Confusing? Aggravating? Of course, but also correct.

By David Enna, Tipswatch.com

I’ve had several communications recently from readers who are new to U.S. Series I Savings Bonds and freaking out by the apparently low interest payments reported so far on the TreasuryDirect website. Here’s an example from this week:

After fourteen months, the value of my (March) 2021 bond has increased only 3.84%, or by $384. If the bonds truly tracked inflation, they would have increased by at least $850 – one year at 8.5% plus another two months’ interest. … I suspect the 6-month calculation period is the clever “trick” by which the government sees offering these bonds as worthwhile. It is what gives the house the advantage. … I feel swindled.

First of all, and most importantly, the Treasury is not swindling anyone. I Bonds do accurately track official U.S. inflation, but investors need to keep in mind that the I Bond’s current variable rate is set by inflation six months in the past. Eventually, if you hold them, all I Bonds catch up to current U.S. inflation (either up or down).

This particular reader purchased $10,000 in I Bonds in March 2021 and then $10,000 again in March 2022. In my opinion, those were excellent investments. But the reader has looked at the TreasuryDirect website and sees his two I Bonds have earned only $500 in interest so far, when current U.S. inflation is running at 9.1%. He asks: “Why?” (And he is not alone. I get this sort of question several times a week.)

Note: I wrote an updated article on the Treasury’s interest rate calculations. View it here.

What is happening here?

The key issue is that I Bonds cannot be redeemed for one year, and I Bonds redeemed from year one until year five will lose the last three months of interest. When you look at your I Bond earnings on TreasuryDirect — if you haven’t yet held them 5 years — the interest that TreasuryDirect reports WILL NOT include the latest three months of interest.

A second issue is that when I Bonds are issued, they earn the current variable rate for a full six months before transitioning to the next variable rate, and so on, every six months. Eventually, all I Bond holders get exactly the same variable rates, but the trigger dates are staggered by the month of issue.

In the case of this reader, the I Bonds were purchased in March, which means that the variable rate will update each September and March. This is crucial for understanding the interest calculation.

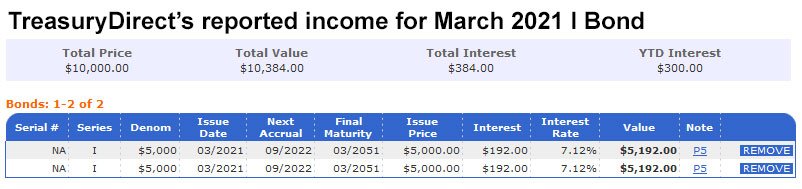

Example one: I Bond issued in March 2021

I used TreasuryDirect’s Savings Bond Calculator to get the current value of a $10,000 I Bond issued in March 2021. Because the calculator is supposedly “only” for paper I Bonds, I had to enter $5,000 twice into the calculator. Here is the result:

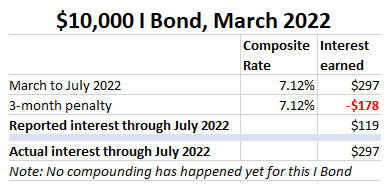

The reader was correct in noting that this I Bond had only earned $384 in reported interest since March 2021. Why is that? One factor is that in March 2021, the I Bond’s composite rate was 1.68% (fixed rate of 0.0% + variable rate of 1.68%) for a full six months. And now I will let my chart take over:

Well, look! … This March 2021 I Bond has not yet started earning the current 9.62% composite interest rate because it is still in the six-month period earning 7.12% interest, though this month. In September, the I Bond will begin earning 9.62%, earning at least $482 over the September to February period.

My total of $380 differs from TreasuryDirect’s $384 because of compounding, but close enough.

The I Bond so far has earned $558 in interest (actually a little more with compounding), but TreasuryDirect will only report $384 because it will always eliminate the last three months of interest for an I Bond that hasn’t yet hit the 5-year mark.

A bit of advice: Before redeeming any I Bond before 5 years, make sure to check the term of the current composite rate. In this March 2021 example, you wouldn’t want to sell the I Bond until three months after the 9.62% rate runs its course. That would be June 2023, at the earliest, but the next variable rate could be nearly as high.

