Investors benefited from turmoil in the financial markets.

By David Enna, Tipswatch.com

In the midst of a highly volatile bond market, the Treasury’s offering of a reopened 10-year TIPS — CUSIP 91282CEZ0 — generated a real to maturity of 1.248%, the highest for any auction of this term since July 2010.

This was a stunning result, but also predicable, after the Federal Reserve yesterday made clear its intention to battle soaring U.S. inflation to the bitter end, suggesting increases in interest rates would continue well into 2023.

The result was also historic, because the real yield was the highest for any TIPS auction of the 9- to 10-year term since July 8, 2010, when a new issue 10-year TIPS got a real yield of 1.295%. Since then, there have been 73 TIPS auctions of this term, all of them with real yields below 1.2%. Until today. And it is amazing to consider that less than a year ago, on Nov. 18, 2021, a 10-year TIPS reopening got an all-time low real yield of -1.145%, 293 basis points below today’s result.

At times this morning, this TIPS was trading on the secondary market with a real yield of 1.28%, so the auction ended up a bit lower, indicating strong demand. The bid-to-cover ratio was 2.54, also indicating decent demand.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.248% means an investment in this TIPS will exceed U.S. inflation by 1.248% for the next 9 years, 10 months.

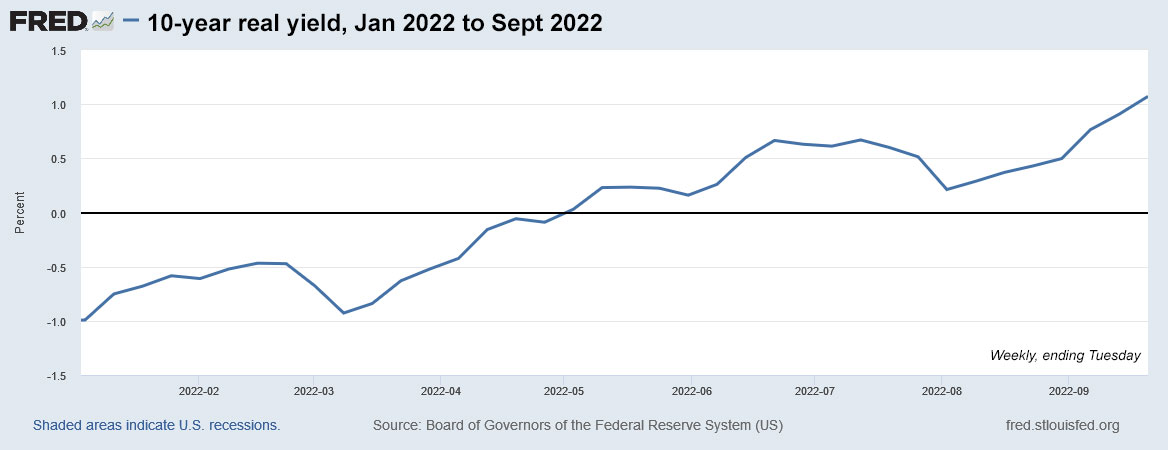

Here is the year-to-date trend in 10-year real yields, showing the steady surge higher since the Federal Reserve unveiled its inflation-fighting plans in March:

Pricing for the auction

CUSIP 91282CEZ0 carries a coupon rate of 0.625%, set at the originating auction two months ago, on July 21, when it auctioned with a real yield of 0.630% (attractive at the time, remember?). Because today’s real yield was nearly double the coupon rate, buyers got it at a substantial discount — an unadjusted price of about $94.27 for $100 of par value.

This TIPS will have an inflation index of 1.01972 on the settlement date of Sept. 30, so investors bought an additional 1.97% of principal, plus about 13 cents of accrued interest per $100. The adjusted price was about $96.13 for about $101.97 of principal, once accrued inflation is added in.

An investor putting in an order for $10,000 of this TIPS paid about $9,613 for about $10,197 of principal, as of September 30.

Inflation breakeven rate

With a 10-year nominal Treasury trading with a real yield of 3.68% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.43%, meaning it will out-perform the nominal Treasury if inflation averages more than 2.43% over the next 10 years. That result is in line with most auctions over the last two years.

