Still, real yield was lower than expected as inflation expectations surged higher.

By David Enna, Tipswatch.com

The Treasury’s offering of $21 billion in a new 5-year Treasury Inflation-Protected Security resulted in a mixed bag for investors: The real yield of 1.732% hit a 15-year high and was quite positive, but that yield was a bit below market levels right up to the auction.

This is CUSIP 91282CFR7, and the auction result set its coupon rate at 1.625%, the highest coupon rate for any TIPS of this term since an originating auction on April 24, 2007. Buyers paid an adjusted price of about $99.48 for about $99.98 of accrued value and interest. This TIPS will have an inflation index of 0.99982 on the settlement date of Oct. 31.

This is the first 4- to 5-year TIPS auction to result in an adjusted price below $100 since April 26, 2010. The price means than a person who bought $10,000 in par value for this TIPS paid about $9,948 for about $9,982 in accrued value, plus a very small amount of accrued interest, about $7.

So all in all, this is a very positive result for investors. It’s baffling, though, that the Treasury had estimated the real yield of a 5-year TIPS at 1.89% at yesterday’s market close, and the most recent TIPS of this term had been trading all morning on the secondary market with a real yield of about 1.85%.

One factor is that inflation expectations seemed to surge higher, which would indicate strong demand for this TIPS, even though the bid-to-cover ratio was a mediocre 2.38. At yesterday’s market close, the Treasury estimated the five-year inflation breakeven rate at 2.46%, but this auction resulted in a breakeven rate of 2.67%. That’s a big move higher and would explain a lot of the gap between yield and expectations.

Also interesting is that non-competitive bids — made by small investors like us — totaled $256 million, nearly double the bids of $131 million for a new 5-year TIPS issued in April. But that surge higher probably had zero effect on a $21 billion offering.

Here is the trend in the 5-year real yield since the beginning of 2020, showing the remarkable surge higher after the Federal Reserve announced tightening intentions in March 2022:

Inflation breakeven rate

With a 5-year Treasury note trading at 4.40% at the auction’s 1 p.m. close, this TIPS gets an inflation breakeven rate of 2.67%. As I noted earlier, the 5-year inflation breakeven rate has been lingering around 2.45% for several days. A 22-basis-point jump is quite a move, and it indicates that investor demand for inflation protection is increasing.

Here is the trend in the 5-year inflation breakeven rate since January 2020:

Reaction to the auction

Over the last year, we’ve had a lot of upside surprises at the close of TIPS auctions, but this one was the reverse. While the real yield of 1.723% was a 15-year high and very attractive, it came in a little below expectations. (My expectations, anyway.) As you can see in this chart, the net asset value of the TIP ETF, which holds the full range of maturities, actually declined after the auction’s close at 1 p.m. That indicates higher yields.

And now, at 1:48 p.m., the real yield of the most recent TIPS traded on the secondary market has surged to 1.91%. Doesn’t make a lot of sense. I’ll look around for a logical explanation, but I don’t expect to find one. The bond market can humble you. It’s always a good reminder: never assume anything.

But I refuse to be disappointed with my purchase of a 5-year TIPS with a real yield at a 15-year high of 1.732% and a coupon rate also at a 15-year high of 1.625%. That’s a significant real yield after nearly a decade of ultra-low yields. And it means, most likely, that this TIPS will earn a return that will beat inflation, after taxes, if you are holding it in a cash or traditional tax-deferred account.

From today’s Reuters report:

“(T)he U.S. Treasury auctioned $21 billion in five-year Treasury Inflation-Protected Securities, with the high yield of 1.732% stopping short of the expected rate at the bid deadline, which suggested increased demand.

“Analysts said demand was fueled by strong participation from direct bidders. According to investment bank Jefferies, direct bidders took down 17% of the auction, which is about six percentage points higher than the average of the last four auctions. In dollar terms, Jefferies said this is the biggest takedown since December 2019.

FYI, the Treasury defines direct bidders as: “Non-Primary dealer submitters bidding for their own house accounts.” And another worthless definition, from Investopedia: “Direct bidders include primary dealers, hedge funds, pension funds, mutual funds, insurers, banks, governments and individuals.” Doesn’t that include just about everyone? More research is needed.

