By David Enna, Tipswatch.com

The year 2022 broke through several economic milestones, and most of them were dreadful: Highest U.S. inflation in 40 years. U.S. stock market down 20%. U.S. bond market down 13%. Federal Reserve aggressively raising interest rates. War in Europe sending gas prices soaring at mid-year. Pandemic causing supply shortages. Mortgage rates nearly doubling.

But there was a bright side: The Federal Reserve actually stuck to its plan to fight inflation despite possible damage to the U.S. economy. (I was surprised.) And interest rates — especially short-term rates — rose to attractive levels, finally giving investors a chance to build a safe, worthwhile cash holding.

Real yields on Treasury Inflation-Protected Securities also rose to attractive levels, the highest in 15 years. And U.S. Series I Savings Bonds became the surprising star of mainstream financial news.

U.S. inflation

It was easy to see this surge in inflation coming, after years of easy money from the Federal Reserve and massive stimulus payments from Congress. The Fed argued inflation was “transitory.” It wasn’t.

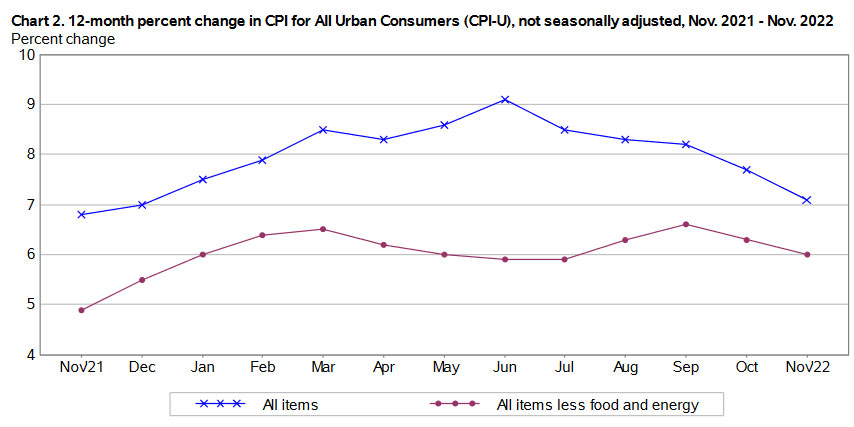

U.S. inflation ended 2021 at 7.0%, the highest annual rate in 40 years. And things got much worse early in 2022, with inflation rising at an annual rate of 12.2% in the six months from January to June, before moderating in the last months of the year. Year-over-year inflation peaked at 9.1% in June 2022, the largest 12-month increase since November 1981.

But since June, inflation has been slipping lower along with falling gas prices, dropping to an annual rate of 7.1% in November. Here is the year-over-year trend in U.S. inflation in the last 12 months, showing the gradual decline in all-items inflation, even as core inflation has remained stubbornly around 6%:

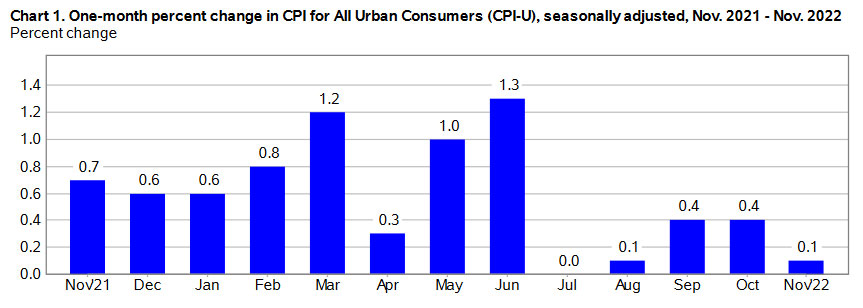

What’s ahead for inflation? It’s impossible to predict, but my gut feeling is that month-to-month and annual inflation will continue to moderate. One reason: Last year’s monthly inflation numbers were very high from December 2021 to June 2022, as shown in this chart:

Even if inflation runs at 0.4% to 0.5% each month through mid-2023, annual inflation will be declining because of the higher year-ago numbers. So could inflation drift toward an annual rate of 4% to 5% in 2023? It looks likely, as long as gasoline prices hold steady. But as I always note: It’s impossible to predict the future. And annual inflation of 4.8% would remain unacceptable in the long term.