Although 2.43% for a 10-year inflation breakeven rate is historically high, it seems very reasonable at a time when U.S. inflation is running at 8.3%. Inflation over the last 10 years, ending in August, has averaged 2.5%.

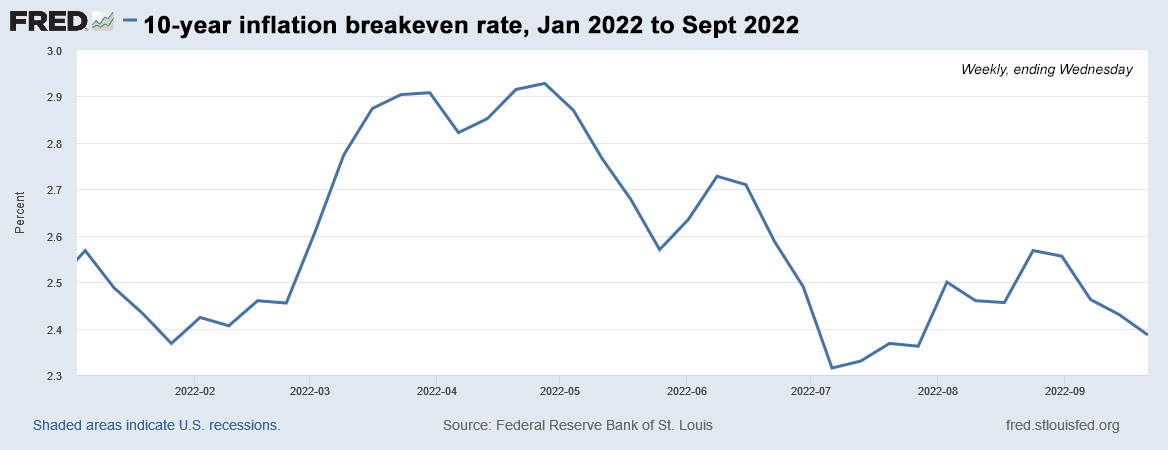

Here is the year-to-date trend in the 10-year inflation breakeven rate, a rather wild track higher into the spring and then much lower through the summer. The financial markets are buying the premise that the Federal Reserve can get U.S. inflation under control.

Reaction to the auction

Investors in today’s auction (I was one of them) benefited from the Fed’s hawkish statements Wednesday and the market disruptions they caused. For investors, getting the highest real yield for this term in more than 12 years was very, very welcome.

As I noted, the auction’s real yield result was actually a bit lower than where this TIPS was trading before the auction close, which indicated decent demand. After the auction’s close at 1 p.m., the TIP ETF — which holds the full range of maturities — got a slight boost higher. It had been trading substantially lower all morning.

The TIPS market has been largely ignored by investors for several years. That includes small-scale investors who have been piling into inflation-tracking I Bonds with a gaudy current annualized rate of 9.62%. But I Bonds carry a real yield of 0.0%, based on the current fixed rate. This 9-year, 10-month TIPS has a real yield of 1.248%. That’s a 125 basis-point advantage.

I Bonds have many advantages over a TIPS: flexible maturity, better deflation protection, tax-deferred interest, ease of ownership. But at this point, as long as real yields remain substantially positive, TIPS are a highly attractive investment to add to your inflation-fighting arsenal.

Here is a history of 9- to 10-year TIPS auctions over the last three years:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Uncertainty surrounds this week’s 10-year TIPS auction | Treasury Inflation-Protected Securities

I read Jimbo’s post and of particular interest is “For example, last week I purchased a 5 year TIPS with an inflation adjusted price of $98.72. The worst case scenario is that I’ll get $100 back when the TIPS bond matures. That’s a gain of $1.28 (plus accued interest)”.

In seeing today’s price of the 04/2027 TIPS do you think it is worth buying this now on the secondary market and/or waiting for the Oct 20 new 5 year issue?

I personally don’t buy TIPS on the secondary market, so I don’t have an opinion. If you see a yield you like on the secondary market, make the purchase. Yields are highly volatile right now, so anything can happen.