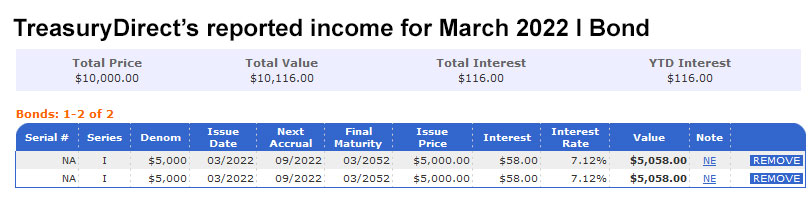

Example two: I Bond issued March 2022

Here is TreasuryDirect’s calculation:

This one is a lot simpler. TreasuryDirect says that this I Bond has earned $116 interest so far. Again, the composite rate is 7.12% through August, and then will transition to 9.62% from September to February.

Here’s my calculation of how this interest was determined:

In this case, my calculation matches the TreasuryDirect number because no compounding has yet taken place for this I Bond. The first accrual will be in September, so the principal balance will climb a bit just as the 9.62% interest rate kicks in.

Final thoughts

I may be weird, but I actually trust the way the Treasury reports my I Bond interest, but I know all about the quirks of the three-month penalty and staggered variable rates. I recently redeemed EE Bonds we purchased in 1992 and the Savings Bond Calculator nailed our proceeds to the penny. The Treasury is not looking to cheat Savings Bond investors, I am certain of that.

Not everything in life is a conspiracy to cheat you. Savings Bonds are a trustworthy investment.

• Confused by I Bonds? Read my Q&A on I Bonds

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Let’s ‘try’ to clarify how an I Bond’s interest is calculated | Treasury Inflation-Protected Securities

Could you explain how compounding works for I bond interest. Is it 6 months?

Interest is earned monthly, and the total compounds every six months. From then on, interest is applied to the new principal amount.

Hi Tipswatch,

I wanted to find out the historical rates of return for the Series I Bonds. I searched the TreasuryDirect.gov website and found the link to I Bond Interest Rates. That page explains how the “I bonds earn a combined rate of interest” and states the following:

“the interest on I bonds is a combination of:

a fixed rate

a inflation rate”

The page explains the Fixed Rate and the Inflation Rate, and ultimately there is a section for “Current Composite Rate” and a table for historical Composite Rates.

When I look at Composite Rate table it is stated to be the following: “The table below shows the current composite rate for all I bonds. Each composite rate is a yearly rate that applies for 6 months.”

I’m thinking it’s the historical interest for the I bonds. It shows a rate range from 2022 to 1988, and a range of rates from current 2022 at 9.62% to latter years at over 13%, no lower rates than 9.62%. As I look at all the returns I shake my head and think “this table is not telling me the historical returns for I bonds because it doesn’t make sense when compared to how the Fixed Rate and Inflation Rates are calculated, and they are way too high”.

Can someone explain to me what this “Current Composite Rate” table is showing????

It is showing the CURRENT composite rate, which is 9.62% + the i Bond’s fixed rate. It isn’t a historical rate of return. I don’t know of any site that has that specific information for all I Bonds ever issued. Probably exists, somewhere.

So I see the CURRENT composite rate at 9.62%, which I know I will get that 6 mo return on my I Bond.

But how does, for example, say the line with Nov. 2005 to April 2006 at 10.67% make any sense, or any of the other lines? The I Bonds were not consistently giving 9-13% returns for the past 30+ years.

The following website shows the historical returns for last 10+ years and they are significantly lower than what is shown on the “Current Composite Rate” table.

http://kirklindstrom.com/Articles/I_Bond_Rate_History.html

Can you provide an explanation of the older rates shown on the “Current Composite Rate” table shown on TreasuryDirect.gov website?

