A weak bid-to-cover ratio of 2.18 indicates lousy demand from big-money investors.

By David Enna, Tipswatch.com

The Treasury’s offering of $17 billion in a new 10-year Treasury Inflation-Protected Security — CUSIP 91282CEZ0 — generated a real yield to maturity of 0.630% at auction Thursday, the highest yield at auction for this term in two years.

The coupon rate was set at 0.625%, the highest coupon for a new TIPS in three years. In fact, this auction broke a string of 15 consecutive auctions of 9- to 10-year TIPS with a coupon rate of 0.125%, the lowest the Treasury will go for a TIPS.

Definition: The “real yield” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 0.630% means an investment in this TIPS will exceed U.S. inflation by 0.630% for 10 years.

Investors in today’s auction should be pleased, because a surprise rate hike this morning by the European Central Bank had set both nominal and real yields sliding lower. Nothing drastic, but for much of the morning it looked like this auction’s real yield might dip below 0.60%. The bid-to-cover ratio was 2.18, a very low number and an indication that weak demand forced the real yield higher.

Because the Treasury set the coupon rate at 0.625%, slightly below the auctioned yield, investors paid an unadjusted price of about $99.95 for $100 of par value. However, because this TIPS will have an inflation index of 1.00495 on the settlement date of July 29, the adjusted price was about $100.45 for $100.49 of value, after the inflation accrual is added in.

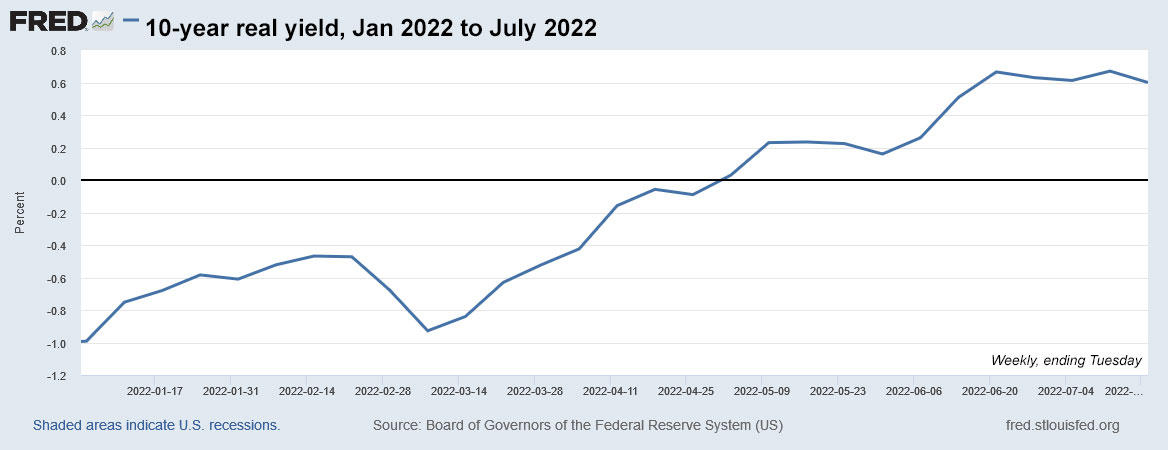

Here is the trend in 10-year real yields in 2022, showing the strong surge higher since the Federal Reserve committed to future rate hikes in March, in an effort to slow soaring U.S. inflation:

Inflation breakeven rate

With a 10-year nominal Treasury trading today with a yield of 2.96%, this TIPS gets an inflation breakeven rate of 2.33%, which looks like an attractive number. It means this TIPS will out-perform a nominal Treasury if inflation averages higher than 2.33% over the next 10 years.

U.S. inflation is currently running at an annual rate of 9.1%. While that number is expected to begin falling in future months, most experts agree it is likely to remain in the 4% to 5% range well into 2023, maybe higher. So again, this auction looks like a positive result for investors.

Here is the trend in the 10-year inflation breakeven rate through 2022, showing how inflation expectations have been falling in reaction to the Federal Reserve’s commitment to fight inflation:

Reaction to this auction

I was a buyer at today’s auction, so I was keeping my eye on TIPS trends through the morning. The European Central Bank’s surprise rate hike (the first in more than 10 years) did appear to roil the bond market, but the moves weren’t dramatic. One effect of the rate hike could be a stronger Euro and weaker dollar, which could slightly elevate inflation in the U.S., but also boost profits of U.S. corporations doing business in Europe.

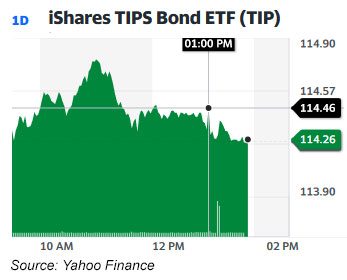

It’s possible big money investors decided to sit this auction out, especially as real yields appeared to be declining through the morning. Bloomberg’s report noted that demand was “soft” at this auction. The bid-to-cover ratio of 2.18 indicates weak demand, which forced the Treasury to accept a higher real yield. But as shown in this chart for the TIP ETF, the market reacted to the auction’s close at 1 p.m. with a yawn. Nothing to see here.

But for buyers at today’s auction, a real yield of 0.630% and a price very close to par is a welcome result. Keep in mind that principal balances for this TIPS will rise 1.37% in August, based on non-seasonally adjusted inflation in June 2022. That’s a darn good first month. (And as a side note, I will point out that the nominal 10-year German bond is currently yielding 1.22% annually, less that the upcoming one-month inflation accrual for this TIPS.)