If a TIP Bond on the secondary market has a YTM > the yield at auction of a similar term TIP bond, is the secondary market bond a better investment? Is it that simple?

Buying a TIPS on the secondary market is a little more complicated, possibly, because there is a market price factor plus an inflation accrual. But the real yields should be similar for that TIPS if it is being reopened at auction. A lot of people buy on the secondary market and like seeing exactly what they will get, which isn’t true for the auction. But at the auction, a non-competitive bidder always gets the “high yield,” and that is an advantage over competitive bidders.

Hi, just found your site through a Diamond Nest Egg video. Good stuff, and I “think” I am learning.

One question, if anyone can point me to a link to similar or if the TIP ETF reacts similarly — in my 401k my only option is DIPSX, inflation protected securities, which I moved a good portion of my 401k into back in January.

From a NAV it has performed very poorly in my view, supposedly acting as inflation protection. Certainly I am making some of the loss back through dividends, but how should I correctly view such a fund when the only obvious indicator is the NAV ticking down literally day after day?

Thanks!

TIPS mutual funds and ETFs have been hard hit this year because of rising real yields; higher real yields lower the market value of a TIPS and causes the NAV to decline. DIPSX has a total return of -13.12% year to date, and this factors in the inflation accruals and coupon payments. The fund has an effective duration of 7.11 years, meaning it should decline about 7.1% when real yields rise 100 basis points. On January 1, the 10-year TIPS had a real yield of -0.97% and today that real yield is 1.56%, an increase of 253 basis points, which would equate to a decline of about 18% in NAV (roughly). So even with the inflation accruals, you can see how you get to a total return of -13.12%. Real yields have soared in the last week; rather remarkable.

My thinking is that much of the interest rate risk in these funds has washed out, but I also thought that two weeks ago, before this latest surge higher. … One alternative would be to buy individual TIPS and hold them to maturity, which allows you to ignore market fluctuations. But you can’t do that in a 401k.

Thank you for the detailed and understandable answer!

Not asking for financial advice here, but if I agree that we are nearer to the peak in rates than not, averaging down into this fund now is a relatively lower risk proposition than it was a few weeks or months ago? I would buy individual TIPs but cannot in my 401k.

Yes, I do think these TIPS funds get less risky as real yields increase. Of course, inflation could also come tumbling down. As some point, I believe, the Fed will back off and possibly even move to stimulate the economy. But they can’t do that in 2022 or even early 2023.

You know things are getting weird when even Marketwatch is singing the praises of TIPS (albeit grudgingly).

https://www.marketwatch.com/story/want-to-gamble-your-savings-on-a-quick-collapse-in-inflation-11664202818?siteid=yhoof2

That’s a surprisingly intelligent article. I’m reaching the point where I will probably supplement my TIPS purchases, which will continue, with a 5-year Treasurys yielding 4% or higher. Hedge my bets for 1) the day the Fed caves or 2) the day the economy collapses.

I’m near retirement age but completely new to TIPS so trying to educate myself. I love math but am a bit confused by the financial concepts around TIPS. From reading David’s super informative explanations on this site, I understand that the total final value (FV) of a TIPS would simply be the par value (PV) + accrued interest + accrued principal adjustments (right?). But is there also a way to calculate (model) FV using the real yield at auction (RY)? For example if we bought a 5 yr TIPS in Dec 2015 and kept it to maturity, is the following method valid?

FV = PV x (1 + [RY×5 + CI]/100), where

CI is cumulative annual inflation % during the 5 yr (2016-2020 inclusive in this example).

To use concrete #s….Suppose we bought the above TIPS, then is it valid to use the CPI % numbers from say here: https://www.minneapolisfed.org/about-us/monetary-policy/inflation-calculator/consumer-price-index-1913-

….and calculate that since CI = 8.8% from 2016-2020, if the auction had RY = 1%, then

FV = PV*(1+0.05+0.088) = 1.138*PV (???)

My hunch is this method probably misses something….if so, does anyone know another way to use RY to get FV? I don’t really get the point of knowing RY if it can’t be used to get FV somehow.