Dave, you quoted “Each composite rate is a yearly rate that applies for 6 months.” Each I Bond has a permanent fixed rate and a variable rate that changes every six months. That current composite rate listing is showing the rate now in effect — for six months — for I Bonds that had fixed rates of 0.0% and above 0.0%. Back in Nov 2005 the fixed rate was 1.0% so the composite rate works out to 10.67%, based on the Treasury’s formula. That is the current composite rate and it lasts for six months for the I Bond issued in Nov. 2005. Please, read my Q&A on I Bonds: https://tipswatch.com/qa-on-i-bonds/

When I calculate for Nov 2005 – April 2006, the result is 6.73% (not 10.67% shown in the “Current Composite Rate” table):

[1% + (2 x 2.85%) + (1% x 2.85%)] = 6.73%

How did you calculate to 10.67%?

Below are a few more randomly chosen dates for calculating a rate for a 6 month period. The results between what I calculate and the numbers shown on the TreasuryDirect.gov are different, why is that???

May 1999 – Oct 1999, the result is 5.05% (not 13.08%)

[3.3% + (2 x 0.86%) + (3.3% x 0.86%)] = 5.05%

May 2011 – Oct 2011, the result is 4.60% (not 9.62%)

[0% + (2 x 2.30%) + (0% x 2.30%)] = 4.60%

Nov 15 – April 2016, the result is 1.64% (not 9.72%)

[0.10% + (2 x 0.77%) + (0.10% x 0.77%)] = 1.64%

Dave, you are misunderstanding the concept of “current composite rate.” What is listed is the CURRENT composite rate, meaning the rate that is CURRENTLY being earned by that I Bond issued in that year. CURRENT means right now, for six months in 2022. If the fixed rate of an I Bond is 1.0%, and the variable rate is currently 9.62%, it is currently earning 1.0% + 9.62% = 10.67% with compounding. Stop overthinking this. The current composite rate is the rate the I Bond is earning RIGHT NOW for six months.

Buy the bond on the last day of the month and sell it on the first and the penalty is actually one month and a day. Assume I buy an I bond on 8/31/22 and sell on 10/1/23. I will have had my money invested for thirteen months and a day but have received fifteen interest payments. When Treasury takes the last three I will be left with twelve months of interest. Assuming that I am selling the bond because its rate is declining my penalty will be a month of the lowest rate.

It’s true you can earn a full month by buying late in the month, but you have to hold the I Bond until the last day of the month to get interest for that month. Selling early in the month is fine, but you don’t get that month’s interest.

Thanks. Can you give me a reference on that? I can only see where internet accrues on the 1st.

I researched this a few years ago, can’t seem to find the reference. It probably came up in the Bogleheads forum. When you buy an I Bond near the end of the month, you own it on the last day of the month, so you get that interest payment on the 1st of the next month for the month of purchase. When you sell an I Bond before the last day of the month, you won’t get interest for that month. The last day of the month is the trigger.

Although I cannot find a reference for how interest is calculated in the final month, it appears on closer examination that you are correct. Bonds I bought in April of this year are showing one months interest and those bought in May are showing none. That would mean that those bought in April will have eleven months of interest posted as of June 1st of next year making the interest penalty two months of interest if I sold them on june 1st of 2023. Buying I bonds at the end of a month makes the interest penalty for selling in less than five years equal to two months of interest.

So always sell on the last day of the month to get that months interest?

Actually, I’d suggest waiting until the first days of the next month, to be safe.

I created a spreadsheet and I’m stumped. I purchased $10k with an issue date of Jan 2022. TD shows a current value of $10,236; interest of $236 earned. From Jan to July (7 months), my understanding is that I should have $237.33 of interest (7.12% for the first 4 months of the year excluding the last 3 months of “penalty”). What’s the explanation? My last 3 months of penalty earns at 7.12% for May and June, and 9.62% for July, right?

Thanks

You are correct that the 9.62% would start in July and your current penalty period is the months of May June and July, since you haven’t completed August. So yeah, it looks like you should have $237 in interest.

The TD savings calculator also shows interest of $236.00, not $237.33 (for $10k issued on 1/2022). This is consistent with my acct displayed value. $236.00 interest equates to a rate of 7.08% not 7.12%. Is the $1.33 discrepancy due to interest rate rounding, acct value rounding or something else?

