Have we passed the peak for real yields? Or is this another head-fake?

By David Enna, Tipswatch.com

Well, that was a wild week. Look back to Nov. 3, when both 5- and 10-year TIPS real yields were closing in on 12-year highs, with the 5-year at 1.82% and the 10-year at 1.74%, based on U.S. Treasury estimates. Then came Thursday’s October inflation report, and everything changed.

October inflation came in well below expectations, only the second downside surprise in more than a year. Annual all-items inflation was running at 7.7%, below estimates of 8.0%, and core inflation came in at 6.3%, below estimates of 6.6%. Both the stock and bond markets took this as a signal the Federal Reserve can soon begin easing future interest rate increases. The S&P 500 soared nearly 6.5% in the next two days. The U.S. bond market — represented by the AGG ETF — rose about 2.1% in a single day (the bond market was closed Friday in honor of Veterans Day).

For bonds, higher prices equal lower yields. And real yields on Treasury Inflation-Protected Securities moved substantially lower from Nov. 3 to Nov. 10, according to Treasury estimates:

- The 5-year real yield fell from 1.82% to 1.48%, a drop of 35 basis points.

- The 10-year real yield fell from 1.74% to 1.43%, a fall of 31 basis points.

- The 30-year real yield fell from 1.76% to 1.58%, a drop of 18 basis points.

And now, on Thursday, the Treasury will offer $15 billion in a reopening auction of CUSIP 91282CEZ0, creating a 9-year, 8-month TIPS. At this point, although real yields are down, this TIPS still looks attractive. But we are entering a week of high uncertainty.

A look at CUSIP 91282CEZ0

Update: 10-year TIPS reopening auction gets real yield of 1.485%, highest in more than 12 years

I’ve been a fan of this TIPS, buying a small amount at the originating auction on July 21, which produced a real yield of maturity of 0.630% and set the coupon rate at 0.625%. At the time, that was the highest coupon for a new TIPS in three years. Then I bought a larger amount in the first reopening on Sept. 22, which boosted the real yield to 1.248%, the highest in more than 12 years.

CUSIP 91282CEZ0 trades on the secondary market, and at the week’s close it had a real yield of 1.40% and a price of $92.98 for $100 of value, according to Bloomberg’s Current Yields page. That quote may include some international trading on Friday, because it is a bit below the Wall Street Journal‘s Thursday real yield estimate of 1.432%.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.40% means an investment in this TIPS will exceed U.S. inflation by 1.40% for 9 years, 8 months. If inflation averages 2.5%, you’d get a nominal return of 3.9%, pretty much on par with a nominal U.S. Treasury. But if inflation averages 4.5%, you’d get a nominal return of 5.9%.

So let’s go with the real yield of 1.40% and price of $92.98, which is below par value because the real yield is currently well above the coupon rate of 0.625%. This TIPS will carry an inflation index of 1.02147 on the settlement date of Nov. 30. That means investors will be paying about $94.98 for $102.15 of accrued value, plus maybe 23 cents more for accrued interest.

An investor buying $10,000 in par value of this TIPS will pay about $9,521 for about $10,215 in accrued value plus $23 in accrued interest. That is a rough estimate and things can change before Thursday.