A couple things to consider: The final payment at maturity actually only includes one final coupon payment, since all the previous coupons were paid out semi-annually in real time. The second thing is to look at this site: http://eyebonds.info/tips/index.html …. It gives historical data for (I think) all TIPS in history, including the CPI indexes. … The real yield of a TIPS is set for the purchaser at the purchase, based on the discount or premium to the coupon rate. From then on it is just coupon rate paid in real time + principal rising and falling with inflation. So day to day it changes. When you buy a TIPS, you have a real yield set in stone: That is the yield above or below inflation you will receive for the term of the TIPS.

Thanks David. Still confused by one thing: in light of your last sentence, isn’t there a way to at least approximate the final payout using just the RY and annual CPI #s, as in my equation? Sorry, Forgive me if I’m still not grasping some concept you already explained….But isn’t there any equation out there (or spreadsheet model or whatever) that can do such a calculation? I find equations more intuitive to understand than words for such matters. 🙂

In figuring the final payout, the real yield is irrelevant. The final payment is par value + inflation accrual + the final coupon payment. The real yield would be a factor if you wanted to determine how well your investment did over the term, but doesn’t factor into the amount of the final payment. Do you really want the final payout, or the total investment proceeds, which would include any discount/premium to par at purchase and the semi-annual coupon payments?

Ah, thanks.again, I understand now. Yes it’s the final payout I’m interested in, which I define as the grand total amount we’d get back upon maturity. So I guess the question boils down to whether the inflation accrual term in your equation can be calculated using the annual CPI #s? Going back to my example, would the maturity payout on that hypothetical Dec 2015, 5 yr TIPS simply be

par value x 1.088 x (1+coupon rate)

(.088 being the sum of the 5 annual CPI %’s for 2016-2020)

You could look back at an actual 5-year TIPS issued in 2017. That was CUSIP 912828X39, issued April 15, 2017, with a coupon rate of 0.125%. The index ratio at maturity was 1.16099. So, $100 of this TIPS should have had a payout of $116.10 at maturity, plus the final coupon payment, about 72 cents per $100. This page gives the details: http://eyebonds.info/tips/hist/tips65hista.html

I’m a long time avid reader, first time poster…Some general q’s (for David or anyone else with relevant experience):

I’ve dabbled in tips through Treasury Direct (TD) but never through the secondary market. I looked at Fidelity’s offerings recently and it seems they have lots of tips available (https://fixedincome.fidelity.com/ftgw/fi/FILanding#tbindividual-bonds|tips). But I’m very unclear about some important details:

(1) Are the listed yields actually the tips’ real yields?

(2) Are the purchases essentially instantaneous, i.e. are we basically assured we’ll get the listed (real?) yields?

(3) Are broker-purchased individual tips just as “safe”” as from TD, i.e. are they fully backed by the govt, exempt from non-fed taxes, etc.

(4) If yes to all of the above, is it really worth taking the risk to keep bidding in TD’s auctions?? …Put another way: My main goal is to hold tips to maturity, so wouldn’t it be simpler/safer to just buy on the secondary market since we’d know what yield we’re getting *up front*?? (As another commenter said, it’s the old adage of a bird in the hand….)

….I can’t find clear answers about these particular details despite lots of googling

I use Schwab rather than Fidelity but to get answers to these kinds of questions I’d go straight to the source and call Schwab’s fixed income department. They’re always patient about answering my perpetual-newbie questions. I haven’t used Fidelity for a few decades (long story) but I imagine you’d get similar help from them. All of these answers are Schwab-based:

1. Schwab says on every TIPS quote detail page that the numbers assume no future inflation, so they are the TIPS’ real yields.

2. Schwab enters secondary market bond orders as Fill or Kill, so while there may be a delay of 30 minutes before I see a fill, the fill is at or a hair better than the price quoted on the order entry page.

3. I view the bonds held at a broker as very nearly as safe as those purchased directly through and held at TD. I only buy TIPS in IRA accounts, and I don’t think you can open an IRA at TD, so whether buying secondary or at auction I do it through my broker.