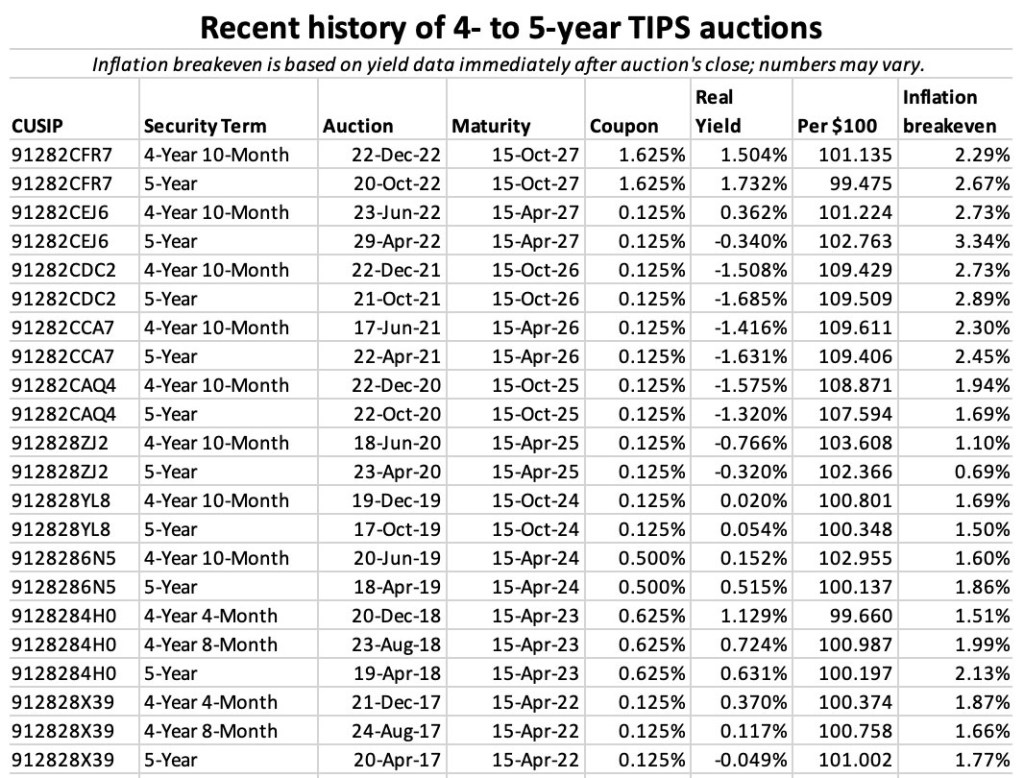

CUSIP 91282CFR7 will be reopened at auction on Dec. 22, 2022. Here’s a history of auctions of this term since 2017, showing the long string of negative real yields, including the record low real yield of -1.685% just one year ago.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I have $20,000 in 4 year 10 month TIPS CUSIP 91282CFR7. Inflation adjusted value is $20,882 as of 4/15/24. I feel like selling them before maturity and just putting them in a high yield savings account where I could be earning around 5%, (along with other underperforming cash) and generating a better return than screwing around with TIPS. I know the risk is the HYSA can change their interest rate, but I’m tired of dealing with Treasury Direct’s pathetic website and small biannual interest payments.

I’ll have to transfer them to my brokerage account, which is a huge pain. My first mistake was buying them directly from Treasury Direct. I just don’t see any benefit to TIPS vs a HYSA.

Advice? Thanks!

Hard for me to say for sure, but if you bought that at auction in December 2022 it had a real yield to maturity of 1.504% and the coupon rate is 1.625%, a bit below the current market. So at this point it is going to sell at a slight discount. This is probably a toss-up decision, except for the hassle of moving that TIPS to a brokerage and then selling it. Market prices could change in the meantime. Eventually, your high-yield savings account is going to get a lower interest rate after the Fed actually starts cutting, which will be next month. I think 5% is a solid return for safety, and sets up an inflation breakeven of 3.5%. Advantage to the savings account. The problem is that the 5% yield isn’t likely to continue, while the TIPS will continue paying that 1.625% + inflation through maturity in October 2027.

Right, I’m making the bet that inflation is going to fall, at least as measured by the Dept. of Labor. If we run into another global financial crisis and deflation, I’d rather have the cash, even at a discount, because then I may be able to purchase big ticket items for less in times of financial stress. The ‘boom’ isn’t going to last forever, the upcoming election is making everyone nervous, and I think we have kicked the recession can too many times too far down the road. All assets are overpriced, we are overdue for a huge crash and when there’s a crash, I just want cash.