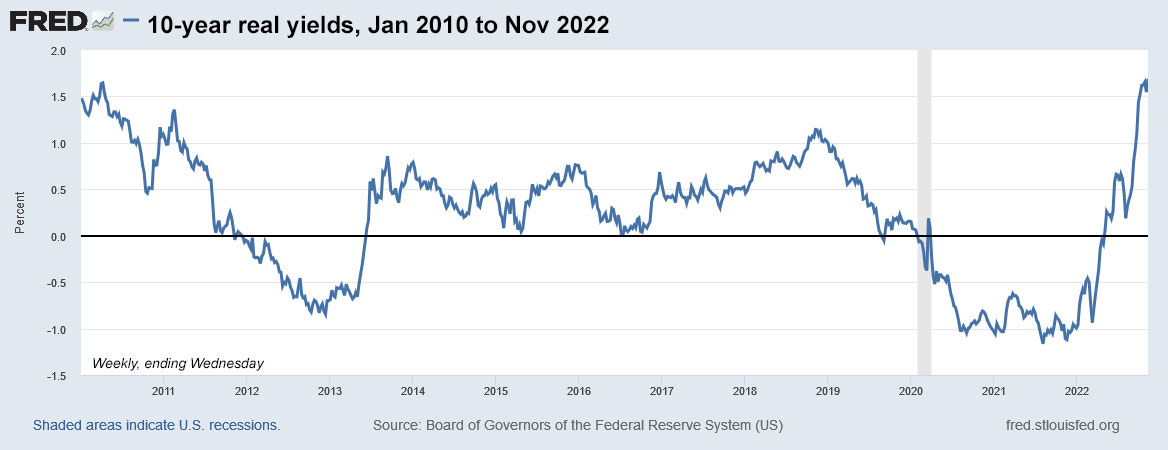

It’s still attractive. While we might have been dreaming two weeks ago of 10-year real yields reaching 2.0% or higher, a yield in the range of 1.40% is still attractive, at least in view of the past decade of ultra-low interest rates. It would be the highest real yield for any 9- to 10-year TIPS auction since April 2010, when a 10-year TIPS reopening auction got a real yield of 1.709%.

Here is the trend in the 10-year real yield over the last 12 years, showing that current yields remain at decade-old highs:

• Confused by TIPS? Read my Q&A on TIPS

• Upcoming schedule of TIPS auctions

Inflation breakeven rate

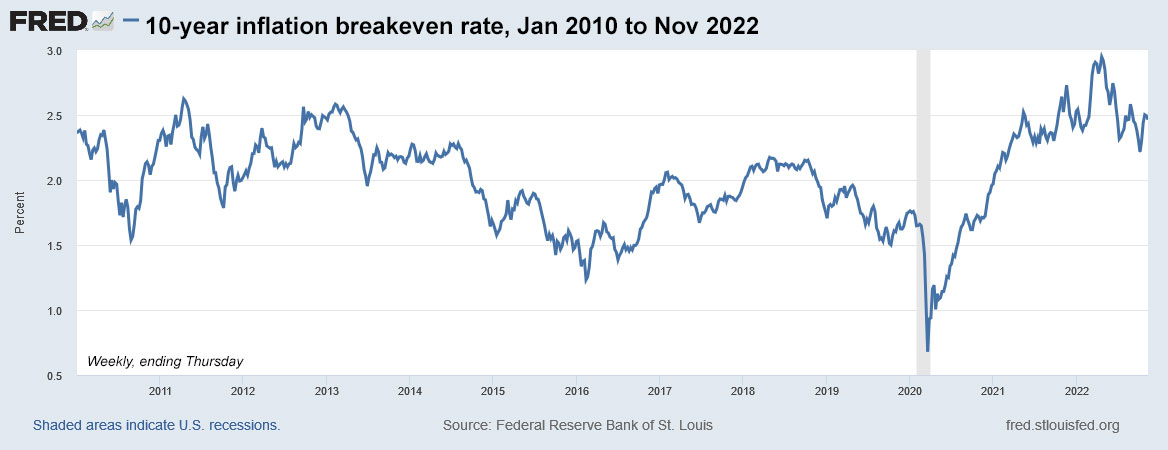

With the nominal 10-year Treasury note now yielding 3.81%, a 10-year TIPS with a real yield of 1.40% gets an inflation breakeven rate of 2.41%, in line with recent auction results. Inflation expectations have been falling in recent months, as the Federal Reserve shows resolve in fighting inflation with higher interest rates and balance sheet reductions. At this point, with U.S. inflation running at 7.7% annually, this breakeven rate looks reasonable.

