By David Enna, Tipswatch.com

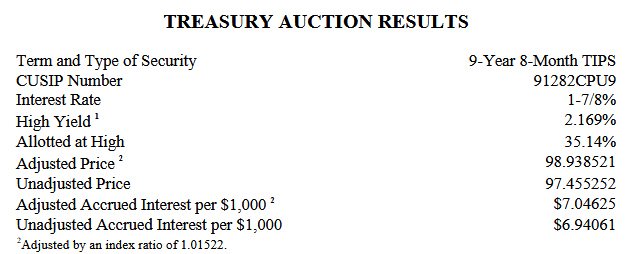

The Treasury’s offering of $19 billion in a reopening auction of a 10-year Treasury Inflation-Protected Security — CUSIP 91282CPU9 — generated a real yield to maturity of 2.169%, a bit above secondary market trading.

This is a 9-year, 8-month TIPS with a coupon rate of 1.875%, set at the originating auction on Jan. 22. It had been trading on the secondary market Thursday morning with a real yield to maturity of about 2.14%, and the “when issued” bond-market prediction was 2.15%. This indicates demand was a bit weak for this offering, even though the bid-to-cover ratio was a reasonable 2.52.

Definition: The “real yield to maturity” of a TIPS is its yield above future U.S. inflation, over the term of the TIPS. So a real yield of 2.169% means an investment in this TIPS would provide a return that exceeds official U.S. inflation by 2.169% for 9 years, 8 months.

Most likely, the real yield rose a bit higher because of market jitters over the U.S. stalemate with Iran, which has sent oil prices soaring. Iran reportedly is in talks on setting up a permanent toll for ships passing through the Strait of Hormuz, a position the U.S. opposes.

The result was a good one for investors. The real yield of 2.169% was near the top of the range for auctions since mid 2022, when real yields rose out of negative depths. At its originating auction in January, this TIPS got a real yield of 1.940%.

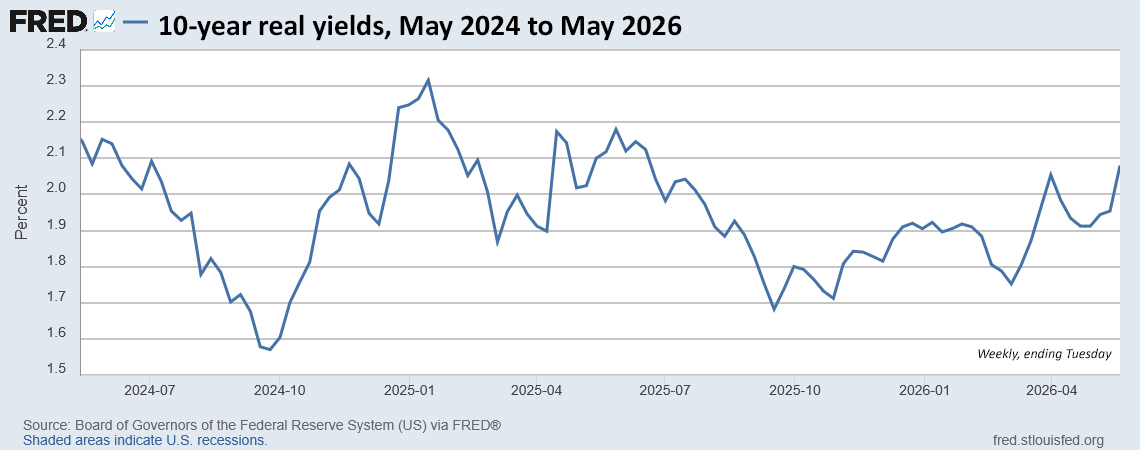

Here is the trend in the 10-year real yield over the last two years. While real yields have now climbed above 2.0%, they remain below highs of early 2025:

Pricing

Because the real yield came in well above the coupon rate of 1.875%, this TIPS auctioned at a discount, with an unadjusted price of 97.455252. It will also carry an inflation index of 1.01522 on the settlement date of May 29. With that information, we can calculate the cost of a $10,000 par value purchase at this auction:

- Par value: $10,000.

- Principal purchased on settlement date: $10,000 x 1.01522 = $10,152.20.

- Cost of investment: $10,152.20 x 0.97455252 = $9,893.85.

- + accrued interest of $70.46.

