Quantitative tightening will have to ramp up in coming months if the Fed wants to bring U.S. inflation down.

By David Enna, Tipswatch.com

The basic monetary rule of the last two decades has been this: When the economy slips lower and the stock market stumbles, the Federal Reserve steps in with aggressive stimulus. But when the economy is thriving, and the stock market is soaring, the Fed sits on the sidelines and watches.

That rule has been crushed in 2022, because U.S. inflation has soared to a 41-year high of 9.1%. Now the Fed has been forced to act, and it is aggressively raising interest rates and beginning to reduce its massive balance sheet of Treasurys and mortgage-backed securities.

Amassing the Fed’s current $8.8 trillion balance sheet has taken more than a decade in a process known as quantitative easing. What is quantitative easing? Here is a concise definition from Investopedia:

Quantitative easing (QE) is a form of monetary policy in which a central bank, like the U.S. Federal Reserve, purchases securities from the open market to reduce interest rates and increase the money supply. … As money is increased in an economy, the risk of inflation looms.

When the Fed reduces its balance sheet, it uses a process known as quantitative tightening. Again, here is the Investopia’s concise definition:

Quantitative tightening (QT) refers to monetary policies that contract, or reduce, the Federal Reserve System’s balance sheet. This process is also known as “balance sheet normalization.” In other words, the Fed (or any central bank) shrinks its monetary reserves by either selling Treasuries (government bonds) or by letting them mature and removing them from its cash balances. This removes liquidity, or money, from financial markets.

On March 23, 2022, the Federal Reserve’s balance sheet topped off at $8.96 trillion, an increase of 282% over the total of $2.44 trillion in January 2011. Since March, the Fed has begun to raise interest rates and to allow Treasurys and mortgage-backed securities to mature without reinvestment. Now, as of Aug. 2, 2022, the balance sheet stands at $8.87 trillion, a reduction of just 1% in four months.

I repeat, a reduction of 1% after an increase of 282% over a stretch of 11 years. This is what the Federal Reserve does when it implements quantitative tightening, at least so far into this inflationary crisis. Here is a look back at the Fed’s moves to “ease” and “tighten” over the last 11 years:

There are so many things to consider in this chart.

- Note that the easing periods — when the Fed was adding to its balance sheet and increasing the U.S. money supply — lasted longer and moved higher very quickly.

- The Fed increased its balance sheet by 84.8% from January 2011 to November 2014, then essentially kept it stable from 2014 until March 2018.

- The one period of quantitative tightening that is completed lasted from about March 2018 to September 2019, only 17 months. That 2018-19 tightening resulted in a reduction of only 13.1%.

- Then in late 2019 through March 2022, the Fed increased its balance sheet by an astounding 138.3%.

- Now, with tightening beginning again, the Fed is taking a slow-motion approach, reducing the balance sheet only 1% over four months.