I’d say it does look like rounding. One-sixth of $356 is $59.33, round down to $59 and you get to $236.

I did some Googling, and I think I found an explanation. My interest calculation was off. Check out DiamondNestEgg on Youtube…she walks through how to calculate the interest in a recent video.

Hello! I am the guy who’s message to tipswatch prompted this article.

I would like to clarify: I was not accusing the U.S. Treasury of misrepresenting the interest earned. Of course they are not doing this, it would be fraud on a massive scale. Instead, I was pointing out how those suggesting that “I Bonds accurately track inflation” are incorrect.

As the analysis in this article demonstrates, even accounting for the 3-month penalty, the I bonds still did not accurately track inflation. The “actual interest” stated above is about 5.58%, where year over year inflation was 8.5%. In order for the statement “I bonds accurately track inflation” to be accurate, the bonds would need to earn interest at a rate equal to the inflation rate. But as you saw above, they do not…

In other words, the wealth, the purchasing power I placed into I bonds has decreased since I purchased the bonds. Their value increased by 5.5% and inflation ate away at their value by 8.5%. Plus, most will have to pay tax on the 5.5% earnings.

My comments about feeling swindled arose from some delicate language I see in statements about I bonds, on this website and elsewhere. Here is a statement from this website’s Q&A on I Bonds:

“If inflation in the next 30 years suddenly soars to 7%, 10%, 15%, your principal will increase by that amount because of the inflation-adjusted interest rate.”

This is demonstrably untrue, as in the above article. Principal increases don’t always match the inflation rate.

However here is another statement from the I Bond Manifesto on this site:

“They offer inflation protection.”

A much softer claim that is accurate. The bonds do offer some protection, but not all.

Remember, the treasury offers bonds in order to make money, they don’t do it to be nice and give people free money – even if you earn a bit, they still come out ahead. Economists and actuaries at the treasury investigated the financial sense of offering an inflation protected bond and concluded accurately that they would not make any money if the bonds earned at the exact inflation rate. They needed to add some house edge, such as the requirement that he bonds be held for at least 1 year, the 30-year lifespan, the 3-month penalty, and the 6-month delay in calculation. Adding those rules to the algorithm lets them “keep” money they would otherwise have to pay out, such as when people cash out bonds early, when they don’t cash them out after 30 years, or when inflation rises steeply over a one year period and principals are not paid at the yoy inflation rate. This keeping is how they make their money, and if you look on the treasury website, they make no claims about full inflation protection. They are just bonds that enjoy an inflation adjusted rate. No more, no less.

There are situations where I bonds work out well. In my case, I do have educational expenses so I will not have to pay tax, and even 5.5% isn’t bad. But to be sure, my bonds did not earn the same amount as they would have to in order to be fully protected from inflation. They didn’t this year and unless inflation falls and I start earning a 6-month calculation that is higher than actual inflation (as I would in a period of declining inflation), I will continue to lose purchasing power in the face of increased prices. To be a truly safe investment, inflation must go up, /and then also back down/, so that these bonds accurately track inflation.

Who knows if they will, even in 30 years? This is still gambling!

Can I just point out that your I Bonds are about to earn 9.62% for a full six months, while inflation will probably be lower? And then maybe 8% while inflation is even lower? I Bonds do accurately track inflation, yes with a lag time because the rate is based on a past six month period. Over time, I Bonds accurately track inflation, because the rate is based on actual inflation. It is not gambling. It is not misleading.

“To be a truly safe investment, inflation must go up, /and then also back down/, so that these bonds accurately track inflation.”

That’s the thing, over time Inflation rates do go up and down. Yes, while inflation rates are on the upswing, the I-bonds are lagging behind at a lower rate, but when the rates go back on the downswing (as they will), the I-bonds will lag behind at a higher rate. Over time the ups and downs even out.

So yes, the I-bonds do accurately track inflation, it’s just that there is a lag factor to consider.