In summary, an investor paid $9,893.85 for $10,152.20 of principal on the settlement date of May 29. From then on, the investor will earn accruals matching future inflation, plus an annual coupon rate of 1.875% on adjusted principal. The accrued interest will be returned at the first coupon payment on July 15.

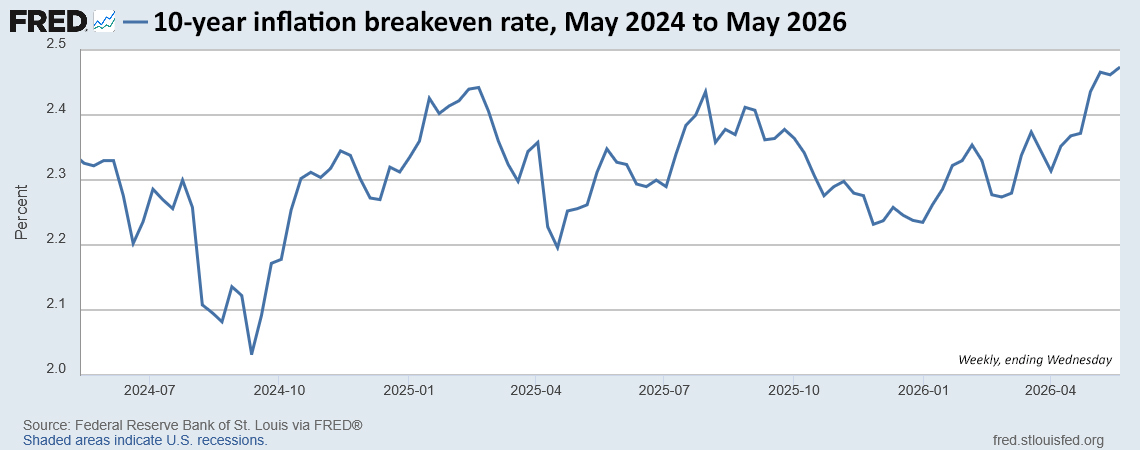

Inflation breakeven rate

At the auction’s close, the 10-year Treasury note was trading with a nominal yield of 4.60%. That creates an inflation breakeven rate of 2.43% for this TIPS, the highest number since a similar auction in September 2022. A high inflation breakeven rate indicates a TIPS is “expensive” versus the nominal Treasury of the same term.

Investors were betting that U.S. inflation will exceed 2.43% over the next 9 years, 8 months. Over the last 10 years, inflation has averaged 3.4%.

Here is the trend in the 10-year inflation breakeven rate over the last two years, showing the recent surge higher in inflation expectations:

Thoughts

This was a good result for investors, with the real yield rising well above the most recent reopening of this term, 1.896% on March 19. But the fact that investor demand was lukewarm indicates the market fears higher real yields in the future.

Nevertheless, for an investor committed to holding to maturity, a real yield of 2.169% is attractive.

Interesting side note: Because non-seasonally-adjusted inflation surged 0.85% in April, holders of this TIPS will get a 0.85% boost to principal in June. The same goes for all TIPS, no matter when they were issued.

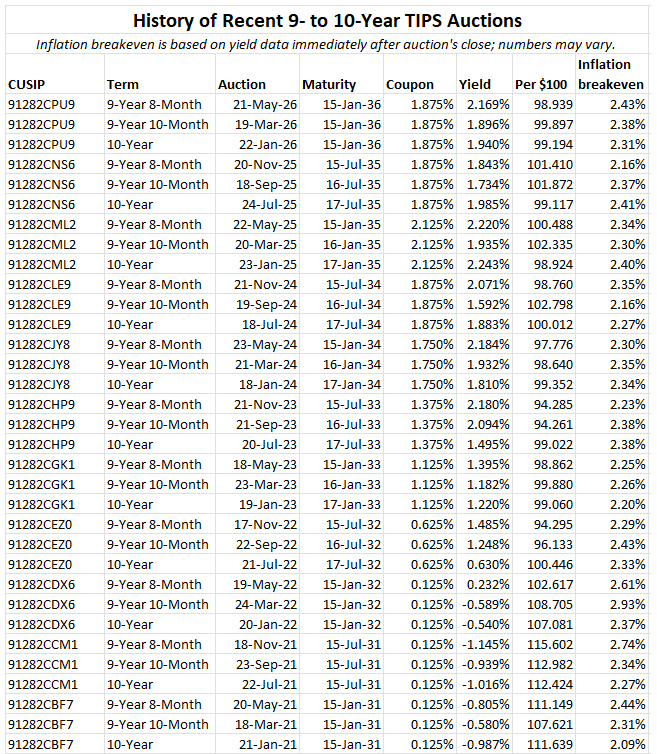

Here is the history over the last five years for TIPS auctions of this term. We’ve come a long way from the deeply negative real yields continuing through March 2022:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: UBS Just Cut Its Gold Target by $400. The Part They Kept Is the Real Story. – Serenity Wealth

