Hint: It won’t be a thing of beauty. But investors may snatch it up.

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer $16 billion in a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CCM1. The coupon rate and real yield to maturity will be determined by the auction result.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or in this case, below) inflation.

This is a new TIPS, and auction results for new issues can be a little more complicated to predict. After all, there will be $16 billion in new supply entering the market. And these TIPS auction amounts have been inching higher as the Treasury requires more borrowing to finance ever-larger U.S. deficits. Here are auction amounts for recent new 10-year issues:

- July 22, 2021: $16 billion

- Jan. 21, 2021: $15 billion

- July 23, 2020: $14 billion

- Jan. 23, 2020: $14 billion

- July 18, 2019: $14 billion

- Jan. 17, 2019: $13 billion

In less than three years, the 10-year auction amounts have increased 23%. At some point, will the offering size grow too large for demand? That’s not likely for now, as the Federal Reserve continues aggressively buying TIPS and other U.S. Treasurys, keeping yields under control.

One thing about Thursday’s auction is certain: The Treasury will set the coupon rate for this TIPS at 0.125%, the lowest it will go for any TIPS.

As of Friday’s market close, the Treasury, on its Real Yields Curve page, was estimating that a full-term 10-year TIPS would have a real yield of -1.02%. That estimate has dropped 15 basis points since July 1. So the yield trend is working against potential investors in this TIPS. And that deeply negative yield — much lower than the coupon rate of 0.125% — will make this TIPS pricey. The adjusted auction price will probably be about $112 for about $100.39 of value, after accrued inflation is added in.

This TIPS will have an inflation index of 1.00387 on the settlement date of July 30. That number, by the way, is a reflection of the extraordinarily high non-seasonally adjusted inflation of 0.80% in May 2021. One month later, in August, the principal balance of this TIPS will adjust 0.93% higher, matching non-seasonally adjusted inflation in June. This two-month inflation trend definitely adds to the appeal of this TIPS.

If CUSIP 91282CCM1 does auction with a real yield to maturity of -1.02%, it will be the lowest yield ever for any 9- to 10-year TIPS auction. The current record low of -0.987% was set in a January 2021 auction.

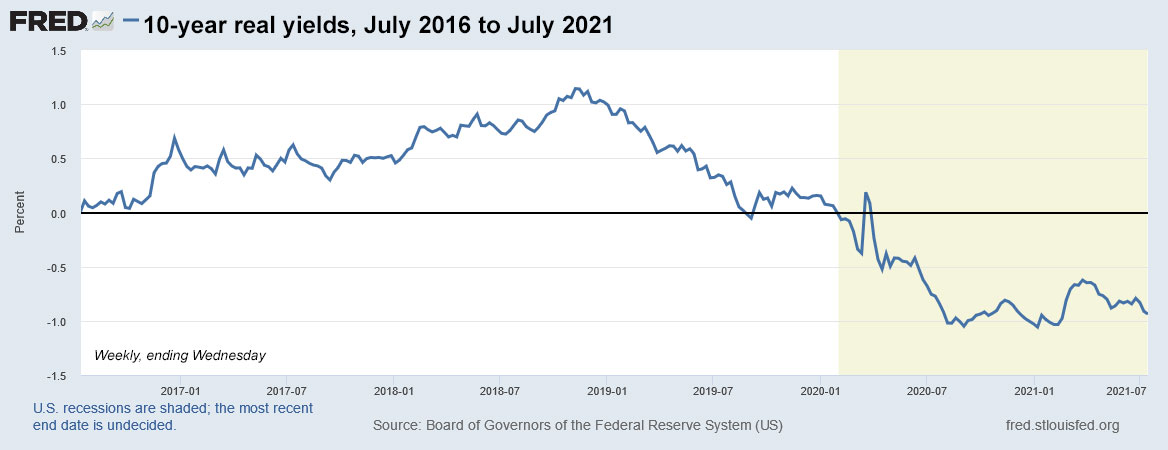

Here is the trend in 10-year real yields over the last five years, showing the deep decline in the period after March 2020, when the COVID-19 pandemic began exploding across the United States. In mid-March, the Federal Reserve began an aggressive program of bond-buying, which has kept both real and nominal yields at extremely low levels.

Inflation breakeven rate

The Treasury is currently estimating the nominal yield of a full-term 10-year Treasury note at 1.31%, which means that if CUSIP 91282CCM1 auctions with a yield of -1.02%, it will get an inflation breakeven rate of 2.33%. That is well off recent highs for this metric, which hit a one-year high of 2.54% on May 17.

A lower inflation breakeven rate makes this TIPS more attractive versus its nominal alternative, and that should increase investor demand for this offering. It’s just a mathematical calculation. At current yields, this TIPS would greatly outperform a nominal Treasury if official U.S. inflation continues at 3% or higher. Here are the numbers:

Of course, this TIPS would also be a loser if inflation doesn’t maintain at an average of 2.33% for 10 years. Over the last 10 years, inflation has averaged 1.9%, so the market is pricing in higher-than-usual inflation over the next 10 years. My conclusion: I am not at all interested in a nominal 10-year Treasury yielding 1.31%. This new TIPS is at least a bit more intriguing, even if it gets a record low real yield.

