- All-items inflation for July came in at 0.5% and 5.4% for the year.

- The Social Security COLA is still on track for about a 6% increase.

- I Bonds could get a variable rate of 6% (or higher) for six months.

- TIPS principal balances continue rising at a brisk pace.

By David Enna, Tipswatch.com

The U.S. Bureau of Labor Statistics released its July inflation report this morning, and for the first time in awhile, economists’ inflation estimates were pretty much on target, after months of under-estimating the recent surge in U.S. inflation.

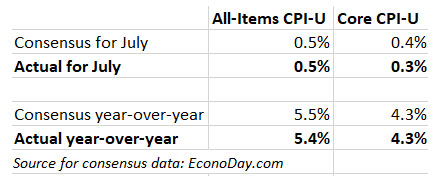

The facts. The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.5% in July on a seasonally adjusted basis, the BLS said. Over the last 12 months, the all-items index increased 5.4%. While 0.5% indicated brisk inflation, the July number was well below the 0.9% inflation recorded in June. The July numbers came close to the consensus estimates, so they shouldn’t cause a market surprise this morning.

Core inflation, which removes food and energy, rose 0.3% in July, a bit below the consensus estimate of 0.4%. But year-over-year core inflation was 4.3%, matching the estimate. This was the smallest monthly increase in core inflation in four months. But, no surprises.

The report disclosed some disturbing trends in the prices of consumer “basics.” For example, the price of food increased 0.7% in July and is now up 3.4% year-over year. Gas prices surged 2.4% higher and are up 41.8% for the year. Shelter costs rose 0.4% in July, and are up 2.8% over the last year.

On the other hand, prices for used cars and trucks — a major trigger for higher inflation over recent months — rose only 0.2% for the month, after rising 10.5% in June. The index for new vehicles rose 1.7% and is up 6.4% for the year.

The index for motor vehicle insurance was one of the few major component indexes to decline in July, falling 2.8% after rising in each of the last 6 months. The index for airline fares fell slightly in July, declining 0.1% after rising sharply in recent months.

Here is the 12-month trend for both all-items and core inflation, showing the strong surge higher since February, as economic stimulus continued at a brisk pace while the U.S. economy was reopening:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For July, the BLS set the inflation index at 273.003, an increase of 0.48% for the month and 5.4% over the last 12 months. This was the seventh month in a row that non-seasonally adjust inflation ran higher than 0.40%.

For TIPS. The July inflation report means that principal balances for all TIPS will increase 0.48% in September, following increases of 0.90% in July and 0.93% in August. In September, principal balances will have increased 5.4% over the previous 12 months, a lofty number. Here are the new September Inflation Indexes for all TIPS.

For I Bonds. The July inflation report was the fourth in a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on November 1. As of July, non-seasonally adjusted inflation in that four-month period ran at 3.07%, which would translate to an annualized variable rate of 6.14% for all I Bonds for six months. Obviously, that would make I Bonds an extremely attractive investment, but keep in mind that two months remain and inflation can be quite finicky in the summer months.

Here are the data so far:

You can find a lot more information on I Bonds on my “Inflation and I Bonds” page, where I track all the monthly inflation updates.

What this means for the Social Security COLA

The July inflation report is the first of three — for July to September — that will set the Social Security Administration’s cost of living adjustment for 2022. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For July, the BLS set CPI-W at 267.789, an increase of 5.4% over the last 12 months. But remember, it will be the average of July to September inflation indexes — compared to the same three-month average a year ago — that will determine the Social Security COLA. In a recent article, I had predicted a COLA increase in the range of 5.8% to 6.2%.

At this point, the data are pointing to a 5.7% increase in the Social Security COLA, but that will rise if inflation continues to surge in the next two months. Here are the numbers so far, with the July inflation report setting the first of three data-points that will determine the COLA:

What this means for future interest rates

Because U.S. job growth seems to be surging and inflation is running much higher than the Federal Reserve’s target of “maybe 2.5%,” the Fed governors are pondering a tapering of their $120 billion in bond purchases a month. But I think an announcement of a future tapering date is still a few months away, and then we’ll see how the market reacts. In theory, medium and longer-term interest rates should rise, as they did in 2013.

Any increase in short-term interest rates is probably a year off, I’d guess.

The huge unknown factor is the effect of the delta variant of COVID-19 on the U.S. economy. If the current surge slows down, as it has in Europe, then it’s possible the economy will continue running very hot. That would force an earlier Fed action. But too much is unknown. Right now, with the 10-year Treasury yielding 1.34%, the market doesn’t seem to fear Fed tapering.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

what did you think of the PPI report and what are the short-term implications (if any) for the CPI?

I don’t follow PPI much, but I saw that the Producer Price Index was up 1% in July and 7.8% for the year. That was the largest increase on record. Even without food and energy, core PPI was up 1% in July. That tells me that the economy is starting to bake-in future inflation, which might mean inflation won’t be as transitory as the Fed believes.

SS COLA gives a bit, Medicare premium hikes take a bit..

Thanks again for a great article, and your predictions for rates.

Hi, David. Thanks for the update. I’m probably wrong but this period of the year seems to be typically benign for inflation. From a COLA and I-bond perspective, part of me hopes for a higher inflation print for the next 2 months but suspect once they remove food and energy we may see some sideways movement or small drops from July’s number.

Every summer is different. We often have surprises, such as a hurricane knocking out oil refineries in 2017, cause a big one-month surge. This year, drought conditions could send food prices higher. (CPI-W does include food costs.) But the reverse can happen, too. I have been expecting gas and used car prices to top out and maybe decline a bit.

Last year, inflation was fairly mild in August (0.32%) and September (0.14%), after a 0.55% increase in July. So the next two months have easier comparisons.

My fingers are crossed in anticipation