I Bonds

U.S. Series I Savings Bonds were already a mainstream hit late in 2021, after the annualized composite rate rose to 7.12% on November 1, 2021. And then inflation surged even higher, pushing the next rate reset to 9.62% on May 1, 2022. For years, I Bonds had been a fairly esoteric and sleepy niche investment. I remember a day in 2021 when CNBC’s Becky Quick asked her co-hosts: “What is an I Bond? I’ve never heard of it.”

Sleepy, no more. Interest in I Bonds became so intense that buyers crafted strategies to double-, triple-, and even quadruple-dip the $10,000 annual investment limit. In October, the flood of buyers crashed the TreasuryDirect website, crippling it for days. And even with the slowdown, the Treasury sold $979 million of I Bonds in one day, on Oct. 28, the last day to lock in the 9.62% rate for six months.

Then, on Nov. 1, 2022, the Treasury made a very welcome decision. Even though it faced raging demand for I Bonds, it raised the fixed rate for I Bonds purchased from November 2022 to April 2023 to 0.4%, creating a composite rate of 6.89% for six months, still highly attractive. That move demonstrated that the Treasury does pay attention to rising real yields, and acted correctly to raise the I Bond’s fixed rate. This was a move I had been urging. Very glad to see this happen; it’s the first I Bond fixed rate above 0.0% since the November 2019 reset.

Treasury Inflation-Protected Securities

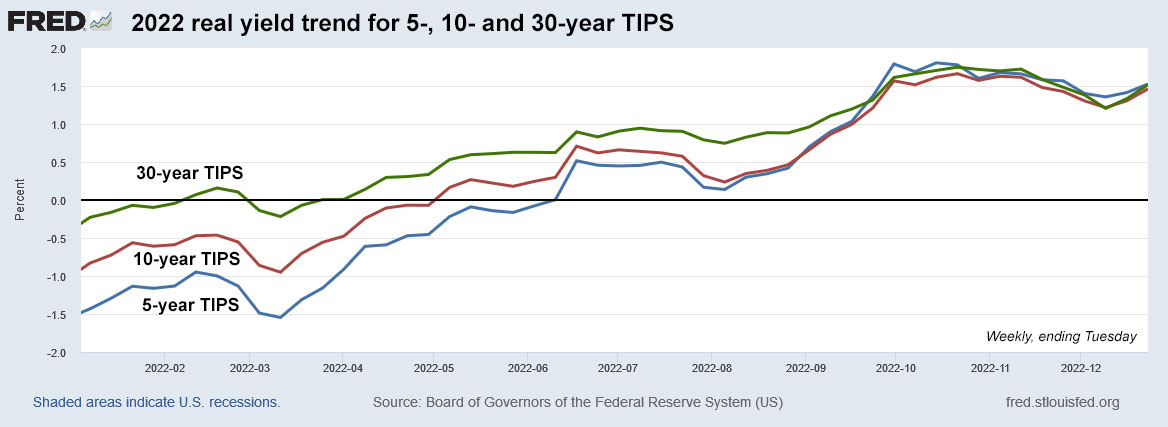

TIPS began the year as an “undesirable investment,” but by mid-year they started getting more and more desirable. The reason can be summed up in this one chart, the trend of TIPS real yields throughout 2022:

Here are the starting and ending real yields for TIPS, based on the market close on Dec. 29:

- 5-year, started the year at -1.53%. Ending the year at 1.62%, an increase of 315 basis points.

- 10-year, started the year at -0.97%. Ending the year at 1.56%, an increase of 253 basis points.

- 30-year, started the year at -0.36%. Ending the year at 1.63%, an increase of 199 basis points.

Obviously, an increase of 250+ basis points of real yield makes TIPS much more attractive today, but holders of TIPS mutual funds and ETFs felt the pain in 2022, even with inflation soaring to a multi-decade high. The TIP ETF has had a total return of about -12% year to date, reflecting its duration of about 6.63 years. The increase in real yields — causing a decline in the value of the underlying TIPS — were enough to wipe out 2022’s inflation accruals.

Investors who buy individual TIPS and hold to maturity can ignore this market volatility, and this was the year when — finally — TIPS became a strong addition to an investor’s “safety” allocation, with real yields surpassing the supremely popular I Bond. Here’s a recap of the year’s TIPS auctions:

CUSIP 91282CDX6: 10-year

The first TIPS auction of the year got a real yield of -0.540%, and its first reopening in March was even worse at -0.589%. This may be the last 10-year TIPS with a coupon rate of 0.125% for awhile. (I hope.)

