The U.S. Treasury will offer $14 billion at auction on Thursday. Who’s interested?

By David Enna, Tipswatch.com

Even as the Federal Reserve is hinting loudly that it will soon begin tapering its $80 billion in monthly Treasury purchases, the real yield of a 10-year Treasury Inflation-Protected Security remains very close to record-low auction levels.

The last time the Fed launched an actual tapering program, in 2013, the real yield of a 10-year TIPS soared 142 basis points in a single year. But today’s investors either don’t care, or don’t believe the Fed has the courage to act.

So that brings us to Thursday’s reopening auction of CUSIP 91282CCM1, creating a 9-year, 10-month TIPS. The originating auction for this TIPS — on July 22, 2021 — generated a real yield to maturity of -1.016%, the lowest in history for any TIPS auction of this term. Its coupon rate was set at 0.125%, the lowest the Treasury will go for a TIPS.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or in this case, below) inflation.

CUSIP 91282CCM1 trades on the secondary market, so you can track its real yield and cost in real time on Bloomberg’s Current Yields page. As of Friday’s market close, this TIPS was trading with a real yield to maturity of -0.99% and a cost of about $111.49 for $100 of par value. The cost is much higher than par value because the real yield to maturity is well below the coupon rate of 0.125%.

In simple terms, investors are willing to pay an 11.5% premium for this TIPS, even though the investment will end up lagging official U.S. inflation by nearly 1% for 9 years, 10 months.

Also of interest is that this TIPS will carry an inflation index of 1.01843 on the settlement date of Sept. 30. That means investors will pay an additional 1.8%, but receive a matching amount of additional principal. At this point, the adjusted price looks like it will be about $113.54 for $101.84 in value, after accrued inflation is added in. But things can change before Thursday.

Here is 2021’s year-to-date trend in 10-year real yields, with the entire year presenting real yields well below zero. The Treasury’s recent hints about tapering have moved real yields slightly higher, but not significantly:

Inflation breakeven rate

With a nominal 10-year Treasury currently trading with a yield of 1.36%, this TIPS has an inflation breakeven rate of 2.35% as of Friday’s close. That is well below the current U.S. inflation rate of 5.3%, but well above the average U.S. inflation of 1.9% over the last 10 years.

I think 2.35% looks like a reasonable number. Here is the question posed by the 10-year inflation breakeven rate: Would you rather invest in a 10-year nominal Treasury paying 1.35% a year, or a 10-year TIPS lagging U.S. inflation by 0.99% a year? If you think inflation will average less than 2.35%, you buy the nominal Treasury. If you think inflation will be higher than 2.35%, you buy the TIPS.

Here is 2021’s year-to-date trend for the 10-year inflation breakeven rate, showing that inflation expectations have leveled off since early summer:

Thoughts on this auction

I think enough big-money investors will decide that a 10-year TIPS remains a decent alternative to a 10-year Treasury note, and demand at Thursday’s auction will at least be satisfactory. But this offering isn’t very attractive for a small-scale investor.

The obvious alternative in September 2021 is the Series I Savings Bond, which offers a real yield of 0.0%, 99 basis points better than CUSIP 91282CCM1. It will accurately track official U.S. inflation, even as this TIPS lags behind by 0.99% a year. So a small-scale investor’s first choice should be I Bonds, up to the $10,000 per person per year limit. After that, consider TIPS when the real yields look attractive (and in September 2021, they don’t).

For more on I Bonds, read this: I Bonds vs. TIPS: What’s the best bet for inflation protection? Also, you can read a primer on my Inflation and I Bonds page.

Investors interested in this auction should continue checking Bloomberg’s Current Yields page to watch for yield shifts. Noncompetitive bids — like those made at TreasuryDirect or a brokerage — have to be placed by noon Thursday. The auction closes at 1 p.m. EDT.

I am traveling this week, but I hope to post the auction results soon after the close.

