You don’t seriously think I have answers, right? Just some ideas.

By David Enna, Tipswatch.com

What the heck was I thinking? A couple weeks ago, I started on a trek to review Federal Reserve actions and bond market reactions for the period of 2013 to 2021. My theory was that in July 2021, we are sitting on the edge of change, just as we were in June 2013, when the Federal Reserve “announced” it was “planning” to cut back on quantitative easing, its aggressive bond buying program.

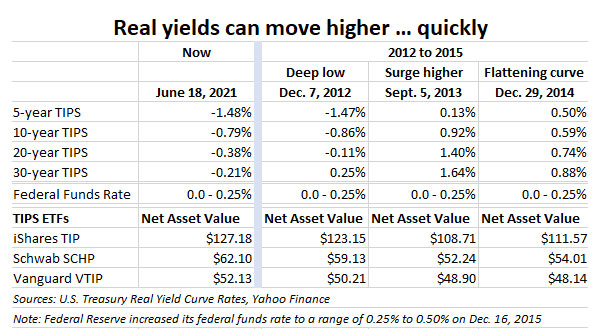

Back in mid-June I created this chart for a similar article looking toward future Fed actions. I think it is remarkable how close real yields were in December 2012 to those of mid-June 2021. The surge higher in 2013, which was very strong, only took about 10 months, and it made the 2013 the worst year for bond funds in the last 10 years.

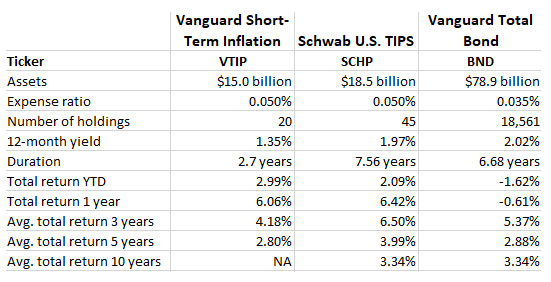

I thought it would be worth taking a year-by-year look at how my three favorite bond ETFs — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed during this time of financial change. These are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a recap of their basic statistics and performance.

Shifting focus back to 2013, it’s important to stress that the Federal Reserve didn’t actually do anything in that year. Because of ensuing market turmoil, the Fed delayed tapering of bond buying until January 2014. Nevertheless, 2013 was a disastrous year for the bond market, with a “taper tantrum” causing both real and nominal yields to soar 100 basis points or more. Is that where we are heading in 2021, now that the Federal Reserve has announced it is “talking about talking about” tapering its current bond-buying stimulus?

So far, at least, the financial markets don’t think so.

2021: So far, so good

In the first half of 2021, as the COVID-19 pandemic slowly wound down, financial markets took a breather. Bond yields were up, but not dramatically. The stock market was up — strongly — with the S&P 500 registering a total return of 17.8% in 2021, through June 30. Inflation is also surging, hitting an annual rate of 5.4% in June, the highest rate in 13 years.

The one nagging point came June 14, when Federal Reserve Chairman Jerome Powell said this at a news conference:

“But you can think of this meeting that we had as the talking about talking about meeting, if you like. And I now suggest that we retire that term, which has served its purpose well, I think.”

Powell said, in essence, that the Fed is now willing to talk about future tapering of its aggressive program of buying U.S. Treasurys and mortgage-based securities in support of the U.S. economy. We don’t know when the bond buying will end, or how quickly it will end, but it is now on the table. In addition, increases in short term interest rates could begin in late 2022 or 2023, a year earlier than had been expected.

That one statement should have been enough to set off at least a mini “taper tantrum,” but after a day or two of market unrest, the financial markets continued in happy bliss, with the yield on a 10-year nominal Treasury dipping 9 basis points in the month after Powell’s statement.

It is clear that the markets don’t believe any tapering of the Fed’s bond buying is likely in the near future, and that any increases in short-term interest rates are at least 18 months away. And the markets are probably right. Powell’s statement on June 14 was the first step in a months-long campaign to prepare the markets for the eventual tapering and then end to the bond-buying program.