Pingback: 2022 in review: Scary year for inflation, better year for inflation protection | Treasury Inflation-Protected Securities

Pingback: 5-year TIPS reopening gets a real yield of 1.504%, a bit higher than expected | Treasury Inflation-Protected Securities

Hi David. Good Morning. With respect to your post on Twitter that the real yield for 5-year TIPS has fallen to 1.52% – How does it affect the buyers who plan to hold it until maturity. Can you please explain. Thank you

When real yields fall, the value of the TIPS rises on the secondary market, but it has no affect on your return if you are holding to maturity.

I invested 25% of my retirement savings into this TIPS. Given that the fed is not done with interest rate hikes, what are the chances I will regret my purchase in 6 months? As I understand there isn’t a direct relationship between fed’s overnight interest rate and the TIPS interest rate. But it does tend to rise when the overnight rate rises, right? Is there a possibility we may see 2.5% or 3% yield in the next year, if the fed keeps raising the overnight rate?

The 5-year TIPS real yield does tend to track higher with the federal funds rate, simply because it is the shortest maturity of newly offered TIPS. So it wouldn’t be surprising to see the 5-year real yield climb above 2%. But that has only happened once in the last 14 years, during the financial crisis of 2008-2009 and it was a brief move. In the era from 2003 to 2008, however, it wasn’t unusual at all 10- and 30-year TIPS to have real yields above 2%, but not above 3%.

Medium- and longer-term TIPS yields will tend to track higher as nominal rates increase, so if the nominal 10-year Treasury hits 5%, the 10-year TIPS yield should rise above 2%, but a lot will depend on inflation expectations. And if the U.S. economy sinks into stagflation, you could see longer-term nominal rates falling, and that would pull down TIPS yields.

So this 5-year TIPS isn’t going to be a “bad” investment, especially if you hold to maturity, because you are going to earn 1.732% above inflation over the next 5 years. Putting 25% of your retirement savings into it was a bold move. What was your thinking?

I have a 60-40 portfolio where 60% is invested in the stock market, and 40% in safer investments. For the last 10 years that 40% has been in money markets. (I avoided bonds completely, believing that investing in bonds during periods of low interest rate, where the interest rates can only go up, is not a good idea.) Now because of the alarmingly high inflation rate that is showing no signs of abating, I decided I need to find a better investment than money markets for the 40% of my portfolio. And that’s how I ended up buying TIPS. I intend to hold my TIPS investment to maturity.

In the current investment climate, are there better options than TIPS for the “safe portion” of someone’s investment portfolio?

I also like to dedicate a portion of my portfolio to safety, and that means some combination of bank CDs, shorter-term Treasurys, I Bonds and TIPS. All of these are very safe, and I like mixing nominal and inflation-protected investments. Bond funds are “riskier,” so I don’t count them in this safety allocation. But I do like having a sizable holding in a core bond fund (Vanguard’s Total Bond Market). This year, though, has been a disaster for that fund. It’s more appealing now, with yields higher.

You’ve purchased a good hedge against future inflation, especially because you intend to hold this bond until maturity. It should provide a much better return than a money market.

At an historically-high and attractive 1.732% real yield, this was a relatively great purchase for a 5-year TIPS. That said, anything is possible with regard to future interest rates. It’s notoriously difficult to time any market, hoping to buy a bond at the perfect moment. Therefore, it’s a good strategy to make periodic investments over time — referred to as “laddering” in the case of bonds and CDs, and “dollar-cost averaging” in the case of stocks and mutual funds.

If you’ve never held a bond in a brokerage account before, keep the following in mind. The account statement will reflect the secondary-market value of the bond, based on whatever the current real yield is on the date of the statement. If the real yield on the 5-year TIPS is above 1.732%, it will appear that your bond has lost some value. However, you can ignore any loss of value shown on the statement, as it is not real unless you sell the bond before maturity.

There are several academic studies that refute the efficacy of dollar cost averaging. Of course mutual funds promote it, to their own benefit.

Excellent advice, jvalente.

I think I ‘ve made a mistake by buying the 5-Year TIPs in my Treasury Direct account.

My plan to rectify this is to buy the re-opening in December in my IRA account, while at the same time selling the TIPs in my Treasury Direct account.

You can’t sell a TIPS that you are holding at TreasuryDirect. If you want to sell it, you will need to have it transferred to a broker, and then sell it.

