September inflation numbers should nail down the Social Security COLA at 5.8%+ and set the I Bond’s inflation adjusted rate at 6.5%+, annualized.

By David Enna, Tipswatch.com

Next Wednesday, at 8:30 a.m. EDT, we’re going to get a whopper of an inflation report. That is when the U.S. Bureau of Labor Statistics will release the official U.S. inflation numbers for September, setting in stone next year’s Social Security COLA and the next 6-month inflation-adjusted interest rate for U.S. Series I Savings Bonds.

Both Social Security and I Bonds will be getting historically high numbers: The Social Security COLA should be increasing 5.8% or more for payments beginning in January (the highest increase since 2008), and the next I Bond inflation-adjusted rate should soar to somewhere near 6.9%, annualized That would be the highest six-month variable rate in history. The next highest was 5.7% set in November 2005.

Let’s take a look at what’s coming up in next week’s inflation report.

Social Security COLA

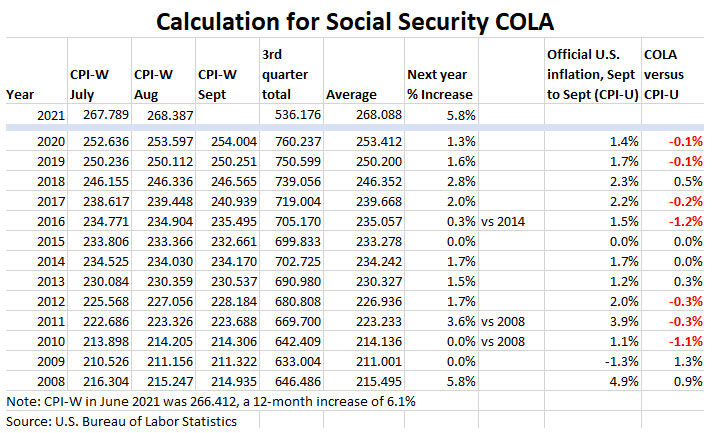

The Social Security COLA is based on an unusual inflation index – CPI-W – and is determined by averaging the indexes for July, August and September and comparing that number with the same average for the year before. For 2021, the COLA was set at 1.3% with the release of the September inflation report on Oct. 13, 2020.

I have been projecting that the 2022 COLA looks likely to fall into a range of 5.8% to 6.2%. The July and August inflation reports have been in line with that projection. At this point, the data seem to point to a 5.8% increase in the Social Security COLA, but that will rise if inflation continues to surge in September’s inflation report.

We won’t know the actual COLA number until the September inflation report is released, completing the data needed for the 3rd quarter average of CPI-W. Here are the numbers so far:

So let’s be conservative and say that CPI-W (technically, the Consumer Price Index for Urban Wage Earners and Clerical Workers) increased by 0.2% in September. That would make the average for the indexes from July to September 268.366, an increase of 5.9% over the average for the same months of 2020. The Social Security COLA then would be set at 5.9% for payments in 2022.

The Social Security Administration currently estimates that the average retired beneficiary receives $1,555.25 a month, so a 5.9% increase would boost that monthly payment to about $1,647, an increase of $91.75 a month. If you are in the Social Security “limbo” period — older than 62 but not yet taking benefits — your future benefits would also climb by this percentage.

However, recipients can also expect that Medicare Part B costs will rise in 2022, which will subtract — at least partly — from the higher benefits. The base premium is now $148.50 a month. I could see that rising to $158 a month, cutting the effect of the COLA increase by $9.50 a month. But this is just speculation.

Also, read this: More details on the complex Social Security COLA formula

Series I Savings Bonds

I Bonds have two components that make up their composite rate (total yield): a fixed rate and an inflation rate.

- The fixed rate is fixed for the entire life of any given I Bond. The fixed rate for newly-issued I Bonds is announced on May 1 and November 1 of each year, and applies to all I Bonds issued during that six-month period. The fixed rate is equivalent to the “real” yield of an I Bond, meaning the yield above inflation. It is currently set at 0.0% and is highly likely to remain at 0.0% at the November reset.

- The inflation rate is based on the Consumer Price Index and is also announced every six months, on May 1 and November 1. The May rate is based on the change in the CPI-U from the previous September to March and the November rate on the change from March to September. This inflation adjustment applies to both existing I Bonds and newly-issued ones, but the timing of that adjustment depends on the original issue date of the I Bond.

