By David Enna, Tipswatch.com

Can anyone make the case that a 5-year Treasury Inflation-Protected Security with a yield lagging inflation by 1.73% and an upfront premium cost of nearly 10% makes sense as an investment?

Hey, I can.

But that doesn’t mean I will be investing in Thursday’s $16 billion reopening auction of CUSIP 91282CCA7, creating a 4-year, 10-month TIPS. I probably won’t. Nevertheless, in today’s low-interest-rate environment — accompanied simultaneously by surging inflation — this TIPS reopening remains an intriguing investment, “relatively speaking.”

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

CUSIP 91282CCA7 was created in an originating auction on April 22, 2021, when it generated a real yield to maturity of -1.631%, the lowest in history for any TIPS auction of any term. The Treasury set its coupon rate at 0.125%, the lowest it will go for a TIPS. Investors had to pay a sizable premium, about about $109.41 for about $100.32 of value, after accrued inflation and interest were added in.

It now trades on the secondary market, and you can follow its current real yield and price in real time on Bloomberg’s Current Yields page. As of Friday’s market close, it was trading with a real yield of -1.73% and a price of $110.30.

If that yield holds through Thursday’s auction, it would set a new auction low for any TIPS of any term. Investors at this week’s auction will actually pay a higher price than Bloomberg indicates, while getting additional principal. Accrued inflation and interest will put the price at about $111.45 for $102 of adjusted value. This TIPS will have an inflation index of 1.01804 as of the June 30 settlement date.

(Just for nerds: As an aside, it’s remarkable that this TIPS was originated on April 15 and non-seasonally adjusted inflation has increased 1.8% since then. The inflation accrual on a TIPS is applied two months after each monthly inflation report. So the calculation for this TIPS is half of February’s rate of 0.547, which is 0.274%, plus 0.71% in March and 0.82% in April. It adds up to 1.804%, and that’s how you get an inflation index of 1.01804).

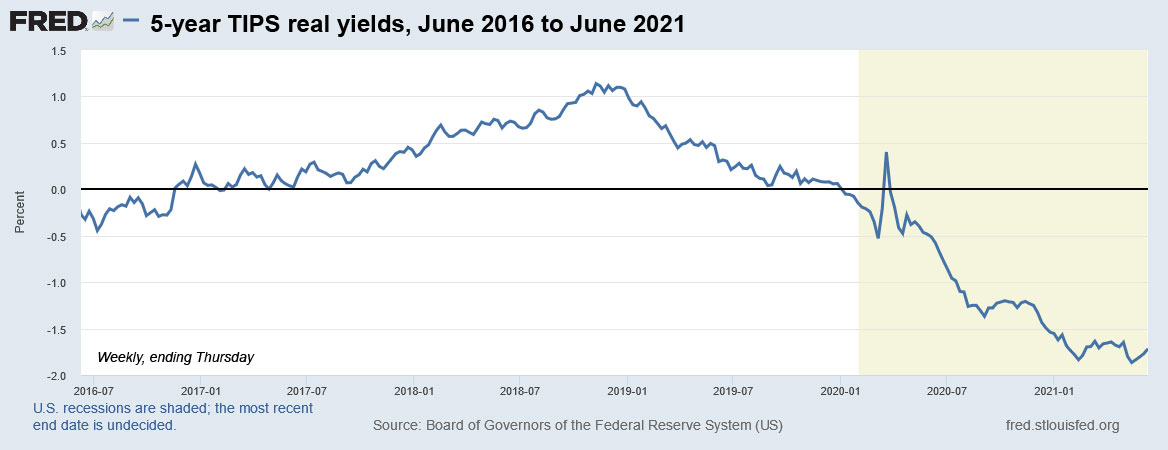

Here is the trend in the 5-year TIPS real yield over the last five years, showing the remarkable move lower after the market mania of February 2020, which triggered aggressive moves by the Federal Reserve to suppress interest rates and by Congress to stimulate the U.S. economy:

So, how could this TIPS look attractive?

Thursday’s auction could result in a record low real yield for any TIPS in history, of any term. And investors will have to pay a large premium, just to under-perform inflation by about 1.73% over the next 4 years, 10 months. How could that look appealing? It can, because this TIPS might be the prettiest ugly duckling in a pond of extremely ugly ducks.

There is only one U.S. dollar investment that is both very safe and guaranteed to match official U.S. inflation over the next five years. That is the U.S. Series I Savings Bond, which carries a real yield of 0.0%, a whopping 173 basis points better than CUSIP 91282CCA7’s current return. But I Bonds come with a purchase cap of $10,000 per person per calendar year. Once you’ve made that purchase, where do you look for a very safe 5-year investment? Five-year Treasury notes? A 5-year bank CD? Both of those options are safe, but look very likely to severely lag inflation over the next five years.