It seems like there is a strategy here. Inflation runs in a somewhat predictable cycle at least when one looks out over the forward twelve months. I bond pricing is also predicatable. In a couple of weeks we will know five of the six data points used to set I bond rates for November. If you load up on I bonds in the months leading up to and immediately after an inflation peak you should be getting above inflation returns. Roll out of them when inflation troughs taking a two month penalty at the lowest return rates and moving into higher yielding fixed income investments. Repeat again at the next cycle. What am I missing?

This is a legit short-term strategy. My strategy is to hold for the long term, until I need the money. Also, for clarity, the interest penalty is the last three months, not two, even if you shortened the holding period by buying late in a month.

David,

Nice explanation. Though the info is all contained, it might be worth making it more explicit just how long the delay can be before the “correct/current” interest actually shows up in the Treasury Direct account balance. In this particular case, the monthly interest accumulated as shown in the TD balances will lag the current rate by a full 9-months; 1 month short of the max 10-month lag (for iBonds purchased in Apr or Oct).

That is, the 3-month penalty window stacks with a 5-month lag in rate paid and also stacks with a 1-month delay because the interest is only paid monthly, in arrears.

You state that the letter writer’s rate will jump to 9.62% starting in Sept. Though that’s true, it STILL won’t show up in the account balance on TD until Jan 1, 2023. Rather, the increase to the balance(s) will reflect a previous month @7.12% rate rolling out of the penalty window. Specifically on Sept 1, the interest earned during the month of May will be added to the TD balances.

OK, obviously the 9.62% rate won’t show up in the TD reporting until three months have passed, but the I Bond is actually earning interest at 9.62% annualized through those three months. It is still in the penalty period. There is no 5-month lag that I know of; are you talking about when TD posts the accrual, which creates compounding? That happens every six months, but the interest is actually earned once each month is complete. Interest for August will be earned on September 1, for example.

No, the 5-month lag I’m referring to is just relative to the “current” announced rate. That is, because it’s purchased in March, the rate “lags” announced rates by 5 months. That’s why in the example, the 9.62% rate doesn’t kick in until Sept (and not actually paid until Jan 1) as opposed to May when it was announced. I know you know this, I was just trying to illustrate why people aren’t seeing their balances increase as much as they expect (yet).

I know this isn’t a negative, everybody gets basically the same payments eventually. I only mention it because of big jumps recently in rates and all the headlines about iBonds, lots of folks who’ve recently jumped into iBonds (including the letter writer) are concerned they’re not getting the appropriate interest. I’m just pointing out that when the Treasury announced the juicy 9.62% rate in May, some people won’t actually see that rate of interest start to add to their account balance for up to 10-months until Feb 1, 2023.

I ended up making a spreadsheet in Excel. Not so much due to trust, but curiosity. I extended it out for a couple of years with monthly increments. All I have to do is type in the rate for the six months and it changes the “how much would they be worth” value. I also included the penalty. Sure some might be “worth” $522, but I could only get them at $296. Of course I couldn’t even do that since they haven’t been held for a year. With inflation still running rampant I don’t plan on touch them anytime soon. However, with a fixed rate of 0% and eventually getting a low/negative variable rate I might get rid of them and invest elsewhere after 0% interest for three months. Hey, it’s a way to dodge the penalty, no? However, there still might not be a better place. With the $10,000 limit, it’ll at least be stocked away for the next storm.

Yes, the correct selling strategy is: If you need the money for any reason, and the composite rate is very low, that is a good time to sell. If you haven’t held the I Bonds 5 years, wait out the three months of low interest and then sell. …. But only if you need the money.

I agree with Mr. Enna. I have almost $200K in I-bonds, so I have been doing this for a while. Don’t worry about the way interest is calculated. It is pretty complicated. Just go to the I-bond interest calculator at the Treasury web site and input your data and get your interest.

For a position that large I assume you’ve been adding for 8-10 years? What’s the range of the weighted average return over 5-10 years?

I bought in the early 2000s when you could buy $30,000 in one year and the base rate was around 3%. Total is actually around $300,000. Well over half of that is interest gained. But it was not all clear sailing. Some periods I earned 0% interest. Fortunately, I-bond rules say you cannot lose money ever, so even in disinflationary periods, I did not lose anything.

