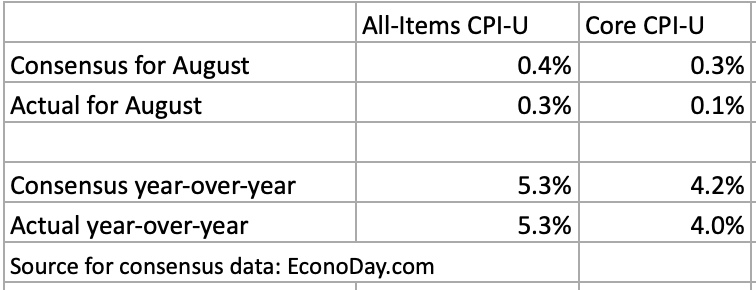

- U.S. inflation increased 0.3% in August, under the consensus estimate.

- At this point, the Social Security COLA will increase 5.8% for payments in January, but one month of data remains.

- The I Bond’s new inflation-adjusted variable rate is on track to increase to 6.56%, annualized, for six months. One month of data remains.

By David Enna, Tipswatch.com

U.S inflation slipped slightly under consensus estimates in September, but remains at a brisk pace throughout the economy.

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3% in August on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 5.3%. The monthly number fell just short of the consensus estimate of 0.4%, but the year-over-year number matched the consensus.

Core inflation, which removes food and energy, increased only 0.1% in August, the BLS reported. That was below the consensus estimate of 0.3%. This was the smallest monthly increase for core inflation since February 2021. Year-over-year core inflation came in at 4.0% for the month, also below the consensus.

The August report shows that inflation continues at a brisk pace across many sectors of the U.S. economy. For example, gasoline prices rose 2.8% for the month, and are up 42.7% over the last year. Some other examples:

- Food prices increased 0.4% for the month and are up 3.7% year over year. The BLS said the index for meats, poultry, fish, and eggs rose 0.7% over the month, which won’t surprise grocery shoppers.

- Shelter costs increased 0.2% for the month and are up 2.8% for the year.

- The costs of medical care services were up 0.3%, but are up only 1.0% for the year.

- The index for used cars and trucks fell 1.5%, but is still up 31.9% year over year.

- The cost of new vehicles rose a sharp 1.2% for the month, and is up 7.6% for the year.

- The index for transportation services fell a sharp 2.3%. One reason: The index for airline fares fell 9.1% over the month.

