By David Enna, Tipswatch.com

For the third month in a row, U.S. inflation surged to higher-than-expected levels in May, reaching the highest annual level in nearly 13 years, the Bureau of Labor Statistics reported today.

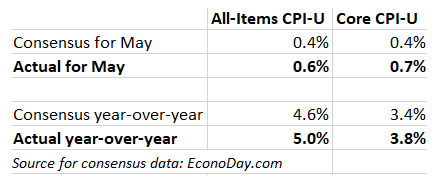

The Consumer Price Index for All Urban Consumers increased 0.6% in May on a seasonally adjusted basis, the BLS said. Over the last 12 months, the all-items index increased 5.0%; this was the largest 12-month increase since a 5.4% increase for the period ending in August 2008. The May numbers were well above the consensus forecasts of 0.4% for the month and 4.6% for the year.

Core inflation, which removes food and energy, rose 0.7% in May and 3.8% over the last 12 months, also racing well ahead of the consensus forecasts of 0.4% and 3.4%. That was the highest increase in core inflation since June 1992.

One amazing aspect of this report was that seasonally-adjusted gasoline prices actually fell in May, down 0.7% for the month but still up 56.2% over the last 12 months. I expected to see higher gas prices, caused by shortages throughout the Southeast thanks to the Colonial Pipeline shutdown. (Gasoline prices in the Southeast have definitely not fallen. Before seasonal adjustment, gasoline prices rose 4.2% in May, the BLS said.)

The index for used cars and trucks continued to rise sharply, the BLS said, increasing 7.3% in May. This increase accounted for about one-third of the all-items increase. Here are other highlights from the report:

- Food prices increased 0.4% in May, the same increase as in April, but are up only 2.2% over the last year.

- The May increase for food was mostly due to the index for meats, poultry, fish, and eggs, which increased 1.3% over the month. The beef index rose 2.3 percent in May.

- The energy index was unchanged in May after declining slightly in April, but is up 28.5% over the last year.

- Apparel prices rose 1.2% in May and are up 5.6% over the last 12 months.

- The household furnishings and operations index increased 1.3% in May, its largest monthly increase since January 1976. Widespread shortages are being reported in furnishings.

- The index for car and truck rentals continued to rise, increasing 12.1% after rising 16.2% the prior month.

- The medical care index declined 0.1% in May after rising in each of the four previous months.

- The costs of shelter rose 0.3% in May, and are up 2.2% over the last 12 months.

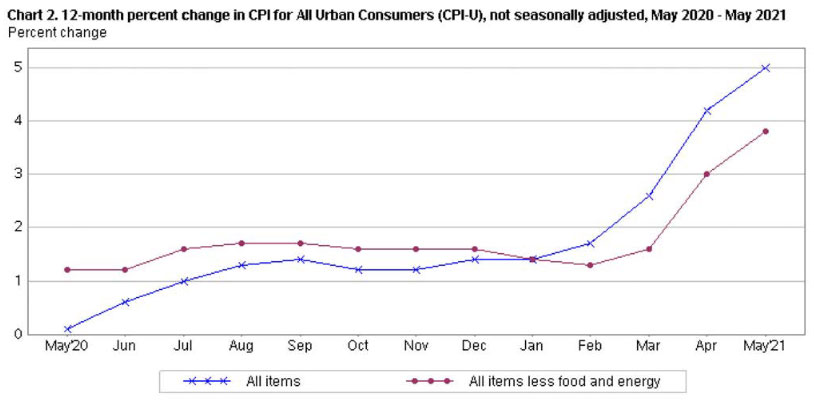

The May report again shows a widespread pattern of unexpectedly high inflation across the U.S. economy, with almost every category except energy showing strong price gains in the month. Here is the 12-month trend for all-items and core inflation, showing the impressive surge higher after the Federal Reserve and congressional stimulus programs stepped up in March 2020:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For May, the BLS set the inflation index at 269.195, an increase of 0.80% over the April number. This follows increases of 0.82% in April, 0.71% in March and 0.55% in February.

For TIPS. The new inflation index means that principal balances for all TIPS will rise 0.80% in July, following the 0.82% increase in June. Because non-seasonally adjusted inflation rose a bit faster than the seasonally adjusted number, you can expect a reversal of that trend in coming months. (Seasonal and non-seasonal numbers balance out over 12 months.) Here are the new July inflation indexes for all TIPS.

For I Bonds. The May inflation report is the second in a string of six months that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on November 1. After two months, inflation is up 1.63%, which translates to a variable rate of 3.26%, already getting close to the current rate of 3.54%. Four months remain, and a lot can happen in four months (especially summer months, when inflation is notoriously volatile.)