OK, then I just keep it and will buy some extra in my IRA come December.

Ed, I mentioned a while back that you cannot sell Treasuries or Tips in Treasury Direct. You have to transfer your holdings to a broker to sell. Brokers charge nothing to buy or sell Treasuries. The only thing I buy at Treasury Direct is I-bonds, because there is no other option.

This table posted by the WSJ makes no sense to me: https://www.wsj.com/market-data/bonds/tips

Let’s take the first row: 2023 Jan 15, 0.125, 99.24, 99.26, +1, 0.964, 1283.

So, this TIPs matures January next year, has a bid-ask spread of 99.24-99.26, the yield is 0.964% and the accrued principal is 1283 (supposedly).

But wouldn’t that imply that I can spend $992.60 today and get $1283.00 in January??! That’s almost a 30% gain in 3 months! What???

OK, you are buying $1000 of par value, but actually $1,283 of accrued value, and the cost would be about $1,278. You have to buy the accrued principal, but you would be getting it at a slight discount. In addition, you would get a coupon payment of 0.0625% on Jan 15. Inflation accruals will continue to be slightly negative through October, and then rise 0.22% in November. We don’t yet know what the inflation accruals will be for December and half of January. In other words, this looks fairly priced, and you won’t get rich. I wrote about these ultra-short maturities a few weeks ago: https://tipswatch.com/2022/09/02/whats-up-with-those-crazy-real-yields-on-ultra-short-term-tips/

Thanks for the explanation. Now it makes sense to me.

In short: better to buy 13-week bills than ultra-short term TIP maturities.

Thank you so much for your website and engaging with all of us to understand TIPS more thoroughly. I am learning so much, and as has been said…the smart people work with bonds, stocks are much easier to trade. We plan to retire in 5 years and plan to implement a 7 year ladder of tips to significantly provide income until RMD age of 72.5. I purchased 67k yesterday at the 5yr TIPS auction. I am trying to figure out if it is best to buy a new 5 yr tips rung at auction each year going forward? Or should I look at a prior issue maturing in the needed year on the secondary market? For example, for the rung to payout in 2028, cusip 912810FD5 appears to offer a 1.9% yield? Is that a relatively expensive ask at the moment?

I would appreciate your commentary on this and apologize if my questions are so elementary 🙂

FYI the half year RMD rule is gone, it is now the year you turn 72. May not make a difference for you, but it might. I am also retired and use a 5 year ladder to meet RMDs and my budgeted withdrawals to avoid market risk for at least 5 years, that is where I am comfortable. My ladder is not jut TIPs, but also include I-Bonds and some straight bonds (Treasury and AA rated corporates).

When shopping on the secondary market, make sure to note the accrued principal, which you will be buying. That will raise your price above the par value you might think you are purchasing. 912810FD5 is a very complicated investment. It is a relic of the past, an aging 30-year TIPS with an insanely high coupon rate of 3.625%, and that means its current price is close to $109 for $100 of par value. It has an inflation index of 1.831, meaning you’d be purchasing a whopping 83% of accrued principal, at a 9% premium. So rough estimate, $10,000 par of this TIPS could cost you $19,958. Ouch. But after all that you’d get a 1.9% real yield to maturity because of the 3.75% coupon rate.

David deserves some sort of award for his insights and analysis. You won’t find such anywhere else. Thank you David!

The quoted price per TD is 99.475435 per $100 but my brokerage account shows executed price of $99.4933 per $100. I figured it must be the accrued interest and according to my calculation of accrued interest is 0.017865 per $100 using this formula:

[1.01625^(16/365)-1]*100

Can you tell me why the difference? This is my first time buying TIPS and just trying to learn the mathematics behind the numbers. Thank you.

The executed price the brokerage is showing you is the unadjusted price, which was 99.493344. Vanguard showed the same price. OK, so you bought $100 of par value, reduced by the inflation index of 0.99982 = $98.982. Take that $98.982 x the unadjusted price of 0.99493344 = $99.47543. So maybe the accrued interest makes up the very small difference.

The brokerage firms really try to be as opaque as possible. For each 10K, mine shows the same executed price of $99.4933, a total cost of $9,954.58 and interest of $7.14. Of course, this information isn’t enough to verify their math.

So, I had to go to the Treasury Auction Results printed statement to get the rest of the information I need. I was able to verify that the executed price was actually the unadjusted price and that the relevant index ratio is 0.99982 (Footnote 2 on the printout).