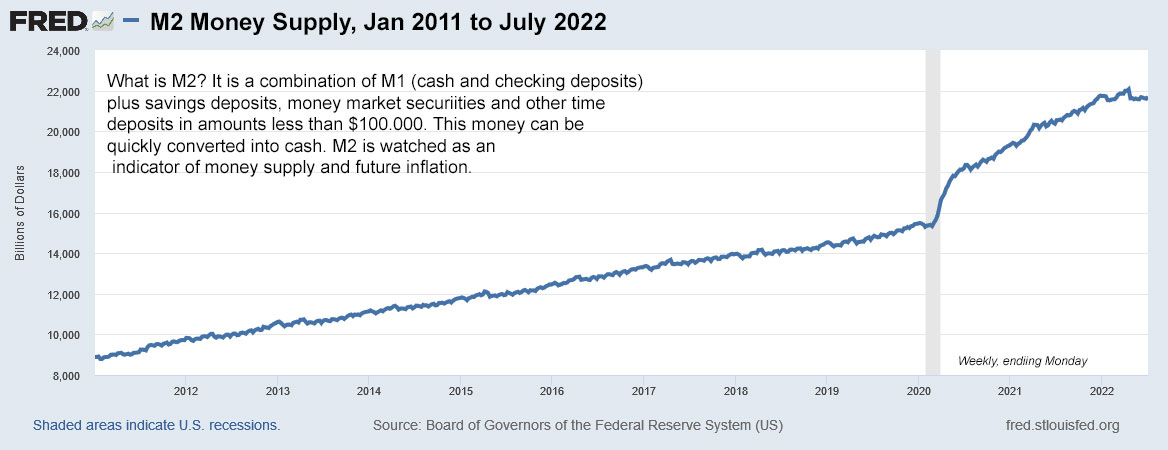

Over this same period, here is the trend in the U.S. money supply, as defined by M2:

And to complete the picture, here is the trend in the annual U.S. inflation rate, by month, over that same time period:

Logical conclusion: Increases in the Fed’s balance sheet, especially in the period after 2018 through the pandemic — and combined with aggressive direct-to-taxpayer stimulus from Congress — resulted in a strong surge higher in both money supply and U.S. inflation. To solve today’s dangerous inflation problem, the Fed will have to get serious about reducing its balance sheet, running the risk of weakening the U.S. economy.

But so far, the Fed hasn’t seriously addressed its balance sheet, which has probably resulted in a weird combination of effects: 1) allowing longer-term interest rates to drift lower, and 2) allowing the stock market to surge off its bear market lows.

Barron’s published a story yesterday with a great headline: “The Fed Is About to Ramp Up Balance-Sheet Shrinkage. It May Get Dicey.” The article makes the point that the Fed’s half-hearted balance sheet reduction so far is barely being noticed by the markets. From the article:

When the central bank began QT in June, it set out to partially unwind roughly $4.5 trillion in quantitative easing, or QE, that was conducted in response to the pandemic. The Fed started by letting up to $30 billion in Treasuries and $17.5 billion in mortgage-backed securities, or MBS, roll off its balance sheet, as opposed to reinvesting the proceeds. Starting next month, those caps will rise to $60 billion and $35 billion, respectively, meaning the pace of balance-sheet runoff is about to double. Fed Chairman Jerome Powell has suggested that QT would go on for two to 2½ years, implying that the Fed’s $9 trillion balance sheet would shrink by roughly $2.5 trillion.

Barron’s points out that the Fed has attempted quantitative tightening only once before, in the 2018-19 period, and even though that tightening wasn’t aggressive, it resulted in disruptions to the U.S. bond market. More from the article, with thoughts from Joseph Wang, former senior trader on the Fed’s open markets desk.:

September and beyond is when Wang warns something is apt to break, not unlike what happened the last time the Fed embarked on QT, and chaos in the repo market prompted an early end to the program. …

And from Solomon Tadesse, head of quantitative equities strategies North America at Société Générale:

… in order to bring inflation back to 2%, the Fed needs to shrink its balance sheet by about $3.9 trillion — significantly more than what investors expect, Tadesse says. By his calculations, QT alone would amount to about 4.5 percentage points in additional rate hikes.

“I don’t think there is appreciation for QT, by markets or the Fed,” Tadesse says. “In the end, if QE mattered, so will QT,” he says, referring to the big lift quantitative easing gave to risk assets. “It might not be totally symmetrical, but there will be a meaningful impact.”

The Barron’s article ends with this: “… investors should brace for added volatility. The Fed is entering the unknown, and so are markets.”

Some final thoughts

We have just ended a very strange month for the Treasury and TIPS markets, with uncertainty driving yields higher, lower, higher, lower — almost at random. Much of this volatility followed statements from Jerome Powell, chair of the Federal Reserve, and actions by the European Central Bank. While those statements seemed hawkish to me, the markets reacted with talk that the Fed would soon ease off and begin cutting interest rates again next year.

