An earthquake has hit the Treasury market. The result is that TIPS are becoming much more attractive.

By David Enna, Tipswatch.com

The investment world — from Suze Orman to your Uncle Bob — has been fascinated by U.S. Series I Savings Bonds for the last 12 months, and rightly so. These inflation-tracking savings bonds are ultra-safe and are currently offering a gaudy yield of 9.62% annualized, for six months.

I’m a huge fan of I Bonds, and I highly encourage people to invest in them. But today, rather suddenly, there is a true alternative to I Bonds: Treasury Inflation-Protected Securities. Over the last 2 1/2 years, TIPS have been a mediocre investment, with real yields lagging behind the official U.S. inflation rate. But all that has changed — dramatically — in June 2022.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match current U.S. inflation. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

In the last two weeks — and especially after Friday’s high-side shocker of an inflation report — both nominal and real yields have surged higher, transforming a “meh” TIPS market into something very interesting: Real yields positive to inflation at a time of dangerously high inflation.

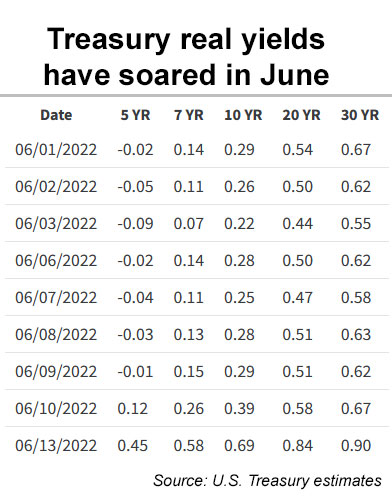

Here are the real yield numbers since June 1, based on the Treasury’s daily yield curve estimates:

These are some crazy numbers. The 5-year real yield surged 46 basis points in two days. The 10-year TIPS real yield was up 40 basis points. For those of you who invest in TIPS mutual funds, that’s pretty much “half a duration,” meaning those funds have been hit with a half a duration event in just a couple days. For example, the broad-based TIP ETF has a duration of 7.12 years. Last Thursday, it closed at $117.51 a share. Now it is trading at $113.72, a loss of 3.2% in a few days.

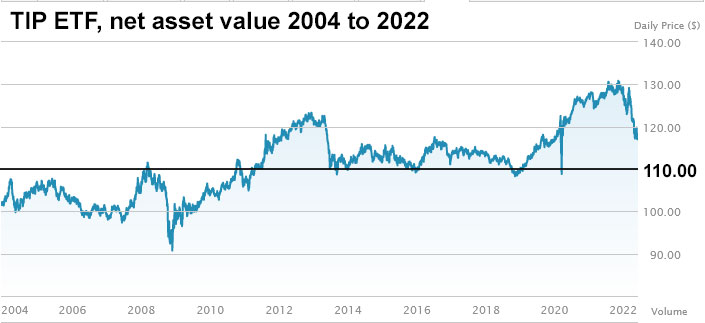

Many times in the 2015 era of Fed tightening (seems like a lifetime ago) I pointed to a price of $110 for the TIP ETF as a “buy signal.” I’ve thought about discussing that target again, but honestly I thought it would be too alarming and even embarrassing to point to a possible price decline of about 12% from where the TIP ETF was trading as recently as March 8, when it closed at $129.16.

Here is a historical chart, showing how $110 was a resistance level through nearly a decade of trading, right up to the pandemic-triggered market chaos of March 2020:

Although I prefer to buy TIPS at auction and hold them to maturity, I do have investments in Vanguard’s Short-Term TIPS ETF (VTIP) and Schwab’s Total TIPS ETF (SCHP). Because of very high inflation adjustments over the last year, VTIP hasn’t performed horribly. It has a total return of -0.71% year to date. But SCHP’s total turn has been -8.08% year to date because of its much higher duration. That is similar to its return in 2013, the year of the bond market’s “taper tantrum.”

I will continue to hold these funds, but I have been moving some money out of SCHP and into individual TIPS throughout this year.

What this means …

Yes, all of this is bad news for investors in TIPS mutual funds and ETFs, but it is good news for investors seeking to increase their holdings in inflation-protected investments. Real yields are now solidly positive across 5 to 30 years, giving TIPS a strong yield advantage over I Bonds, which if bought today will have a 0.0% real yield going into the future. So as of Monday’s market close:

- The 5-year TIPS has a yield advantage of 45 basis points over an I Bond purchased today.