I’ve got a spreadsheet that I use to keep track of TIPS. Here’s the formula that I use to verify that what the broker charged me is correct.

Set the price to the unadjusted price of 99.973344.

Multiply this times the inflation factor of 0.99982.

That yields an inflation adjusted price of 99.4754.

Since I buy in 10K lots the extended price $9,947.54.

Adding in $7.14 of accrued interest and the total cost is $9954.68.

I don’t know why the broker doesn’t just show the adjusted price.

Pingback: Get ready: This week’s 5-year TIPS auction is a ‘unicorn’ | Treasury Inflation-Protected Securities

David (or anyone), Would you mind explaining to a newbie. I bought several k in this auction in a roth account, then immediately came back to see what you might have posted. Seeing you mentioned 1.9% after the auction, I went to look, but I’m not sure what I’m looking at. There is a treasury bill on the secondary auction for instance, that says it has a coupon of 2.5. Does this really mean that it is guaranteed to provide 2.5% +/-inflation, till it matures? Or am I missing something?

Sorry for such a newbie question. (I am pretty happy with my purchase, and VERY happy that you made me aware of the possiblility!)

The coupon rate of 2.5% is only one factor in determining real yield. The other factor is the price per $100 of par value, which in this case is probably would be around $103.50 for $100 of value, so you have to pay a premium for that 2.5% coupon when the market real yield is 1.9%. This TIPS is only going to outperform inflation by 1.9%. Also that particular TIPS — maturing 2029 Jul 15 — has an inflation index of about 1.158, so you’d be buying nearly 16% extra principal and also paying a premium for that. … TIPS are complicated investments on the secondary market. Anyway, congrats on this purchase today; an auction purchase is a great way to start.

Thank you David, for your kindness in explaining. I don’t know how to figure out any of what you said, but that just tells me I should stick to the auctions till I understand better….which is itself a huge help. Thanks you!

Maybe you might consider that to be the topic of a post one day…how to figure out tips on the secondary market, looking for example, at a screen grab from Vanguard. 🙂

Thank you for writing about this TIPS auction. After regarding TIPS (and Treasuries) as a bad deal for the past few years due to zero or negative real yields, this looks like a good deal so bought 10K worth in a Roth. Real yield + inflation + no tax means getting to keep my money!

Can you explain exactly where the ‘inflation index’ number at issue comes from and why it doesn’t just start from 1.000000. Is it a result of the expected or actual auction results somehow or is it set from somewhere else and thus it influences the auction results.

The inflation clock starts on the issue date, which is Oct. 15, so there is a half month of inflation accruals until the closing date on Oct. 31. October’s inflation adjustments are based on August non-seasonally adjusted inflation, which was down 0.04%, so there is a half month of very minor deflation.

While very mildly disappointing in that I thought the real yield would be a tenth of a percent higher, I’m also pleased with the result of my first foray into TIPS. This is a learning experience.

For context, I’ve been buying I Bonds for about 10 years, and many of them have a fixed rate of 0%, and I’ve been happy to have those too. The 0.1% lower real yield on these TIPS versus what I had hoped for is nothing compared to the large gap of these TIPS above what my I Bonds are paying. (And again, I’m happy to hold onto those, as they have other advantages.)

Good Afternoon All, I have locked in $5K in this one in Roth. My original intent is to hold it through maturity. Now I have two questions.

1. With the discussion that we got a lower yield, should we hold or sell it ? Asking this because of the discussion on buying it in the secondary market. (sorry, if this is a noob question – this is the first time buying TIPS)

2. What do you mean by this will again open for re-auction on Dec, 22 ? Can you please explain.

Thank you for all your effort for the information you have here on the site. I’m learning a lot ! 🙂

You made a very good investment today, one of the most attractive TIPS new issues in years. We are just griping. Definitely hold it and don’t worry about it. On the reopening: The Treasury stages originating auctions, like this one, for a TIPS and then follows that up with one reopening (for 5-year and 30-year TIPS) or two reopenings for 10-year TIPS. Next month is a 10-year reopening and then in December this TIPS will be reopened at auction.

Thank you for the response and putting me at ease. Will hold on to this !

Where do you get information on the Treasury reopening the 5-year or the 10-year?

