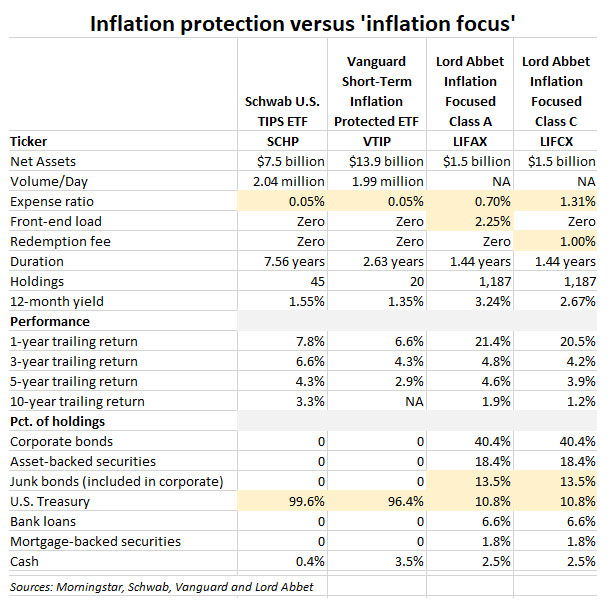

The Lord Abbet Inflation Focused fund is a mixed-bag short-term corporate bond fund, not a typical TIPS fund

By David Enna, Tipswatch.com

I have an elderly friend (she’s 90+ years old so I think it’s OK to call her elderly) who is whip-smart and able to monitor her own finances. But sometimes she calls me for advice on safety-first investments.

“I am not a financial adviser!” But I listen. In this case, she had a Goldman Sachs brokered CD that was paying 3%, but got called, leaving her with more than $50,000 in cash and no good alternatives that would yield more than 0.5%. This cash was now in the hands of a “wealth adviser” who is “affiliated” with her credit union.

She told the adviser that she is worried about surging inflation. His advice: Put that cash into the Lord Abbet Inflation Focused Fund, either class A or class C.

She asked me: “What do you think of these funds?” I think she already had a good idea what I was going to say. Like I said, she’s smart.

Well, let’s see … the class A version (LIFAX) comes with a 2.5% upfront load and an expense ratio of 0.70%, and the class C version (LIFCX) has no upfront load, but a 1.31% expense ratio and a 1% redemption fee. Does it make sense for a 90+ year old to pay a 2.5% load to buy into any mutual fund? No. Does it make sense to pay an expense ratio of 1.3% and a redemption fee of 1% when there are much cheaper options? No.

(FYI, LIFAX can be purchased at Fidelity — and probably other quality online brokers — with the load fee waived. But her wealth adviser wasn’t offering her that opportunity).

I am not a financial adviser, but this looks like questionable advice to me. My immediate advice would have been to just open an online savings account paying 0.5% and live with it. But my friend was looking for a safe investment with a reasonable return that could rise with surging inflation. She is very worried about inflation.

So, my suggestion was that she look at a couple of ETFs that hold Treasury Inflation-Protected Securities: Schwab’s SCHP, which holds the full range of maturities, and Vanguard’s VTIP, which holds maturities of 0 to 5 years. Both of these have expense ratios of 0.05% and can be purchased without any commissions at most brokers.

The Lord Abbet Inflation Focused fund is an easy “sell” right now because it has had a spectacular performance in the last year, with its class A shares gaining 21.4%, versus returns of about 7% for typical TIPS funds. But why was that gain so high? Because this fund skews much higher in risk, with large holdings of corporate bonds, asset-backed securities and even 13.5% of assets in junk bonds. Its U.S. Treasury holdings are right around 11% of assets. It is NOT a traditional inflation-protected fund, even though Morningstar classifies it as “Inflation-Protected Bond.”

This chart shows how it is unlike traditional inflation-protected funds, with low fees, no sales charges and investment focused on U.S. Treasurys:

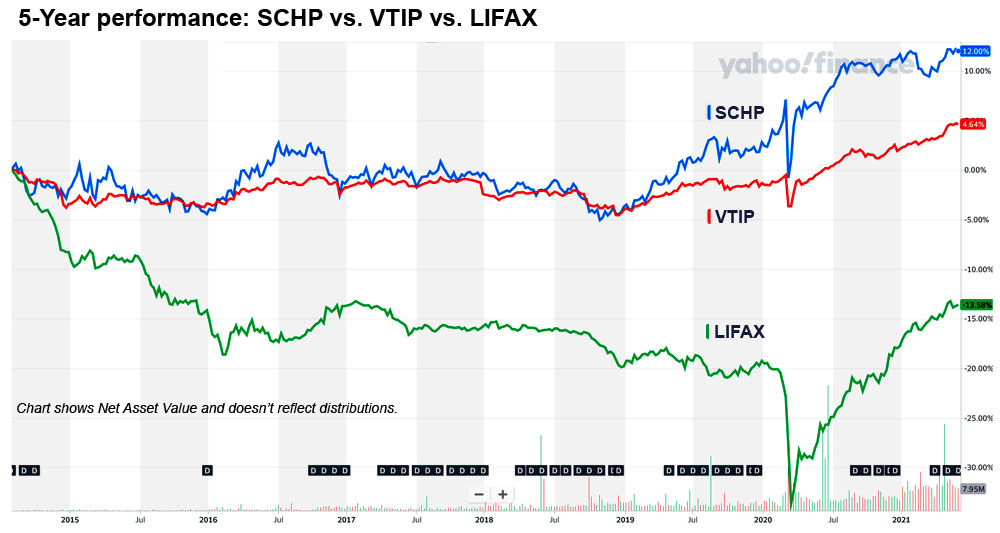

Look back 10 years, and The Lord Abbot fund’s annual return is only 1.9% (class A) and 1.2% (class C). This fund carries much higher risk than the typical TIP fund, even though its duration is quite low, at 1.44 years. Here is how LIFAX has performed versus SCHP and VTIP over the last five years:

This chart — which doesn’t reflect any load fee paid by the investor — shows how the recent out-performance of LIFAX can’t overcome years of poor performance in a time of consistently declining interest rates. This is from Morningstar’s investment analysis:

“Lord Abbett Inflation Focused’s aggressive style and unconventional inflation-protection tools have contributed to a volatile experience for investors in its otherwise conservative peer group. … This strategy’s allocation closely mirrors Lord Abbett Short Duration Income LLDYX, which carries a risky profile through significant corporate bond stakes (40%-55% of assets) and securitized credit (35%-55%). Exposure to below-investment-grade issues accounted for 14% of this portfolio at the end of July 2020 and even reached 25% back in 2014. …

“(T)his team hedges against inflation via Consumer Price Index swaps as they are less sensitive to interest-rate spikes than TIPS. Still, they can be volatile with changes in inflation expectations.”

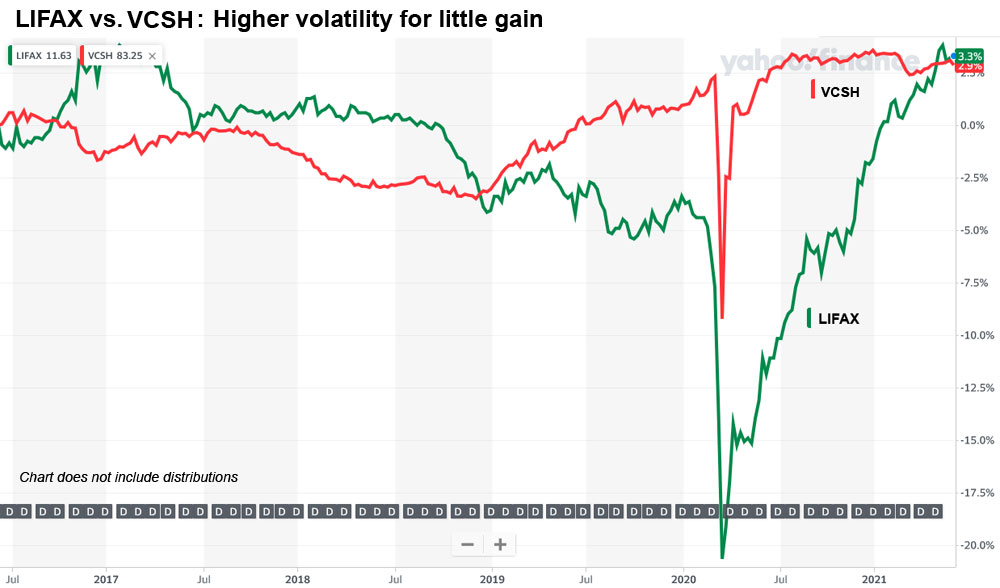

So, it is clear that Lord Abbet Inflation Focused is much more of a short-term corporate bond fund with very little direct exposure to U.S. Treasurys. That raises the question: How has it done versus more traditional short-term corporate bond funds, such as VCSH, Vanguard’s short-term corporate bond ETF, with an expense ratio of 0.05%? Here you go:

Keep in mind that this chart does not reflect the 2.5% load fee charged by advisers. LIFAX was down more than 20% in the depths of the market mania of March 2020, but has rebounded nicely since then. VCSH was less volatile.