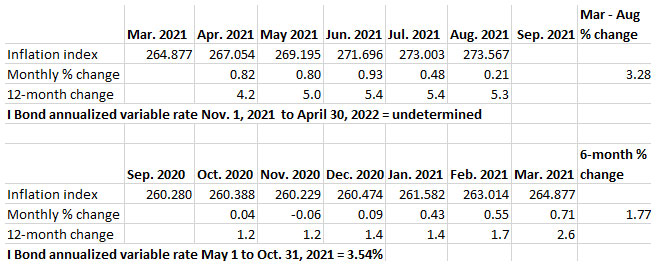

An I Bond purchased before Oct. 31 will have a fixed rate of 0.0% and an inflation-adjusted rate of 3.54%, creating a composite annualized rate of 3.54% for six months.

We have completed five months of the six-month string to determine the next inflation-adjusted rate, which is currently running at 6.56% annualized. If inflation comes in at 0.2% for September (it could be higher), the annualized rate will jump to 6.96% for six months.

The formula used to set the inflation-adjusted variable rate for I Bonds doubles the six-month inflation number, creating an annualized rate of return, which investors get for six months. Here are the numbers so far, five months into the rate-setting period:

If the inflation-adjusted rate comes in around 6.9% it will be, by far, the highest six-month variable rate in the I Bond’s history, dating back to September 1998. There has never been a variable rate above 6.0%.

Purchases of I Bonds are limited to $10,000 per person, per year (plus an opportunity to get $5,000 in paper I Bonds in lieu of a federal income tax refund). So, should you buy before November 1, or after November 1?

I recommend buying before Oct. 31 to lock in the 3.54% rate for six months, and then you will get that close-to-7% rate for the next six months. Starting off with six months at 3.54% and then getting 6 months at 6.9% is super attractive in today’s market.

You have to hold an I Bond for 12 months before you can redeem. The combined rate over the year is going to top 5.2%, about 10 times what you can earn on a 1-year CD. But either way — before or after Nov. 1 — the investment is attractive. Also, keep in mind that the purchase cap resets on January 1, so you’ll be able to make another purchase getting the full six months of near-7% rate.

Also, read this: I Bond Manifesto: Why inflation-linked savings bonds can work as part of your emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It seems Treasury Direct changed their rules and in order to update the bank on your TD account, you have to have some sort of bank guarantee signature (not a normal notary signature) that you get from a local bank. TD sure doesn’t make things easy dealing with them!

Sometimes banks will refuse to do these signature guarantees, which is very annoying. My credit union is my backup, and they will always do it.

Thanks to you I purchased my first I Bond; I have been laddering TIPS for years. Thank you.

Given the I-bond Oct. 31 opportunity… If my Treasury Direct I-bonds are registered as “my name WITH my wife’s name,” can I buy two $10k I-Bonds in the one TD account?

No, you need to have two separate accounts, with each account having a $10,000 purchase cap. One account would be registered to Spouse 1 with Spouse 2, and the other one to Spouse 2 with Spouse 1. More info: https://tipswatch.com/2021/05/09/ready-to-open-a-treasurydirect-account-here-are-some-tips/

David, I read your comment on the MarketWatch October 5th article “This simple investment can earn you more than 6% with no risk” and I asked this question:

“Just to clarify, are you saying that if we buy before Oct 31 we will get 1 month at 3.54% and then the rate will go up to nearly 7% on Nov 1? Is the fact that we can redeem the bonds one month sooner the only significant advantage?”

Based on your article above, I infer that the current I-Bond rate is in effect for six months from the month of purchase. So, if I purchase I-Bonds in late October, the interest will remain fixed for six months at the current rate (3.54%) and then will increase to the new (Nov 1st) rate in April 2022, which will remain in effect for the subsequent six months. Is that how it works?

Yes, that is accurate. If you buy before Oct. 31, you will get 6 months at 3.54% annualized and then a full six months at the new higher rate.

Thanks

I live in NC and was putting our extra cash into NTFIX (the Dupree North Carolina Tax-Free Income Series), which is an NC muni fund that pays 2.06% tax-free but is somewhat volatile. The I-Bonds look like a much better buy since they are risk-free (unless the guvment defaults) and we (me and my wife) won’t need the $20K over the next five years, and I doubt we’ll ever need it before 2051 when the bonds come due. I’ll probably kick in another $20K in 2022 and 2023.

I crunched the numbers on a spreadsheet and the decision to buy $10K now or $10K in November depends entirely on future interest rates (reset in April 2022 and later). It’s breakeven to the penny if the future rates average out to 3.54% over the next five years, which makes sense both intuitively and mathematically.

If the future average rates are less than 3.54% (the current rate), then it’s better to purchase the $10K max now, in October. However, if the future average rates are greater than 3.54% then it’s better to wait until November.

Since the I Bond interest rates are linked to the CPI inflation rate, it all depends on whether one believes that inflation will persist — in which case one should wait until November — or if one believes it will eventually revert to the mean (about 2.1% over the past 20 years). I personally believe that high inflation will persist for the next year or two, at least, but who knows? There could be a deflationary recession. As Yogi Berra said (and before him Niels Bohr), “making predictions is difficult, especially about the future.” So, to hedge my bets, I’ve just now bought $5K and will buy the remaining $5K in November.