I am a new TIPS holder. I’m retired. My TIPS funds are in a Vanguard Traditional IRA, so buying their brokered TIPS. I’m using this money to cover living expenses. My question is the choice between a 5-year ladder and a 10-year ladder? I have sufficient funds to cover either. Is the decision influenced by diversification of real yields through longer ladders, or any other strategies that I’m missing.

This is your personal decision. How long will you need this predictable cash flow at maturity? Do you expect to live another 10 years? Are you likely to need the inflation-adjusted cash in the next 5 years instead of 10? Are you comfortable committing the money to 10 years out? FYI, you can also buy at auction at Vanguard with no commission.

As TIPS matures I will keep it in VMFXX and draw off of it for the year’s expenses. The plan is to keep doing this until I mature/expire (I use 85 just to be safe in my other financial projections). I’m currently 57 and retired. I’m comfortable committing the money to 10-years out. My question was trying to understand if there were any nuanced financial benefits when starting a ladder construction to choose a 5-year ladder or 10-year ladder. Currently I have TIPS maturing 3 years out, 4 years out from the secondary market, and 5 years out from the recent auction. I’ll buy 5-year Aprils going forward, but should I fill out the 6-10 years now, or be content with re-upping a 5-year ladder. Again, I’m new to ladders and may be missing something basic.

Following up on David’s Interesting side note:

The baked-in 85 basis point bump for TIPS in June makes buying TIPS now quite attractive. A key point is that the bump is not reflected in the published yield to maturity.

Using Excel’s YIELD() function and just a 60bp bump gives a 6bp increase in YTM of the Jan 2036 TIPS under reasonable assumptions (simplified to avoid the messiness of partial periods). So a truer estimate of the break-even inflation rate is about 6bp lower than published. Other things being equal, I would expect the break-even rate to drop after June.

For fellow wonks, here are my method and assumptions:

You buy a 10-year 1.875% TIPS at issue, at a price of 97.5, giving a stated real yield of 2.154%, and hold it to maturity.

The general market expectation of inflation is 3%, or roughly 0.25% per month, so the extra bump over what might have been expected in June is 0.85% minus 0.25% or 0.60%. It is this extra bump that I used to determine the modified real yield.

I checked my work by projecting semiannual cash flows under reasonable rates of inflation and calculating the IRRs.

My wonk credentials: I am a retired Fellow of the Society of Actuaries.

Full disclosure: I bought $65,000 of this TIPS yesterday.

This is an interesting take. Since the market is fully aware of the high inflation accrual coming in June, TIPS prices and yields should be reflecting that fact, which could continue for several months. So it makes sense that real yields are being suppressed a bit, causing the inflation breakeven rate to report out larger than reality, given the certain inflation accrual in June and possibly 0.5% more in July and months beyond.

Thanks for the common-sense view of this phenomenon, David.

Here’s a simple example of the extreme case: The WSJ last Friday showed a price of 100.875 and a negative annualized yield of 6.08% for the 0.125% TIPS maturing July 15, 2026.

Why would you pay over par? Because the Reference CPI is guaranteed to increase by 1.05% between the settlement date and July 1 (the latest baked-in value), thus increasing the maturity value. This is not reflected in the yield calculation, but is the major factor in the market price.

kneth,

I think you summed part of it up with your statement:

“They work in almost the same way, (as bonds) except that TIPS have an inflation factor added.”

As an investor I don’t really need “complicated” I need easy. Also, the fact that you can’t get them in less than 5 years, except maybe in the secondary market is a bit of an issue. Most young investors can’t get a good handle on where they will be in 5 years so it is a bit of a problem sinking money into something that has to stay there for 5 years or more.

