Inflation breakeven rate soars to 3.34%, probably an all-time high for any TIPS of any term.

By David Enna, Tipswatch.com

The Treasury’s offering today of $20 billion in a new 5-year Treasury Inflation-Protected Security generated a real yield to maturity of -0.340%, the highest for this term at auction in two years and a remarkable 117 basis points higher than a similar auction just four months ago.

This is CUSIP 91282CEJ6, and the Treasury set its coupon rate at 0.125%, the lowest it will go for a TIPS. Investors paid an adjusted price of about $102.76 for about $100.42 of principal, after accrued inflation is added in. This TIPS will have an inflation index of 1.00424 on the settlement date of April 29.

It’s hard — for me at least — to predict real yields of new TIPS at auction, but this result seemed surprisingly high. At yesterday’s market close, the Treasury estimated the real yield of a 5-year TIPS at -0.49%, and a similar TIPS was trading on the secondary market with a real yield of -0.54%. Big-money TIPS investors could be waiting on the sidelines, anticipating higher yields in coming months. But the bid-to-cover ratio for this auction was a decent 2.73, indicating reasonably strong demand.

Today’s auction result continued a several-months trend of new and reopened TIPS getting higher-than-expected yields at auction. For investors, this is a welcome trend.

Definition: The “real yield” of a TIPS is its yield above or below official U.S. inflation, over the term of the TIPS. So a real yield of -0.340% means this TIPS will trail U.S. inflation by 0.34% for 5 years. A negative real yield isn’t necessarily a bad investment; the quality of the investment will depend on whether inflation rises above expectations in future years.

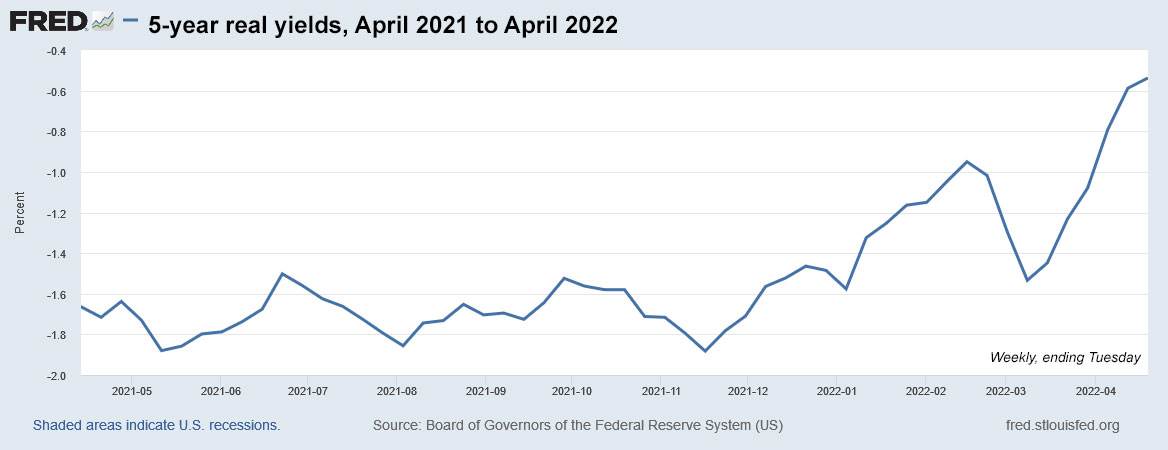

Here is how the 5-year real yield has trended over the last 12 months, based on Treasury estimates:

Inflation breakeven rate

With a 5-year nominal Treasury currently trading with a yield of 3.0%, this TIPS gets an inflation breakeven rate of 3.34%, which I believe is the highest breakeven ever recorded at auction for any TIPS of any term. (I can track data back to 2003.) It shows how much inflation expectations have soared over the last four months. In a December reopening auction of a 5-year TIPS, the inflation breakeven rate was 2.73%, 61 basis points lower.

What does this mean? If inflation averages more than 3.34% over the next 5 years, this TIPS will outperform a nominal Treasury. U.S. inflation is currently running at 8.5% and is likely to remain at least in the 4% to 5% range well into 2023. (Still, I have to admit that a 5-year nominal Treasury paying 3% is starting to get interesting. Might need to mix and match.)

Here is the trend in the 5-year inflation breakeven rate over the last 12 months:

Reaction to the auction

I was a buyer of a nibble-sized investment in this TIPS. While watching yields this morning, I fully expected the yield to come in at -0.50%, 16 or 17 basis points lower. So, nice surprise. In addition, this TIPS (along with all other TIPS) will get an inflation accrual of about 1.3% in May, based on non-seasonally adjusted inflation in March.