- The 10-year TIPS, 69 basis points

- The 30-year TIPS., 90 basis points

Historically, I Bonds had have a real yield lower than a typical TIPS, and that is OK because I Bonds have several advantages: 1) a flexible maturity of 1 year to 30 years, 2) tax-deferred interest, and 3) much better protection against deflation.

But purchases of I Bonds are limited in electronic form to $10,000 per person per calendar year, plus $5,000 in paper I Bonds in lieu of a federal tax refund. I love I Bonds as an investment, but after you hit the $10,000 cap where do you go for inflation protection?

There are no limits on TIPS purchases. You can buy them on the secondary market, even in an IRA account if you choose, or participate in monthly auctions. See my Q&A on TIPS.

I want to state clearly that TIPS are for preserving wealth, not building wealth. If you are in the early stages of investing and far from your long-term needs for buying a house or for paying for college or especially for retirement, TIPS aren’t going to be a great investment. That’s especially true when yields are less than 1% over inflation. You probably won’t build enough wealth to meet your goals.

However, if you are nearing retirement, or in retirement, and have an adequate nest egg, then TIPS make sense as part of your investment portfolio – especially if you buy and hold them to maturity. That strategy is risk-free, and you can protect a part of your savings from the dangers of unexpected inflation.

The downside to TIPS

TIPS are a complicated investment. I’ve had long discussions with finance-savvy reporters at the Wall Street Journal and other media who simply “didn’t get” the idea of a return based on future inflation, or a “real yield to maturity,” or a “discount” or “premium” price at TIPS auctions.

Complicated, yes, but investors can simplify TIPS investing by buying them and then holding them to maturity. That strips away almost all the risk of market fluctuations, as we have seen with TIPS mutual funds. You can simply track par value x the current inflation index and ignore market value.

If you buy a 10-year TIPS that yields 0.69% above inflation, you are going to get a return that is close to 0.69% over inflation for a decade. (The actual return could be affected by a long deflationary period, which could reduce accrued principal. This is one advantage I Bonds have over a TIPS.)

Also, the inflation accruals earned by TIPS are federally taxed as income in the year they are earned, even though they aren’t paid out until maturity or redemption. This creates a “phantom tax” issue, and is the reason most financial advisers recommend buying TIPS in a tax-deferred account. (You can purchase TIPS at auction through most major brokerages with no commissions or fees.)

Where are real yields heading?

Of course, I can’t predict the future. But I have examined several Fed easing and tightening cycles of the past and it seems clear to me that we haven’t reached the top for real yields, especially for shorter-term issues, which will be more sensitive to Fed rate increases. A 10-year real yield rising above 1% seems like a certainty, unless the Fed loses its nerve. (And at that point, we should also see the I Bond’s fixed rate rise above 0.0% in the November 2022 or May 2023 rate resets.)

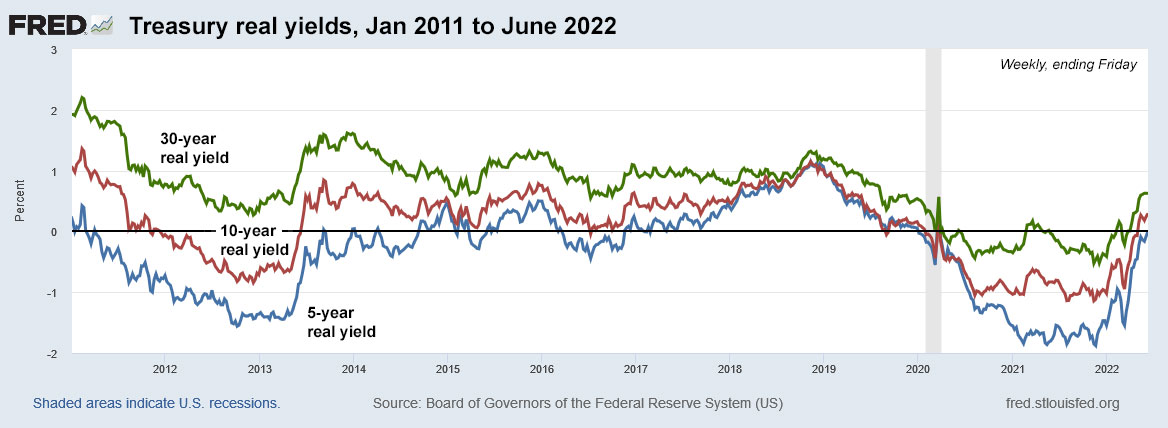

Here is a long-term view of 5-, 10- and 30-year real yields through several Fed easing and tightening cycles:

It’s been an “incredible” (too nice a word?) 11 years for TIPS, with real yields falling deeply negative under the weight of Federal Reserve quantitative easing, first in the 2011 to 2013 era, and then again after the pandemic outbreak in 2020. The period of 2015 to early 2019 was a time of “implied tightening” by the Fed. It was raising interest rates, but not dramatically reducing its balance sheet of Treasurys.