David points out this in his Q&A’s first answer to why not to buy TIPS:

“First off, I want to state loudly that TIPS are for preserving wealth, not building wealth. If you are in the early stages of investing and far from your long-term needs for buying a house or for paying for college or especially for retirement, TIPS aren’t going to be a great investment.”

So, if you dissect this what he is saying is if your goal is building wealth, TIPS aren’t going to do it for you, and neither are bonds, but if I have to choose between the two for a younger investor (read that under 40) I am going to use bonds or something like Vanguards MMF that pays very near short-term bond rates.

As an advisor I would try to stay away from putting investors in things they don’t understand and are hard to explain. This goes along with not investing in companies you don’t understand, especially when easier methods exist.

Frankly, ibonds are an easier concept to digest and IMHO are a better investment for preserving wealth because the principal is protected – TIPS are not when deflation rears its ugly head.

Now here is what I think is the sad story about TIPS and long bonds in general. They are not going to preserve your wealth into the future very far. By that I mean, if you know even the basics about TIPS and bonds you know that you only “get what you pay for” and if the future looks nothing like what you paid for, you may win or you may lose. What you are preserving is your VIEW of the future, not the future itself. If you lived through the inflation of the 1980’s it wasn’t by buying long bonds or TIPS in the 1970’s, but it was by buying the long end of the curve in CDs and bonds going out of this. Holding your nose and buying an adjustable rate mortgage at the height of this madness turned out to be the right play. Others like my folks were buying long CDs that paid quite well long after they were gone.

So yes, like most investments, they have a place and a time when they make sense and because we don’t have a crystal ball you can’t expect one investment to preserve your wealth. It takes diversification.

Thanks financialdave, those are all good points. In my reply to the comments below, I wasn’t asking whether TIPS are a good investment for an individual investor, which obviously could depend on a wide variety of circumstances. I was only asking about David’s statement that “most financial advisors don’t understand TIPS and find them hard to explain.” I guess I didn’t state my point well. At their heart, TIPS are just a type of bond, but with an extra inflation factor. My point was that it is the bond aspect of TIPS that is complicated and harder to understand, not the inflation factor. After completing all of the complicated bond calculations (which are the same for a TIPS as for a nominal bond), one need only do a simple multiplication by the appropriate inflation index to get the various TIPS values (adjusted price, adjusted principal, adjusted accrued interest, etc). So, if most financial advisors don’t understand TIPS, why is that? Is it because they don’t understand bonds in general? I would hope not. I think in order to call oneself a financial advisor, one probably ought to understand bonds. Or is it more of a willful avoidance of TIPS, due to the advisor’s personal biases or assumptions about their clients? Or is it something else entirely?

Part of the reason I ask such questions is, not having a financial advisor but having been told I should get one (but also being skeptical about their motives and concerned that they might annoy me more than help me), I wonder what I should look for or what I should look to avoid in a financial advisor.

Kneth,

I understood your question but was trying to be nice to the FA industry because I was an advisor for over 10 years (retired now), but I have no idea whether most advisors understand TIPS to the extent David thinks is necessary. I have a pretty good feeling though that most people haven’t gone to the extent of developing the exact interest rate calculation for ibond interest rates in Excel, such that they can replicate their balance to the penny without checking with TD. But that fact doesn’t keep them from investing in ibonds and it shouldn’t. One thing I am pretty confident in is if an advisor wants to “sell” you things on a commission like annuities – stay away. If they want to charge you near 1% of your AUM – in most cases stay away, as they aren’t going to make up the difference year in and year out.

What I tried to give you was my take on TIPS and bonds in general. They are ballast in your boat to keep it from tipping over in a storm. The fact that you understand how they work means you can probably understand how to construct a portfolio that matches your risk tolerance with just a little bit of study. A good advisor listens and tries to build on what you know and teach along the way. He doesn’t need to “sound” smart by putting you in things you don’t understand when a simple portfolio can be built with 7-10 investments. Here’s the bad news – most advisors don’t understand taxes, and this can cost you almost as much as 1%. One final pet peeve of my own and that is they don’t understand the “bad news” of over emphasizing Roth Conversions, or the bad news of oversized taxable brokerage accounts.

FinancialDave, I agree with much you say here, but TIPS do offer some certainty of the future. In this case, the return is certain to be 2.169% higher than official U.S. inflation over the next 9 years, 8 months. That is a certainty, unless the Treasury market collapses. What is uncertain is if 2.169% will look like an acceptable real yield in five years. It might not. But the return is certain.

