Let’s be realistic. It won’t happen.

By David Enna, Tipswatch.com

This is a question I’ve been getting often in reader e-mails: “Dave, do you think the Treasury will raise the I Bond’s fixed rate in November? Should I wait until November to buy?”

Here is my in-depth analysis:

- Could the Treasury raise the I Bond’s fixed rate in November? Yes, it could.

- Will the Treasury raise the I Bond’s fixed rate in November? No, it won’t.

The Treasury does not disclose how it sets the fixed rate on Series I Savings Bonds, and so this leads people to speculate about what’s coming at the next reset, on November 1. This is a very important decision, because the I Bond’s fixed rate stays with that investment until redemption or maturity in 30 years. The fixed rate is combined with an inflation-adjusted rate (I call it the “variable rate” but that’s not the official term) that adjusts every six months, based on official U.S. inflation.

Want to know more about I Bonds? Read this.

An I Bond purchased today will have a fixed rate of 0.0%, combined with a variable rate of 3.54%, creating a composite rate of 3.54% for six months. The fixed rate will be “reset” on November 1, but I’m predicting with 99% certainty that it will remain at 0.0%. Why not 100% certainty? Because the Treasury occasionally does strange things. But I don’t think that’s coming in November. Not under these market conditions.

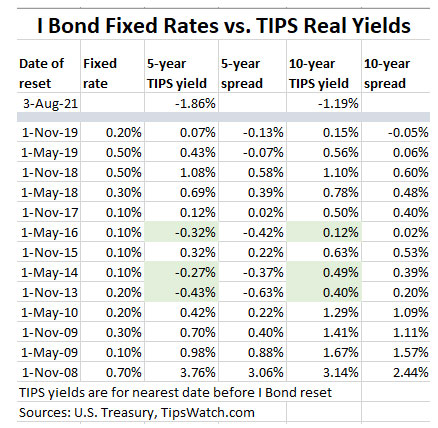

I think the best indicator of a future I Bond’s fixed rate is the spread between the fixed rate and the real yield to maturity of a 10-year Treasury Inflation-Protected Security. Under “normal” circumstances, a 10-year TIPS will have a real yield 40 to 50 basis points higher than the I Bond’s fixed rate. This has varied widely, though, because the Treasury does strange things.

Take a look at this chart, which shows every fixed rate reset for the I Bond where the rate was higher than 0.0%, going back to November 2008.

The important thing to note is that in no case, going back 13 years, has the Treasury set the I Bond’s fixed rate above 0.0% when the 10-year TIPS had a negative real yield. Right now, a 10-year TIPS is yielding -1.19%, meaning that an I Bond with a 0.0% fixed rate has a massive 119-basis-point advantage over a 10-year TIPS.

Remember, under “normal” circumstances, a 10-year TIPS would have a 40- to 50-basis-point advantage over an I Bond. (This is justified because of the I Bond’s flexible maturity, tax-deferred interest and better deflation protection.) Now that situation is reversed, with the I Bond having a 119-basis-point advantage, making the I Bond a much, much better investment. There is no way, under these market conditions, that the Treasury would increase the I Bond’s fixed rate.

But things can change, right?

Hey, isn’t it possible that the Federal Reserve could radically change course and halt its bond-buying stimulus and begin raising interest rates, before November 1, causing 10-year real yields to soar well above zero? (I’ll pause here for laughter.) No, that isn’t going to happen.

I’d expect 10-year real yields to drift a bit before November 1, possibly even rise a bit, but not get anywhere near zero in just three months. So expect real yields to remain negative through 2021, and expect the I Bond’s fixed rate to remain at 0.0%.

