Inflation continues at a four-decade high, with costs of shelter, food and gasoline surging.

By David Enna, Tipswatch.com

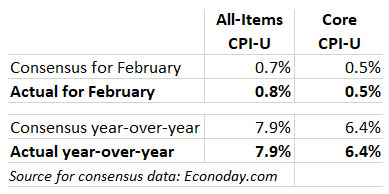

The numbers are ugly, but today’s inflation report mostly matched economist expectations, despite hitting a 41-year high.

The Consumer Price Index for All Urban Consumers increased 0.8% in February on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported. Over the last 12 months, the all-items index increased 7.9%. The monthly number slightly exceeded expectations, but the year-over-year number matched predictions.

Annual U.S. inflation of 7.9% is the highest for any year ending in February since 1981, when inflation soared to 11.4%.

Core inflation, which eliminates food and energy, rose 0.5% in February and is up 6.4% year-over-year. Both these numbers matched expectations.

The BLS noted that increases in the costs many American staples — gasoline, shelter, food and apparel — led the way on price increases. This is a high-pain event. Here are some of the data:

- Gasoline prices increased 6.6% for the month and are up 38% over the last year. Remember, this is the February number, and does not factor in strong increases so far in March. The BLS said gas prices accounted for almost a third of the overall gain in monthly inflation.

- The food at home index increased 1.4% and is up 8.6% over the last year.

- The index for fruits and vegetables rose 2.3%, its largest monthly increase since March 2010.

- The index for meats, poultry, fish, and eggs increased 1.2% in February.

- Shelter costs rose 0.5% in February and are up 4.7% for the year. The BLS said shelter costs accounted for more than 40% of the increase in core inflation. This was the largest 12-month increase in the shelter index since May 1991.

- Apparel costs were up 0.7% in February, after rising 1.1% in both December and January.

- On the positive side, the costs of medical care services rose only 0.1%, and prices of medical care commodities were up a moderate 0.3%.

- Also, prices for used cars and trucks, which had been soaring, fell 0.2% in the month but remain 41.2% higher year over year. Costs for new vehicles rose 0.3%.

Side note: I did a search for the word “largest” in the BLS news release, and I found the document contained that word 12 times, across a broad spectrum of price categories. These are history-making numbers, and March will probably get worse with the sudden, steep surge in gas prices.

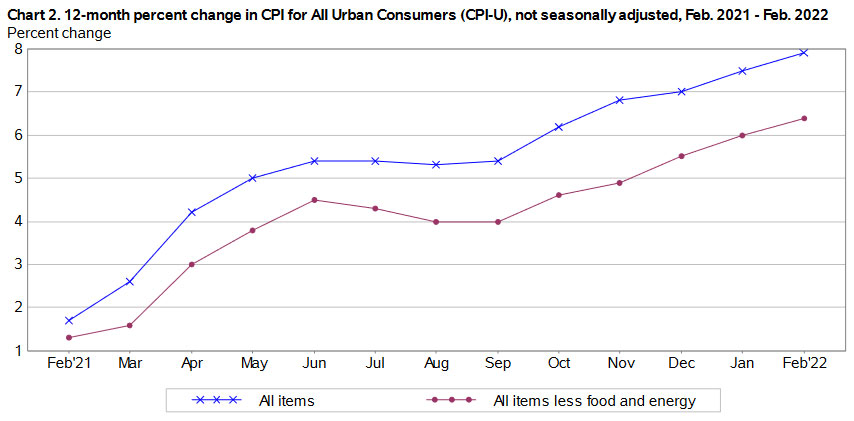

Here is the one-year trend for all-items and core inflation, showing the incredible surge higher. Hard to believe that annual inflation in February 2021 was running at a mundane 1.7%.