In his July 27 news conference, Powell said: “We are continuing the process of significantly reducing the size of our balance sheet.” But as the data show, that process has started slowly and has been an insignificant factor, so far, in bond markets. The 10-year Treasury note had a yield of 0.54% on July 1 and closed at 0.37% on Aug. 5.

This isn’t the way it was supposed to work, which forced San Francisco Fed President Mary Daly to step in Tuesday to declare that there is still “a long way to go” to bring inflation down from four-decade highs.

It seems clear to me that if the Fed ever wants to institute quantitative easing again in the future (and you know it will) it has to first drastically reduce its balance sheet, probably down to at least the September 2019 level of $3.8 trillion. That will take a lot of quantitative tightening, over a period of two years, or more.

Unfortunately, that sort of sustained tightening is not likely. And so … inflation will continue to be a problem. And inflation protection continues to make sense as part of your asset allocation.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Brian, a weird combination of effects: ” 1) allowing longer-term interest rates to drift lower, and 2) allowing the stock market to surge ” could be restated as , ” 1) allowing longer-term interest rates to drift lower, and 2) encouraging the stock market to surge “. In other words, the usual malarky.

Thank you for this informative post. I first bought inflation-indexed bonds in 1998, when TIPS with a 30 year maturity and a 3.875% coupon/real yield were selling at par and you could buy up to $30,000 per year of I-Bonds with a coupon/real yield of 3.4%.

When TIPS real yields went to near zero, I sold the TIPS and bought Vanguard’s High Dividend Yield Index Fund, but kept the (nonmarketable) I-Bonds. I am watching the TIPS market. but I don’t see myself getting back into TIPS unless/until real yields reach 2%.

It could happen, on very long maturities. I can’t see the Fed holding off long enough to let nominal and real yields climb to what we could consider “historical” levels. Historically, even 10-year nominal Treasurys yielded close to 2% above inflation. Today’s bond market is constantly under the watchful eye of the Fed.

Am I crazy for wanting to get at least 50% of my assets into TIPS? I’m late 50’s, just retired (at least for now due to being burnt out), frugal, and have likely saved enough as long as my investments keep up with inflation. (Also, I’ve always been a very conservative “investor” due to anxiety.) Even with 50% in TIPS, I would still struggle with where to put the rest (since having more than 30% in stock funds would likely stress me out). Thank you for such a great blog and for helping me take action. (2 months ago, I didn’t own any TIPS; now I’m up to 20%…if nothing else, hopefully TIPS are likely to be better than CDs)

I have both TIPS and “fixed-rate” fixed income. The TIPS make me comfortable buying longer-term fixed rate. I bought a fixed-rate Multi-Year Guarantee Annuity for the first time. At least within the state’s guarantee limit. It is important to check that out. Our state has a “per annuitant” limit that is NOT disclosed on the guarantee association’s website, a big mistake, that could mean some people are unknowingly uncovered.

Good luck. The people hurt worst by central banks are the studious savers, who are being forced into taking risk.

I’ve been reading about MYGA’s the past few days, and I noticed that the rates are better than CDs, but I don’t know what impact the sales commission would have of my final return. (I wish I could buy an MYGA online the same way that I can buy CDs.)

It is almost not worth the hassle to buy an annuity. Though they can be bought online. The rate can be better – but can also be the same – as a CD. The money does grow tax deferred for a while. But the best rate over a CD currently is about 100 basis points, and there is more risk with an annuity.

Bogle Heads has a good “MYGA thread” and Deposit Accounts is a good place to compare CD rates.

Good luck to all responsible people.

I don’t think that you just can compare the annuity “payout” rates to CD rates. From my understanding of them part of what you receive from the annuity each includes a partial repayment of principal. That principal payout artficially inflates the posted annuity “payout” rates. I actually think that you’d have to die In order to determine the actual rate of return. Here’s a link to a calculator that actually breaks it down by year.

https://iqcalculators.com/calculator/annuity-rate-of-return-calculator/

your misinformed on Annuities! MYGA are CD type investments, insured by the state to 250k!