Thanks very much your excellent website.

I’d say don’t overthink it. But if you are really stumped, buy $5,000 in October and $5,000 in November. I think buying in October makes sense, but I understand that some people will disagree, and they may end up being right. (But the dollar amounts won’t be enough to change your life, trust me.)

Right, it’s just a hundred dollars either way over five years. Chump change, but I needed to look at the math, as is my wont.

No chance of the fixed rate increasing, even with these inflationary times?

The fixed rate really has nothing to do with the inflation rate. The inflation-adjusted variable rate will already match inflation in the future. The fixed rate is a lot more dependent on the current status of real yields, reflected primarily in the real yield of a 10-year TIPS, which is currently -0.89%. When a TIPS investor is willing to accept -0.89% a year less than inflation for 10 years, the Treasury isn’t likely to raised the fixed rate of an I Bond. More on this: https://tipswatch.com/2021/08/04/any-chance-the-treasury-will-raise-the-i-bonds-fixed-rate-in-november/

Ah, I see. I was missing that part, likely didn’t read it close enough.

Great website. I’m looking at some safer investments for a little excess cash that I have no short to middle term plans with, so these seem a good bet.

Pingback: I Bonds November Inflation Interest rate | Keil Financial

One thing hardly ever mentioned is the importance of automation as we age. If my savings requires “hands on” then there is a definite danger that a loss of my faculties could negatively impact my decisions (not to mention actually having some n’er do well steal them).

Always brightens my day when you post another I-Bond article. Been following you since that seeking whatever site.

Started out as a small emergency fund which morphed into our primary fixed income allocation. Now we have over 12+ years max contributions earning over 6%.

I-Bonds may be boring and perhaps in the end will have not have been as competitive as other options but it sure helps us sleep at night. But for now I can tell all the I-Bond naysayers, told you so…..

Agree with you Rogan M I found a note in a women’s magazine in 2000 and she mentioned I-bonds.No idea what she was talking about but this was a great time to buy, highest rate.

Looked it up and opened up 2 accounts. In that time you could put in 30k per person plus you could charge it to a credit card on which I got 1% back. Glad I did it.

I am so happy to see your email these days. Both Ibonds and Social Security are very much on my radar these days, but I rely on your compilation of data to see where things may be headed. Thanks!

Thanks as always for info. How does this affect TIPS?

TIPS are currently trading with real yields well below zero, so I Bonds have a big yield advantage over TIPS. However, investors in TIPS have gotten the same benefit from the last year’s surge of inflation, with principal balances rising 5.3% over 12 months ending in October.

Another excellent easy to read article (as always). Thank you.

“I recommend buying before Oct. 31 to lock in the 3.54% rate for six months,” Since today is Oct. 6, don’t you mean “lock in the 3.54% rate for 25 days,” ?

No, this is the way I Bonds work: When you purchase them, you get six months of the current composite rate (which is now 3.54%, annualized). After that six months, you get the next composite rate (which will be about 6.9%) for six months. So six months at 3.54%, then six months at about 6.9%.

Thanks for the explanation. So you’re predicting (and your track record is great) that the rate which will be set on May 1, 2022 will be less than 3.54% annualized.

No, I have no idea where inflation will be charting through May 2022. It could definitely be higher, but 3.54% is the highest rate we have seen since May 2011 (when it was 4.6%). It’s an attractive rate when best-in-nation 1-year bank CDs are paying 0.55%. FYI, I bought my I bond allocation in January, when the variable rate was 1.68%. So I got six months at 1.68%, six months at 3.54% and now will get six months at 6.9% or whatever it ends up being.

Thank you, Mr. Tipswatch. How interesting the difference between the i-bond and SS may be. Nearly 1% less for SS recipients if I read your article correctly.

This is because the I Bond rate is based on the inflation rate from March to September (which will be about 3.4% or 3.5%) and the Social Security COLA is based on the average of inflation indexes for three months — July, August and September. Inflation ran hot in April, May and June, but cooled off just a bit this summer. It looks like the COLA will run ahead of overall U.S. inflation, though. It usually doesn’t.

As always thank you for your article. Have been a follower since you were on SA.

hanna

I always appreciate my long-time, loyal readers. Thanks, Hannah!

If I turn 62 in December and plan to apply for Social Security, should I wait to apply until January to be on the safe side?

You will get the 2022 increase no matter when you start collecting, even if you wait a year or two or three. The increase will permanently increase your future benefits. Technically, the 2022 increase goes into effect for the December payment, but recipients don’t receive that payment until January.