4. Buying at auction, you’re getting the TIPS with very close to a 1.000 inflation factor (especially at the first auction, rather than a reopening auction like this one). Secondary offerings through a broker probably have more deflation risk built in, but if you can find a bond with an inflation-adjusted price below par, that’s probably not an issue.

I’m sure David will have simpler and more precise answers, but I was in the mood to try to think these questions through in writing …

Rusty:

I bought a 12 year TIPS ladder in Fidelity earlier this month. I purchased 9 different CUSIPS online, all in the secondary market, through my IRA account. The website features for buying are very intuitive. You can also call for help and they are very helpful. I used a spreadsheet from #Cruncher at the Bogleheads site to identify the CUSIPS and number of bonds I needed in each rung of my ladder. In response to your questions, my experience at Fidelity was as follows:

1. Yes, those are the real yields. When you buy the bond online you get to review the transaction before actually executing. So you know the yield before you buy. All of the trades were very close, and slightly more favorable, than the prices I was expecting based on my spreadsheet, which was based on the prior day closing. I believe this is because prices were falling the day I purchased. But it is totally transparent.

2. My purchases took a matter of seconds to fill, with one exception. For some reason unknown to me, one order was killed before filling. I simply re-entered the order and it filled almost instantly.

3. and 4. I agree with Woody832 on these two points.

Huge thanks to both of you for the very helpful and thorough replies! A big reason I was asking such details: I was pretty peeved after the last 5 yr TD auction resulted in a substantially lower yield than the market was showing in the days and even hours beforehand. Luckily that was a relatively small sum but now I’m thinking of jumping in with a big chunk of our savings (via fidelity most likely) well before the Oct 20 TD auction, rather than waiting and risking being disappointed with lower-than-market yields again.

Oh one more issue….From what I understand these two big brokerages don’t charge any fees for any treasury transactions? If so I wonder what’s the benefit to them if e.g. a client strictly uses their acct for that purpose….Am I missing something??

You are correct. I was not charged for buying my TIPS ladder and I have bought treasuries at auction many times at Fidelity. I also recently sold some ST treasuries to buy my TIPs ladder. I am never charged anything, even if I call them and get them involved in helping me. I would speculate that it is probably inexpensive for them to provide this service for free, and there is always the possibility they can sell you something.

Could there be a difference for auction purchases and secondary market purchases? I would definitely expect the auction purchases to be commission-free.

My vague recollection is that Schwab doesn’t charge a commission on bond trades but they do add a $10 markup, which seems kind of like the same thing, except that it is included in the quoted price.

Woody832: interesting that Schwab would do that. Is the mark up disclosed in the transaction or just built into the price? I will check on this, but I am pretty sure Fidelity does not charge a mark up, or so they claim. And if Fidelity does not, then I am surprised that Schwab does. I wonder if it is related to the size of the trade or the account? Do you have a large account at Schwab?

Rusty, several readers have given excellent feedback on your questions (I’ve been out of town for several days) and I appreciate their contributions. But I will add a little about preferring to buy at auctions:

This works for me because I write about every auction and that means I am paying extra attention to the yield trends at that moment. A non-competitive bidder always gets the “high” yield in the auction result. This can be significant. In Thursday’s 10-year reopening, the high yield was 1.248% but the median yield won by competitive bidders was 1.180%, substantially lower. Nearly 30% of investors in that auction got less than the high yield.

Secondary market vs. auctions is probably a toss-up, as long as you are getting the actual market real yield in the secondary market, and not a mark-down based on a small purchase. I don’t purchase in the secondary market, so I can’t say, but either way it is just a matter of market timing and either way has a potential to be slightly better.

Many many thanks again to all 3 of you for the very helpful replies! I really appreciate your thoroughness (and patience with my questions!) — gave me lots to think about. Wish you guys continued success with your saving strategies.

Thank you for your knowledge sharing. I am new to TIPS and still trying to learn and absorb everything I read.