What this means for TIPS and I Bonds

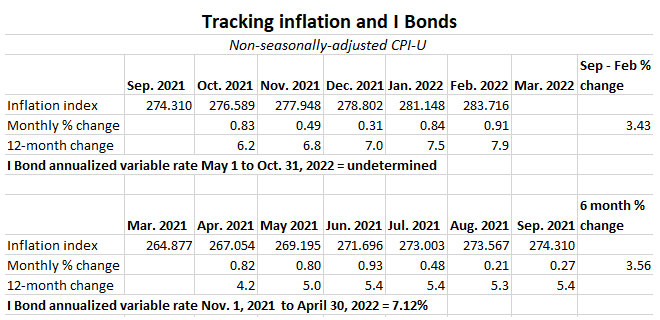

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust TIPS principal balances and set future interest rates for I Bonds. For February, the BLS set the inflation index at 283.716, an increase of 0.91% over the January number.

For TIPS. The February inflation report means that principal balances for all TIPS will be increasing 0.91% in April, following an 0.84% increase in March. For the year ending in April, principal balances will have increased 7.9%, a remarkable — and let’s admit it, unexpected — surge higher. Remember, the reason for investing in TIPS is to protect against “unexpectedly” high inflation. That strategy is working.

Here are the new April Inflation Indexes for all TIPS.

For I Bonds. The February report is the fifth of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on May 1 for all I Bonds. So far, inflation from September 2021 to February 2022 has been running at 3.43%, which translates to a variable rate of 6.86%. One month remains, and March inflation is likely to be quite high. It’s easy to see the possibility of a variable rate exceeding 8% — or even 9% — at the May reset, higher than the current rate of 7.12%.

One factor to consider, however: Non-seasonally adjusted inflation increased 0.71% in March 2021, setting up a rather high number for March 2022 to beat. Gasoline prices rose 9.1% in March 2021 over February 2021. That will lessen the effect of this year’s sudden surge, but only in the year-over-year number. Clearly, gasoline prices have increased in March 2022 over February 2022, and that will push up the March monthly number.

If, for example, non-seasonally adjusted inflation rises 0.9% in March — definitely possible — then the six-month inflation number would be 4.33%, creating a variable rate of 8.66%. If it hits 1.0%, the variable rate would rise to 8.86%.

Does that mean you should wait until after May 1 to invest in I Bonds, which have a purchase cap of $10,000 per person per year? Absolutely not. If you buy an I Bond before May 1, you will earn an annualized 7.12% for a full six months, and then the new variable rate for the next six months. Buying before May 1 — in my opinion — is the way to go.

Here are the numbers so far, which I track on my “Inflation and I Bonds” page:

What this means for future interest rates

While the February inflation report could reasonably be called “shocking,” increases of this level were clearly predicted and should not have much effect on the Federal Reserve’s near-term actions. But I believe the market turmoil caused by the war in Ukraine and surging gas prices will cause the Fed to go the moderate route in raising short-term interest rates.

I think the Fed will raise its federal funds rate by 25 basis points next week, and then continue with 25-basis-point increases at points through the year and next year, eventually hitting a target of 1.50% to 1.75%, up from current level of 0.0% to 0.25%. That’s a total of five rate increases, but who knows.

The March inflation report will be ugly, reflecting the spike higher in gasoline prices and related transportation costs. The threat of recession is at least “looming,” and that should hold down longer-term interest rates as the yield curve flattens. After March, inflation could begin sliding lower, but nowhere near the Fed’s target of about 2.25%.

This insight is from inflation guru Michael Ashton, @inflation_guy on Twitter:

“So wrapping up: there’s no real sign of any ebbing of inflation pressures. In fact, there are some signs that food inflation will stay elevated for longer than the normal oscillation cycle. But we are closer to the end of the spike, anyway, than to the beginning. …

“Core inflation will likely peak next month, and headline inflation in the next couple of months. That’s good. But we’re not going to go back to 2%. Right now, the monthly prints point to an underlying core rate around 6%. I suspect we will end 2022 in the 5s, or high 4s.”

Right now, the only very predictable thing is “uncertainty.”