Thanks

Here is the schedule of the Treasury’s upcoming auctions … https://home.treasury.gov/system/files/221/Tentative-Auction-Schedule.pdf

Like I mentioned, I always intend to hold to maturity, but life sometimes throws emergencies at us, and sometimes those require cashing out some holdings quickly. That is why I prefer to buy (and sell if necessary) Treasuries through a broker.

I bought at TreasuryDirect for years and I am now letting those mature with taxes pre-paid, so there is little tax consequence at maturity. Worked fine. Now that I am retired I am buying TIPS in a traditional IRA brokerage account, where I can easily raise the money for the purchase without triggering any taxes.

One logical reason for lower yields on new issue TIPS, is the inherent deflation protection. Especially true for shorter-term TIPS.

Of course, it is silly to consider there might be deflation over the next five years.

Much like, it is silly treasury bills were essentially 0% the past two years, or the US Federal Reserve would own 1/3 of all US Treasury, while having negative equity.

Good luck everyone.

Silly and scary!

For example, there are two TIPS maturing Jan 15 2027.

Principal Yield

1226 1.931%

1468 1.954%

2 also Jan 15 2026

1246 1.978%

1492 2.015%

https://www.wsj.com/market-data/bonds/tips

These are interesting examples. Logically, I would want to buy a TIPS with the biggest discount to the inflation accrual. In both these cases, the higher inflation accrual is also associated with a higher coupon rate and also a much higher price. In 2027, the higher inflation number costs you 101.62 for 100 of value, versus 93.20 for the lower inflation accrual. In 2026, it’s 99.28 versus 95.23. Wouldn’t your rather buy the inflation accrual at a bigger discount? So you have a point.

I don’t know that a price premium or discount to maturity value of 100 matters, but maybe it does? I don’t know why. I understand it impacts yield to maturity.

A quick scan shows five dates, with two issues maturing on each date.

https://www.wsj.com/market-data/bonds/tips

In each case, the lower inflation accrual, yields a slightly lower real yield. It isn’t much, but it seems logical, to me, that the lower the principal, the lower the deflation risk.

So, I think the “new issue” value of a 100 principal value, as in this case, has real value.

I don’t get it. Which of the two is the better deal? Bigger discount and lower yield, or lower discount and higher yield? Shouldn’t this be a wash?

I’d say the two factors are really discount/premium and coupon rate. Those two factors combine to create the real yield to maturity, and that is the most important thing when you purchase a TIPS. In this thread, Eric was noting that a higher inflation accrual might make a TIPS slightly less attractive than one of the same term with a lower accrual. Why? Anything above par value is not protected against deflation.

I am not claiming one is the better deal.

I simply stated that when two TIPS have the same maturity date, the one with the lower “accrued principal,” is valued more, as shown with a higher “yield-to-maturity.”

https://www.wsj.com/market-data/bonds/tips

The difference in yield to maturity is minor.

The difference is minor today, that is.

Maybe the cost changes, when deflation is considered a real possibility.

How did you arrive at 101.62 vs 93.28 for 100 of value in the above example for Jan 15 2027 TIPS?

One TIPS has a coupon rate of 2.375%, which is higher than the current market, so it is priced higher. The other TIPS has a coupon rate of 0.375%, well below market, so its price is much lower. .

Right, I get that. My question was specifically about 101.62 for 100 of value and 93.28 for 100 of value. What formula did you use to calculate those prices?

It is based on the bid/ask price, which was ?? when that comment was posted. As of today it is about $102.71 for the one with a coupon rate of 2.375%, and about $94.23 for the one with the coupon rate of 0.375$. The coupon rate sets the price, versus the current market real yield of the TIPS maturing in Jan 2027.

Hi, David!

It looks like the “indirect bidders” bought most (75%) of the TIPS in this auction and they determined the price and real yield of this issue. Do we have any ideas who these indirect bidders are? Indirect bidders are apparently calling the shots!

I suspect the traders in the secondary market are shunning all long-term treasury securities – whether they are conventional notes and bonds or TIPs. There may be a growing lack of liquidity in the secondary market. Hence, traders in the secondary market are demanding a higher real yield than we saw in the auction. Hence, from now on, it might be cheaper for us little guys to buy TIPs in the secondary market, rather than in auctions which are dominated by indirect bidders. Do I make any sense?

Good point. Indirect bidders are: “Customers placing competitive bids through a direct submitter, including Foreign and International Monetary Authorities placing bids through the Federal Reserve Bank of New York.” You are right, they submitted 75% of the accepted bids in this auction. But in April, it was even higher, 89%.