It would be useful if Tipswatch would write an article about how to minimize taxes as one approaches the 30 year limit. I’ll probably redeem gradually from years 27 to 30. I’ll have to do the math.

Great site, Mr. Enna.

Yes, a couple can accumulate $200,000 in I Bonds in 10 years just buy buying each person’s limit every year. This is not difficult. For dedicated I Bond investors, it is a very common practice.

I also recommend being careful about redeeming EE bonds. The interest to maturity may be huge given that they double in value after 20 years.

Excellent point. For the newer EE Bonds, it’s important to hold them 20 years and then immediately redeem, since they revert back to the fixed rate of 0.1%. But you also have the flexibility to wait a year or two to take the redemption in a year you can limit the tax burden.

Thank you, David, for the information that you recently redeemed one of your EE bonds. That reminds me that My EE bonds issued 7/1/2003 will have reached 20th year anniversary on 7/1/2023, in less than one year from now. Currently it has a fixed rate of 1.6%. After the 20th year anniversary, will the bonds revert back to 0.1% or will it continue to have 1.6%. I assume this EE bonds will double in value in 20th year. If it reverts back to 0.1%, I might redeem it.

EE Bonds in the past had all sorts of terms. The ones I bought in 1992 doubled in value in 12 years (6% effective interest) and then paid 4% for the next 18 years. That was very nice. According to TreasuryDirect, EE Bonds issued from May 1997 through April 2005 earn a variable rate of interest. And right now for your EE Bond that rate is 1.6%. It looks to me like yours will double in value in July 2023 and then will earn a variable rate of interest after that. You can at least see the current variable rate using the Savings Bond Calculator: https://treasurydirect.gov/BC/SBCPrice

Nice example. Too bad either the Treasury or someone else could have a website where your ladder of bonds could be entered and automatically calculate this information without having to massage it. Hoping to hold mine for the 5 year period adding each year and then as rates fall pull out some every month, pay the taxes and supplement my income if needed. Better than a stick in the eye right now though it’s not a real return given the actual inflation rate.

You can use the Savings Bond Calculator, even though “technically” it is for paper I Bonds only. It appears to be accurate for electronic I Bonds, too. I wrote a step-by-step guide back in 2018: https://tipswatch.com/2018/06/04/heres-a-step-by-step-guide-to-using-the-treasurys-new-savings-bond-calculator/

The one caveat with the calculator is it also has the paper bonds limit for bond size ($5k). so if you want to track your $10K electronic bond, you have to play around with it a bit (use $5k and double the result or use $1k and multiply result by 10).

Yes, I just enter all my $10,000 purchases as two $5,000 purchases. I don’t bother with serial numbers, but I do make note of the fixed rate, in case I want to roll over 0.0% I Bonds later on.

The Savings Bond Calculator gives the same results for paper and electronic I-bonds.

Great explanation and wisdom.

Ditto!

The next reset rate should still be fairly attractive? I’ve maxed out for 2022 – but should be able to allocate in Jan-23, capturing the Nov-22 rate correct? Thank you for all of the helpful information here!!

At this point, I think the November reset should be to about 8%, but inflation is going to be tricky this summer. Tomorrow’s report will tell us a lot. The consensus is for an all-items increase of 0.2% because of falling gas prices. Non-seasonal inflation could take a hit since we expect gas prices to increase in the summer.

Do you still think there will be little chance of a fixed component for November new issues?

At this point, “little chance” with the 10-year real yield at just 0.38%. The variable rate is going to still be pretty high and the Treasury could pass on raising the fixed rate and still see plenty of demand for I Bonds in 2023. I am not ruling out a higher fixed rate, though. Let’s see what happens in the next 3 months.

I doubt if the fixed rate will ever be much higher than zero. There is no incentive for the government to raise it. Remember, they have never told us how it is constructed. Buy I-bonds for inflation protection, i.e., for the variable rate.

Thanks so much! I think in the first calc table, second line, the time period should be Sept-Feb rather than Sept April.

Thank you Robert, this is fixed.