David E, I also agree with mostly what you say, but being an Engineer, I prefer accuracy over precision. In that regard I think the below is technically a more informative response for the general investor.

A newly issued TIPS held to maturity guarantees a real return of +2.169% relative to CPI‑U. What is not guaranteed is whether CPI‑U will match your personal inflation, whether 2.169% will be attractive in the future, or what the bond will be worth before maturity.

I am also pretty sure you have said most of the below, if not all, over the years as you do an excellent job covering this topic.

Sometimes, in investing it is more about what is not said and what we don’t know that can “bite” us. Some of these items are:

TIPS are indexed to official CPI‑U, not “true” inflation.

TIPS give you inflation protection, not purchasing‑power certainty.

If held in taxable accounts:

PS: I don’t hold any kind of bond in a taxable account. Personal choice as I don’t need to spend that account so it would be an unneeded tax drag.

We also know the BLS can change the CPI-U and in fact in 2025 introduced a known ripple into the system with missing data for one month. Not a big deal, just an example of a bigger problem when thinking “precise is good”

10 years is a very long time to think you can lock any significant amount of money into a strategy that once again can be disrupted by needing the money before the 10 years is up. I guess that’s the need for a well-constructed ladder, which is only as good as the total size of it to your “emergency need.”

I’ll just point out I always say TIPS inflation accruals are based on “official U.S. inflation,” and definitely not each individual investor’s personal inflation. That’s the deal we accept. As for selling TIPS before maturity, I have been investing in TIPS for 27 years and I have never sold before maturity. My household portfolio makes TIPS and I Bonds a puzzle-piece investment, amounting to around 15% to 18% of assets. The I Bonds will be sold when I need the cash. I won’t be selling TIPS before maturity. This is the path I encourage for readers of this site.

I bought a little of this TIPS back in January, but hoped the real yield might go higher at one of the reopening auctions. I bought some more today, and I’m pleased with the result.

Thanks as always for your excellent and educational reporting. I did buy at this auction to increase holdings for 2036 maturity and will continue to fill in other years on the secondary market.

The Economist issue released today talks about TIPS. https://www.economist.com/finance-and-economics/2026/05/19/investors-fear-another-surge-in-inflation

Paywall, unfortunately.

Try here:

https://www.kokthum.com/international/market-puzzle-why-inflation-fears-aren-t-showing-up-in-bond-prices

I read that China and Japan are divesting a lot of US bond holdings currently. I’d say that may be a big factor in the rising rates.

Thank you for your coverage. I seldom see any articles about TIPS popping up in my newsfeed. Perhaps it’s because salespeople don’t profit from them?

I have been able to verify that I can do Roth Conversions by moving a portion of the TIPS to my Roth. I will continue on that track.

Happy investing and may the odds be ever your favor.

I hate to say this, but most financial advisers don’t understand TIPS and find them hard to explain. Same with most financial journalists.

Why do you think that is? I know TIPS are complicated, but I don’t think they are that much more complicated than nominal Treasury notes/bonds (excluding Treasury bills, which are much simpler). They work in almost the same way, except that TIPS have an inflation factor added.

Kneth, think of it this way: 1) You buy $10,000 of a 10-year nominal Treasury note at 4.5%. While the market value of that investment will change over time as yields rise and fall, the principal will never vary from $10,000, and the coupon payment will always be based on $10,000. And the final payment will be $10,000. Pretty simple.

2) You buy $10,000 of a TIPS with a real yield of 2.0%. The market value also varies based on yield trends, BUT … the underlying principal will begin changing on day 1 and continue changing every day of the year, based on daily inflation accruals. Principal usually goes up, but could go down in a time of deflation. The 2.0% coupon payment (in actual dollars) will rise and fall with the accrued principal. At maturity, you get par value adjusted for inflation over those 10 years.

The TIPS isn’t massively complicated, but it takes some work.

Ok. Well, I’m probably a weirdo but I enjoy tracking the varying principal and the varying coupon payments for my TIPS. I don’t think I am too obsessive about it. I don’t track the changes every day, but I do at the end of each month, and on the dates when coupon payments occur. I don’t look at this so much as making TIPS more complicated, but rather it makes them more interesting.