Hi, David,

I saw headlines early this afternoon which quote Bank of America analyst saying that the US treasury market (i.e. secondary market) is at risk of large scale forced selling. Also, increasingly I hear about all this growing lack of liquidity in the treasury secondary market. I wonder who will be doing the forced selling? If the “forced selling” really happens, it might be a good time to buy some TIPs in the secondary market at real yield above 2%.

This sort of thing happened drastically in the financial crash of 2008 and then very briefly during the pandemic chaos in March 2020. One way it can happen is if a highly levered hedge fund suddenly had to cover margin calls; it would then sell everything to raise the money.

Hopefully, the FED won’t feel the need to bail-out hedge funds.

Also wondering if TIP funds have been forced to sell based on individual withdrawals. Seems like investors would be disillusioned by losses created from rising real yields, in spite of the high inflation these funds were promoted as protection for. Haven’t been able to find funds flow data which would support this.

Because the latest TIPS auction gives you a guaranteed 1.732% yield over inflation for the next five years. Those short term Treasuries are currently losing 4% to inflation.

So would it have been better to purchase these on the secondary market when available?

In this case, yes. The most recent 5-year TIPS has 4 years, 6 months remaining and it appears to be trading right now with a real yield of 1.91%. This assumes you can get 1.91% even with a bid-ask spread and possible yield penalty for smallish purchases.

I just looked and there are 10+ TIPS CUSIPs available with ask-side yields over 2.0 up to about 2.1% with maturities from 2 to 25 years. It seems interesting that the yields are so similar over such a wide range of maturities. The order books all have sufficient depth for most retail investors and then some, but the overall size of this secondary market is probably a lot smaller than the huge auction today. There were probably some whales that are anticipating persistent inflation for the next 5 years, just like this minnow is. The difference is that they are too big for the secondary markets. I don’t know who is selling, but I doubt it is panic driven yet.

The yield curve is flat, so this sort of makes sense. I’d love to find TIPS with 2% real maturing in 13 to 15 years. However, since the Treasury refuses to issue 20-year TIPS, there are no TIPS maturing from July 2032 to Feb 2040. Oh well, I’ll look at 2040 and beyond.

Although the end result is good, it still leaves a bad taste in my mouth. The stock market started the day on a positive note. That optimism seems to have existed in the bond market as well. The result was bond yields dropping early on. However, they never went below 1.82%. So, getting a yield of 1.732% is pretty hard to explain. That’s almost a 10 basis point change in just a few hours.

Quite frankly, anything under 1.80% seems a bit of a stretch. And, with yields over 1.91% after the auction, it’s totally bizarre. I guess in the future I’ll have to go back to my cat and mouse game of buying some on the secondary market before the auction, some at the auction and some after the auction.

Jimbo, I am sure you have noticed the markets are unusually nuts (the pros use the word “volatile”) right now. Trying to make sense of them is mainly for amusement.

My understanding is that yield is based on the competitive bids, sorted from low to high. From a $21 billion offering, subtracting the $256 million of non-competitive bids, there were $20,744 million of competitive bids submitted at or below 1.732%.

Perhaps some large buyers were very eager to get in on this auction of new 5-Year TIPS securities, such that that they were willing to accept a lower yield to ensure they got in? Although the secondary market is an option for acquiring similar-term TIPS, as Brian points out in a different post, such large buyers (whales) may be too big for the secondary market to satisfy their needs.

jvalente, I think this is an excellent analysis. Big-money investors jumped in on this auction with aggressive bids and didn’t care if they lost 10 basis points. Those kind of bidders can’t be nickel and diming in the secondary market.

I wonder why anybody would by a TIPS or a Treasury ETF or bond fund. My strategy is to buy Treasuries at auction, sell at maturity, which is why now I never buy Treasuries beyond 1 year maturity. I like three and six months for now. When inflation cools, then I might go to five year treasury notes.

I also wonder why people buy Treasuries (or TIPS) through Treasury Direct, where if you need to sell before maturity, like in an emergency, you have to first transfer them to a broker. All the big brokers charge nothing to buy or sell Treasuries. Buying at auction you avoid the secondary market. Holding to maturity you avoid any loss.

If you really intend to hold to maturity, then no big deal to purchase at TreasuryDirect. But if you want the TIPS in a tax-deferred account, as is recommended, then you’ll definitely want to buy through a broker.