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you for this website. I am new to I-bonds and TIPS so this information is wonderful. Can you please indicate if you still think it wise to buy I bonds before May with the new April inflation numbers out? I am a little confused as to why I shouldn’t wait until the new higher inflation takes effect in May. Thank you again.

I do believe if you want to be a long-term holder of an I Bond, you should buy before May 1. And here is the rationale, copied from a previous answer:

We don’t know what the next variable rate (to be set Nov. 1) will be, based on inflation from March to September. If you buy $10,000 in I Bonds before May 1, you are guaranteed to get a return of $853 in 12 months. If you buy after May 1, you are guaranteed to get a return of $481 in six months, and then some unknown amount in the next six months. So $481 is your worst-case scenario, while investing before May 1 has a worst-case scenario of $853.

For the May 1 scenario to pay off, the next variable rate would need to be more than 7.12%, obviously, which equates to an inflation rate of about 3.56% from March to September. If it is higher than that number, both the investor who bought before May 1 and the investor who bought after May 1 would benefit, because both would get the new variable rate some time after November 2022. Long-term holders should buy before May 1 and get the immediate 7.12% for six months, then 9.62% for six months, and then all future variable rates.

But, sure, if you are looking to hold the I Bond for only 12 months and then immediately redeem, it could make sense to buy after May 1, because you would be losing three months interest from the unknown second variable rate, which probably will be lower. A buyer before May 1 should hold for 15 months before selling, to get the full benefit of the 9.62% interest for six months.

Pingback: [Repost] US Treasury Bonds Rate Set To 7.12% (I Bonds) - Doctor Of Credit

I already plunked down my $10k for 2022. I know that 2023 is a long ways away (and dependent on Nov’ 22’s final CPI data) but do you think it’s likely that I Bonds will be a good investment into next year?

I like buying I Bonds and holding them for the long term, and so yes, I do think they will be a fine investment in 2023 and beyond. Not as great as they are today, this is very rare. But this is a solid, safe investment.

If the price of crude has crested and is headed back down on a parabolic trajectory (>8% drop today?) we have the makings of a low-fixed-rate IBond owner’s wet dream: super-high variable interest rate in the current semiannual computation period followed by steeply negative variable interest rate in the following semiannual computation period. Unlikely—but we can dream!

That doesn’t look likely, in my opinion, but inflation is going to settle down later this year, probably into the 4% range (my guess). I think a six-month period with a composite rate of 0.0% would frustrate a lot of I Bond holders. (It happened in May 2015, for example). But in reality it is not horrible. 1) It gives you a chance to redeem I Bonds held for less than 5 years with zero penalty, and more importantly, 2) since I Bonds can never go down in value, holders get the full advantage of next leap up in inflation.

The prices of TIPS bonds are also going up, depressing the yield relative to what we were guessing it might drift to “way back” in January. I assume this is driven by more investors paying attention to TIPS. So maybe we will be in negative yield territory for some time? Crystal ball no less fuzzy I guess!

Clark, I have to agree it is depressing to see real yields dropping lower again. Inflation fears are increasing interest in TIPS, obviously. The 5-year real yield has fallen 51 basis points in less than a month. The 10-year is down 47 basis points. This reflects a lot of inflation fears, plus a general flight to safety, I think.

“Inflation fears are increasing interest in TIPS, obviously. The 5-year real yield has fallen 51 basis points in less than a month. The 10-year is down 47 basis points. This reflects a lot of inflation fears, plus a general flight to safety, I think.”

I think you are correct in your assumptions here.

I bought a big chunk of STIPs duration 3 yrs. 3% yield, up 3%! Lightened equities. The perfect storm!

Schadenfreude. Well we finally get the benefit of investing in inflation-indexed debt after years of ‘insuring’ against unexpected inflation.

I think you’re phrasing this overly conservative here, though I understand you wouldn’t want to unintentionally mislead readers by saying/projecting it might be higher when many potential factors could dampen inflation these next few weeks.