Notice how the yield curve flattened in early 2019, after several years of the Fed’s moderate actions. Now, in June 2022, the Fed is acting much more aggressively, with a 0.75-basis-point increase in short-term interest rates looking likely this week, plus sizable monthly efforts to reduce its balance sheet. The Fed knows it has to act as inflation is surging globally.

So, I do expect real yields to continue to rise, and the yield curve to flatten as fear grows of an economic slowdown. But even with higher yields “possible” in the future, I’d be a buyer of individual TIPS in this current market of reasonable yields and very high inflation. We can’t be sure of the Fed’s future actions.

Next week … A 5-year TIPS auction

The Treasury will be holding a reopening auction June 23 for CUSIP 91282CEJ6, creating a 4-year, 10-month TIPS. That TIPS is currently trading on the secondary market with a real yield of 0.66% and an unadjusted price of $97.45 for $100 of value. It’s looking attractive, in my opinion. But a lot can change, as the last two weeks have shown.

I’ll be posting a preview article on that auction on Sunday.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Mr. Enna, today is June 23rd, and the TIPS maturing July 15 (less than a month away) has an adjusted principal of $125.55. Can you kindly explain to me why they are selling at a price around $100 instead of $125? I can buy the TIPS for $100, wait one month, and collect $125 plus interest. What am I missing here?

Yes, that TIPS currently has in inflation index of 1.255, which means if you bought this TIPS, you would be buying about 25.5% additional principal, and you would pay for it. So a $10,000 investment in this TIPS would cost you $12,550, plus you probably would have to pay a very slight premium, since it is trading with a price of about $100.50.

I want to get iBonds from my tax refund. My wife and I file a “married filing jointly” return. Can we get $10,000 in iBonds, or only $5,000?

If you file jointly, you are limited to $5,000 per tax return.

Today the Treasury reported the real yield at 0.48% for the 5-yr TIPS, a small drop from 0.54% from Tuesday, June 21. Is that still considered attractive, assuming Inflation will stay elevated for the near term?

Sure, it’s still attractive. This TIPS originated in a auction on April 21 with a real yield of -0.34%. We’ve taken a pretty big jup higher in two months.

I noticed on the treasurydirect website that the 4 week Bill does not have an area for purchase yet? Do you know if they auction every week?

Also, If one was to buy a 4 week bill say once a week for say 12 weeks, would that be considered a bill ladder and every week one would roll over to the next series? Seems like doing it this way would stay on top of the ever increasing interest rates if that is what the fed decides to do.

Thanks for all your information,

I believe they auction every Thursday. So if you did 4 in a row and set them all to rollover, you’d be set.

Is there any reason to prefer buying at the 5-year TIPS reopening on Thursday as opposed to buying on the secondary market now? (Being risk-averse, it would be nice to know what yield I’m getting instead of rolling the dice.) By the way, I REALLY appreciate your postings and responses! Thank you!

Since I write a preview about every auction, I always buy at the auctions and I don’t have any experience with the secondary market. The negatives might be 1) a large minimum investment is sometimes required and 2) TIPS are lightly traded so there could be some bid – ask spread. The positive is that you can jump on a buying opportunity, as happened last week with a sudden half-day surge in real yields.

During the period of time when the 5 year TIPS were at the lowest price this week, the minimum purchases were in the 100K to 150K range. It wasn’t until Friday that a 10K minimum was available.

There was only 1 offering for the 5 year TIPS at my brokerage firm. Against that offering was a single bid that was considerably below the asking price. That offer was not accepted by the seller.

I’m going to keep and eye on things starting next Tuesday and see what’s available on the secondary market. This should give us some indication of what the prices are going to be on the Thursday auction.

I too don’t like the unknowns related to the auctions. I guess that’s typical of ultra-conservative TIPS purchasers. However, at least you can determine the amount that you want to purchase.

The yield on 5 year TIPS has backtracked a tad to +0.51. No longer can you purchase them with an inflation adjusted price under par. It’s currently going for $100.38. There’s some available on the secondary market with a minimum quantity of 10 (10K). If it wasn’t so close to next week’s re-opening, I’d probably purchase a small amount. On the other hand, you really don’t know what you’ll be getting a week from now at that re-opening. Things have definitely been trending in the wrong direction the last few days. A bird in the hand? Maybe I’ll pop for a few after all.