Today’s auction of CUSIP 91282CEZ0 is the first of three for this issue. It will reopened at auctions in September and November. I think there is a reasonable chance yields will be higher at those future auctions, but a lot will depend on the state of the U.S. economy and the Federal Reserve’s commitment to fighting inflation.

Here is a chart of all 9- to 10-year TIPS auctions going back to January 2019, the last auction before the Fed abandoned its tightening policy that began, very slowly, in 2015:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: 2022 in review: Scary year for inflation, better year for inflation protection | Treasury Inflation-Protected Securities

Pingback: Uncertainty surrounds this week’s 10-year TIPS auction | Treasury Inflation-Protected Securities

Pingback: 10-year TIPS reopening auction gets real yield of 1.248%, highest in more than 12 years | Treasury Inflation-Protected Securities

Pingback: This week’s 10-year TIPS reopening auction is worth a serious look | Treasury Inflation-Protected Securities

Pingback: Confused by TIPS prices? Here’s a walk-through. | Treasury Inflation-Protected Securities

Can anyone explain if it makes sense to say, ladder up on TIPS through Treasury Direct, vs. buy a TIPS ETF such as VTIP? I’m interested in short duration only.

I’m very disappointed in VTIP. I’ve read a lot here and at many other blogs, but it still doesn’t click for me. If this is the way TIPS behaves during actual inflation, I may just stick with I bonds, despite the yearly maximum, as well as other investments.

TIPS ETFs are just bizarre and frustrating.

TIPS funds are like any other bond fund. When real yields rise, as they have dramatically this year, the market value of the TIPS investments falls. For TIPS funds, high inflation accruals can partially offset the decline in value. VTIP has a total return of -0.80% so far this year, versus -8.72% for BND (total bond fund) and -5.98% for IEI (7-10 year Treasury fund). So, relatively speaking, VTIP has done well.

I am a fan of VTIP, but I would prefer holding individual TIPS to maturity, and the 5- and 10-year terms are ideal for that, especially now that real yields are again above zero. So, for you, building a ladder of TIPS would make sense if you commit to holding to maturity and not watching the fluctuations of market value. (And remember that I am a journalist, not a financial adviser.)

This auction was an “oddity,” because it generated a higher-than-market real yield at a time when real and nominal yields were declining. The market was spooked by the European Central Bank’s actions, apparently. But here is the craziest thing: The Treasury’s estimate of the 10-year real yield dropped today to 0.43%, 20 basis points lower than the auction result.

Yup, I saw that this morning.

The best explanation that I’ve seen about why the yields are falling is the following:

https://www.schwab.com/learn/story/fed-rate-hikes-why-are-bond-yields-falling

I don’t know if I quite buy the argument yet.

But the latest bond market trends are a bit disconcerting.

The current yield on the 5 year TIPS is +0.26%.

How long will it take before it goes negative?

At this rate, tomorrow!

I suspect this will all turn around in days. Especially the 5-year. It is going to hit 1%+, eventually (opinion)

Laddered up again – 4 times a year. This was a nice one.

You mention an auction reopening: Why, in general, would one want to buy at a reopening vs buying on the secondary market? Is it to avoid the bid/ask spread? To be able to hold in a TD account? Is there some other advantage?

Thanks.

The reopening is another opportunity to get an auction’s “high yield” without any bid/ask spread or requirement to purchase any set amount. The minimum purchase is $100. The secondary market is fine, however, as long as the spread and minimum investment meet your needs. If you want to hold the TIPS at TreasuryDirect, then the auctions are the only alternative.

Thanks. I didn’t think about the minimum purchase. Your insight to TIPS is invaluable — it’s made me re-think my strategy for short-term (5yr) “buying power” protection as I start the early stages of my retirement. While I was a participant at this auction, I think I’m going to ladder out my 5-year needs with 5-year TIPS for the foreseeable future. This recent period of high inflation was just a little unsettling — it’s just not worth the minimal potential upside of trying to preserve buying power using a tradition treasury or bank account over a 5-year timeframe (IMO). One may not “win” with a TIP, but they cannot lose buying at auction and holding to maturity.

Anyway, thanks again. (I was already a fan of I-bonds although well after the $10K minimum was established but I hadn’t taken the time to understand TIPS — your writing makes that easy.)

Thanks for reading and participating. Understand that I struggle with these same questions and issues, and I don’t have all the answers. If you decide to have a certain percentage of your portfolio in safe investments — Treasurys, CDs, money market funds, etc. — it makes sense to add inflation protection to that mix. You are right, you might lose some upside potential. But if inflation continues raging, you are somewhat protected.

As a participant to this auction, I’d drink to that. The $63 a year is very close to a free lunch. If inflation persists at an elevated rate above the Fed’s target of 2% for many years, I think Uncle Sam might have to limit the issuance of TIPs just like they do to I Bonds.

Well, I guess that things worked-out about the best that they could on this auction.

A yield over 0.60% with a breakeven rate of 2.33% is acceptable (considering FED policies).

Granted, a coupon that’s $63 a year for each 10K is basically beer money.

But, a TIPS yield over zero is like Christmas in July.

I’ll drink to that.

Pingback: This week’s 10-year TIPS auction has ‘potential’ | Treasury Inflation-Protected Securities