I brought this very same TIPS today in the secondary market via Vanguard. The purchase price was $91.789. The Principal was $936 with $1.28 for accrued interest. The cost to me will be $937.28. Unless I am totally backward in my thinking, it will seem what I purchased today is a better deal than if I had bought it during the auction. Is there an absolute advantage in buying during the auction other than if the price increases in the secondary market for the same security after the auction? Or, is this the “beginner’s luck” with this purchase where most of the time secondary market is more expensive?

Real yields have been rising every day since the auction … and for several days before the auction. You caught the wave higher. The opposite can happen, obviously.

Since other people have covered questions 1, 2 and 3 adequately, I just thought that I’d weigh in on the 4th question.

If you can purchase the TIPS bond on the secondary market with an inflation adjusted price at or below par, it’s a pretty safe bet.

That way, you’re guaranteed to get at least your principal back even if there’s deflation for the entire remaining term of the TIPS bond.

For example, last week I purchased a 5 year TIPS with an inflation adjusted price of $98.72.

The worst case scenario is that I’ll get $100 back when the TIPS bond matures. That’s a gain of $1.28 (plus accued interest).

That’s not necessarily the case for all purchases made on the secondary market – or, even at auction re-openings.

Back in July, I purchased a 5 year TIPS bond on the secondary market for $101.18. I’ll be out $1.18 if there’s deflation thru to maturity.

Back in June, I purchased a 5 year TIPS bond at the re-opening auction for $101.22. I could be out $1.22 on that one.

Is it likely that over the course of the remaining term of the bond that there could be enough sustained inflation to result in a loss?

That totally depends on what premium was paid for the TIPS bond and the duration of the remaining term.

If you try to create a 10 year TIPS ladder by purchasing them on the secondary market, the deflation risk increases dramatically.

For most all of the current offerings you’ll be paying a price significantly over par.

Any net deflation over the remaining term of these offerings will result in a loss.

For the ones that I purchased over par we’re talking about needing net deflation for nearly 60 months. And, the loss is 1%.

If you purchase one at $120 with a remaining term of less than a year, both the probability of a loss and the percentage loss increase.

One final observation on purchasing TIPS in the current environment is that you’d better be sure that you can hold them to maturity.

The good news about interest rates going-up is that bond prices are going down. That makes the yields quite attractive right now.

However, for that very same reason the market value of the TIPS that you’ve purchased in the past has gone down as well.

All of the TIPS that I’ve purchased this year look great from the perspective of the current par value (par times inflation factor).

If you have these TIPS in a brokerage, they’ll show you the current market value. And, it’s basically a major nosebleed.

Since I’m just converted maturing CD’s to TIPS, I’ll be doing this over an extended period of time.

How extended that period is depends on how long the TIPS yields remain in the plus column.

Excellent observations Jimbo. Very insightful and through provoking.

I was unable to buy TIPS in my retirement account until about 2 years ago and I am 68 yo and a couple of years from retirement. So I was not able to build my TIPS ladder slowly over time by buying at auction. So in my case, if I wanted a ladder I had to purchase in the secondary market and did so earlier this month.

Just checked my ladder and your observation is correct. If there is significant deflation I will get back less than what I paid — especially on the shorter maturities. For the entire ladder this would amount to about 6.7% of what I paid. I guess I get solace from two things: (1) the reason I bought a TIPS ladder is to lay down a floor of purchasing power, and that does not change if we have deflation. So I am still getting exactly what I paid for. It’s just that I forgo the chance of receiving a windfall if we have major deflation. The role of TIPS in my retirement plan is to insure against unexpected inflation, so that objective is still achieved. (2) I think the chances of sustained deflation are quite low.

Having said this, all else equal, I would have preferred to buy my TIPS at a discount below par and would encourage those who can to do so. But I would not forgo buying TIPS in the secondary market due to the risk of deflation.

Has there been a study comparing the 10 year TIPS vs rolling a 2 year nominal (or 1y, 5y).

I am not aware of a study like that.

Hi David,

I am looking with interest at the 5 yr tips auction on October 20 and have a question about my understanding about TIPS I would like to run by you. If anything is wrong, please correct me!

I believe the official TIPS value in the eyes of the treasury is simply the par value plus any increases (or decreases) in principal due to inflation (or deflation) plus whatever interest payments have been applied since purchase.