Here is the trend in the 10-year inflation breakeven rate over the last five years, showing the lofty surge higher after March 2020, when both the Federal Reserve and Congress launched aggressive economic stimulus programs:

I Bonds remain the better alternative

I always feel the need to mention that U.S. Series I Savings Bonds, which currently can be bought with a permanent fixed rate of 0.0%, are a much better investment than a 10-year TIPS with a real yield of -1.02%. The I Bond has a 102-basis-point yield advantage, earns tax-deferred interest and has much better protection against deflation.

I Bonds have a purchase limit of $10,000 per person per calendar year. So if you are interested in inflation protection, I recommend purchasing I Bonds first, up to the limit, and then consider an investment in a Treasury Inflation-Protected Security.

For investors with a longer investment horizon, EE Bonds are also very attractive in our low-rate environment. They have a fixed rate of 0.1%, but will double in value if held for 20 years, giving them a return of 3.5%. But they have to be held 20 years. If that is reasonable for you, they are a strong investment today. A 20-year nominal Treasury is yielding 1.86%, so the EE Bond has a yield advantage of 164 basis points. EE Bonds also have a separate purchase cap of $10,000 per person per calendar year.

Conclusion

I probably won’t be an investor in this new 10-year TIPS, but I will be watching the Treasury’s Real Yields Curve page to see if yields are surging higher. I can see the appeal for an investor who believes real and nominal yields aren’t likely to rise dramtically in the mid-term future. In fact, if you believe real yields are heading even lower, this TIPS is an attractive investment.

I will be reporting the results soon after the auction closes at 1 p.m. Thursday. Non-competitive bids have to be made before noon.

Here is a history of recent TIPS auctions of this term:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thursday 7:30 am update: Yesterday the Treasury’s estimate of the real yield of a full-term 10-year TIPS rose to -0.98%, which would put this auction very close to the record low of -0.987% on Jan 21, 2021. That auction had an adjusted price of $111.64, but this one will have a bit more accrued inflation.

Hi David. Thanks for your commentary about this auction, as well as about the other inflation-related topics you cover. I find the information extremely valuable. I’ve been curious about one aspect related to these TIPS auctions, though, and I hope it’s not a dumb question. What is the formula for deriving the purchase price, in the case of this 10-yr TIPS $112, based on the expected .125% coupon and -1.02% real yield (as of the date of your writing)? I note that the real yield has ticked down to -1.03% as of day-end yesterday. Thanks very much.

Hello, I appreciate your kind words. Now that you have posted an initial comment, your comments will go up immediately. On the purchase price: The coupon rate will be 0.125% and the real yield will probably be around -1.03%, leaving a 1.15% shortfall to create the premium price. We’ve never had a 10-year TIPS with a negative yield so low. On Jan 21, the yield was -0.987%, resulting in an adjusted price of $111.64. That same TIPS is now trading on the secondary market at -1.03% and a price of $111.55 for $100 of value. Add in accrued inflation and you can easily get to $112.

Thank you!

I just found your website this morning. Perfect! Twenty years ago when I retired I took a leap – I created a 10 year TIPs ladder; it has done its job. Several years ago I stopped rolling over my 10 year TIPs. At age 77 I feel I need to disassemble the lader, which is inside my IRA, to avoid being forced into pre-maturity redemption of my TIPS to feed my RMDs. I do not want to gamble with the TIPs market. I am now digesting TIPs funds (eg data on my 20 year old $1000 purchase of VIPSX) and how to use them as an alternative to CDs. Your blog is helping me understand how “when you buy TIPs bond funds does matter” a lot. I think I will hold off 6-12 months, hold my free cash, and not join what I see to be current a “inflation lemmings” rush. The Fed will have to inch rates back up.

Hi Nick, welcome aboard. In the last year I finally moved my remaining 401k assets into a Vanguard traditional IRA, and I will be buying my TIPS there (only made one small purchase so far, last month’s 5-year). I’m letting my TreasuryDirect holdings mature out and so far I’ve used the proceeds to buy I Bonds each year. In that IRA I do own SCHP and VTIP, and I will sell some SCHP each time I buy a TIPS, which I will then hold to maturity. This week’s auction doesn’t look very attractive, unfortunately, yields are falling again today. But there are six auctions a year for this maturity.

No problem in having cash, especially as we get a bit “older”!

Hi David, do you recommend buying EE Bonds on the last day of the month — e.g., Fri July 30 2021, then redeeming on the first day — e.g., Mon July 1 2041? Will the bonds double in value using that strategy? Thank you! I always enjoy reading your articles and find them very useful.

I generally don’t recommend buying on the very last day of the month, just to make sure TreasuryDirect gets the sale through in the correct month. So for this month, I’d probably set the purchase date to Wednesday, July 28, or Thursday, July 29. Then there is at least one additional business day to complete the purchase.

With EE Bonds, the exact date doesn’t matter much, since this will be a 20-year holding. This strategy comes into play more for I Bonds, which can be sold 11 months later (plus a couple days) using this strategy.

I put my orders in last night.