If you think we are likely to have a run of higher-than-typical inflation over the next five years, this TIPS becomes a logical investment amid a bunch of disastrous choices. Here are the numbers under varying inflation scenarios:

Once inflation averages more than 2.53% a year, this TIPS will out-perform a 5-year Treasury note at 0.76% or a 5-year bank CD at 0.80%, currently among the best in the nation. But the Treasury note and bank CD have no upside potential; they are both going to return well below 1% for five years. The TIPS has unlimited upside potential once inflation averages higher than 2.53% a year.

For that reason, I think this 5-year TIPS is an attractive alternative to other safe 5-year investments.

Inflation breakeven rate

With a 5-year Treasury note currently yielding 0.76%, this TIPS would get an inflation breakeven rate of 2.49% if it auctions with a real yield of -1.73%. That means it will out-perform a U.S. Treasury note if inflation averages more than 2.49% over the next 4 years, 10 months. That’s high, but this breakeven rate has actually dipped a bit in the last two weeks.

Here is the trend in the 5-year inflation breakeven rate over the last five years, showing the remarkable surge in inflation expectations after Federal Reserve and congressional stimulus kicked in in March 2020:

A year ago, I would have said 2.49% is a ridiculously high breakeven rate for a 5 year TIPS. A year ago, in May 2020, inflation had averaged only 1.5% in the previous 5 years. This year, after an impressive surge in inflation, that average has risen to 2.3%. I have no idea what the “new normal” is going to look like, but an inflation rate of 2.5% (or higher) in coming years looks like a reasonable bet.

Conclusion

The key question for investors is: When do you think nominal and real yields will begin rising? If you think higher rates are coming soon, waiting to invest makes sense. If you think rates will remain stable or decline further, and you want to lock in inflation protection, an investment in this TIPS is reasonable. I expect demand to be pretty strong under these market conditions.

If you are planning to invest, keep an eye on that Bloomberg Current Yields page until the morning of the auction. Real yields have been volatile in the last week. This auction closes at noon EDT Thursday for non-competitive bids and finalizes at 1 p.m. I will post the auction results soon after the auction closes.

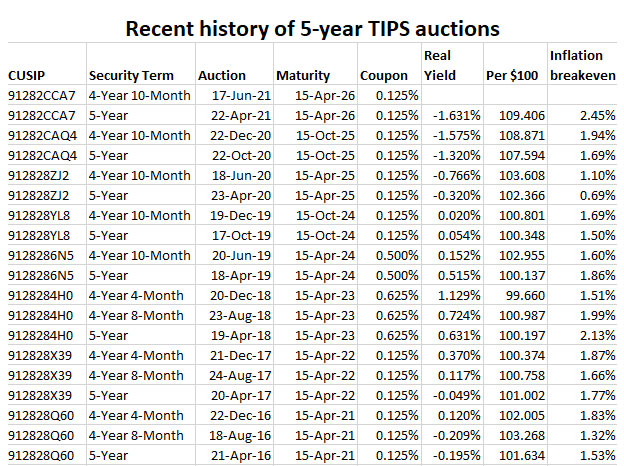

Here’s a chart of recent auction results for 4- to 5-year TIPS:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dear Mr. Enna , How is the DAILY NAV for TIP’s ETF calculated based on the the Monthly CPI and bi-annual resetting of TIP’s ??? Thanks very much .

I believe most (or maybe all) TIPS mutual funds pay out both the coupon payment and the inflation accrual as dividends, so the Net Asset Value tracks the value of the underlying TIPS issues. The VTIP prospectus says this: “Income fluctuations associated with changes in interest rates are expected to be low; however, income fluctuations associated with changes in inflation are expected to be high.” Still, I imagine that the NAV would reflect unpaid dividends, until they are paid.

Thank you so much for your reply.

Much appreciated

On Sat, Jun 19, 2021 at 11:51 AM Treasury Inflation-Protected Securities wrote:

> Tipswatch commented: “I believe most (or maybe all) TIPS mutual funds pay > out both the coupon payment and the inflation accrual as dividends, so the > Net Asset Value tracks the value of the underlying TIPS issues. The VTIP > prospectus says this: “Income fluctuations associated w” >

You said “So the calculation for this TIPS is half of February’s rate of 0.547, which is 0.274%, plus 0.71% in March and 0.82% in April. It adds up to 1.804%, and that’s how you get an inflation index of 1.01804”

That you get exactly the 1.01804 index ratio may make some readers think this is how it is calculated. But yours is just an approximation (a good one). Here is how it is actually calculated:

261.582 CPI Jan 2021

263.014 CPI Feb 2021

264.877 CPI Mar 2021

267.054 CPI Apr 2021

262.25027 Ref CPI 4/15 = ROUND(261.582 + (14/30) * (263.014 – 261.582), 5)

266.98143 Ref CPI 6/30 = ROUND(264.877 + (29/30) * (267.054 – 264.877), 5)

1.01804 Index Ratio = 266.98143 / 262.25027

Click to access A_20210610_4.pdf

Wednesday 8:10 am update: One day from the auction, this TIPS is trading with a real yield of -1.73%, exactly where it was Friday. But the Fed talks will end today, could see some disruption tonight and into tomorrow.