CUSIP 912810TE8: 30-year

The Treasury stages only two 30-year TIPS auctions a year (and that is plenty, in my opinion.) This TIPS originated in February with a real yield of 0.195% and a coupon rate of 0.125%. By the August reopening the yield was up to 0.92%, and now it trades with a real yield of 1.65% and its price has plummeted to about $64.91, a decline of about 34% in 10 months. Investing in a 30-year TIPS in a rising rate environment is a dangerous idea.

CUSIP 91282CEJ6: 5-year

The first 5-year TIPS auction of the year was in April, just as real yields were starting to inch higher. This TIPS got a real yield of -0.340%, but at least it looked attractive versus the year-earlier 5-year auction, with a real yield of -1.631%. At its only reopening two months later, the yield climbed to 0.362%.

CUSIP 91282CEZ0: 10-year

By July, 10-year real yields had climbed to 0.630%, giving this TIPS a coupon rate of 0.625%, the highest coupon for a new TIPS in three years. By November, the real yield had soared to 1.485%, even as the inflation breakeven rate was declining.

CUSIP 91282CFR7: 5-year

By October, real yields were flying high, leading to the most attractive TIPS auction of the year on Oct. 20. This TIPS got a real yield of 1.732% and a coupon rate of 1.625%, both setting 15-year highs. At the time, the result looked disappointing, but it has held up as a very strong yield. By the December reopening, the real yield had slipped to 1.504%, still attractive.

Importance of inflation protection

I know a lot of investors have been flooding into I Bonds (and more recently, TIPS) as yields have become attractive against a backdrop of harsh inflation. I’m sure many of those investors will eventually move on to the next “hot thing,” and that is fine. But I’ve argued for a decade that it makes sense to keep a certain portfolio allocation dedicated to inflation protection, through I Bonds and individual TIPS held to maturity. Maybe that allocation could be 5%? 10%? 15%?

This incredible and awful year, 2022, has demonstrated the need for inflation protection. That need will still be with us in 2023 and beyond.

Happy new year, everyone.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

For the last 10+ years, every early January, I have been buying I-Bonds for my wife and me. Deferred taxes and inflation increases have been good enough reasons for us to buy these. We have no plans to sell any of these for a long time. I am fairly new to this site, and I have already learnt a lot. For the first time ever, I bought TIPS. I bought my 5-year TIPS at the December 22nd auction for my wife and my rollover IRA accounts. Keeping this or any individual bonds to maturity has alaways been my strategy. I got out of bond funds many many years ago for two reasons: 1) unacceptable expence ratios and 2) rates could have only gone up from where they have been for the last many many years. Obviously, these are exciting times for cash. Unfortunately, I am getting greedy and spreading myself into areas that I am less comfortable, TIPS is one of them. Ok, I bought the 5-year TIPS because it is only 5 years and I consider it to be a measured guess. I do follow the FED, Larry Summers, Barron’s, WSJ, and FT articles related to the economy and ineterest rates. The 10-Year TIPS auction on January 19th is the new focus. David says that he will most likely buy if the real yield is above 1.50%. Expanded thoughts by David or anyone else will help. 10-Year break even inflation rate, as of December 30th, was 2.3%. Confession: there is a side of me that says, inflation to go below 2% in the new economic world in the next 10 years is not a chance beacuse gone are the deflationary forces such as cheap labor from China or the like….sorry, I can go on and on…will look forward to your take…really like the exchanges on this blog…best chander

Hello Chander, welcome to our group. I will be posting a preview of the Jan. 19 10-year TIPS auction on Sunday morning, Jan. 15. On the 5-year TIPS, your comment matched my thinking I have expressed many times: A 5-year TIPS is great because it’s only 5 years.

Thanks!!…I have been mostly buying US treasury bills while keeping an eye on the notes and beyond. On one hand, reinvestment risks with not buying longer maturity notes or bonds is worrysome while, on the other hand, hope/greed/expectation for longer duration to inch up and wait is also there. Slowly moving to 3, 5, 7 years is starting to look acceptable. Since I keep these to maturity, worst case is not too bad. I look forward to your Sunday post on the 10-year TIPS original auction ( I seem to like these more than reopening).thanks again!!..best chander

Based on your meticulous record keeping of the the individual TIPS inflation indexes, what was the inflation accrual for say a 5-year TIPS in 2022 (1/2 to 12/30/22)? Will vary a bit from bond to bond, but the index change is what it is. I thought I had this data, but looks like I don’t, the trading systems don’t capture it, so curious what you have. Thanks!