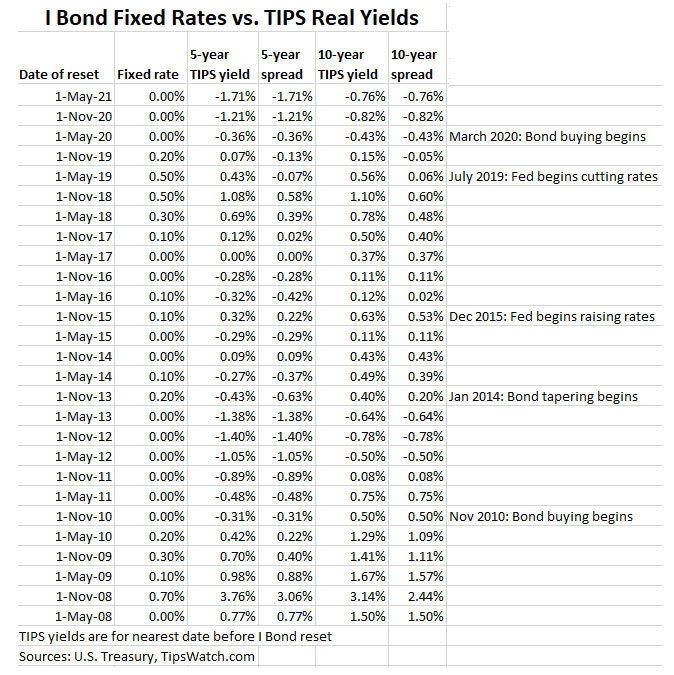

Here’s a look back at the I Bond’s entire fixed-rate history back to 2008, which includes the Fed’s last periods of bond-buying-tapering (beginning in January 2014) and interest-rate-hiking (beginning in December 2015) and the effect these actions had on the 10-year real yield, and the I Bond’s fixed rate:

Note that the Fed’s initial launch into quantitative easing, in November 2010, set off a string of six consecutive I Bond rate resets to 0.0%. During that time, the 10-year real yield dipped well below zero several times at the reset date, and at each of those times the I Bond got a 0.0% fixed rate.

The fixed rate finally rose above 0.0% in November 2013, after a year of market turmoil caused by the bond market’s “taper tantrum.” Up to this point, the Fed had loudly announced its intention to taper, but didn’t actually begin slowing its bond buying until January 2014. It ended in October 2014.

Where are we right now?

At the moment, the Federal Reserve is holding short-term interest rates near zero and is buying $120 billion of Treasurys and mortgage-backed securities each month. We are solidly in a period of quantitative easing, but the Fed is now hinting it “may” begin scaling back its bond-buying “sometime in the future.”

What time in the past matches up our current conditions? I’d say mid-2012, when both the 5-year and 10-year TIPS had real yields deeply below zero. But by November 2013, when the Fed had announced plans to taper its bond buying — resulting in a bond market “taper tantrum” — the 10-year real yield had soared to 0.40% and the Treasury finally raised the I Bond’s fixed rate to 0.2%, up from 0.0%.

The past indicates we are a year or maybe 18 months away from a higher fixed rate for the I Bond, if the Fed carries through with its hints of an end to aggressive economic stimulus. But this Fed seems stubbornly insistent on keeping the stimulus pumping as long as possible. So who knows? But it won’t happen in 2021.

What this means for an I Bond purchase

If I am correct that the fixed rate will stay at 0.0%, I’d say it makes sense to buy I Bonds now to take advantage of six months of the very attractive composite rate of 3.54%. The next variable rate reset in November could be even higher, possibly has high as 6%, but all I Bonds will get that new variable rate for six months, no matter when they were purchased.

Waiting to purchase after November only makes sense if you think the fixed rate will rise. If it doesn’t, you’ll miss out on 3.54% for six months, an extremely attractive rate in our current market.

Looking back at Fed actions. Here is more on this topic, from a series of articles I wrote speculating on possible results of the Fed’s future actions:

When the Fed begins tapering, what will happen to TIPS?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Your advise about timing a purchase is incorrect. The current inflation rate applies FOR THE FIRST SIX MONTHS YOU OWN THE BOND. Direct from gov website.

Hello Tom, yes, as I have consistently said, when you purchase an I Bond you get the current inflation-adjusted rate for six months. From the article: “An I Bond purchased today will have a fixed rate of 0.0%, combined with a variable rate of 3.54%, creating a composite rate of 3.54% for six months.”