Last post. I promise. Many of us having lived through financial crisis are thinking exactly about this: https://upcomingworldnews.com/analysis-comment/opinion-the-fed-cannot-control-its-easy-money-monster/

My IRMMA message was confusing. According to her, if for example, one had high cap gains year in 2019, Medicare would get my SS AGI info and with a two year look-back in 2021 I’d get hit with IRMMA premium for that high AGI 2019 year. Now it’s year 2022 and Medicare determines they will have a three year look-back. Oh my, Medicare would look-back on 2019 again. I hope the person I spoke with at Medicare was incorrect about this. Can’t understand how one could pay a much higher Medicare premium based upon when Medicare decides to do their next “look-back.”

I’ve never heard of a three-year lookback from Medicare IRMAA and I don’t think that is right. But IRMAA is a very weird and confusing calculation. The current IRMAA charts you see for 2021 (which were issued in November 2020), have a lookback to 2019 income. OK, that means that you have already filed your 2020 return, but you *DON’T KNOW* what the IRMAA levels will be for that 2020 lookback. They will be released in November 2021. in other words, you have to file your 2021 taxes and finalize your MAGI before you know what the actual IRMAA levels will be. Most people don’t understand this. I use the current 2021 levels as a guideline for the probable levels for 2021 income, but those levels won’t be determined and announced until November 2022. Weird, huh?

I wrote about this back in November 2020: https://tipswatch.com/2020/11/15/medicare-costs-will-rise-slightly-in-2021-but-beware-of-irmaa/

Of course delaying SS till 70 is best. If one can. Most in my circle cannot hold-off till 70. Would like to think that SS policy makers would consider the annual AGI of those receiving SS when deciding who would be most negatively affected by cuts. An across the board percentage cut for all receiving SS benefits would not cut it.

Another “gotcha” situation some may find themselves in. The IRMMA premium for Medicare should drop/fall off altogether when individuals AGI falls back down to the lower IRMMA brackets, though I’ve been informed that it could be possible to be hit twice by IRMMA for same singular high AGI year. That is, one could have high cap gains (real estate/investment sales in a single year), and Medicare does their two-year look back. Individual pays their IRMMA penalty for the high AGI year, only to have Medicare decide to do a three-year look back. One can see how if the timing is just right, one could be paying IRMMA premium twice for single high AGI year. I will have to confirm this again, but I received this information when I called SS/Medicare for a neighboe who is now recuperating from a stroke.

One thing I think is a given, a flood more retirees are going to need extended care not paid for by Medicare, and for many individuals/couples without pricey senior medical/estate planning professionals, they will eventually wind-up in overcrowded, understaffed, rundown Medicaid facilities. Destitute and at total mercy of substandard care facility ids not how anyone would choose to live out the last chapter of their life. I have seen much of the latter as I worked in Health & Human Services for decades. For many the term “golden years” is spoken.

BT, you make a lot of good points. Whether Fed intends to or not, it is pushing retired people into riskier assets to seek some sort of return. And of course, immediate income annuities are paying less and less in this low-rate market. Delaying Social Security as long as possible makes sense, since you can benefit by 8% every year you wait, plus it is indexed to inflation. (However, benefits could be cut by 30% around 2030.) If inflation catches fire for years, the situation will get much, much worse.

What a time to be near or just beginning ones’ retirement. For those of us who cannot continue employment due to health reasons or because of time required to attend to family caretaking of parents, these are particularly trying times. Like many seniors, I have watched our total bond index funds returns plummet. Life SPIA payouts are not very good. $200K lump sum gets single 65 year old less than $1000 a month. As most are aware, CD’s and savings accounts at today’s rates are losing money with inflation is factored in. The Fed’s not purposely driving retirees to take-on more risk in their retirement investments, but that is net result of rising prices on staples and near-zero bond returns. I am not one who views “alternatives” to bonds such as cryptocurrency, private loans and farmland as suitable alternatives to bonds. Would like to see the $10,000 I-Bond cap raised to $20,000 for those over 60 with AGI under $50,000 as single and $100,000 as couple. Won’t help with the insane cost of long-term care for those that wind-up in that web, but for other seniors of modest incomes, it just makes sense to squirrel away more dollars that keep up with inflation for our advanced senior years if we are so blessed to have reach advances age.