Here are the inflation indexes for all TIPS in January 2022: https://www.treasurydirect.gov/instit/annceresult/tipscpi/2021/CPI_20211210.pdf

And here they are for December 2022: https://www.treasurydirect.gov/instit/annceresult/tipscpi/2022/CPI_20221110.pdf

thanks, I chased it back from the sample you had in your “complicated” post, so arrived there about the same time. BTW I got 8.87% so call it 8.9% from a 1/15/27 maturity. thanks!

If you have the choice between buying a 5-yr CD with a 5% APY or a 5-yr TIPS with a real yield of 1.5% to 1.6%, which one would you select? The breakeven inflation rate for the 5 years for these two investments would be 3.5%.

If I saw a 5-year CD (or Treasury) yielding 5%, I would buy it. Same for a 10-year. But those don’t exist, yet, unless you are finding a great deal on a non-callable brokered CD. And I would still buy a 5-year TIPS yielding above 1.5%. That does exist.

You can get a 5.4 rate on a five year MYGA with an A rated company. I know Jimbo is down on these, but I don’t see the entire insurance industry going under.

I have no opinion on annuities, but here is an article by Allan Roth pointing out how they can shift bond-loss costs to their customers: https://www.advisorperspectives.com/articles/2022/12/19/did-rising-rates-cripple-the-insurance-industry

Interesting article, thanks David. I don’t think this would apply to MYGAs, which is the insurance version of a bank CD, with a fixed rate and term. There are no additional fees or rate adjustments.

Amazing website, David, thank you!

Next question up for me: for long-term investments in my traditional IRA, do I wait for the February 30-year auction (and hold to maturity until I’m almost 80) or build a ladder for slightly shorter durations from the secondary market while real yields to maturity are around 1.7%? Let me know if anyone has any thoughts on this!

I did participate in both 30-year auctions in 2022. It’s been educational to see the market value plummet–but in my view, had I invested that money back in February in broad index bond or stock funds instead, I’d be *actually* down at least 12%, so the 30-year TIPS (if held to maturity, as I’m committed to doing) did it’s job as a rock solid safe investment.

Just an opinion, I am not a financial adviser: I’m too old to buy the 30-year and hold it to maturity, so that term is out for me. But a few months ago I bought a 20+-year (Feb 2043) on the secondary market with a real yield of 2.032%. When real yields rise above 2%, you are looking at the “historical” return of long-term Treasurys over inflation. We haven’t seen this, except briefly, for 15 years. If I was the right age, I’d probably be willing to buy a 30-year with a real yield above 2.0%.

My TIPS holdings include two 30-years from the past, still holding. 1) matures April 2029 with a coupon rate of 3.875% (!) and 2) matures Feb 2041 with a coupon rate of 2.125%.

David,

I have been buying I Bonds, TIPS, and TBills for several years. So glad I discovered your column which has helped me so much to buy these instruments more selectively and knowledgeably. I enjoy your column and your acknowledgement of what you don’t know (mainly the future) and appreciate you writing for the non-expert layman.

David, I became a regular reader in 2022. I’ve long been a fan of both TIPS and I-Bonds, but regularly found new perspectives and insights. Thank you.

FWIW one of my strategies in 2023 will be to do some Roth conversions of individual TIPS holdings. Roth conversions are often recommended when markets are down. With TIPS that you own in a traditional IRA there’s a unique wrinkle. As you point out, many TIPS are trading at a discount to their inflation-adjusted principal. If you already owned TIPS before the run-up in real rates and plan to hold them to maturity, a Roth conversion will let you pay taxes only on today’s market value. For example, if you bought the 30-year TIPS due 2052 at auction in February you have a large unrealized loss. The market value is currently about 64% of the inflation adjusted principal, which means you can cut your tax bill significantly and receive all future inflation adjustments tax-free. What do you think?

Interesting idea. Is is just a straight transfer from account 1 (IRA) to account 2 (Roth)? And then tax would be due on the market value of the TIPS at the time of the transfer?