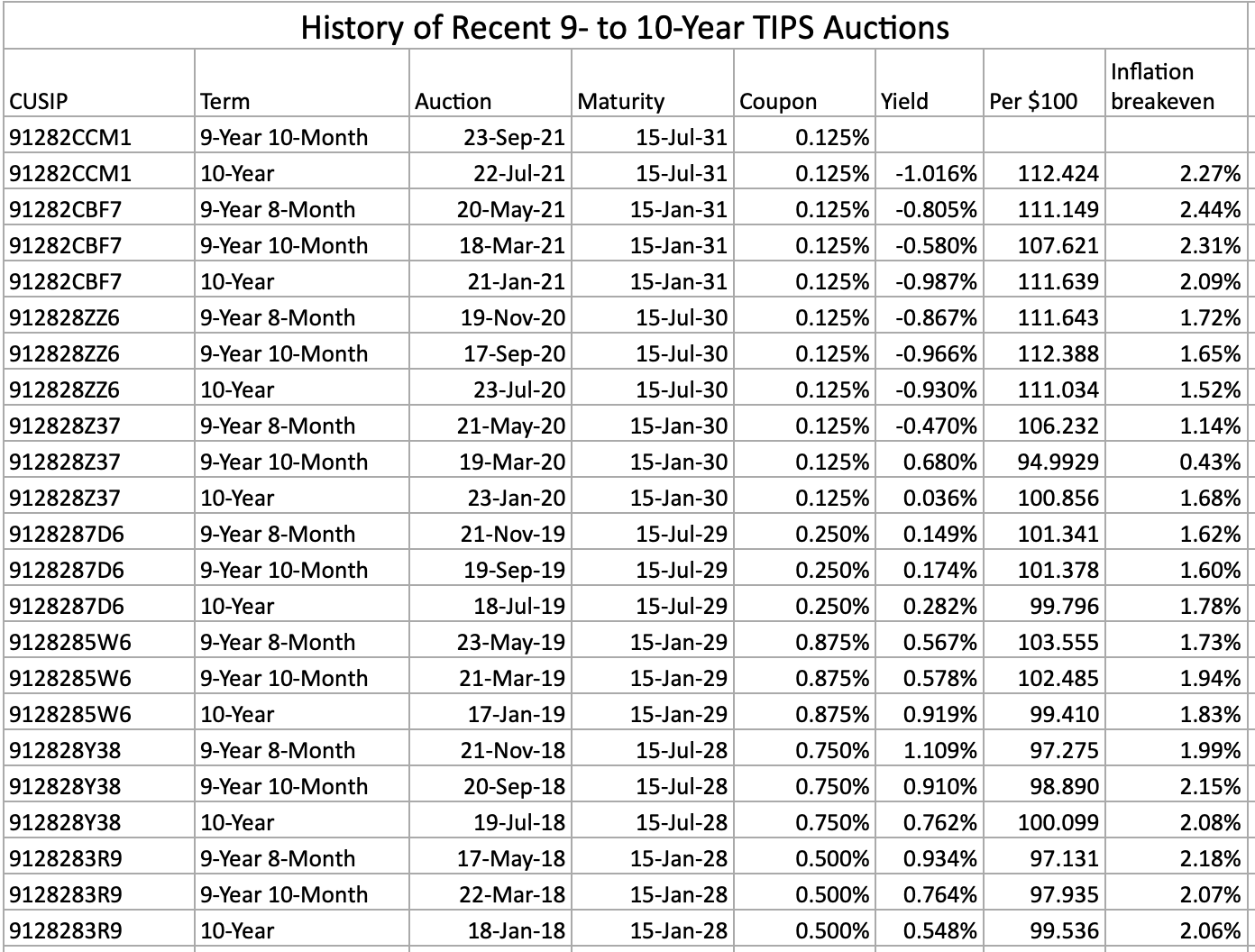

Here’s a history of recent TIPS auctions of this term, showing the depressing string of 8 consecutive auctions with real yields negative to inflation:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Update: At 11:05 am Thursday, the real yield on this TIPS had inched up to -0.92%, a good trend for investors. The base price is now at $110.73.

FYI, at Wednesday’s market close, CUSIP 91282CCM1 was trading with a real yield to maturity of -0.98%, still below the the auction record for a 9- to 10-year TIPS. The price was $111.38 for $100 of par value, but that does not include the inflation accrual, which will bump the adjusted price to about $113.38.

I’ve got a spot in my TIP’s ladder for this ten year note but locking in a 1% discount to inflation doesn’t sound like a good idea to me.