Talk about being misinformed! The “state” does not insure annuities. US states are not on the hook for anything. Annuities are regulated and protected by nonprofit insurance guaranty associations at the state level. And, in California it’s only 80% coverage.

I live in California and annuity coverage here is only 80% of the amount covered. That put an abrupt end to any idea I had for purchasing an annuity.

I’m a huge advocate for inflation protection, and my stock allocation is about 35%. I am almost 69 (just a few days!) But my inflation-protected holdings are still only about 15% over my overall portfolio. I combine those with CDs, short-term Treasurys, short-term bond funds and the plain-jane total bond fund. I’d be willing to have more in inflation protection, but the yields need to be attractive. Right now, I will take any yield that looks attractive, but it needs to be nearly 100% safe.

If you are in your late 50s, you still can afford to take risk, but I totally understand where you are coming from. If you know you have enough to live on for the next 35 years, you can be as conservative as you like. (I am not a financial adviser.)

Thank you for your reply! I typically feel as though I should be wearing a paper bag over my head anytime I mention CDs/treasuries, so it’s comforting to know that there are informed people who use them. The inflation spike has spooked me…and I no longer have a sense of what an attractive yield would be. (It’s all been downhill since I got my first CD (when in in high school) which had a rate of 16.3%…in contrast, the last CD I got in 2021 had a appalling rate of 0.6%.) I also don’t know what an attractive yield is for a TIPS, but given what they were a year ago, I salivated over what I received during the recent 10-year auction and on the 20-year ones I’ve bought on the secondary market. Waiting for something better almost always seems to come back to haunt me, so hopefully it won’t be foolish if I buy significantly more TIPS on the secondary market in the next week or two (and I may get some brokered CDs and/or short-term treasuries while I’m at it) since I have a couple of huge CDs maturing. Thanks again!

Regarding CD’s, I like to build a matrix of CDs with 1 CD expiring monthly for a set number of years. In other words a ladder. If it’s a 3 year ladder, I have 36 CDs. When a CD matures, I either use the cash or reinvest 3 years out if rates are attractive or something else.

Mine is 3 months ladder now, until the Fed misses a chance to raise, then I would go longer. Im starting from scratch savings account money! I got 1/3 out waiting for the next raise.

TIPS are great for preserving purchasing power against losses due to “unexpected” inflation. The inflation over the last year shows exactly how valuable TIPS and iBonds are for accomplishing that goal.

If preserving wealth is your main goal, I don’t think that putting 50% of your assets in TIPS is crazy. I’m also struggling with the decision of what percentage of my assets I should assign to TIPS. I’m in my 70’s now with about 15% in TIPS and iBonds (0% stocks).

Since the 1980’s, I’ve always been able to beat inflation simply by purchasing 5 year CD’s. As inflation and interest rates have declined, the spread between the two has diminished. For the first time in 40 years, those CD’s are losing big time to inflation (5%+).

As long as TIPS can be purchased with a positive yield, as my CD’s mature I’ll be converting them to TIPS. Right now, I still haven’t decided on what percentage TIPS should be. However, I may just put 100% of my retirement funds into TIPS.

I have a very simple 10 year plan. I’ll be putting 10% of my retirement cash into TIPS each year. This will easily cover the required minimum distribution that I have to make each year now that I’m over 70.

The muddle is what I need to do with my taxable cash. I could just start putting 10% of my taxable cash into iBonds and TIPS. I’ve never had TIPS in a taxable account before. However, I can now stomach paying taxes on phantom interest over losing to inflation.

The reason that I can take such an ultraconservative approach is because both my wife and I are collecting Social Security. As long as us are both alive, we can actually pay all of our recurring expenses with SSI. The survivor will have to dip into the RMDs.