Mechanically, yes. General Roth conversion considerations still apply (e.g., not expecting a much lower tax rate in the future; having non-IRA money to pay taxes). So it’s important for everyone to analyze their own situation.

Peter, I’m going to do the same. The 10 yr that I bought at auction last January will be transferred to my Roth as a conversion this year. Makes great sense tax-wise.

David, yes, it’s just a transfer of securities from one account to another. The distribution amount will be the market value on the date of transfer, not the inflation-adjusted principal balance. Yes, the income tax on the distribution will be based on the market value.

I am grateful to have found your invaluable tipswatch.com site. We sold our home in May 2022 and were flush with liquidity. We initially put into CDs that were attractive at the time around 2%. Thankfully we only forfeited 2 months interest in canceling our CDs, and based on what I learned from your site, we were able to purchase the I-bonds at 9.62%. Got the 4 yr 10 mo TIPS (even beginning to understand the “language of TIPS”, and also have created a ladder T-Bills, based on your https://tipswatch.com/2022/07/04/looking-to-put-cash-to-work-consider-short-term-treasury-bills/. This has been a blessing. We are retired with no earned income and feel fortunate to have these inflation protected securities for now! Thank you!

I can’t wait to read your always well-informed speculation about the first TIPS auction of the new year scheduled on January 19 for 10-year TIPS.

Thank you for a great year of very useful articles. No other place is there such a comprehensive discussion of inflation-related investments. Happy New Year!

“The TIP ETF has had a total return of about -12% year to date…The increase in real yields — causing a decline in the value of the underlying TIPS — were enough to wipe out 2022’s inflation accruals.”

Question: Suppose I had $100K in the TIPS ETF on Jan 1 2022 and reinvested all the dividends I got throughout 2022. Is my TIPS ETF now worth just $88K? Ugh…

That’s correct. Total bond market is a little worse, at -12.75%.

A loss of -12% coupled with a mere .75% advantage over Total Bond in a year of very high inflation is really, really bad. Hard for me to see 2022 as “a better year for TIPS,” unless you have never owned them before. In fact, 2022 was an awful year for TIPS holders (like me) who thought TIPS would protect them from inflation. I have to ask myself: Is a real rate of 1.5% going forward really going to be of much solace when one can still lose something like 12% nominal and 19% real if we have a year of 7% inflation or more in the future? I’d be curious how you feel about this? Have your views changed at all?

BondGuy, I own a lot of TIPS from the past and I am perfectly happy having 7%+ inflation accruals annually over the last two years. If you are a TIPS trader, 2022 was a lousy year. But if you are holding to maturity, you can psychologically distance yourself from “market value.” Also, I wasn’t buying TIPS in the period from 2019 to mid-2022, so I didn’t buy any with deeply negative yields.

A nice trick is to pencil in the inflation-adjusted principal value of each bond next to the market value on your brokerage statement. I care more what the Treasury thinks each is worth than what the market does. They’ll be the one paying me at maturity.

Hi David,

Do you care to wager if the next I bond Fixed rate will stay the same at .4%, go lower, or higher? Or is it literally a 33.3% odds for each scenario at this point?

Too early to guess. If the 10-year real yield holds above 1.50%, then the chance is good.

Miss, for those of us holding 0% fixed rate I Bonds, that’s the big I Bond question, isn’t it? And the answer is it’s a mystery. Why? There’s no apparent reason.

For 2023, I’d like to buy another I Bond. How to do it seems like a multiple choice question. Do I:

A. buy in mid-January after the CPI report so I know half of the next inflation rate and capture the current 6.89% composite rate inclusive of the 0.4% fixed rate?

B. wait until mid-April when I will know the exact inflation rate and can still capture the current 6.89% composite rare inclusive of the 0.4% fixed rate?

C. wait until May 1 and likely get a lower composite rate due to lower inflation and risk losing the 0.4% fixed rate in the hopes the mystery fixed rate will be higher than 0.4%

OR

D. Forgo a purchase, exchange Gift I Bonds with my spouse to reach my 2023 limit, and then buy another Gift I Bond for my spouse, and her for me, using Option B.

I’m going with Option D. In the meantime, I have the money for the Gift I Bonds in a T-Bill that will come due before mid-April.

Hi David, I am looking forward to your 2023 I-Bond Buying Guide. Thanks!