One thing I have learned in this nine-article review of Fed history is that the Fed is very slow to reverse “easing” financial actions, and very quick in reversing “tightening.” So in 2021 we have entered at holding pattern, with inflation and the stock market surging, and the bond markets remaining relatively calm, so far. Here is a snapshot of the bond market in 2021:

Notice that real yields have been rising at a slower pace than nominal yields, which indicates the market is pricing in higher inflation expectations. Rightly so, since annual U.S. inflation has surged from 1.4% in January to 5.4% in June. In this scenario, you can expect TIPS funds to outperform nominal funds of similar duration.

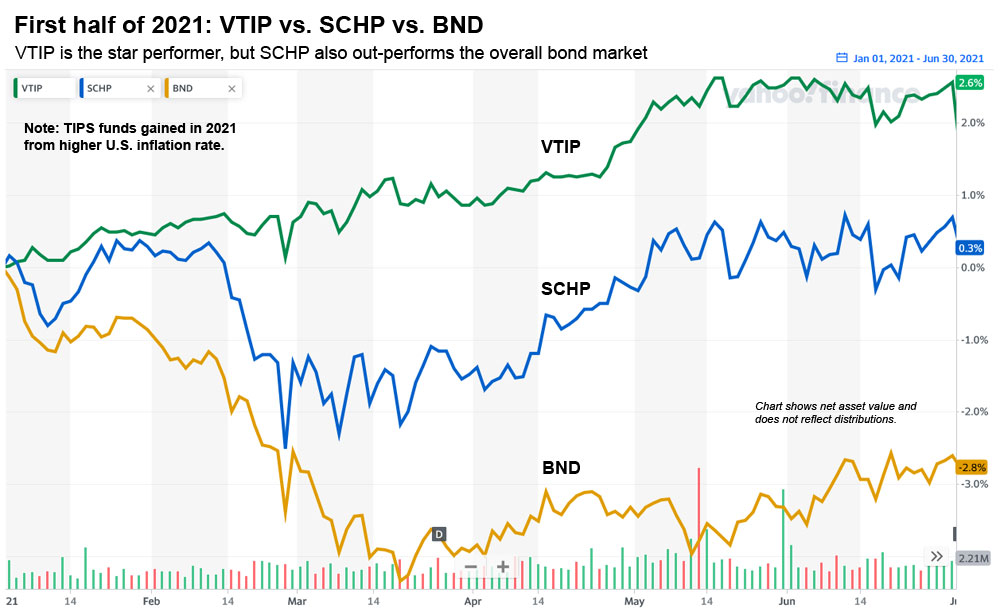

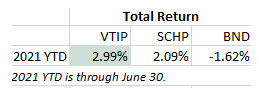

Here is how our three bond ETFs performed in the first half of 2021, with the chart showing net asset value and not including distributions:

Vanguard’s VTIP fund, with its lower duration and gains from the inflationary surge, has been the top performer, despite the higher real yields. Schwab’s U.S. TIPS ETF has also performed well, aided by inflation accruals. The total bond market, BND, has lagged because its underlying nominal rates can’t overcome the effects of higher nominal rates.

All in all, though, 2021 has been a ho-hum year in the U.S. bond market. Will that continue? Well ….

Beyond 2021: Where are we heading?

OK, now we begin the pure speculation portion of this article. I can only describe my “gut feelings,” which tend to be right about as often as they are wrong. What is ahead? This speculation is based on the pandemic fading away and the U.S. economy avoiding any serious financial shocks.

- The Fed will begin tapering its bond buying. If inflation continues to surge higher, remaining well above 5%, I’d guess this could happen in 2021, but more likely it will be early 2022. If the economy remains stable, bond-buying should end six months later. But the Fed will continue to hold a huge supply of U.S. Treasurys and mortgage-backed securities.