Here are the numbers so far:

What this means for future interest rates

The Federal Reserve continues to predict this surge in inflation will be “transitory,” but it’s disturbing that inflation has been running much higher than expectations for three months in a row, even while gas prices were stable. The Fed is hoping to discourage an “inflation psychology” seeping into our consciousness, because it could set off a snowball effect of higher wages and higher raw material costs.

From today’s Wall Street Journal report:

Food makers said their costs are climbing at an alarming rate, prompting them to raise some prices. “The inflation pressure we’re seeing is significant,” General Mills Inc. Chief Executive Jeff Harmening said at a recent investor conference. “It’s probably higher than we’ve seen in the last decade.”

He and his peers point to transportation, commodity and labor costs all increasing at the same time. They expect the trend to continue for at least the rest of this year.

The Federal Reserve tracks a different inflation index — Personal Consumption Expenditures — which was up 3.6% through April and looks likely to top 4.0% for May when that number is released later this month. The Fed wants inflation to “average” above 2.0% for a sustained time. It seems well on its way to reaching that goal.

At some point, probably soon, the Fed will need to begin “talking up” potential plans to taper its bond-buying stimulus programs, which would allow longer-term U.S. rates to begin rising. As of this morning, the stock market is rising nicely despite today’s inflation report. That indicates the financial markets don’t see Fed tapering beginning anytime soon.

But the Fed faces serious challenges if U.S. inflation continues to rise much higher than expectations.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David – Thank you for your timely and insightful reports.

I’ve been intrigued with Deferred Income Annuities. The kind that make payments for life. I plugged in some numbers to a income estimator. The assumptions were funding the annuity at age 60 and beginning payments at age 75. There was an option for 2% inflation factor or straight line. With the 2%, one would double their money after about 14 years of payments age 89 but 29 years after the initial investment. At 0% it would take about 15 years. Living to age 100 would quadruple the initial investment with the 2% factor.

When compared to EE Bonds which double at 20 years these investments seem risky right now although the lifetime payment benefit is definitely the hook with this kind of investment and there is longevity in my family. And you get a stream of income and don’t have to wait the 20 years to get the payments.

Of course you can get a stream of income by laddering EE bonds too.

Do you see any circumstances where these investments might make more sense? Maybe with rising interest rates improving the rates of return and shortening the doubling period? I don’t see it right now with the terms that are being offered.

I don’t know enough about annuities to have a strong opinion, but the only type of annuities I’d consider are either a straightforward immediate income annuity, or a deferred income annuity like you describe. The fees would need to be very low and the insurance company would need to have solid financials. Having these in the mix of a total financial plan could make sense, to ensure some level of lifetime income.

“But the Fed faces serious challenges if U.S. inflation continues to rise much higher than expectations.”

I don’t think the Fed faces any challenges. They will just act very surprised that the inflation wasn’t transitory in the same way that they were very surprised that subprime wasn’t contained.

The challenge will come when “something has to be done about it.” The Fed has been very reluctant to do anything that would disrupt the stock market, which hit another all-time high today. Going up, no problem. Going down, big problem. I don’t think the Fed has the courage to use its “tools” to control inflation. If things go well for the Fed, inflation will settle in around 2.75% to 3% for the next couple years. But there are big risks it could be higher.

I’m guessing that they will say that a little inflation is good for the economy and that they are raising their inflation target to 3% or 4%. That will buy them another year or two. And then I think we get to even higher inflation at which point Michael Burry’s prediction will start playing out.

Thanks David for yet another timely and insightful post!

It makes me wonder (at the risk of being thought to be a market timer, which is really not my thing) if putting some or all of one’s cash/money market funds into a short-term TIP ETF like VTIP isn’t a no-brainer choice at the moment. MM funds of any type are yielding nothing, online CD’s under 5 years not much better. Once one has maxed out the 10K per person iBonds allotment what else is there?

VTIP will do very well (and has been doing very well) if inflation surges and real interest rates stay level or drop lower. That looks like a solid bet for the near future. VTIP is more risky than cash — it had negative total returns in 2013 and 2014 — but nothing dramatic.

My prediction of a 5% variable rate in November might come true at this rate!

Anything is possible. I know from experience that summer inflation is incredibly unpredictable. A 5% variable rate would require inflation of 2.5% from March to September. We are on the track now, but inflation will begin waning (a bit) in June, July and August because of less-favorable year-over-year comparisons.