Since you’re “only” 59, you’re going to have to take a long hard look in the mirror and decide if you really will be able to make it thru retirement on the assets that you have accumulated. According to the life expectancy tables, you’ve got at least 25 years left.

On the other had, you don’t want to be one of those people that kept working until he drops dead. Like you said, there’s always a certain amount of stress involved with working even if you enjoy your career. It took me six months to decompress after I retired.

If you want to put lipstick on a pig, just look at TIPS as an inflation adjusted revenue stream with absolutely no fees involved. You’ve got the luxury of being young enough to set-up a 20 year TIPS ladder to protect the money you’ll need in the future.

What a terrific article! You took a complex subject and explained it with such ease, supported with charts and references from other equally reputable sources. I’m GRATEFUL to have the opportunity to read your SMART/VALUABLE articles. I walk away a smart man after every read.

-With gratitude + utmost respect

Well, everytime we get ZIRP and QE TIPS bond yields go negative. One would think that any increase in the interest rates or a reduction in the FED’s “balance sheet” from where were at right now would keep TIPS in positive territory. However, the 5 year TIPS actually went negative again for a few days this past week. It’s finally “rallied” back to +0.29%. That’s lower than the +0.36% yield at the last auction in June. With inflation and interest rates increasing over the last two months who would have “thunk” that would happen?

Yes, shocking. I went into this tightening cycle thinking the 5-year real yield would rise above 1%, just as it did in December 2018 before the Fed gave up. The 5-year TIPS should be most sensitive to the rising federal funds rate, but I think inflation/deflation fears are messing up that theory.

What a great, clear, and timely article! Thank you. It is indeed going to continue to be “interesting times” for the small investor. Wow.

The market value of the bonds has increased, as interest rates declined.

David,

Thanks so much for that highly-important and highly-informative post on a highly-neglected topic. That post raises some questions as to which I’d very much appreciate your opinions, or even just conjectures.

First, why is the Fed moving so slowly on QT?

Second, which would be more likely to bring inflation down more quickly: aggressive raising of interest rates or aggressive QT?

Third, which would negatively affect the stock and bond markets more: aggressive raising of interest rates or aggressive QT?

Fourth, how much more quickly would the inflation rate be coming down if we had simultaneous aggressive raising of interest rates and aggressive QT?

Fifth, why did Powell make that statement on Wednesday which is so contrary to the facts?

Sixth, is there any connection between that misstatement by Powell and his strange statement on Wednesday that the stock and bond markets used to justify their continued euphoria (at least for the remainder of last week)?

Seventh, and finally, why has the business media generally been so silent on the issues raised by your post and the Barron’s article?

I imagine that the Barrons article may provide some answers to those questions. But I don’t have a subscription to Barrons, and I imagine that many other readers of Tipswatch don’t either.

Brian, great questions. I think the Fed is moving slowly on QT to see how the market reacts and it knows that the last bout of QT (2018-19) ended up creating chaos in bond markets. On interest rates, the Fed can really only “control” short-term rates and this is being demonstrated again with the flattening of the yield curve. It could flood the market by selling off longer-term bonds (not just waiting for maturation) and boost long-term rates, but I doubt it will do that. The Fed has decided to raise short-term rates aggressively, hoping that will send a needed message to the markets. But then Powell seems to walk it back, walk it forward. This is a tightrope.

A decade of quantitative easing created huge liquidity, sending cash sloshing through the financial markets. That boosted the stock market, but also highly speculative investments like meme stocks and bitcoin. Quantitative tightening should have the reverse effect, but who knows? And would this even have any effect on inflation, since inflation is a global problem? Will we just end up with stagflation?

I thought “Other Points to Consider” at the bottom tells it all, https://www.ubs.com/global/en/wealth-management/insights/chief-investment-office/market-insights/2019/quantitative-tightening-impact.html

What’s especially interesting is that this UBS article was written in 2019, before the Fed’s massive pandemic-era ramp up of bond-buying.