I am seeing the current real yield at 0.50% and since the coupon rate is 0.125%, this TIPS will be sold with a discounted unadjusted price of about $98.20, at current rates. But, because the inflation index will be 1.02376, investors will be buying about 2.4% additional principal. That would make the adjusted price around $100.53 for $102.38 of principal. Still a discount. A lot can change before Thursday.

Hi Michael – what opportunity cost risk do you see from the winding down of fed TIPS holdings creating another step function up in mid to long term TIPS real yields over the next year? i.e. hitting 2-3% based on the ‘increased supply’ factor

Hi David – sorry had Michael Ashton in my head

I don’t see TIPS real yields hitting 3% (OK, maybe on the 30-year). My gut feeling is that the Fed won’t have the fortitude to push rates that high. If the 10-year Treasury note hits 4.5%, then the 10-year TIPS should be right around 2%. But we are entering uncharted territory.

Thanks

Given the discussion on Bogeleheads about how infernal the Treasury Direct web site can be especially to the elderly, holding onto TIPS at one of the big three brokers may be a viable alternative for those who think that they may be passing their assets to heirs in the foreseeable future.

David, many thanks for the I-Bond and Tips information. Your 5/19 commentary on the 10Y TIPS reopening with a 2.24 bid-to-cover indicated a weak demand. Do you think this was because the Fed is not buying more bonds? What is considered a normal or good bid-to-cover ratio?

Thank you again, looking forward to your Sunday comments on the reopening of the 5Y TIPS

I think demand was fairly weak because big-money investors were sitting on the sidelines waiting for more favorable yields, which ended up happening. TIPS have been getting mediocre auction results for several months (which benefits investors since the yield is higher than the current market). That trend will probably reverse soon, since real yields have popped higher. Small-scale investors like us have zero influence on these auctions, so I don’t think we’ll have much effect on the results.

For TIPS, I think the consensus is that a bid-to-cover ratio of 2.50 is considered typical.

Is there any possible benefit to me in buying into the upcoming 5 year tip reopening if i bought at the original auction 2 months ago except for having more of a possibly good thing .ie has it become a more valuable hedge on inflation

Thanks..enjoyed your travel accounts

I also bought at the auction 2 months ago and will very likely buy at next Thursday’s auction, too. Basically, you will be buying more of an asset at a lower price. Really it depends on how you want to allocate your money. This is a 4 year, 10 month commitment in an inflation-protected bond. But note that yields are going to be very volatile in the days leading up to the auction.

Is the cusip 91282CE16 and can they be bought through Vanguard or other housees?

Yes, it is 91282CEJ6 and the term will be 4 years, 10 months. You can place an auction order at Vanguard and other brokerages (no fees or commissions) but you can’t wait until non-competitive bidding ends at noon next Thursday. Put the order in Wednesday evening to be safe. (Vanguard does not have this issue active yet.)

The rationale for Treasury paper funds has always eluded me. Another lesson with the TIPS ETFs it seems to me. The 5 year re-opening looking interesting.

TIPS go completely over my head unfortunately and I’ve maxxed out my I Bond purchases.

Do you recommend making any CD purchases yet? Fidelity and Vanguard have some 13-18 month brokered CDs for 2.95% and Connexus has a 12 month for 2.26%. Or should one wait a bit longer to dive in?

I’m also interested in CDs as rates are rising quickly. But more interesting to me are nominal U.S. Treasurys. The 13-week is at 1.83%, 6-month at 2.43%, 1 year at 3.15%, 2-year at 3.45%. Those are good rates for short term investments.

David,

Is it allowable to hold TIPS in a Roth IRA and would a Roth be a good vehicle for doing so?

Yes and yes.

Yes, you can buy and hold TIPS in any tax-deferred account, through a brokerage. You can’t open an IRA at TreasuryDirect. My strategy is to hold TIPS in a traditional IRA account, following the advice of many financial advisers to put your riskiest assets (stocks) in a Roth account, which will be your last to withdraw. One negative of this strategy: TIPS in a taxable account are free from state income taxes, but that perk goes away when you hold them in a traditional IRA. A Roth account doesn’t have this problem.

The 5 year TIPS is going for $99.49 WITH the inflation index included. Since that’s below the $100 par value, even a “glass half-empty” person like myself can’t see a downside to start buying them at next weeks auction if the below par price holds thru next Thursday.

