And while an after-inflation yield of -0.805% is very low by historical standards for a TIPS of this term, it was still above the record low of -0.987% set at the January auction.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or below) inflation.

The negative real yield does not mean that this TIPS will have a negative nominal return. But it does mean it will have a return that lags official U.S. inflation by 0.805% over the next 9 years, 8 months.

Because the real yield was well below the coupon rate of 0.125% (the lowest the Treasury allows for a TIPS) investors at today’s auction had to pay a sizable premium for this TIPS, an adjusted price of about $111.149 for about $102.13 of value, after accrued inflation and interest is added in. This TIPS will have an inflation index of 1.0166 on the settlement date of May 28.

So, in other words, an investor who put $10,000 into this TIPS will have paid about $11,115 for $10,213 in value, and will earn an annual coupon rate of 0.125% along with inflation accruals that match U.S. inflation for 9 years, 8 months.

CUSIP 91282CBF7 trades on the secondary market, and had been trading with a real yield in a range of -0.84% to -0.85% right up to the auction’s close at 1 p.m. EDT. Because the real yield came in a bit higher at -0.805%, this indicates less-than-strong demand for this reopened TIPS. On the other hand, the bid-to-cover ratio was 2.5%, indicating decent demand.

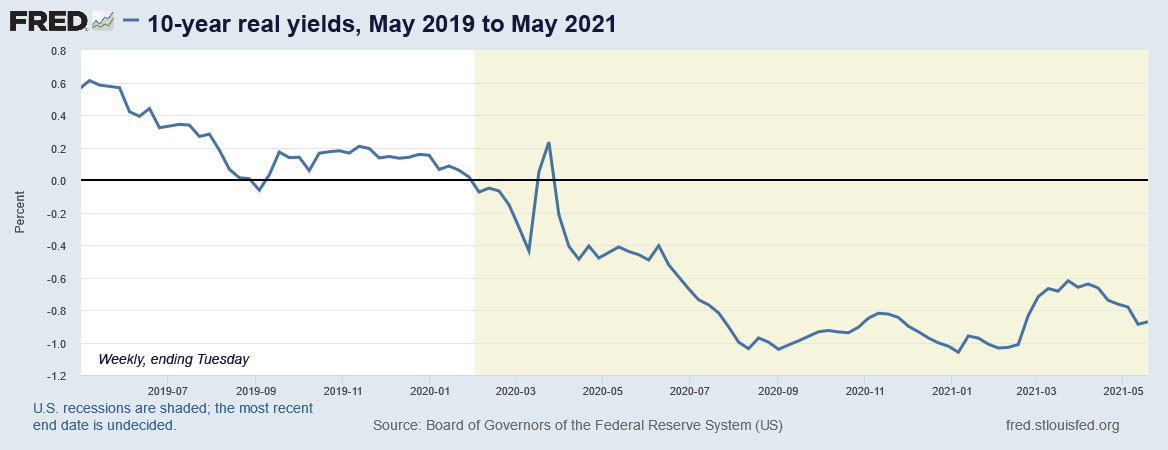

Here is a chart showing the history of 10-year real yields over the last two years, showing the dramatic bump higher in mid-March 2020, when COVID-19 fears caused a market panic, and then the dramatic fall after the Federal Reserve stepped in with its bond-buying programs, which continue today:

Inflation breakeven rate

With a 10-year nominal Treasury trading with a yield of 1.63% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.44%, high by historical standards. (You have to go back to 2013 to find inflation expectations higher than 2.5%.) This means that the reopened TIPS will out-perform a nominal 10-year Treasury if inflation averages higher than 2.44% over the next 9 years, 8 months. Think it will be higher? Buy a TIPS. Think it will be lower? Buy a nominal Treasury.

Before the auction, the trendline looked like the inflation breakeven rate would break the 2.5% barrier today. But investors backed off. From a Reuters report today:

Market expectations of a further rise in inflation would need evidence of the economy moving past full employment very, very rapidly, said Steven Ricchiuto, U.S. chief economist at Mizuho Securities USA LLC.

“We’ve probably already reached the peak level of economic activity, and that probably happened in March and April,” Ricchiuto said.

If you don’t “reach full peak employment very, very quickly, then you have to rethink, reset your overall expectations on the market,” he said.

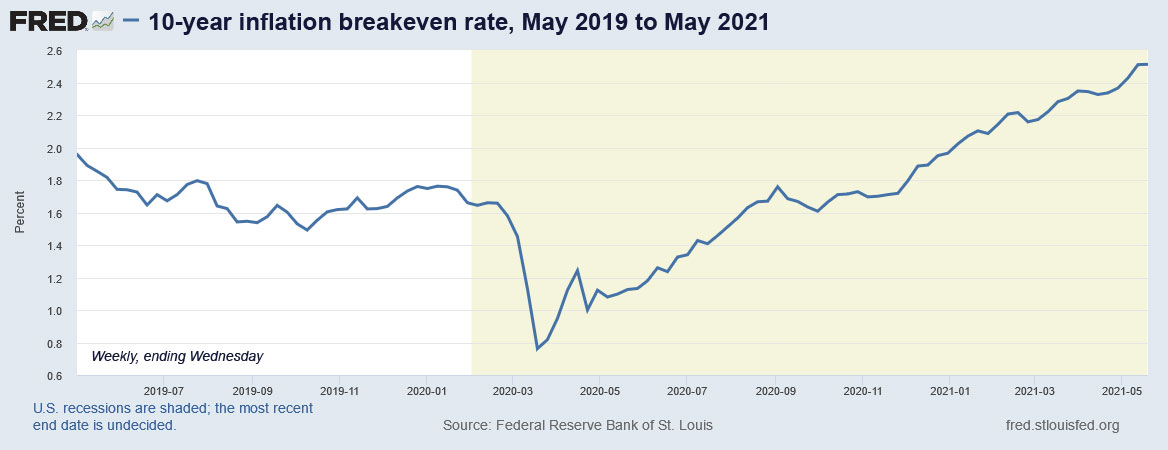

Here is the trend in the 10-year inflation breakeven rate over the last two years, showing the remarkable surge higher since the Federal Reserve and Congress began aggressive stimulus programs in March 2020:

Reaction to the auction

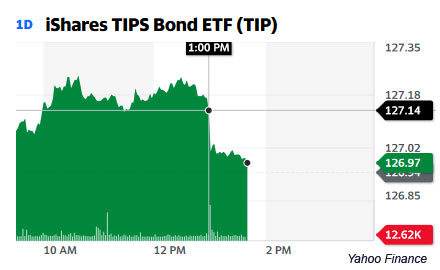

The TIP ETF, which holds the full range of maturities of TIPS, was trading slightly higher all morning, but its price fell immediately after the auction’s close at 1 p.m. EDT. This is another indication of weak demand for the reopening auction.

Overall, however, this auction result looks like was in the range of “predictable.” The Treasury was adding $13 billion in new supply, and bidders wanted a slightly higher-than-market yield.

The auction closes the history of CUSIP 91282CBF7, with three auctions that all produced real yields deeply negative to inflation. The Treasury will offer a new 10-year TIPS at auction in July and then reopen that issue in auctions in September and November.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

This discussion raises in my mind what is the optimal amount of inflation bonds to hold in a diversified bond…