It’s hard to say what ‘inflation’ as measured by the Fed will be versus the reality that real people are contending with. I’ve noticed numerous articles from food producers and manufacturers as well as from chain restaurants posting that prices will begin increasing from high-single digit to low double digits this summer.

I think the BLS’s “food” and “food away from home” categories reflect reality pretty well. “Housing” is a disaster, though, officially up 2.2% in a year when housing prices have increased 12% or more.

Looking to upcoming months: Non-seasonally adjusted inflation rose 0.55% in June 2020, 0.41% in July 2020 and 0.32% in August 2020. So the “easy” comparisons for non-seasonally adjusted inflation ended in May (which was 0.0% last year.) The next few months will be interesting.

Isn’t this just base effect? A year ago, prices were misleadingly low, because we were in a state of deflation (or disinflation?) because of the pandemic?

Yes, base effect is a factor. If you look back two years, inflation has increased 5.1% total over that time May 2019 to May 2021. That’s an average of 2.55% a year, more reasonable, but still a fairly brisk pace. What’s weird right now is that inflation has sharply increased in the last 4 months after being dormant for nearly a decade.

It’s not my intention to quibble, but I don’t think it’s weird at all, given the lack of normal inflation in most of the months of 2020, which is what 2021 prices are being compared to. It would be interesting to see a chart of CPI from 2010 or 2015 through March 2020 and see if the trend would have put us where we are. I assume prices increased something like 2% per annum until around April 2020, and then prices were close to flat for much of 2020, and now we’re just catching up to where we would’ve been had there been no pandemic. In other words, 2021 inflation is not weirdly high. Rather, 2020 inflation was weirdly low.

You can find all that historic inflation data on this page: http://eyebonds.info/tips/cpi/cpibig_06.html (for non-seasonally adjusted inflation). For the five years ending in June 2020, inflation averaged 1.6%. For the 10 years ending in June 2020, inflation averaged 1.7%. So, in other words, we had a decade of 1.7% average inflation.

Wow, thanks. So in that context, 2.55 is indeed a little hot

Using your link, average annual inflation from 1972 to 2008 was 4.7%, median 3.7%. After the crash, from 2009 to 2020 average annual inflation was 1.4%, median 1.6%. We are going to need a whole lot more inflation to get back to normal, which is around 4% per year. These crazy low rates over the last decade are either a result of continuing fallout from the crash, or the CPI numbers are being “managed” by the BLS, perhaps to allow the Fed to keep rates artificially low. There is much questioning about whether the CPI nowadays actually measures true inflation.

Thanks for the timely news and analysis, as always David. Referring to a couple of previous posts perhaps, finally, the return on a TIPS purchased in the past will exceed that of a nominal treasury of like maturity purchased then.

Yes, when inflation runs at unexpectedly high levels, TIPS and I Bonds are the investments to have in your portfolio. TIPS principal balances will have increased nearly 2.9% for the four months ending in July.

The rise in costs to get protein, whether fish meat or eggs, has really been shocking to me. I know they say this is a post-pandemic issue, as people resume eating out and eating differently than cooking at home. But I wonder if it’s also related to the widespread drought everywhere. I’ve reverted to eating mostly tinned fish, such a sardines, rather than large fresh fish. And while I eat extremely little meat, I would occasionally like a bit of lamb. I’ve been horrified at what I’ve seen at the stores. I’m retired, and have met my savings goals. This must be so difficult for young working people with families. I guess we’re all going to eat a lot more dried beans.

Nothing wrong with dried beans prepared properly. Soak overnight, rinse thoroughly and cook as usual. Add any salt when done. I haven’t eaten any meat, fish or fowl for decades.

This method will make your legumes much more digestible.

Yes, I didn’t mean it as a negative. I actually make an Indian dal that I could totally subsist on, if needed!

I think it is time to share a link to that recipe!

Beef and Beans are a great recipe I got out of a 1970s Rival Crock Pot cookbook. Best recipe book I ever bought. Yard sale for $2.00. Have too add the salt yes sir.

Beef and fish prices are getting to stunning levels. Even the cheap cut “beef stew meat” can run $7 a pound. I usually buy frozen mahi mahi and tuna steaks in bulk at Costco; those are a good deal, but certainly not cheap. And of course … Costco’s rotisserie chicken, still only $4.99 for their huge birds. (But how long can that last?)

Since this thread keeps growing, I’m adding a link to a Cuban black beans and rice recipe. It’s time consuming, great flavors: https://www.mysaratogakitchentable.com/?p=211

Just go vegan folks. For the animals, for your health, for the planet. At age 66 I run a 5 Km with the forty year olds. Protein needn’t come from animals. 🙂