Here’s my line of thinking: we’re almost 1/3 of the way through March, and the average gas price has increased ~16%. If gas stays flat from here on out, then the average gas expense might go up ~12% month over month. Gas comprises ~5% of CPI, IIRC, so if it went up 12% and the remaining 95% went up 0.5% like we’ve seen core doing lately, that would make March’s number 1.08%.

That monthly number would put the 6-month value at 4.54%, for an I Bond APR of 9.08%. I’d say this number represents something close to a median projection given our knowledge of the first 9 days of the month, and thus I consider 9.5% more likely than 8.0%. Just my thoughts using some back-of-the-envelope calculations.

I can buy your logic but as an inflation watcher, I have learned to use conservative estimates. I had been thinking that inflation might rise 0.7% in February and 0.9% in March, which would have put us at 8.24%. There looks like very little chance that next month’s number would be less than 0.9%. If it is 1.0% the variable rate would go to 8.86%. So … 9% is definitely possible, or a bit higher.

I have to agree with you Scott. Except the price of a gallon where I live has increased from $3.19 on March 1, to $4.19 today – a 31% increase in ten days, which is roughly double your figure.

I think using national numbers is a more-accurate approach. One can get pretty good numbers from GasBuddy, and it looks like the current price is ~23% higher than Feb’s average. If it stays there, the March number will be ~20% higher than the Feb number. That said, I’m certainly biased to assume inflation is higher because my wife and I have seen a huge increase in grocery prices the last two months locally, ouch.

I’ve looked into this more since my original comment. Looks like gas is more like 3% of CPI rather than 5%. That’s a big impact on the calculations. However, food (also not in core) is ~15% of CPI, and food has been increasing ~1.0% per month lately. So a reasonable “best estimate” of 20% rise in gas, 1% in food, and 0.55% everything else (the average of core for the last 5 months) would put the month at 1.20%, setting the next I Bond rate at 9.34%. That would be my best estimate now nearly halfway through March.

But I also realize that Tipswatch isn’t really an inflation-prediction blog, and there is certainly value in keeping guesses on the conservative side. If gas only goes up 15%, food 0.5%, and core 0.2% (typical of the last decade), then the next I Bond rate would be 8.28%. Still high, but more in line with what my guess would have been having seen the Feb number but not having seen the big spike in gas…probably at the low end of reasonable guesses barring some huge drop in price in the back half of March.

Scott, excellent and logical analysis. You would think that gasoline prices would not be expected to rise in March, which means the overall non-seasonal rate should be higher than the “official” seasonal rate that makes the news. But last year gas prices appeared to go up 12%, but the BLS reported it as 9%. At any rate, yours is the best analysis I have seen.

May be better to wait for the adjustment to buy your IBonds, base rate may increase! Inflation does not just go away!

I would have to respectfully disagree. If you were to put $10K in now, then that’s an easy $356. Now add the upcoming 3.43%(+) that is coming up. I can’t do the math, but as has been pointed out, $356 is going to be hard to make up real quick with just a 0.1% to 0.2% fixed rate (and that’s if they even raise it). My opinion.

Don, it is extremely unlikely that the I Bond fixed rate will rise in May. If you buy before May, you will still get a full six months of the new rate, but by buying before May 1 you will get a head start of $356 in the first six months, as Joe points out. The only way buying after May works out is if the last six months you hold the I Bonds have a variable rate higher than 7.12%. That’s very unlikely. (I bought my full allocation in January.)

But when you are talking about holding these 10yrs its different math! This really not big money with the $10k limit. I have others with a 3% fixed rate! These are accidentally high yield right now!

Keep in mind that a fixed rate of 0.2% is equal to $20 a year on a $10,000 investment. If you buy before May 1, that $356 head start will be equal to at least 13 years of the 0.2% fixed rate, after adjusting for inflation. I did the calculation in a previous article. But I really do believe the fixed rate is staying at 0.0% in the May reset.