Here is the trend in the 10-year inflation breakeven rate over the last 12 years, showing that the current rate remains at the top end of the historical range, but below the surge to nearly 3.0% in April 2022, just as the Federal Reserve was beginning to tighten:

Thoughts on this auction

Have we hit a top in the trend of higher real yields? Or was last week’s volatility just another head-fake in a year of bond market fluctuations? Personal opinion: It’s hard for me to resist this auction, since I have bought this same TIPS twice at lower real yields. On the other hand, have I already bought enough TIPS maturing in 2032? Should I look elsewhere? Should I wait until January’s auction of a new-issue 10-year TIPS, when real yields could be even lower? (Or not.)

Each investor will need to find answers to those questions. My general feeling throughout 2022 has been to load up on TIPS while real yields are attractive. My fear: This might not last long. Then again, maybe we have entered a “new era” in the U.S. bond market? Uncertainty.

As an alternative to this 10-year TIPS auction, I have considered going to the secondary market to buy TIPS maturing in 2030 and 2031, two holes in my TIPS ladder caused by the ultra-low yields of the 2020 to 2021 era. Those TIPS also had deep declines in yields after the October inflation report:

I checked on Fidelity’s trading platform Saturday morning and prices were slightly higher than Thursday’s close, but I can’t view prices for smaller lots. (Vanguard’s platform no longer lists any of these, not sure why.) There’s no way to know what we will see Monday, but if the real yields on these remain higher than the current yield of CUSIP 91282CEZ0 I might head in this direction to fill gaps in my TIPS ladder. Then I would look to fill the 2033 slot in January.

I still view this reopening of CUSIP 91282CEZ0 as a solid investment, despite the dip in yields. If you are considering investing, make sure to watch Bloomberg’s Current Yields page for real-time updates on its yield and price. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting the results soon after the auction closes at 1 p.m. ET Thursday.

Here is a history of 9- to 10-year TIPS auctions back to 2018, when the Federal Reserve launched its last tightening cycle, lasting until early 2020. Note that one year ago, on Nov. 18, 2021, a 10-year TIPS reopening got a real yield of -1.145%, the lowest in history for this term.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Wednesday pm update: CUSIP 91282CEZ0 closed today with a real yield of 1.37% and a price of $93.26. This one could end up being unpredictable, and it looks like the real yield could dip below 1.40%. But it could remain the highest real yield for an auction of this term since April 2010.

Tuesday pm update: Real yields had been wandering higher this week, but CUSIP 91282CEZ0 closed today with a real yield of 1.43%, so not much has changed.

Hi Dave, I really appreciate your analysis. I was wondering what your thoughts are on purchasing CUSIP 912810FQ6 (matures 4/15/2032) on the secondary market as an alternative to purchasing CUSIP 91282CEZ0 at auction. The WSJ shows 912810FQ6 trading at a real yield of 1.612%, which is a good bit higher than CEZ0’s yield of 1.484. It seems like that would be a better choice for the 2032 rung but I confess I am not very experienced in this. What am I missing? Thanks.

This is a unique TIPS, because it was originally auctioned in 2002 with a coupon rate of 3.375% and so the current price is at a premium, about $115.35 for $100 of value. It also has an inflation accrual of 67%. So to buy $10,000 par of this TIPS you would be paying about $18,626 and getting about $16,700 of accrued principal. But you also get a 3%+ coupon for 10 years, plus future inflation. The price seems fair because right now TIPS with shorter maturities and higher inflation accruals are offering higher yields than a new TIPS of the same term being offered at auction.

Hi David,

Regarding your point “I have considered going to the secondary market to buy TIPS maturing in 2030 and 2031, two holes in my TIPS ladder caused by the ultra-low yields of the 2020 to 2021 era.”, I am curious how these holes were created. I have constructed a TIPS ladder and maintained it diligently to match expected essential expenses regardless of the real yield, which meant painful decision of sticking with the rung purchases when yields were negative. What could I have done different that would have avoided negative yields without increasing the risk? Purchasing shorter term maturity TIPS and rolling them over till real yields improve is a good approach ex-post but may not be ex-ante.

Thanks.