So for the investor looking for a short-term corporate bond fund with an overlay of inflation swaps and high volatility, LIFAX could be worth a look. (But try to find a way to buy it without the load fee.) Otherwise, if you have a priority on safety and low fees, look elsewhere.

For risk-welcoming investors looking for a twist on inflation protection, I think a fund like The Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL) is worth a look. I don’t own it and haven’t analyzed it carefully. It has an annual expense ratio of 0.99% — a negative — but at least it holds 85% of its assets in SCHP, so it is heavily exposed to TIPS. Then it adds long options tied to the U.S. interest rate curve, so it can benefit from volatility. It had a total return of 14.6% in 2020. It’s a new fund and may not have a large enough trading volume for your brokerage to allow dividends to be reinvested.

So what did my friend do?

After a couple of discussions with me — which basically confirmed her point of view — she asked her wealth adviser if he could put her $50,000 in SCHP or VTIP or some combination, and how much it would cost. She said he paused. Then he said, “I think I could do that with about a $300 commission.”

She laughed. I told you she is smart. She asked for the money to be sent to her by check, and she will no longer work with that adviser. She has a T.D. Ameritrade account where she can buy the ETFs she wants at zero cost.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Disclosure: I have investments in SCHP and VTIP.

Thanks for the blog, I find it very informative.

Your mention of IVOL interested me so I just took a look at the performance. It did not outperform SCHP during the volatility surrounding the start of the pandemic and it got killed last week during the volatility. Looks to me like its another good strategy on paper but difficult to execute.

Good point. One of the big negatives about IVOL — beyond the high expense ratio — is that it has only existed since May 2019, so we can’t see how it will perform in varying markets. Its year to date total return is now -0.30%, versus 0.91% for SCHP.

Thanks for all the great info David!

What do you make of LQDI, a BlackRock/iShares’ intermediate-term corporate bond ETF with inflation hedges? It seems like a reasonable/low-cost fund to add some inflation-hedging to a corporate bond fund, if the term/credit risk make sense in a portfolio & when already maximizing I-bond contributions and in this era of negative TIPS yields. As your post makes clear, its so difficult to really understand everything out there for us regular folks!

I assumed just by seeing the ticker that LQDI overlays the iShares LQD intermediate corporate bond fund with inflation hedges. That looks to be the case. Its expense ratio is 0.18%, a bit higher than LQD’s 0.14%, but reasonable. Total assets are $33.6 million (million!) versus $39.8 billion for LQD. Average volume is also minuscule, so don’t make any market orders. It had a total return of 15.8% in 2019 and 11.8% in 2020, versus 17.4% and 11% for LQD. It was created in May 2018, not much history to look at.

It uses inflation swaps to potentially gain from increases in inflation.

The good thing about this fund (and LQD) is that it is entirely invested in investment grade corporate bonds, skewed toward the BBB rating. No junk in this. Its effective duration is 9.43, so it is going to be volatile when interest rates swing. The big problem for me is that is such a small fund, I have to wonder if it will continue to exist. IVOL has built up to $2.9 billion in assets and a much higher average volume.

Thanks for sharing your thoughts David! I always read your blogs and learn a lot – much appreciated. Will stick to TIPS & Ibonds but keep reading about other options out there.

Nice work, David. Love a story with a happy ending.

I have always assumed credit unions were better than the banksters at looking after their customers but I guess not. I hope your friends wealth advisor reads this article and is ashamed of himself, even if it’s only for a couple of seconds.

I think some credit unions feel they need to provide “all services” to their customers, and so they set up referral arrangements with this sort of adviser at outside firms, who in some cases are just commission sales people. The non-fiduciary status should be made very clear, however.

It is sad how alert you have to be, I am almost 86 what gives you a lot of life experience, but it shows how careful you have to be with money. Glad she is smart and has you to talk to. Hanna

I’m often asked why I’m not a financial advisor. This article is exactly why. I could never push those high fee funds or ask for commissions like that. Just gross.

Bust ’em, David!!!

Thank you!