Besides Zvie Bodie, you’re about the only one out there that does a good job of explaining TIPS and iBonds. The only problem is that the yields are pretty paltry. However, if you’re collecting Social Security and have a decent nest egg, they’re great for preserving wealth.

” … investors can simplify TIPS investing by buying them and then holding them to maturity. That strips away almost all the risk of market fluctuations, as we have seen with TIPS mutual funds.”

Question – If you intend to hold a fixed percentage of your portfolio in TIPS with a fixed duration, aren’t you subject to the same type of ETF market fluctuations as you re-invest maturing TIPs into new ones?

Yes, if you are looking at “market fluctuations” and tracking daily market value. But if you have a ladder of TIPS maturing out into the future, and you intend to hold them to maturity, you can ignore market fluctuations and track par value x inflation index all the way to maturity (plus coupon payments). I never look at the market value of my TIPS, just the current accrued inflation value.

Once you start taking your RMD’s from your IRA’s, you’ll be looking at it. You’ll need it to determine the RMD for the TIPS that you hold in IRA accounts.

This is true. I haven’t started RMDs yet, but I plan to keep more-liquid funds in my tax-deferred accounts to pay them. And I understand the market value of the TIPS will be part of the equation.

David, is the real yield set in stone on the auction date or can it vary over the term of the bond?

This is a great question. Yes, when you purchase a TIPS and hold it to maturity, your real yield to maturity is set by the auction’s purchase price and coupon rate. What is confusing is that the TIPS will immediately start trading on the secondary market, and its real yield will be changing day to day based on market demand. So the “market value” of that TIPS will change, but the real yield to maturity, if you hold to maturity, is set at the auction.

Thanks. I intend to purchase 5-year TIPS at the reopen auction later this week and hold them to maturity.

Just to be clear, if I do that, and ignoring the miniscule coupon rate, then the TIPS principal will appreciate based on the CUMULATIVE 5-year inflation rate (CPI-U) plus the annual real rate. So, as an extreme but simple example, if inflation is 10% per year over the next five years (based on CPI-U), and the real yield is 1% per year, then the bonds will return approximately 55% more ([10% plus 1%] times five) upon redemption than their par value on the auction date. Is that correct?

This sounds right, but there would be some compounding, too, as your principal balance grows. Also, the real yield to maturity does factor in the minuscule coupon rate, which wouldn’t have much effect in this case.

I find it a bit annoying to constantly be talking about earnings in percentage points above and below inflation when you’re talking about TIPS. If there’s a way to extrapolate actual interest rate earnings on these (for example you say ” which if bought today will have a 0.0% real yield going into the future. “) at least mirroring last years inflation rate (I assume if rates were the same as last year we’d be talking at around an 8ish percent rate fluctuating and adjusting for inflation and compounding?) it would make it a lot easier to follow.

Yes, your future return will depend on future inflation, but you will know precisely your future “real” return … it is set by the real yield to maturity when you make the purchase. If you buy a regular Treasury or a bank CD, you will know the “nominal” return but you won’t know the real return. Two sides of the “coin.”

I read awhile ago that the frequently mentioned negative of TIPS “phantom income” in a taxable account is not a negative for an investor who has no need or desire to spend that interest. For such investors the “phantom income” from TIPS is essentially the same as the taxed and paid interest on nominal bonds or bond funds that is immediately re-invested in another bond or bond fund. In both cases current income is taxed but re-invested rather than spent. The same could be said about the currently taxed “phantom” dividends from a stock fund that are immediately reinvested in additional shares. The only difference is that with TIPS the investor does not have the option to spend the taxed income. But again, if one doesn’t intend to spend this income in the year earned anyway, then its actually more cost effective to have what is in effect automatic and immediate re-investment of interest with the TIPS compared to a nominal bond kicking out semi-annual interest that may well languish in a low interest cash account awaiting re-investment.

Barry, this is exactly correct. I have argued against worrying about the phantom return issue, because as you say it is just the same as any bond fund in a taxable account with reinvested dividends. Of course, the theory of “asset location” also suggests puting bonds in tax-deferred accounts and stocks in taxable accounts. …. After I retired, I didn’t want to sell taxable assets to buy TIPS, so I moved my purchases to tax-deferred brokerage accounts, where I could sell and buy within that account without tax consequences.

I read that you are moving money from SCHP to single TIPS. Are you doing it even though SCHP is deep in the red?

It isn’t deep in the red if you consider that SCHP had a total return of 10.9% in 2020 and 5.9% in 2021. But making a switch from SCHP to an individual TIPS keeps my asset allocation exactly the same, so it’s more a matter of moving to an investment I prefer to hold to maturity.