A lot of people do it the diligent way you are and also try to match future expenses. My approach is more chaotic, trying to buy either 5- or 10-year TIPS (generally at auction) when the real yields are attractive. In the 2020 to 2021 era, the Federal Reserve drove real interest rates deeply negative, and so I didn’t buy TIPS in those years. Which is the best approach? Not sure. At least you have a defined system. My approach carries reinvestment risk. That is why I ended up loading up with purchases in 2018 and now in 2022 during Fed tightening cycles. (And buying I Bonds every year.) I’d really like to see a few years of stable, predictable real yields in a good historic range.

Hi David,

Thanks for that clarification, both for its content and candidness. When reading finance blogs or papers, I often feel like I may be missing out on something that others are finding.

I’m new to TIPS. How is the breakeven inflation rate and positive yield at an auction calculated? Any previous articles or resources you could point me to would be great. Thanks.

The breakeven rate is simply the difference in yield between a TIPS and a nominal Treasury of the same term. It gives you an idea of the market’s inflation expectations. The buyer of a TIPS is betting on higher-than-expected inflation; the buyer of a nominal Treasury is betting on lower-than-expected inflation. The real yield of the TIPS is set by bidders at the auction. If there are a lot of bids, the yield goes down. If there aren’t many bids, the yield goes up. A non-competitive bidder at an auction (like all of us) always gets the “high yield” — the highest yield the Treasury had to provide to complete the auction offering. More here: https://tipswatch.com/why-tips/

Thanks David!

Well, it wasn’t until April 29th that 10 year TIPS yields broke over 0%. Three months later, they dropped back down to practically zero. The July auction was +0.63%. It wasn’t until October that yields were over 1.5%.

It comes down to deciding what is an acceptable YTM for TIPS. To me, anything over 1.5% is attractive. Anything over 1% is acceptable. Anything over 0.5% is bearable. Anything over 0% is as low as I’ll go.

So far this year I’ve purchased TIPS in each of the above categories. So, as long as yields remain over zero, I don’t see any reason to stop now. I’ll just keep nibbling away in 10K purchases.

This pretty much matches my thinking.

My approach to fixed income investing is to compare the types of securities (bill, note, tips, etc.) and to determine which is the most attractive at any given time. In that regard, I think that the break-even rate is the most important indicator to watch. If it is low, TIPS are probably the better bet, if it is high, T-Notes and T-Bonds probably are.

Regarding the secondary market brokers, I find Schwab to be very good. You can easily display all of the lots for sale, even those offering only 1 bond at a slightly higher price. All buys (and sells) have no commission and the prices are very good (at least compared to my other broker- Fidelity). You can also put in bids for the auctions. While you are waiting for the perfect pricing before buying your bonds, they have a taxable money market fund that is yielding 3.7%.

Ya, I also noticed that that Schwab usually has better prices than Fidelity. On the other hand Fidelity lets you keep your core position in their money market funds. Unless you have megabucks at Schwab your forced into keeping core funds in Schwab Bank. So, you have to keep moving funds back and forth between the two as needed.

I know Schwab has some MM funds that have a 1$ million minimum. However, I use the Schwab Value Advantage MM (SWVXX) which has no minimum. I have never been forced to use their Bank. However, you are correct that Schwab does not have auto sweeping of cash into their MM funds like Fidelity does. As you say, with Schwab, one has to do buy/sell orders for their MM’s. I think this effort is worth it though, at least with treasuries.

Thanks, as always, for your commentary on this offering. I’m definitely interested now. However, I’m wondering what your current thoughts are about short-term TIPS funds (STIP or VTIP, which both have YTD returns of about -2.95% while the Vanguard site shows VTIP’s 30-day SEC yield as of 11/10 at 1.79%). I believe in a post not long ago you mentioned that you were selling some of STIP in order to fund new bond purchases, and I’m considering doing the same. Thanks.

I own VTIP in a traditional IRA but the fund I have been selling off to buy individual TIPS is Schwab’s U.S. TIPS (SCHP). I like VTIP’s lower duration, meaning the fund focuses more on tracking inflation instead of moving up and down with changes in real yields. The 30-day yield quoted by Vanguard is real yield, not nominal yield.