Despite its negative real yield at auction, this TIPS performed very well.

By David Enna, Tipswatch.com

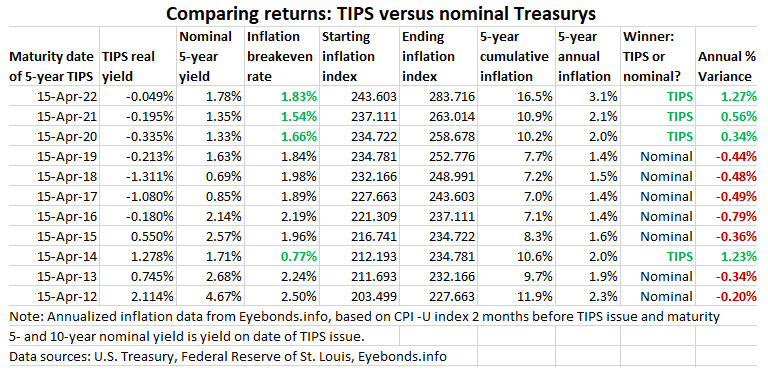

On April 15, 2022, a 5-year TIPS — CUSIP 912828X39 — matured. It was first auctioned on April 20, 2017, with a real yield to maturity just slightly negative to future inflation, at -0.049%. The coupon rate was set at 0.125%,

Here’s the question: How did CUSIP 912828X39 do as an investment versus a nominal 5-year Treasury? It turns out it did quite well.

I’ve been writing about Treasury Inflation-Protected Securities since 2011, and I’ve been investing in these products since 1999. I track the performance of every maturing 10-year and 5-year TIPS, as they mature in January, April and July. For more on this, see my ‘Tips vs. Nominals‘ page.

On the day CUSIP 912828X39 was auctioned, a nominal 5-year Treasury was yielding 1.78%, setting up a 5-year inflation breakeven rate of 1.83% for this new TIPS. As it turned out, thanks to some lofty inflation numbers in recent months, inflation over those 5 years averaged 3.1%. The TIPS investment ended up being the winner, by a fairly large margin — an annual bonus of 1.27%.

(I didn’t buy this TIPS at the originating auction, but I did end up investing in CUSIP 912828X39 at the December 2017 reopening auction, when the real yield to maturity was a more attractive 0.370%. I invested $10,000 and ended up getting $11,609.90 at maturity, plus the 0.125% coupon along the way.)

TIPS have been under-performing nominal Treasurys for most of the last decade because inflation for much of that time ran lower than expectations. We seem to have turned the corner on that, with official U.S. inflation now running at 8.5%, much higher than expectations. Will that trend continue? It seems likely, for awhile at least.

Here is how 5-year TIPS have performed versus 5-year Treasury notes for all maturities since April 2012:

Notes and qualifications

This chart is an estimate of performance, because it uses a full month of inflation in the ending month, when actually TIPS accruals are based on a half month for the first and last months, with the origination and maturity occurring on the 15th of the month.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Many people aren’t aware that the way inflation is calculated has changed several times over the last forty years. According to ShadowStats, inflation is running at almost 17% using 1980 methodology. That’s certainly been my experience in the stores. Current figures are completely bogus. I’m on a fixed income and my wife is a teacher who got a 1.75% pay increase for 2021-22 (and will be lucky to get that again for 22-23). Something has to give!

Right you are. Back when inflation was double digits the government changed the methodology to save on borrowing costs. They also, temporarily, made long term bonds callable. Whatever the vehicle, stocks, bonds, commodities, I never assume the entity ” on the other side of the table” has my best interests at heart.

David

Correct, the brokered CDs pay out interest semi-annually. In a rising interest rate environment that would be a plus of course.

Not too many callable in my experience. Also there is a death ‘put’ enabling our heirs to return the security to the issuer without penalty. ( Haven’t utilized this yet.)

Thanks for the update, good information. Myself I frequently go with brokered CDs rather than the Treasury note (FDIC insured). Sometimes a greater yield depending on the bank’s need for funds. And there may be a $ 10,000 minimum.

Len, am I right in assuming that a brokered CD doesn’t reinvest the interest earned? That’s a small negative. Also, I believe, many of these are callable after a certain number of months. But that can work to your advantage.

I’m not Len, but I have purchased many brokered CDs from Vanguard over the past 15 years for our retirement accounts. They’ve always paid more than a comparable treasury. Lately, they have been paying less, but I’ll bet that is only temporary. During the financial crisis, many paid interest monthly. Most (maybe all now) pay their interest semi-annually. You are correct the interest is not reinvested. It is put directly into the settlement account. I haven’t seen any callable CDs on Vanguard. BTW, I have been reading this site for years. Always great information. I have learned alot from you. Thanks!

I learn a lot reading your posts. The only bonds I own are I bonds and a TIPS fund in my 401k. I hope you will write something about funds as I probably won’t buy individual issues. If this is not your realm then perhaps you can steer me to a trusted source of information. Thanks again for the free education.

Back in July 2021 I wrote a 9-article year-by-year series on how three bond funds: BND, SCHP and VTIP performed during the last Fed tightening cycle. You can read the first article about 2013 here: https://tipswatch.com/2021/07/06/lets-take-a-deep-dive-look-at-my-three-favorite-bond-funds-vtip-schp-and-bnd/ The rest of the articles are linked at the bottom of that piece.

What I theorized was that real and nominal yields could rise very quickly once the Fed committed to raising rates and reducing its balance sheet. In the 2013 to 2017 period, the Fed acted very slowly, but inflation was not a major problem then. Now the Fed is accelerating its tightening, rather dramatically. All bond funds will suffer during this sweeping event. VTIP could end up being the best choice of these three, since it has a short duration and will benefit from high inflation. But things change eventually.

Thanks very much for the wrap-up on this particular TIPS. It was the first one I ever invested in (I’ve since bought others, though I started buying I Bonds a few years earlier), and it’s nice to know that it worked out well, especially given that virtually all my other holdings are under water YTD. Your commentary on these topics is really an invaluable asset it itself!

With the next 5-year TIPS for auction this week, the question is, will inflation stay elevated enough to make it a good purchase? I think we could see higher inflation for a while and I may bite and purchase some TIPS in this auction. I only wish the yield wasn’t negative. But it may improve slightly by auction time.