Let’s take a deep-dive look at my three favorite bond funds: VTIP, SCHP and BND

By David Enna, Tipswatch.com

A couple weeks ago I wrote an article on the possible path of TIPS and TIPS funds as the Federal Reserve begins considering, then eventually implementing, a tapering of its $120 billion a month in bond purchases, followed by gradual increases in short-term interest rates.

You can read that here: When the Fed begins tapering, what will happen to TIPS? So far, the Fed’s “talking about talking about” statement has had only a minimal effect on the TIPS market. It triggered a nice result for the June 17 reopening auction of a five-year TIPS, which produced a real yield to maturity of -1.416%. The yield on that TIPS has now fallen to -1.70%, so in reality, the bond market is reacting to the Fed’s statements with a yawn.

But I still believe that unless the pandemic strikes again with a vengeance, the U.S. economy will continue to improve and the Fed will have to carry through with tapering of its bond purchases and eventually — maybe 18 months from now — will begin increasing short-term interest rates. U.S. inflation will be a key factor. If it continues to run anywhere near the current rate of 5.0% later in the year, the Fed will have to speed up the process.

And that means the bond market patterns of 2013 to 2016 and beyond could be duplicated as the Fed unwinds its easy money policy. I thought it would be worth taking a year-by-year look at how my three favorite bond ETFs — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed over the last decade.

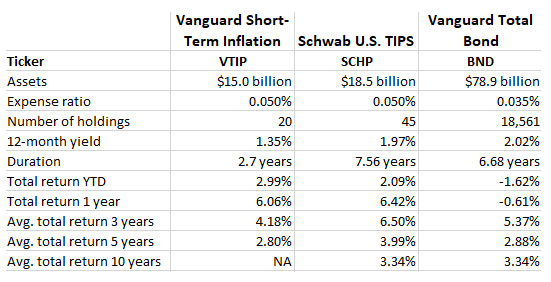

These are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a recap of their basic statistics and performance:

Note that the Total Bond Fund is much more diversified than the TIPS funds, which are focused on a single, esoteric type of Treasury investment. For that reason, I consider it a better “core” bond fund. The Schwab TIPS fund has the longest duration, and is therefore going to be the most volatile in times of interest rate shifts. VTIP lessens that risk (and potential gain) by focusing on TIPS maturing in 0 to 5 years. It launched in mid-2012 and therefore does not yet have a 10-year average return.

I’ll be posting an article a day in the coming week focusing on each year, 2013 to 2021. Today we’ll start with 2013, an epic year in recent bond-fund history.

2013: A year of surging real and nominal yields

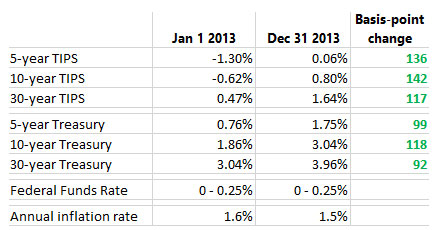

The year 2013 was crucial in the unwinding of the Federal Reserve’s earlier-era quantitative easing efforts. In June 2013, Fed Chairman Ben Bernanke announced an upcoming “tapering” of some of the Fed’s QE policies, but because of ensuing market turmoil the tapering was pushed back to January 2014. But for the market, the path was clear … interest rates were going to rise. The result was a “taper tantrum” that pushed both real and nominal interests rates substantially higher throughout 2013.

Note that the Federal Funds Rate — the Fed’s key short-term interest rate — remained at nearly zero throughout the year, but both real and nominal interest rates rose 100 basis points or more … substantially more for TIPS. This is the “nightmare” scenario for TIPS: Sharply higher interest rates combined with subdued inflation. Here is the result for the three ETFs:

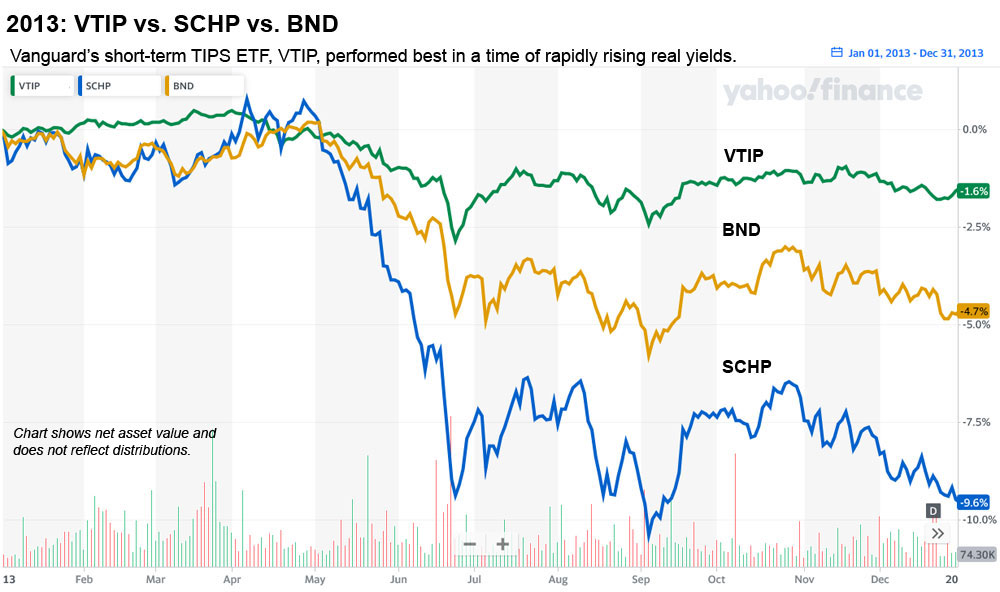

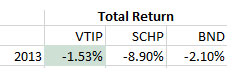

Because of its shorter duration, VTIP held up the best in 2013, while the SCHP’s net asset value plummeted 9.6% before distributions. The chart at the right shows total return, which includes distributions. VTIP was a good performer in a very bad year for bonds.

Conclusion

In a time of rapidly rising interest rates, a shorter duration lessens a bond fund’s interest rate risk. VTIP did reasonably well (meaning not horribly) in 2013 even though Treasury yields surged more than 100 basis points higher. We could be facing a similar scenario in 2022, so VTIP looks like a solid investment in the near term, especially with inflation surging.

- 2014: The deck was stacked against TIPS funds

- 2015: The Fed actually did something!

- 2016: Inflation rises; TIPS out-perform the overall bond market

- 2017: ‘The calm before the storm’

- 2018: Did the Federal Reserve go too far?

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: 10-year TIPS reopens Thursday: How low can it go? | Treasury Inflation-Protected Securities