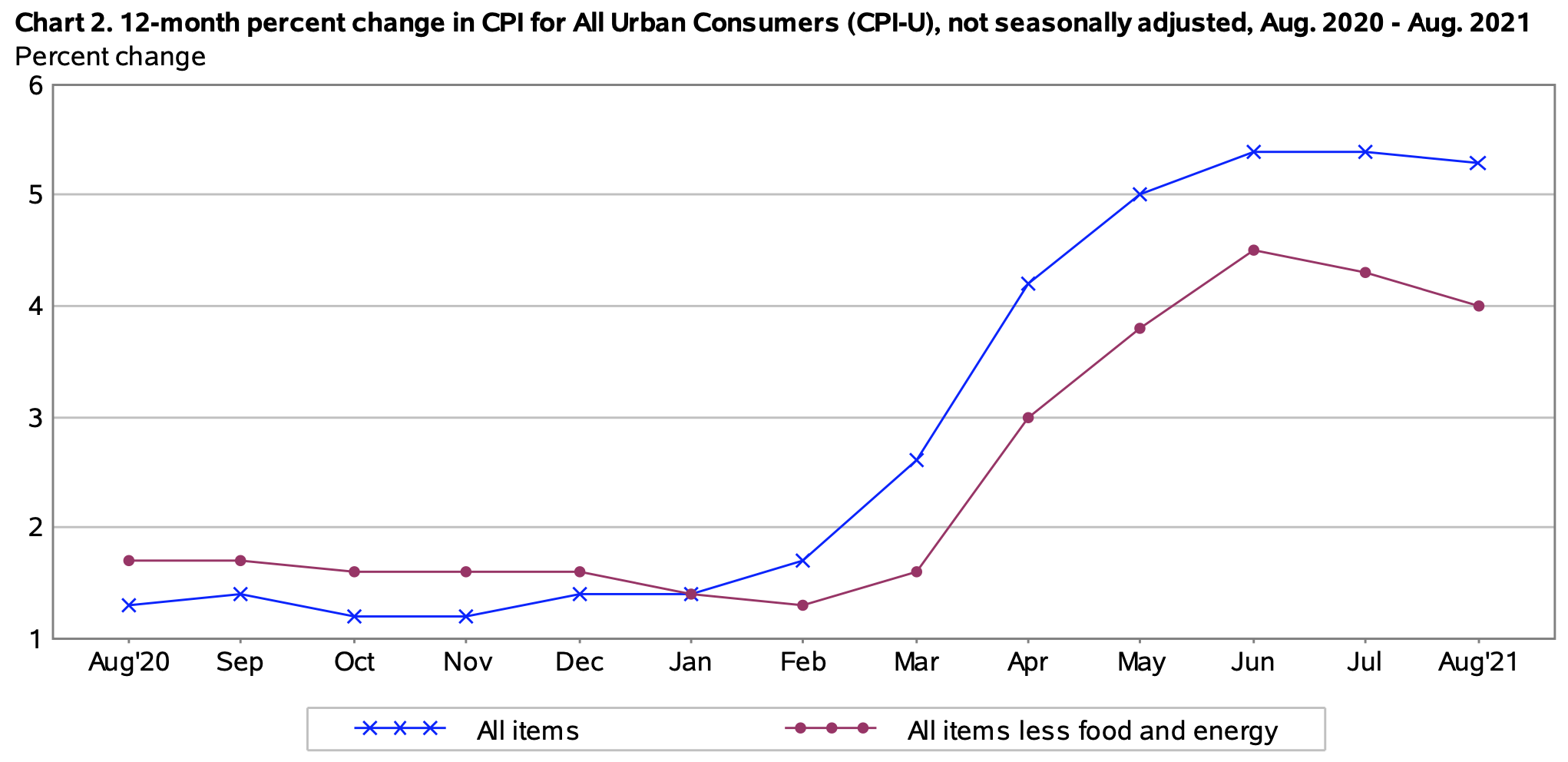

Here is the 12-month trend for both all-items and core inflation over the last 12 months, showing that U.S. inflation seems to be stabilizing at a fairly high level:

What this means for the Social Security COLA

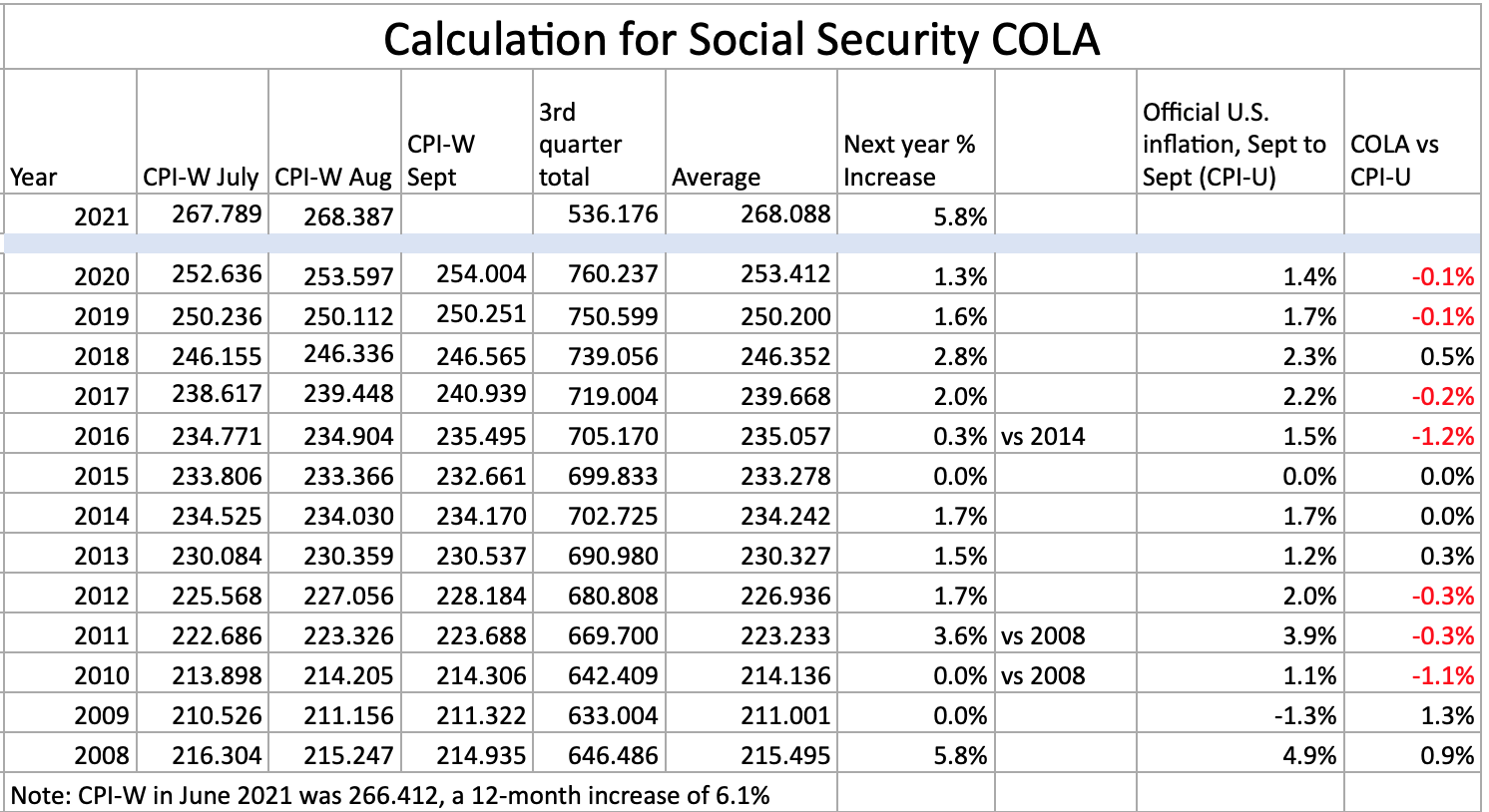

The August inflation report is the second of three — for July to September — that will set the Social Security Administration’s cost of living adjustment for 2022. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For August, the BLS set CPI-W at 268.387, an increase of 5.8% over the last 12 months. But remember, it will be the average of July to September inflation indexes — compared to the same three-month average a year ago — that will determine the Social Security COLA. In a recent article, I had predicted a COLA increase in the range of 5.8% to 6.2%.

At this point, the data are pointing to a 5.8% increase in the Social Security COLA, but that will rise if inflation continues to surge in September. Here are the numbers so far, with one month remaining:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For August, the BLS set the CPI-U inflation index at 273.567, an increase of 0.21% over the July number.

For I Bonds. The August inflation report is the fifth in a six-month string that will determine the new inflation-adjusted variable rate for all I Bonds, to be reset on Nov. 1. At this point, with one month remaining, U.S. inflation has been running at 3.28%, which would translate to a new variable rate of 6.56%, annualized, for six months.

I Bonds are suddenly getting a lot of investor attention, and rightly so with a six-month annualized yield of 6.5% on the horizon. But the biggest benefits will go to those investors committed to purchasing I Bonds every year up to the $10,000 per person per year cap. Newcomers can also benefit: I Bonds purchased before Oct. 31 are likely to have a 12-month return of around 5.0%, 10 times the yield of best-in-nation insured savings accounts.

You can find a lot more information on I Bonds on my “Inflation and I Bonds” page, where I track all the monthly inflation updates and provide a primer on I Bonds. Also, read The I Bond Manifesto, which makes the case for including I Bonds in your emergency fund.

For TIPS. The August inflation report means that principal balances for all TIPS will increase 0.21% in October, ending a seven-month string of increases higher that 0.40%. Here are the new October inflation indexes for all TIPS.

What this means for future interest rates

Today’s inflation report — which came in lower than consensus estimates after months of upside surprises — probably gives the Federal Reserve some breathing room. I think the Fed will continue with its plans to gradually taper down its $80 billion a month in Treasury purchases, but the pressure is off (for a month, at least). A very gradual program of tapering should cause longer-term Treasury yields to rise a bit, but not dramatically, off the currently very low levels.

Any increase in short-term interest rates looks to be 12 to 18 months away.

This morning’s Wall Street Journal headline sums things up well: “Inflation Eased in August, Though Still High.” From that report:

Laura Rosner-Warburton, senior economist at MacroPolicy Perspectives, anticipates the emergence of longer-term price pressures in coming months.

The August CPI report “might be a little bit of a headfake, honestly,” suggesting that the recent inflation surge is proving to be transitory, as economists have predicted, “but other factors might be moving under the surface,” said Ms. Rosner-Warburton.

Inflation continues to run well above the Federal Reserve’s target of 2.0% — or is it really 2.5%? — a year. If this surge in inflation is transitory, the Fed can take its time making repairs. But if it isn’t, actions will be needed. We’ll see in future months.

* * *

Note: I am on the road this week and I’m writing this without my usual setup for calculations and images. Forgive any rough edges and let me know if you see errors.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Many thanks David for another constructive article. I do have a question concerning the fixed rate of I Bonds; namely is that rate related to inflation or not? And what other factors influence the Treasury to set a particular fixed rate?

In November 2018 the fixed rate rose to 0.50% where it remained for twelve months. CPI for 2018 was 2.4% and 1.8% for 2019. Year to date, however, CPI is running about 60% higher than 2018 and about double that of 2019. Yet the fixed rate is expected to remain at zero this November. Of course, the variable rate will increase, but what factors would influence the Treasury to increase the fixed rate in the future? It seems you get a higher fixed rate in periods of subdued inflation.

Thanks, and safe travels.

No, the fixed rate is not directly related to inflation. It is more matched up with the real yield of 10-year TIPS, in my opinion, but the Treasury does not reveal the logic it uses in setting the fixed rate. The inflation-adjusted variable rate accurately reflects U.S. inflation. The fixed rate is meant to track market real yields, and is usually set lower than the real yield of a 10-year TIPS. Since market real yields for 10-year TIPS are currently deeply negative to inflation, the fixed rate is highly likely to remain at 0.0% in November, the lowest it can go.

Thank you for the update, and safe travels.