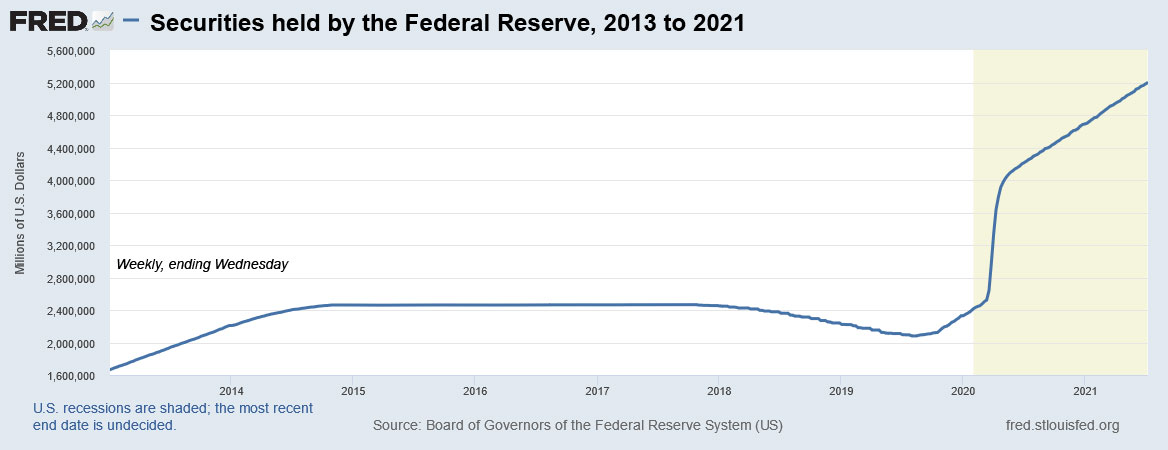

Here is a look at how the Federal Reserve has increased its total assets from 2013 to June 2021, showing how dramatically larger the 2020 bond-buying program has been versus the pre-2013 purchases, which continued through December 2014:

Investors should recognize, and the Fed would readily admit, that the Federal Reserve is manipulating the U.S. Treasury market. For example, examine the New York Fed’s purchase plans for the period of June 14 to July 14, 2021. In that time, the Fed planned to purchase $2.4 billion of 7.5- to 30-year TIPS and $2.0 billion of 1- to 7.5-year TIPS. That’s a total of $4.4 billion for the month, equal to about one-quarter of the value of the reopened 5-year TIPS auctioned in June. This happens month after month, and may actually under-estimate the Fed’s holdings because of reinvestments.

Tapering of Federal Reserve bond purchases is a huge deal.

- The Fed won’t raise short-term interest rates until late 2023. In 2014, the Federal Reserve officially started tapering its bond-buying stimulus in January and ended the bond buying in October 2014. It didn’t raise short-term interest rates above zero until December 2015, 15 months later. So if this pattern continues, rate increases won’t follow quickly after the end of bond-buying stimulus. Expect the Fed to send mixed signals the whole way, but as the rate increase cycle nears, the Fed will give clear signals it is coming.

- The yield curve will flatten once short-term rates begin rising. This is sort of a self-fulfilling prophecy. The end of quantitative easing should cause longer-term yields to rise, expanding the yield curve. But when short-term rates begin rising, the market can lose confidence in economic conditions. So, short-term rates (controlled by the Fed) will begin rising and longer-term rates (controlled by the markets) will begin falling. This ends up supporting the bond market through the early rate hikes.

- Inflation will run higher than 2.5% a year in the mid-term future. The Fed will be highly unlikely to take any tightening action if inflation cannot sustain above 2.5%. So, expect inflation to sustain at that level.

- Eventually, the 10-year real yield should “normalize” to a range of about 0.75% and the 10-year nominal yield could climb to 3% or higher. Maybe this is wishful thinking. But I do think we will again see these yields in the mid-term future. Less than three years ago, in November 2018, a 10-year TIPS reopening auction got a real yield to maturity of 1.109%. Around the same time, the 10-year nominal Treasury was yielding 3.01%.

- The stock market will take a hit along the way. But it won’t necessarily be a disaster. The Federal Reserve has a history of backing up the stock market, acting quickly to intervene at times when stock prices are plummeting. That isn’t going to change. However, the highest-flying, speculative stocks could take a beating if the 10-year nominal Treasury reaches 3% or higher. That opens the door to the “risk off” trade and could bleed money out of the stock market.