After the auction’s close, I noticed news reports that Fed Chairman Jay Powell had signaled in Europe that the Fed is highly likely to raise short-term interest rates by 50 basis points in May. “It is appropriate,” he said, “to be moving more quickly. … I would say 50 basis points will be on the table for the May meeting.” This comment certainly had an effect on Thursday’s auction. The 5-year TIPS is the maturity most sensitive to increases in short-term nominal rates.

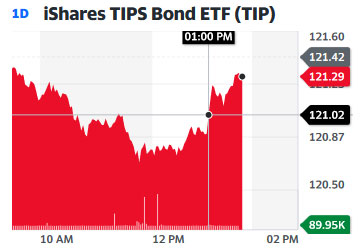

The TIP ETF — which holds the full range of maturities — had been trading slightly lower all morning, indicating higher yields, and then popped a bit higher after the auction close. This indicates the market saw the auction as acceptable.

We are entering a new phase in Treasury issues, with the Federal Reserve no longer buying TIPS on the open market as part of quantitative easing, and also preparing to slim its balance sheet in upcoming months. Higher yields should be coming. But the market is already pricing in the Fed’s future actions.

I am speculating that big-money investors — pensions, hedge funds, foreign central banks — won’t be bidding TIPS yields lower until we see the rate-rising-trend stabilize. I believe we will see the 5-year real yield climb above zero later this year.

CUSIP 91282CEJ6 will get a reopening auction in June and then the Treasury will auction another new 5-year TIPS in October and reopen that one in December. Here is the history of recent TIPS auctions of this term, showing how 5-year real yields climbed substantially higher during the Fed’s last tightening cycle in 2017 to 2018:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: 5-year TIPS reopening auction gets a real yield of 0.362%, breaking a string of negative yields | Treasury Inflation-Protected Securities

Pingback: This week’s 5-year TIPS reopening auction looks like a winner | Treasury Inflation-Protected Securities

I bought some as well, and plan to spread my purchases over 2 more 5-year auctions this year and then three 10-year auctions as well. I didn’t buy any TIPs in 2021 or 2020 because I didn’t feel like getting such a negative yield. So that means that two “wrungs” are missing in my 10 year ladder. Question: I have 10-year TIPs maturing in 7-15-23 and 10-year TIPs maturing in 1-15-24. I never recorded the real yield for these and would like to add this info to my ladder spreadsheet. How can I find this info?

I do like the idea of gradually adding to your TIPS ladder, without going “all in” on a single issue, at least until yields get irresistible. On your previous purchases, it’s impossible to say what the original yield to maturity was, since each 10-year TIPS has three auctions with the same maturity date.

But, for the TIPS maturing July 2023, the coupon rate is 0.375% and the current real yield is -2.99%, but you can ignore that if you will hold to maturity. It is an exaggerated number because of the short term remaining. The inflation index is 1.216, or 21.6% above par value.

For the TIPS maturing Jan 2024, the coupon rate is 0.635% and the real yield to maturity is currently -2.02% (again, exaggerated). The inflation index is 1.213, or 21.3% above par value.

When you see short-term real yields like this, you have to recognize that these TIPS will be getting a 1.34% upward adjustment to principal in May, and probably some high adjustments in coming months. That’s reflected in the market price.

I bought some too. Fingers crossed even this five year moves solidly into positive territory this year!

This is why I have been “nibbling” into TIPS, hoping to ride the wave of higher real yields. For these investments, I have been selling a bit of my SCHP total TIPS fund to buy individual TIPS. Next’s month’s 10-year auction could also be interesting.

I think the Fed will follow the path of least resistance, which is to let inflation run moderately above target, while increasing nominal rates just enough to make it look like they are doing something. The result will be continued negative real rates, and above B/E inflation. On that basis, today’s offering should work out well for us TIPPIES.

I was so pleased to see that already smaller negative yield, move upwards a bit more. I needed to fill a gap in my bond ladder, so I just made a BIG (for me) bulk buy today, rather that splitting it across the year. While the break even is highest ever, I suppose I am biased by the other experiences I am having now with supply chain issues, and how it’s impacting me outside my own personal finances. It just “feels” like this inflation has room to run, for at least the next 12-18 months, which should allow the first year of this TIPS to more than make up for this now smaller TIPS premium.