However, if the TIPS were sold before maturity, it is possible the market value can be lower and needs to be sold at a discount below the par value if for example yields are higher at that time, but these losses could be offset by whatever increases from inflation (or decreases from deflation) and interest payments have occurred to that point. Even if sold with a discount at the time of sale, the discount could be greater or lesser than any principal increases + interest, thus the TIPS could still be sold at a net gain if principal increases + interest are greater than discount.

If the TIPS were held to maturity, IT WOULD NOT MATTER WHAT THE YIELDS WERE AT THAT TIME, the value of the TIPS at maturity simply equals the par value at purchase plus any increases (or decreases) in principal due to inflation (or deflation) plus whatever interest payments have been applied since purchase, or par value at purchase, whichever is greater.

I hope that makes sense!

thank you

Chris

Yes. At maturity, the value of the TIPS is par value + accrued inflation. Along the way you earn the coupon rate. The real yield to maturity is set by the discount/premium you pay at purchase. After the purchase, it’s par value + accrued inflation with the coupon interest paid out twice a year.

Hi David,

But is my understanding about the market value not being any factor if sold at maturity correct? And if sold before maturity on the open market, any price discount would be offset by any accrued inflation + interest? (to whatever degree)

Is there any sense to wait until December re-opening if one expects that yields will be higher then, or is it basically a wash due to lost principal adjustment?

thanks

Chris

The market value at maturity should match par + inflation accrual + final coupon payment. If sold early, would just depend on the current market value. Inflation doesn’t always go up. On the 5-year, I’ll probably buy in October and December.

I purchased part of a ladder a few weeks ago when my net yield was about 75 bp less than it would be today. Ready to buy some additional rungs but after seeing yields on the rise, I don’t want to move too fast. Thoughts? I know timing interest rates is impossible. Still…. Also, is there anywhere that I can view TIPS yields in real time? Rather than after the market closes?

Well, I passed on this one since I’ve already got enough maturing in 2032. At my age I really don’t like 10 year maturities. I popped for the original issue in order to cover my RMD for 2032 (plus a fudge factor since it’s so far out). I figured even if I’m not around then, my wife will have enough to cover it.

Instead, I purchased some 5 year TIPS on the secondary market. The inflation adjusted price was well under par at $98.72 with a yield of 1.481%.

The “logic” behind this purchase is based on the old adage of “a bird in the hand is worth two in the bush”.

A few days before the last 5 year TIPS re-opening I had the opportunity to purchase some on the secondary market with an inflation adjusted principle below par. I passed on it because I thought that maybe the auction would be a better deal. Then the yields took a nosedive. Lesson learned.

From now on, if there’s TIPS offered with an inflation adjusted price below par for a term that I want and I’ve got some cash laying around, I’m going to buy it. The money I used today was cash that I held back from the 5 year re-opening because I wasn’t to thrilled with the .362% yield.

I’ve got some zero coupon bonds maturing next month that I’m going to use for the 5 year new issue. However, with the bond market flip-flopping from month-to-month from negative yields to nearly 1.5% today who knows what the yields will be by then. It’s been a bizarre year.

The bond market is moving so wildly right now that anything could happen before the 5-year TIPS auction on Oct. 20. But it seems highly unlikely that the Fed will back off before then. Interesting times.

I bought the initial offering but sat this out: I’m expecting the 5-year auction next month to have a similar high coupon. Maybe there’ll even be a positive fixed rate for the I bond when the new rate is posted in November. Good times.

Right now that 5-year looks like a winner. New issue, high coupon rate. On the I Bond, I plan to write about the fixed rate in October, when the reset gets closer. My feeling is that the fixed rate SHOULD rise. Will it? I doubt it, because the Treasury is still overwhelmed by demand for I Bonds and doesn’t need to stoke the flames.

David,

Do you think it is legal for the Treasury to keep the process of determining the fixed rate a mystery, especially where the Federal govt, is usually pretty transparent when it comes to its procedures.

Is it legal? Yes.

Wonder if I-Bonds will carry a fix rate of .5 if the 10 Year real yield stays over 1% to november 1st