However, the market in recent weeks has shown that it does not have any belief that the Federal Reserve will carry through with an end to the bond-buying, forcing the 10-year Treasury yield down to 1.25% recently. From a Market Watch report:

“Traders don’t see the Fed repeating the 2015-2018 hiking cycle, which brought the policy rate band to 2.25%-2.50% in December 2018, and a peak 10 year rate of 3.2% in November 2018, said the strategists. …

“Bank of America doesn’t see a sharp rise in rates such as was seen in the first quarter — driven by positive vaccine surprises and fiscal stimulus — but they see scope for modestly higher rates in the next six to 12 months. “We have not changed our forecast for 10y rates at 1.9% by year-end, but downside risks to our forecast have increased,” (BofA’s Ralph Axel) said.

Selecting the right bond ETF? Don’t even try.

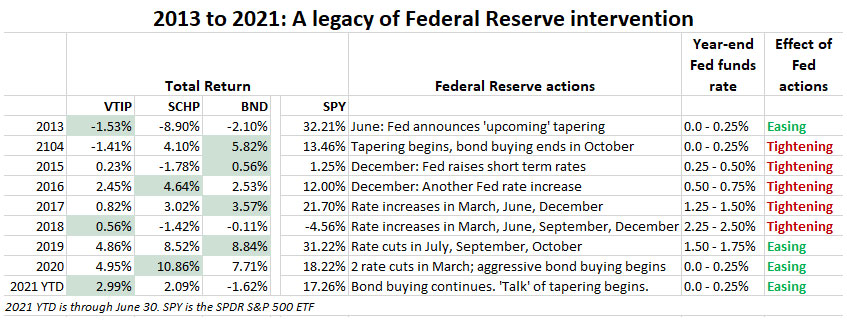

The one thing the 2013 to 2021 era has proven is that there isn’t one “correct answer” when choosing a bond fund. My personal preference is intermediate-term TIPS, combined with Treasury or Treasury-dominated funds with very low expense ratios. Here is a recap of how our three bond ETFs performed through those years, with the addition of the S&P 500 ETF (SPY) and notes on Federal Reserve actions in each of those years:

First of all, please take note of the stock market’s performance during this time of financial turmoil — up 32% in total return in 2013, up 21% in 2017, up 31% in 2019, up 18% in 2020 and up 17% for the first half of 2021. There was only one year — 2018 — when the stock market had a negative total return, and that was only -4.56%. The Federal Reserve’s policies during this period were “very kind” to the stock market, even during periods of tightening. A future period of rising interest rates shouldn’t send the stock market crashing down. (However, high valuations are another matter … )

For the bond funds, I’ve noted the top performer of the three ETFs for each year. VTIP was at the top 3 years, SCHP two years and BND four years. I’d suggest investing in a combination of the three funds: VTIP for the combination of shorter duration and inflation protection, SCHP for longer duration and inflation protection, and BND as an attractive “core” nominal bond fund with very low expenses and an intermediate duration.

Another alternative: Get your inflation protection by buying individual TIPS and U.S. Series I Bonds, and then use BND for your nominal bond allocation. By buying TIPS and holding them to maturity, you can ignore the market swings up and down. But you also lose the chance for a capital gain if real yields decline.

One final conclusion

I am the founder of a website devoted to inflation and inflation protection, and so I definitely have a bias. I am a believer in devoting a portion of your asset allocation to inflation protection. Over the last 10 years, than has been a “losing” philosophy, with inflation lagging well below expectations during that decade. Today, inflation is much higher than expectations.

I don’t know where inflation is heading. I don’t think the Federal Reserve can say where it is heading with much confidence, either. For people in retirement, inflation can be devastating. TIPS and I Bonds provide some reassurance, even if their performance can be underwhelming.

Inflation protection helps me sleep at night. But that’s just me, and this ends my “speculation” on the future.

Coming soon: I’ll take a stab at projecting the Social Security COLA for 2022

Coming soon: Is the Treasury likely to raise the I Bond’s fixed rate in November?

This full 9-article series:

- 2013: A year of surging real and nominal yields

- 2014: The deck was stacked against TIPS funds

- 2015: The Fed actually did something!

- 2016: Inflation rises; TIPS out-perform the overall bond market

- 2017: ‘The calm before the storm’

- 2018: Did the Federal Reserve go too far?

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you for your “speculation” on the future, a series of very informative articles. Most important is, hope we are in it, i.e. “the future”, for awhile anyway.